Market Data

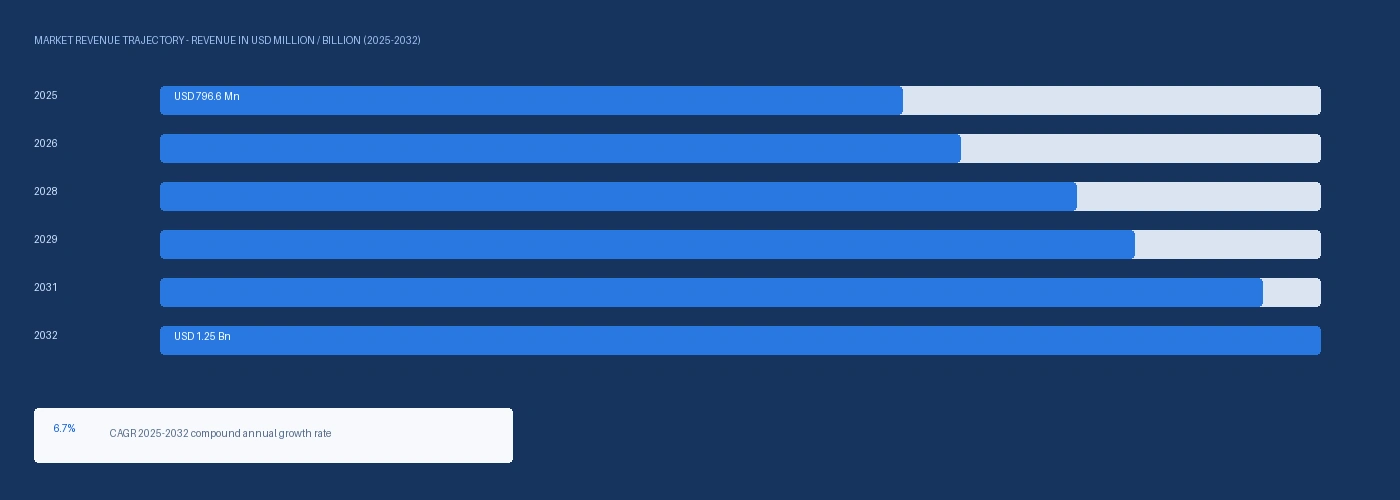

The global 1 decene market size was USD 796.6 Million in 2025 and is expected to register a revenue CAGR of 6.7% during the forecast period. Market revenue growth is supported by EV thermal management PAO fluid demand driving 1-decene allocation toward PAO production at ExxonMobil Chemical Baytown and Ineos Oligomers Hull, above-trend LLDPE film demand from e-commerce flexible packaging and stretch wrap gauge-reduction programmes, and the structural inability of SHOP process co-production economics to expand C10 decene supply selectively without also adding C4 through C20 LAO volumes. ExxonMobil Chemical confirmed in its Q2 2025 product strategy briefing that it was shifting 1-decene allocation toward its internal PAO base oil production at Baytown, Texas in response to EV OEM thermal management fluid specifications from five European automotive manufacturers for 2026 to 2028 platform launches, the first explicit allocation shift disclosure from a major SHOP operator. PAO 4 and PAO 6 base oils produced from 1-decene oligomerisation were indicatively priced at USD 3,840 per metric tonne globally in Q2 2026, against PAO-grade 1-decene at USD 1,840 per metric tonne in North America, giving a PAO conversion margin of approximately USD 700 to USD 1,100 per tonne of 1-decene consumed that makes PAO applications economically rational to prioritise over LLDPE comonomer at USD 1,340 per metric tonne. The IEA confirmed in its Global EV Outlook 2025 that global EV production would reach approximately 35 million units per year by 2030, each requiring approximately 4 to 8 litres of PAO-based thermal management fluid at first fill, implying incremental PAO demand from EV thermal management approaching 200,000 to 280,000 metric tonnes per year by 2030 relative to the 2024 base. Global LAO nameplate capacity from SHOP technology reached approximately 6.2 million metric tonnes per year in 2025, with ExxonMobil Chemical at Baytown, Texas and Chevron Phillips Chemical at Cedar Bayou, Texas collectively accounting for approximately 40% of global SHOP-derived C10 1-decene supply. For instance, in Q2 2025, ExxonMobil Chemical, United States, confirmed an increase in 1-decene allocation toward its internal PAO base oil production at Baytown, Texas, citing growing demand from automotive OEM EV thermal management fluid specifications as the primary reason for the allocation shift away from LLDPE comonomer applications at the same facility. These are some of the key factors driving revenue growth of the market.

