Market Data

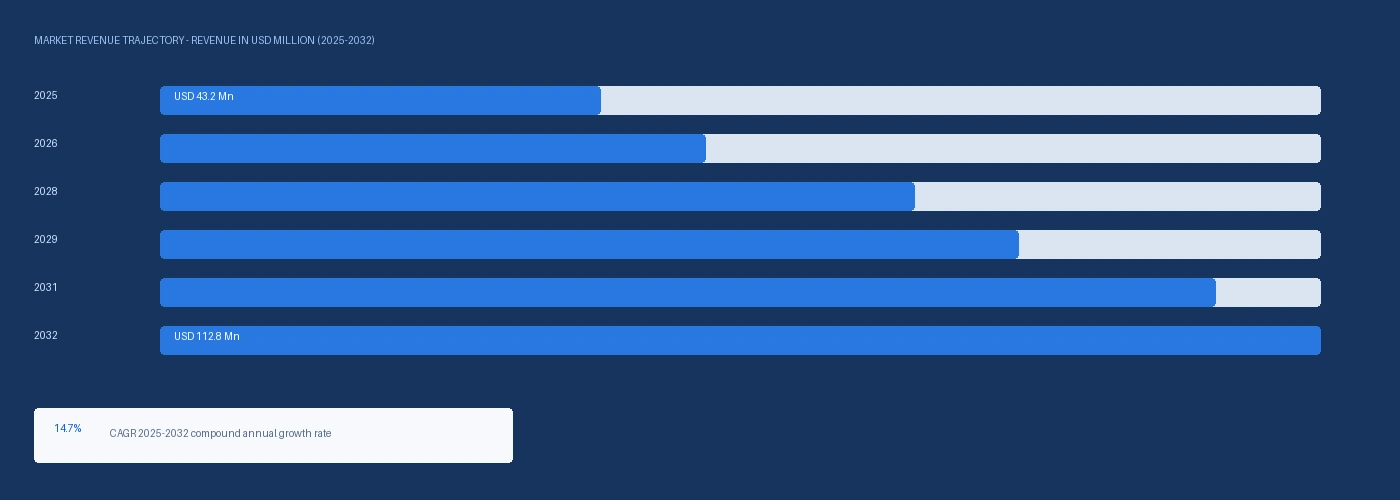

The global 2-ethylhexanol market size was USD 5.12 Billion in 2025 and is expected to register a revenue CAGR of 7.9% during the forecast period. Market revenue growth is supported by the regulatory-mandated migration away from DEHP plasticizer across European and North American PVC applications driving DOTP and DINCH demand that consumes 2-ethylhexanol as a primary feedstock alcohol, expanding 2-ethylhexyl acrylate demand from pressure-sensitive adhesive and coating formulations growing with e-commerce packaging and construction sealant consumption, and ISO-grade diesel fuel antiwear additive applications consuming 2-ethylhexyl nitrate as a cetane improver at above-3% annual volume growth. Global oxo-process 2-ethylhexanol nameplate capacity reached approximately 9.1 million metric tonnes per year in 2025, with BASF SE at Ludwigshafen and Schwarzheide, Dow Chemical at Terneuzen in the Netherlands, and LG Chem at Daesan accounting for the three largest single-site 2-EH production volumes globally. The European Chemicals Agency SVHC restriction on DEHP phthalate plasticizer that entered full force in January 2025 for articles containing greater than 0.1% DEHP concentration has accelerated PVC compounder transitions to DOTP and DINCH alternatives, with Evonik Industries and BASF Care Chemicals each disclosing double-digit DOTP and DINCH volume growth through 2024 driven by European flooring, cable sheathing, and automotive PVC specification changeovers. The IEA Global Buildings and Construction report confirmed the construction sector at approximately 35% of global PVC consumption in 2025, sustaining the primary structural demand signal for plasticized PVC that anchors 2-EH consumption independent of automotive or packaging cycle volatility. For instance, in March 2025, BASF SE, Germany, announced a targeted debottlenecking of its 2-ethylhexanol oxo-synthesis unit at Ludwigshafen, increasing output capacity by approximately 8% through Rh-catalyst optimisation and targeting the growing DOTP and DINCH plasticizer customer base transitioning away from DEHP under ECHA SVHC enforcement, the first disclosed European 2-EH capacity expansion in over four years. These are some of the key factors driving revenue growth of the market.

