Market Data

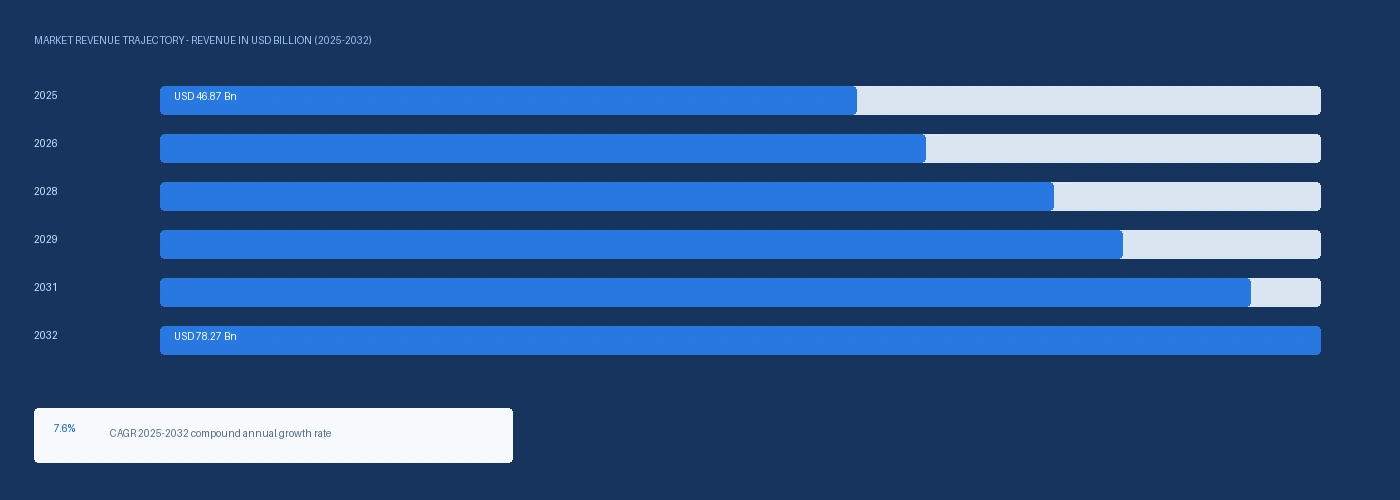

The global 1,3 butadiene market size was USD 46.87 Billion in 2025 and is expected to register a revenue CAGR of 7.6% during the forecast period. Market revenue growth is driven by sustained recovery in global automotive tire production, expanding synthetic rubber demand across emerging market vehicle fleets, and above-trend ABS resin consumption in consumer electronics and automotive interior trim. OICA confirmed global passenger vehicle production of approximately 92 million units in 2024, reinforcing tire compound demand that had been disrupted by semiconductor supply constraints in 2021 and 2022. The China Rubber Industry Association reported Chinese SBR production of approximately 1.8 million metric tonnes in 2024, with domestic butadiene consumption at Chinese integrated complexes running at above 90% of extraction capacity. The International Energy Agency confirmed global ethylene production capacity of approximately 230 million metric tonnes per year in its 2025 chemicals outlook, with C4 cracker co-production supplying the majority of polymer-grade butadiene globally. Demand from the ABS resin sector has remained above trend, with LG Chem and SABIC both reporting sustained ABS capacity utilisation above 85% through 2024 on the back of consumer electronics and electric vehicle interior component demand. Synthetic rubber demand in India is expanding in parallel, with Apollo Tyres, MRF, and CEAT each disclosing capital expenditure programmes targeting additional compounding capacity through 2027, requiring secured butadiene supply from domestic and import sources. For instance, in November 2024, Arlanxeo, Germany, announced a five-year polymer-grade butadiene supply agreement with Bridgestone Americas for feedstock to its Orange, Texas synthetic rubber facility, securing long-term supply at a volume commitment that underpins continued US production investment through 2029. These are some of the key factors driving revenue growth of the market.