PAO-grade 1-decene prices diverged from LLDPE comonomer-grade pricing in 2025 and 2026, with the PAO-to-LLDPE grade premium widening from approximately USD 420 per metric tonne in Q2 2025 to approximately USD 500 per metric tonne in Q2 2026 in North American markets, reflecting the ExxonMobil allocation shift confirmed in Q2 2025 and the Ineos Oligomers Hull Q4 2024 disclosure of 14% PAO demand growth in 2024 on EV drivetrain and industrial gear oil applications. Chevron Phillips Chemical announced a 6% SHOP facility debottlenecking at Cedar Bayou in March 2025, the first US SHOP capacity expansion in over five years, adding an estimated 12,000 to 18,000 metric tonnes per year of incremental C10 decene supply targeted at the LLDPE comonomer and PAO markets. Sinopec commissioned the C10 fractionation unit at its Zhejiang SHOP-equivalent LAO plant in Q3 2024, adding approximately 35,000 to 45,000 metric tonnes per year of domestic Chinese polymer-grade 1-decene and reducing Chinese LLDPE manufacturer dependence on Western imports, creating downward pricing pressure in Asian LLDPE comonomer markets while North American PAO-grade pricing rises.

However, 1-decene supply is structurally constrained by the co-production distribution of the SHOP process, which produces 1-decene alongside C4 through C20 LAO chain lengths simultaneously, meaning that any increase in PAO-grade C10 demand allocation at integrated operators reduces LLDPE comonomer availability from the same production run without offsetting capacity additions in the C4 through C8 LAO segments. Chinese SHOP-equivalent LAO producers including Sinopec and CNOOC have added domestic C10 1-decene supply that is reducing Chinese LLDPE dependence on Western imports and creating a downward pricing reference for LLDPE comonomer-grade 1-decene in Asian markets. These factors substantially limit 1 decene market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EV drivetrains require thermal management fluids with fundamentally different performance specifications than conventional ICE engine oils: battery packs, motor inverters, and gear reduction units operating across wider temperature ranges require PAO 4 and PAO 6 base oil fluids for battery cooling, motor lubrication, and gear unit servicing that provide electrical insulation resistance, low pour point, high viscosity index, and compatibility with the additive systems used in sealed EV drivetrain applications. ExxonMobil commercially launched Mobil EV Fluid 500 and 600 grades based on PAO 4 and PAO 6 from 1-decene in January 2025 with OEM specifications confirmed from five European automotive manufacturers for 2026 to 2028 platform launches. Each tonne of PAO 4 produced from 1-decene consumes approximately 3 to 4 tonnes of 1-decene feedstock, and PAO is sold at USD 3,840 per metric tonne versus LLDPE comonomer at USD 1,340 per metric tonne in Asia-Pacific, making PAO applications the value-maximising destination for each tonne of C10 1-decene allocated. Ineos Oligomers disclosed in its Q4 2024 annual commercial update that PAO demand from European industrial gear oil and EV drivetrain fluid applications had grown approximately 14% in 2024, the highest single-year PAO demand growth rate at Ineos since 2015. Wind turbine gear oil applications for PAO 100 and PAO 150 grades represent a second structural growth channel for 1-decene, with the Global Wind Energy Council confirming approximately 117 gigawatts of global wind turbine installation in 2024. Each large onshore turbine requires approximately 400 to 800 litres of gear oil at first fill and periodic top-up maintenance, and offshore turbines require 1,000 to 2,000 litres, with PAO-based grades specified by turbine manufacturers including Vestas, Siemens Gamesa, and GE Vernova for extended drain intervals and cold-temperature performance requirements. Kluber Lubrication, Shell Lubricants, and Fuchs Lubricants are among the wind turbine gear oil formulators specifying PAO grades from ExxonMobil and Ineos Oligomers as their primary base stock, creating a demand anchor that grows with each annual wind installation cycle. LLDPE Film Comonomer Demand from E-Commerce and mLLDPE Gauge Reduction C10 1-decene as a comonomer in LLDPE and mLLDPE polyethylene film provides superior puncture resistance and heat seal performance relative to C6 or C8 comonomers, making C10 LLDPE the preferred substrate for stretch wrap, heavy-duty bags, and e-commerce protective packaging applications. The US Department of Commerce reported e-commerce at approximately 16% of total US retail sales in 2024, with the e-commerce packaging market demanding above-average performance LLDPE that favours C10 comonomer grades. Berry Global disclosed in its Q1 2026 sustainability report that approximately 35% of its North American stretch film capacity had converted to mLLDPE C10 grades, confirming that the mLLDPE gauge reduction trend documented in ExxonMobil Chemical Exceed product line disclosures is a commercially motivated conversion at major packaging converters rather than a marginal niche trend.