Propylene feedstock costs at oxo-process 2-EH producers in Europe are elevated in Q2 2026 as Hormuz-driven naphtha cost increases flow through to propylene co-production economics at Ruhr Valley and Rhine corridor naphtha crackers, with BASF and Dow reporting propylene procurement costs approximately USD 60 to USD 100 per metric tonne above the 2024 baseline. Chinese 2-EH capacity from SINOPEC Yangzi Petrochemical and PetroChina Lanzhou Petrochemical reached a combined estimated 2.8 million metric tonnes per year of nameplate in 2025 per CPCIF data, creating a structural export surplus of approximately 600,000 to 800,000 metric tonnes per year at current Chinese domestic plasticizer and acrylate consumption of approximately 2.1 million metric tonnes per year, which has entered Asian export markets at USD 1,140 per metric tonne in Q2 2026 and compressed Asian commodity pricing below the cash cost floor of older Western acetaldehyde-route 2-EH producers. Dow Chemical disclosed in its Q4 2024 earnings that 2-ethylhexyl acrylate volumes at its Terneuzen acrylic acid and ester complex had grown approximately 11% in 2024 on pressure-sensitive adhesive demand from e-commerce protective packaging converters in Germany, France, and the Netherlands, confirming the acrylate pathway as the fastest-expanding European 2-EH derivative application and providing a structural revenue signal that is independent of the regulatory DEHP migration timeline.

However, propylene feedstock price volatility represents the most structurally acute production cost risk for oxo-process 2-EH producers, with European propylene contract prices ranging from approximately USD 820 to USD 1,380 per metric tonne between 2022 and 2025 per American Chemistry Council reference data, creating production cost uncertainty of approximately USD 120 to USD 200 per metric tonne of 2-EH output that is difficult to hedge in long-term fixed-price DOTP supply agreements. Chinese oxo-process overcapacity at approximately 600,000 to 800,000 metric tonnes per year of structural export surplus is suppressing Asian commodity 2-EH monomer pricing at USD 1,140 per metric tonne in Q2 2026, below the cash production cost of older Western acetaldehyde condensation route facilities, accelerating Western capacity rationalisation in commodity-grade applications while forcing migration toward higher-margin DOTP, acrylate, and specialty ester derivatives. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has added approximately USD 60 to USD 100 per metric tonne to propylene procurement costs at European naphtha cracker-integrated 2-EH producers, compressing margins at non-integrated oxo-process operators caught between elevated feedstock costs and Asian export price competition. These factors substantially limit 2-ethylhexanol market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