China accounted for approximately 45% of global butadiene demand in 2024, with Sinopec, PetroChina, and Wanhua Chemical operating integrated naphtha cracker and C4 extraction complexes in Jilin, Shanghai, and Guangdong at combined polymer-grade butadiene output approaching 2.1 million metric tonnes per year. European supply tightened materially in Q4 2024 and into 2025 as LyondellBasell reduced throughput at its Wesseling, Germany complex to approximately 82% of nameplate capacity in response to compressed naphtha-ethylene margins, cutting C4 butadiene co-production at one of Western Europe's largest extraction units. The American Chemistry Council confirmed US butadiene demand at approximately 2.1 million metric tonnes in 2024, of which domestic cracker production supplied approximately 1.6 million metric tonnes, with the remaining 500,000 metric tonnes sourced from South Korean and European imports under quarterly term contracts. Wanhua Chemical reported its Yantai naphtha cracker operating at 94% utilisation across 2025, with polymer-grade butadiene output allocated primarily to internal ABS and specialty polymer production, reducing external spot availability and maintaining Asian polymer-grade pricing above Q1 2025 levels through the year.

However, butadiene pricing is structurally linked to naphtha cracker economics rather than direct downstream demand signals, meaning supply can tighten independently of tire or rubber demand when cracker operators reduce throughput to protect ethylene margins. The structural shift toward ethane cracking in North America has removed butadiene co-production capacity that naphtha crackers would have generated, with US ethane-based capacity additions since 2018 at ExxonMobil Corpus Christi, Dow Freeport, and Chevron Phillips Cedar Bayou contributing zero C4 butadiene co-production. Silica-reinforced tire compounds are gaining share against SBR in certain passenger car segments, reducing butadiene intensity per tyre unit and moderating the volume growth signal from OEM production data. These factors substantially limit 1,3 butadiene market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Global tire production has returned to above-2019 volume levels following the semiconductor supply chain recovery, with OICA confirming 92 million passenger vehicle units in 2024 and the China Rubber Industry Association reporting 980 million tyre units produced in China alone. Synthetic rubber demand per vehicle remains stable at approximately 15 to 20 kilograms of SBR and PBR equivalent for a standard passenger car tire set, translating the OEM production recovery directly into butadiene feedstock demand at Arlanxeo, Trinseo, and JSR Corporation synthetic rubber plants. Emerging market fleet expansion is adding incremental demand growth above the OEM cycle: the Society of Indian Automobile Manufacturers reported two-wheeler production exceeding 21 million units in fiscal year 2025, and Indian tire manufacturers including Apollo Tyres, MRF, and CEAT are each adding compounding capacity that requires additional butadiene feedstock supply secured under term contracts from South Korean and domestic Indian sources. The replacement tire market, which is driven by fleet size and average annual mileage rather than new vehicle production, grew at approximately 4.2% in 2024 across Asia-Pacific according to OICA fleet utilisation data, providing a demand floor independent of near-term OEM production cycle volatility. ABS resin demand accounted for approximately 12% to 14% of global butadiene consumption in 2024, with LG Chem, SABIC, and Toray among the largest producers maintaining above-85% utilisation on consumer electronics and EV interior trim demand. Styrene butadiene latex consumed approximately 8% to 10% of global supply, with paper coating and carpet backing applications in India, Vietnam, and Indonesia providing incremental demand at rates above GDP growth in those markets. The American Chemistry Council confirmed SB latex demand in US carpet applications under the EPA Safer Choice programme grew at approximately 3.8% in 2024, supported by residential construction recovery in the US Southeast. Supply Tightening from European Cracker Utilisation Reductions European butadiene supply tightened through 2024 and into 2025 as INEOS, LyondellBasell, and BASF SE reduced naphtha cracker throughput in response to compressed ethylene margins driven by Asian ethylene import competition. LyondellBasell disclosed cracker utilisation at Wesseling, Germany at approximately 82% of nameplate capacity in its Q4 2024 earnings, removing an estimated 60,000 to 80,000 metric tonnes of butadiene co-production from European annual supply relative to full-capacity operation. BASF SE disclosed a 9% year-on-year decline in butadiene extraction volumes at its Ludwigshafen Verbund complex in Q1 2025, consistent with its disclosed naphtha cracker throughput reduction. These supply reductions have sustained European polymer-grade butadiene contract prices at USD 1,440 per metric tonne in Q2 2026, a premium of approximately USD 120 per metric tonne above North American contract levels and USD 300 per metric tonne above Asian spot, as European synthetic rubber producers including Continental, Michelin, and Bridgestone Europe have absorbed the tighter supply through existing term contract inventory cover.