The SHOP process produces 1-decene as one component of a C4-C20 LAO distribution, meaning that PAO demand growth in the C10 segment does not trigger targeted capacity additions without simultaneously adding surplus C4 through C8 and C12 through C20 volumes. ExxonMobil Chemical's Q2 2025 PAO allocation shift disclosure confirms that the constraint is already operating: routing more C10 to PAO removes it from LLDPE comonomer availability at the same facility. Chinese LAO producers including Sinopec at Zhejiang and CNOOC at Guangdong have added SHOP-equivalent domestic C10 supply at an estimated combined 35,000 to 80,000 metric tonnes per year of C10 fraction capacity, creating an Asian spot price reference for LLDPE comonomer-grade 1-decene below European and North American SHOP-derived pricing and compressing the margin available to Western producers in commodity comonomer applications. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated ethylene feedstock costs at European SHOP operators including Ineos Oligomers Hull through naphtha cracker cost elevation, supporting European 1-decene price premiums of approximately USD 120 per metric tonne above North American levels in Q2 2026 versus approximately USD 90 per metric tonne in Q2 2025. These factors substantially limit 1 decene market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Grade | Polymer Grade, Chemical Grade | Polymer Grade |

| Production Route | SHOP Ethylene Oligomerisation, Fischer-Tropsch Derived, On-Purpose Routes | SHOP Ethylene Oligomerisation |

| Application | PAO Synthetic Lubricants, LLDPE Comonomer, Surfactant Alcohols, Drilling Fluids | PAO Synthetic Lubricants |

| End Use | Automotive Lubricants, Packaging Films, Oil and Gas, Industrial Chemicals | Automotive Lubricants |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Polymer Grade segment is expected to account for a significantly large revenue share in the global 1 decene market during the forecast period.

This report evaluates grade across Polymer Grade, Chemical Grade for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates production route across SHOP Ethylene Oligomerisation, Fischer-Tropsch Derived, On-Purpose Routes for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across PAO Synthetic Lubricants, LLDPE Comonomer, Surfactant Alcohols, Drilling Fluids for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive Lubricants, Packaging Films, Oil and Gas, Industrial Chemicals for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