The European Chemicals Agency SVHC restriction on DEHP under REACH entered full enforcement force in January 2025 for articles containing greater than 0.1% DEHP by weight, mandating PVC compounder transitions to non-phthalate or alternative phthalate plasticizers including DOTP and DINCH in flooring, cable sheathing, automotive interior PVC, medical-grade tubing, and children's toy categories. DOTP production requires two moles of 2-ethylhexanol per mole of terephthalate ester, making 2-EH the volume-critical feedstock alcohol for the DOTP transition in a ratio of approximately 0.73 tonnes of 2-EH per tonne of DOTP produced. Evonik Industries disclosed double-digit DOTP volume growth in its specialty additives division through 2024, citing European flooring and automotive PVC specification changeovers from DEHP compounds as the primary volume driver. BASF SE's Care Chemicals division confirmed equivalent DINCH volume growth through the same period, with DINCH consuming 2-EH as a precursor alcohol and carrying a per-tonne price of approximately USD 2,240 per metric tonne in Europe in Q2 2026, approximately 45% above DOTP at USD 1,540 per metric tonne, sustaining the margin rationale for 2-EH producers to supply the DINCH pathway. The US Consumer Product Safety Commission issued parallel DEHP concentration limits for children's products in January 2025, effectively aligning North American toy and childcare article PVC specifications with European ECHA requirements and extending the DOTP demand transition to North American PVC compounders including Mexichem Amanco and PolyOne who supply the US retail and mass market childcare categories. The American Chemistry Council confirmed that non-phthalate and alternative plasticizer volumes in US flexible PVC compounding grew approximately 9% in 2024, the highest single-year growth rate in over a decade, with DOTP accounting for approximately 65% of that alternative plasticizer volume growth and consuming 2-EH from domestic Dow and Eastman Chemical production as well as Korean LG Chem import sources. 2-Ethylhexyl Acrylate Demand from Pressure-Sensitive Adhesives and Architectural Coatings 2-Ethylhexyl acrylate, produced from the esterification of acrylic acid with 2-EH, is a primary monomer in pressure-sensitive adhesive emulsion polymers for label stock, tape, and e-commerce protective packaging, and in architectural exterior coating latex formulations where its long alkyl chain provides low-temperature flexibility and water resistance. Global e-commerce packaging demand grew approximately 14% by volume in 2024 per the International Corrugated Case Association, with pressure-sensitive label and tape consumption directly linked to parcel shipment volume growth. Each tonne of 2-ethylhexyl acrylate monomer consumes approximately 0.58 tonnes of 2-EH feedstock at current esterification yields, translating e-commerce packaging volume growth directly into 2-EH demand at BASF Terneuzen and Dow Zwijndrecht acrylic ester production facilities. Architectural coating demand in Asia-Pacific sustained above-5% volume growth through 2024 per IEA Buildings sector data, with Chinese acrylic emulsion coating production consuming approximately 420,000 to 500,000 metric tonnes per year of 2-ethylhexyl acrylate and representing the largest single national acrylate demand channel globally.

European propylene contract prices ranged from approximately USD 820 to USD 1,380 per metric tonne across the 2022 to 2025 period per American Chemistry Council co-product pricing data, creating production cost uncertainty at oxo-process 2-EH facilities that makes long-term fixed-price DOTP and acrylate supply agreements commercially difficult beyond six-month forward price visibility. The BASF Ludwigshafen and Dow Terneuzen oxo-synthesis units consume propylene at approximately 0.62 to 0.65 tonnes of propylene per tonne of 2-EH produced, meaning a USD 200 per metric tonne propylene price swing creates a USD 124 to USD 130 per metric tonne 2-EH production cost impact that cannot be fully recovered in commodity-grade sales contracts. Chinese nameplate 2-EH oxo-process capacity at approximately 2.8 million metric tonnes per year against domestic consumption of approximately 2.1 million metric tonnes creates a structural export surplus of approximately 600,000 to 800,000 metric tonnes per year, holding Asian commodity 2-EH spot prices at USD 1,140 per metric tonne in Q2 2026, below the estimated cash production cost of USD 1,280 to USD 1,380 per metric tonne at older Western acetaldehyde condensation route facilities and accelerating their closure or conversion. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated propylene procurement costs at European naphtha cracker-integrated 2-EH producers by approximately USD 60 to USD 100 per metric tonne above the 2024 baseline from Hormuz-driven naphtha cost increases, compressing operating margins at non-integrated European 2-EH producers who cannot recover the full feedstock cost increment in DOTP or acrylate contract pricing due to competition from Asian commodity 2-EH export pricing. Formosa Plastics disclosed in Q2 2024 that it was evaluating shutdown of its US acetaldehyde-route 2-EH facility at Point Comfort, Texas, the first publicly disclosed US 2-EH capacity rationalisation evaluation in over a decade, citing the persistent cost disadvantage of acetaldehyde chemistry versus oxo-synthesis routes from propylene as the primary economic driver. These factors substantially limit 2-ethylhexanol market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Grade | Plasticizer Grade, Industrial Grade, Pharmaceutical Grade | Plasticizer Grade |

| Application | Plasticizers (DOTP, DEHP, DINCH), Acrylates and Esters, Solvents, Surfactants, Lubricant Additives | Plasticizers (DOTP, DEHP, DINCH) |

| End Use | PVC and Building Materials, Automotive, Personal Care, Coatings and Adhesives, Industrial | PVC and Building Materials |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Plasticizer Grade segment is expected to account for a significantly large revenue share in the global 2-ethylhexanol market during the forecast period.