US ethane-based ethylene capacity additions since 2018 have added zero butadiene co-production to the North American supply base, because ethane crackers generate less than 2% C4 byproduct versus 8% to 12% for naphtha crackers. The American Chemistry Council estimated the resulting US butadiene domestic supply gap at approximately 500,000 metric tonnes per year in 2024, filled by South Korean and European imports under quarterly term contracts, exposing US synthetic rubber producers to import pricing risk when European supply tightens from cracker throughput reductions. In tire compounding, silica-reinforced rubber systems incorporating silica silane coupling agents have captured approximately 35% to 40% of passenger car high-performance tire compound specifications at Michelin and Continental Europe as of 2024, reducing the butadiene intensity per tyre unit at the premium end of the market and moderating the volume pull from OEM production data. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated naphtha feedstock costs at Asian cracker operators sourcing GCC naphtha through Hormuz transit routes, increasing butadiene co-production cost in Japan, South Korea, and Taiwan and flowing through to Asian polymer-grade contract pricing in Q2 2026. These factors substantially limit 1,3 butadiene market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Grade | Polymer Grade, Chemical Grade | Polymer Grade |

| Application | Synthetic Rubber (SBR, PBR), ABS Resin, SB Latex, Adiponitrile, MBS | Synthetic Rubber (SBR, PBR) |

| End Use | Automotive Tires, Footwear, Adhesives, Paper Backing, Industrial Hoses | Automotive Tires |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Polymer Grade segment is expected to account for a significantly large revenue share in the global 1,3 butadiene market during the forecast period.

This report evaluates grade across Polymer Grade, Chemical Grade for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Synthetic Rubber (SBR, PBR), ABS Resin, SB Latex, Adiponitrile, MBS for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive Tires, Footwear, Adhesives, Paper Backing, Industrial Hoses for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