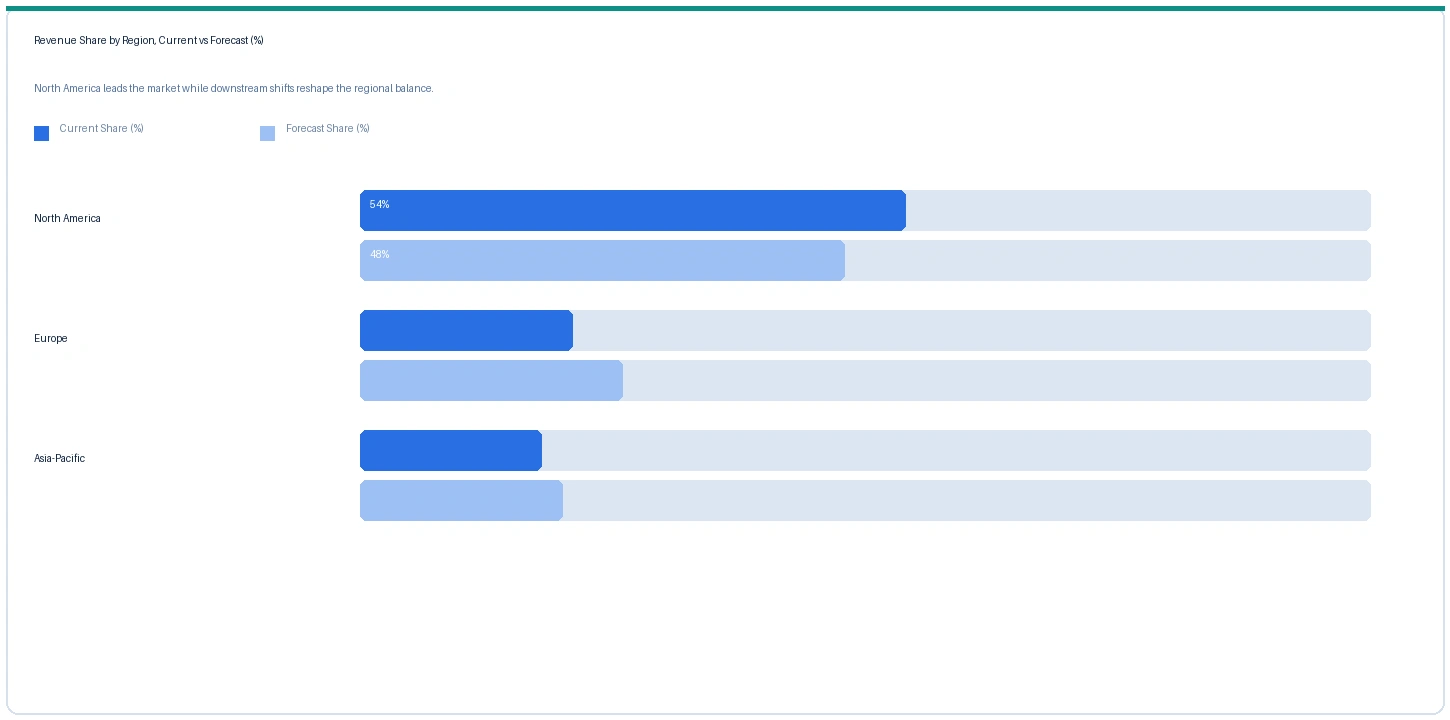

North America market accounted for largest revenue share over other regional markets in the global 1 decene market in 2025. Based on regional analysis, the 1 decene market in North America accounted for largest revenue share in 2025. ExxonMobil Chemical at Baytown, Texas and Chevron Phillips Chemical at Cedar Bayou, Texas collectively account for approximately 40% of global SHOP-derived C10 1-decene supply, with ExxonMobil's integration through PAO base oil synthesis and finished Mobil-branded lubricant formulation giving it end-to-end 1-decene-to-EV-fluid value chain control. The Q2 2025 ExxonMobil allocation shift disclosure, the January 2025 Mobil EV Fluid commercial launch with five European OEM specifications, and the March 2025 Chevron Phillips Cedar Bayou debottlenecking collectively confirm that North American 1-decene supply is being actively restructured around EV and PAO demand priorities. US domestic butane-based ethylene supply for SHOP operations at Baytown and Cedar Bayou provides partial insulation from Hormuz crude oil supply disruption relative to European naphtha-based SHOP operators.

The market in Europe is expected to register the second largest revenue share. Ineos Oligomers at Hull, United Kingdom operates SHOP technology producing 1-decene for European PAO base oil producers and LLDPE film manufacturers, with European PAO demand from EV drivetrain applications growing approximately 14% in 2024 per Ineos Q4 2024 disclosure. European 1-decene prices at USD 1,960 per metric tonne PAO grade in Q2 2026 carry a USD 120 per metric tonne premium above North American levels, reflecting elevated European ethylene feedstock costs from Hormuz-driven naphtha price increases at European crackers supplying Ineos Oligomers Hull. Kluber Lubrication, Shell Lubricants, and Fuchs Lubricants source PAO grades from Ineos and ExxonMobil for European EV drivetrain fluid and wind turbine gear oil formulations.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global 1 decene market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period. Sinopec at Zhejiang and CNOOC at Guangdong commissioned SHOP-equivalent C10 fraction capacity adding an estimated combined 35,000 to 80,000 metric tonnes per year of domestic Chinese polymer-grade 1-decene, reducing Chinese LLDPE producer dependence on Western imports and creating an Asian commodity LLDPE comonomer reference price at USD 1,140 per metric tonne in Q2 2026, approximately USD 200 per metric tonne below North American LLDPE comonomer pricing. Japanese PAO producers including Nippon Oil and South Korean SK Lubricants are sourcing 1-decene from ExxonMobil and Ineos for PAO production, with the IEA confirming Asia-Pacific accounted for approximately 55% of global EV production in 2024 driving PAO thermal management fluid demand from BYD, SAIC, and Toyota Lexus platform programmes.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| 1-Decene (PAO grade) | North America | USD 1,840/MT | USD 1,680/MT | Rising | ExxonMobil ref |