This report evaluates grade across Plasticizer Grade, Industrial Grade, Pharmaceutical Grade, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Plasticizers (DOTP, DEHP, DINCH), Acrylates and Esters, Solvents, Surfactants, Lubricant Additives, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across PVC and Building Materials, Automotive, Personal Care, Coatings and Adhesives, Industrial, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

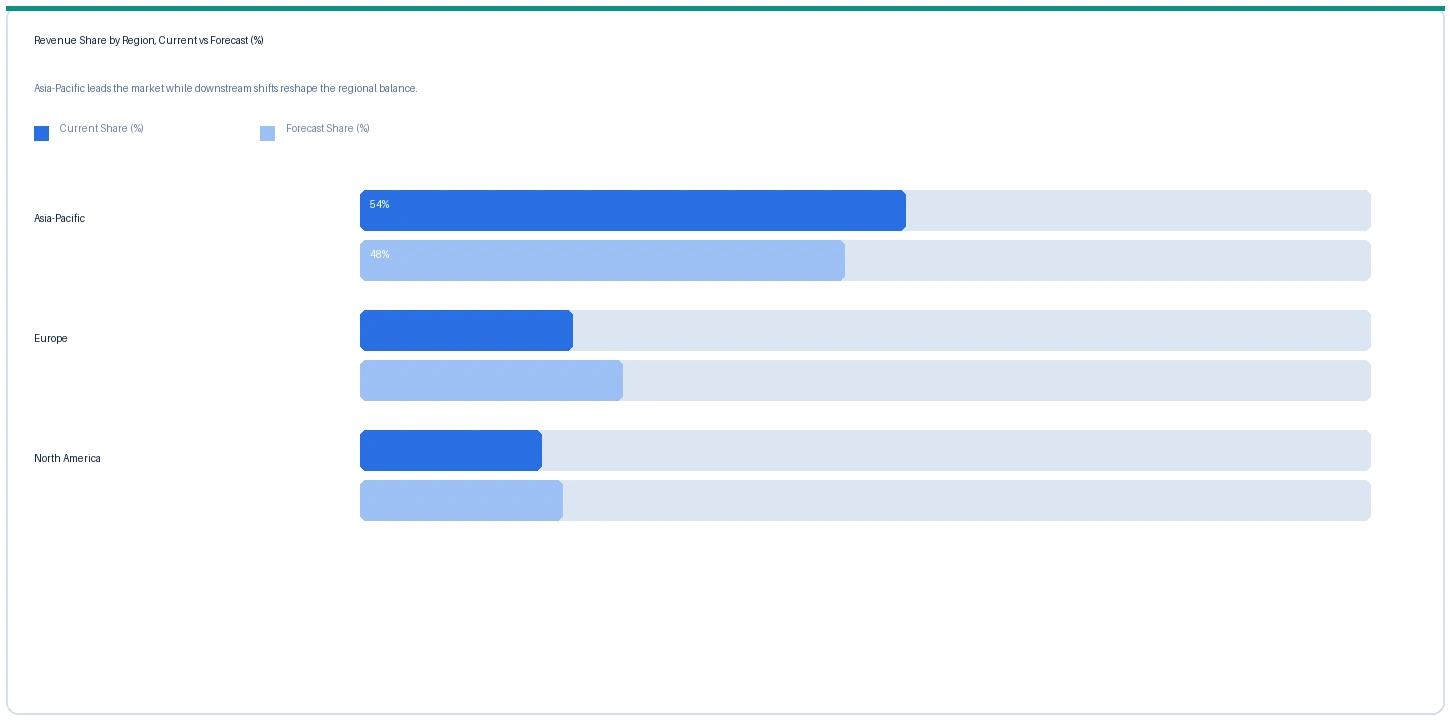

Asia-Pacific market accounted for largest revenue share over other regional markets in the global 2-ethylhexanol market in 2025. Based on regional analysis, the 2-ethylhexanol market in Asia-Pacific accounted for largest revenue share in 2025. China alone accounts for approximately 65% of global 2-EH nameplate oxo-process capacity at approximately 2.8 million metric tonnes per year, with SINOPEC Yangzi Petrochemical at Nanjing, PetroChina Lanzhou Petrochemical, and Shandong Hongye Chemical among the largest single-site producers. Chinese domestic DOTP consumption at approximately 900,000 to 1.1 million metric tonnes per year, driven by PVC flooring and cable sheathing applications for domestic construction, absorbs the majority of domestic 2-EH output in the plasticizer pathway, with the 600,000 to 800,000 metric tonne structural export surplus entering Southeast Asian and Indian spot markets at prices that compress regional commodity pricing. Indian 2-EH demand from domestic PVC cable and pipe compounders including Supreme Industries and Finolex Cables is growing at approximately 8% per year per Indian Petrochemicals industry data, primarily sourced through Chinese and South Korean imports given the absence of domestic oxo-process 2-EH production. South Korean LG Chem at Daesan operates Asia's most integrated non-Chinese oxo-process 2-EH facility, supplying domestic DOTP producers and exporting plasticizer-grade 2-EH to Japanese and Southeast Asian customers under term agreements.

The market in Europe is expected to register the second largest revenue share in the global 2-ethylhexanol market. BASF SE at Ludwigshafen and Schwarzheide and Dow Chemical at Terneuzen, Netherlands operate the primary European oxo-process 2-EH production facilities, with Verbund integration at BASF providing a structural cost and logistics advantage for downstream DOTP, DINCH, and acrylate ester production from internal 2-EH feedstock. European 2-EH contract pricing at USD 1,560 per metric tonne plasticizer grade in Q2 2026 carries a USD 420 per metric tonne premium above Asian commodity pricing, reflecting the elevated propylene feedstock costs from the Strait of Hormuz disruption and the tighter European supply balance from BASF's Q2 2026 prioritisation of DOTP and DINCH derivative production over commodity 2-EH monomer spot sales. The ECHA DEHP SVHC restriction enforcement from January 2025 has structurally increased European DOTP and DINCH demand above pre-restriction projections, with Evonik and BASF each running DOTP and DINCH production above 90% utilisation through 2024 and 2025 to serve PVC compounder transition programmes at Continental Bauelemente, Tarkett, and Prysmian Group cable manufacturing.

North America market is expected to register steady revenue growth in the global 2-ethylhexanol market during the forecast period. The market in North America is anchored in Eastman Chemical at Longview, Texas and Dow Chemical at Freeport, Texas as the primary US oxo-process 2-EH producers, with Eastman disclosing in its Q3 2024 earnings that its Texas 2-EH unit was operating at above-88% utilisation through 2024 on DOTP and 2-ethylhexyl acrylate demand. The US Consumer Product Safety Commission DEHP restriction for children's products effective January 2025 has aligned North American flexible PVC specification changeovers with European timelines, generating domestic DOTP demand growth of approximately 9% in 2024 per American Chemistry Council data. North American diesel cetane improver demand for 2-ethylhexyl nitrate from Innospec at Ellesmere Port UK and Afton Chemical in Richmond, Virginia provides a stable secondary demand channel for 2-EH at above-commodity margins, with the US Department of Energy confirming US diesel fuel consumption at approximately 1.4 billion barrels per day in 2024 and ultra-low sulfur diesel mandates sustaining cetane improver demand. The Inflation Reduction Act energy transition investment is sustaining construction activity in the US Southwest and Midwest, indirectly supporting PVC building materials demand that underpins 2-EH plasticizer consumption.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| 2-EH (Plasticizer Grade) | Europe | USD 1,560/MT | USD 1,390/MT | Rising | BASF / Dow ref |

| 2-EH (Plasticizer Grade) | North America | USD 1,480/MT | USD 1,320/MT | Rising | Eastman ref |

| 2-EH (Industrial Grade) | Asia-Pacific | USD 1,140/MT | USD 1,040/MT | Stable | SINOPEC ref |

| DOTP (auto PVC grade) | Europe | USD 1,540/MT | USD 1,380/MT | Rising | BASF Kollisolv ref |

| DINCH (food/med grade) | Europe | USD 2,240/MT | USD 2,020/MT | Rising | BASF specialty ref |

| Propylene (feedstock) | Europe | USD 1,060/MT | USD 920/MT | Rising | Cracker co-product ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty chemical trade publication monitoring. 2-Ethylhexanol is traded under monthly and quarterly term contracts referenced against regional propylene and propionaldehyde feedstock assessments. Prices vary by grade, application certification, contract volume, and regional supply balance.