| 1-Decene (PAO grade) | Europe | USD 1,960/MT | USD 1,780/MT | Rising | Ineos Oligomers ref |

| 1-Decene (LLDPE comonomer) | North America | USD 1,340/MT | USD 1,220/MT | Rising | Chevron Phillips ref |

| 1-Decene (LLDPE comonomer) | Asia-Pacific | USD 1,140/MT | USD 1,060/MT | Stable | Chinese SHOP ref |

| PAO 4 Base Oil | Global | USD 3,840/MT | USD 3,540/MT | Rising | EV fluid benchmark |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty chemical trade publication monitoring. 1-Decene is traded under term and spot contracts. Prices vary by grade, application, production route, and regional supply balance.

PAO-grade 1-decene prices rose approximately 9.5% in North America and 10.1% in Europe against Q2 2025 in Q2 2026, driven by the ExxonMobil allocation shift toward PAO production removing C10 from LLDPE comonomer availability and by Ineos Hull's Q4 2024 disclosed 14% PAO demand growth tightening European PAO-grade supply. The PAO-to-LLDPE comonomer grade premium widened from approximately USD 420 per metric tonne in Q2 2025 to approximately USD 500 per metric tonne in Q2 2026 in North American markets, confirming that the PAO allocation priority is generating a structural pricing divergence between application segments sourcing from the same SHOP production. LLDPE comonomer-grade North American prices rose 9.8% to USD 1,340 per metric tonne in Q2 2026 despite being the lower-priority SHOP allocation segment, reflecting tighter comonomer availability as PAO applications absorb more of the SHOP C10 output. Asian LLDPE comonomer pricing is stable at USD 1,140 per metric tonne as Chinese domestic supply additions from Sinopec Zhejiang offset regional demand growth. PAO 4 base oil rose 8.5% to USD 3,840 per metric tonne globally on EV OEM fluid specifications creating committed volume demand at above-commodity pricing structures.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 1 decene market, the Hormuz disruption operates through ethylene feedstock costs at SHOP process operators in Europe. Ineos Oligomers at Hull sources ethylene from naphtha crackers with naphtha procured from North Sea and Mediterranean routes that are partially insulated from Hormuz but are affected by global crude oil price elevation from the disruption. The approximately USD 120 per metric tonne Europe-North America PAO-grade 1-decene price differential in Q2 2026, widened from approximately USD 90 per metric tonne in Q2 2025, partially reflects this Hormuz-driven European ethylene cost elevation. US SHOP operators at ExxonMobil Baytown and Chevron Phillips Cedar Bayou benefit from domestic ethane-based ethylene supply that is more insulated from Hormuz naphtha economics, sustaining the US cost advantage and supporting the concentration of PAO-grade 1-decene allocation decisions at US integrated operators rather than European SHOP producers in the current Hormuz disruption environment.

Company Insights

The two key dominant companies in the 1 decene market are ExxonMobil Chemical and Ineos Oligomers, recognised for their integrated SHOP technology operations producing 1-decene for both PAO base oil and LLDPE comonomer applications, their established OEM supply relationships in automotive lubricants and packaging films, and their leadership in EV thermal management PAO fluid development that is defining the new premium demand channel for 1-decene.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 796.6 Million |

| Market Size 2032 | USD 1.25 Billion |

| CAGR | 6.7% |

| Units | Revenue in USD Million / Billion |

| Segments Covered | By Grade, By Production Route, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, UK, Germany, France, China, Japan, South Korea, Saudi Arabia, South Africa, Brazil |

| Companies Profiled | ExxonMobil Chemical, Ineos Oligomers, Chevron Phillips Chemical, Sasol, Sinopec, CNOOC, Mitsui Chemicals, SK Chemicals, Nippon Petrochemicals, LyondellBasell |

| Key Data Sources | IEA Global EV Outlook 2025, OICA vehicle production data, ExxonMobil Chemical Q2 2025 allocation shift disclosure, Ineos Oligomers Q4 2024 PAO demand growth disclosure, Chevron Phillips Chemical debottlenecking announcement, Global Wind Energy Council 2024 installation data, Berry Global Q1 2026 stretch film conversion data, 17 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 260 |

| Published | Q2 2026 |

| SKU | NXC-PC-008 |

Scope & Methodology

Primary Research

Secondary Research