European plasticizer-grade 2-EH prices rose approximately 12.2% from USD 1,390 per metric tonne in Q2 2025 to USD 1,560 per metric tonne in Q2 2026, driven by BASF Ludwigshafen debottlenecking output being absorbed by DOTP and DINCH derivative production rather than entering the commodity monomer market, and by propylene feedstock cost elevation of approximately USD 60 to USD 100 per metric tonne from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026. North American plasticizer-grade prices rose approximately 12.1% on equivalent propylene feedstock cost dynamics and DOTP demand growth from the US Consumer Product Safety Commission DEHP restriction. The Europe-Asia commodity 2-EH price differential widened from approximately USD 350 per metric tonne in Q2 2025 to approximately USD 420 per metric tonne in Q2 2026, reflecting diverging feedstock cost trajectories and the structural portfolio shift by European integrated producers toward DOTP and DINCH derivative value capture rather than commodity monomer spot sales. Asian industrial-grade 2-EH at USD 1,140 per metric tonne remains stable as Chinese overcapacity export volumes maintain the price floor at or below the cash cost of non-integrated Western acetaldehyde-route facilities. DINCH specialty grade at USD 2,240 per metric tonne in Europe rose approximately 10.9% against Q2 2025, sustaining a 45% premium above DOTP that reflects the pharmaceutical and food-contact PVC specification premium commanded by DINCH in medical tubing and food packaging applications.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 2-ethylhexanol market, the Hormuz disruption operates through the propylene feedstock chain that underpins oxo-synthesis 2-EH production in Europe. Naphtha costs at Rhine and Ruhr Valley crackers supplying propylene to BASF Ludwigshafen and Dow Terneuzen oxo-synthesis units are elevated by approximately USD 60 to USD 100 per metric tonne above the 2024 baseline from Hormuz-driven crude oil supply restriction and GCC naphtha export disruption, adding directly to 2-EH production cost and sustaining the Q2 2026 European price increases of approximately 12% against Q2 2025. US oxo-process 2-EH producers at Eastman Longview and Dow Freeport benefit from domestic propane and ethylene-propylene stream supply that partially insulates them from Hormuz naphtha economics, sustaining a US cost advantage relative to European producers and reinforcing the concentration of commodity 2-EH price-setting at Asian Chinese producers during the Hormuz closure period. Chinese 2-EH producers at SINOPEC Yangzi and PetroChina Lanzhou source propylene from domestic refineries with coal-to-chemicals and domestic crude inputs that are less directly exposed to GCC naphtha supply disruption, further entrenching their structural cost advantage over European non-integrated oxo-process facilities and accelerating Western capacity rationalisation in commodity-grade 2-EH applications.

Company Insights

The two key dominant companies in the 2-ethylhexanol market are BASF SE and Dow Chemical, recognised for their integrated oxo-process production scale spanning 2-EH synthesis through downstream DOTP, DINCH, and acrylate ester derivative production, their established supply relationships with major European PVC compounders and adhesive manufacturers, and their technical leadership in plasticizer-grade 2-EH documentation for ECHA and FDA regulatory qualification.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 5.12 Billion |

| Market Size 2032 | USD 8.74 Billion |

| CAGR | 7.9% |

| Units | Revenue in USD Billion |

| Segments Covered | By Grade, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, Netherlands, France, UK, China, Japan, South Korea, India, Brazil, Saudi Arabia, UAE |

| Companies Profiled | BASF SE, Dow Chemical, Eastman Chemical, LG Chem, SINOPEC Yangzi, PetroChina Lanzhou, Evonik Industries, Formosa Plastics, Shandong Hongye, Oxea GmbH, Mitsubishi Chemical |

| Key Data Sources | BASF and Dow investor presentations, ECHA SVHC restriction dossier January 2025, American Chemistry Council US chemical production data, CPCIF Chinese 2-EH production statistics, European Council of Vinyl Manufacturers PVC consumption data, IEA Buildings and Construction report 2025, US Consumer Product Safety Commission DEHP restriction ruling, 17 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | |

| Published | |

| SKU |

Scope & Methodology

Primary Research

Secondary Research