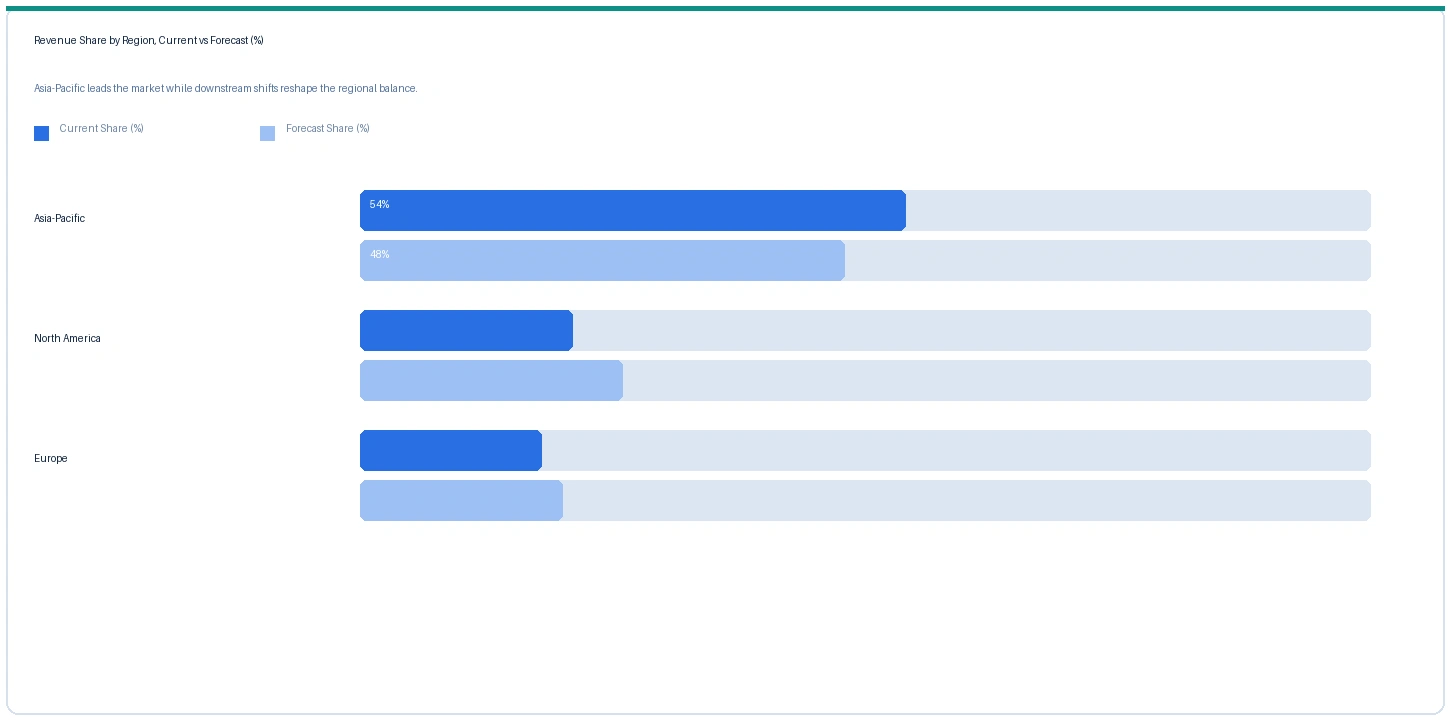

Asia-Pacific market accounted for largest revenue share over other regional markets in the global 1,3 butadiene market in 2025. Based on regional analysis, the 1,3 butadiene market in Asia-Pacific accounted for largest revenue share in 2025. China alone accounts for approximately 45% of global butadiene demand, supported by integrated C4 extraction capacity at Sinopec complexes in Jilin, Shanghai, and Guangdong producing a combined estimated 2.1 million metric tonnes per year of polymer-grade material, of which the majority is consumed internally by Sinopec SBR and ABS production at the same sites. South Korea contributes approximately 420,000 to 480,000 metric tonnes per year of butadiene extraction from LG Chem Daesan and SK Innovation crackers, with a proportion exported to Japan, Taiwan, and Southeast Asia under term contracts. The China Rubber Industry Association confirmed Chinese tire output of 980 million units in 2024, sustaining near-full utilisation at Chinese SBR and PBR plants that are the primary butadiene demand sink for domestic production.

North America market accounted for second largest revenue share in the global 1,3 butadiene market in 2025. The market in North America is expected to register the second largest revenue share in the global 1,3 butadiene market. The American Chemistry Council confirmed US butadiene demand at approximately 2.1 million metric tonnes in 2024, with domestic cracker production at ExxonMobil Baytown and LyondellBasell Houston supplying approximately 1.6 million metric tonnes and import contracts from South Korea and Europe filling the remaining 500,000 metric tonnes gap created by the US ethane cracking structural supply deficit. Arlanxeo Orange, Texas and Trinseo US operations are the primary domestic butadiene term contract buyers, with the Arlanxeo-Bridgestone Americas November 2024 five-year agreement representing the largest publicly disclosed US butadiene offtake commitment of the year.

Europe market is expected to register the third largest revenue share in the global 1,3 butadiene market during the forecast period. The market in Europe is navigating a structural supply tightening driven by naphtha cracker throughput reductions at INEOS, LyondellBasell, and BASF SE. Combined European polymer-grade butadiene production declined by an estimated 8% to 10% in 2024 relative to 2022 peak levels as cracker operators reduced utilisation to protect ethylene margins, tightening the European supply balance and sustaining contract prices at a USD 100 to USD 150 per metric tonne premium above North American levels. Automotive tire manufacturers Continental, Michelin, and Bridgestone Europe absorb the majority of European butadiene through existing term contracts, with spot market volumes limited and spot premiums above contract reference prices reaching 15% to 25% during supply tightening events.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Polymer Grade BD | Asia-Pacific | USD 1,320/MT | USD 1,180/MT | Rising | SBR contract ref |

| Polymer Grade BD | Europe | USD 1,440/MT | USD 1,310/MT | Rising | Continental/INEOS |

| Polymer Grade BD | North America | USD 1,390/MT | USD 1,260/MT | Rising | Arlanxeo ref |

| Chemical Grade BD | Asia-Pacific | USD 1,140/MT | USD 1,040/MT | Rising | ABS grade |

| Crude C4 Stream | Europe | USD 420/MT | USD 380/MT | Stable | Pre-extraction ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, trade publication monitoring, and buyer-side procurement interviews. 1,3-Butadiene is traded under term and spot contracts referenced against C4 extraction economics. Prices vary by grade, contract volume, regional logistics, and cracker utilisation conditions.

Polymer-grade butadiene prices are rising across all three major regions in Q2 2026, with the Europe-Asia spread at approximately USD 120 per metric tonne and the North America-Asia spread at approximately USD 70 per metric tonne reflecting regional supply tightness differentials. European prices are supported by reduced LyondellBasell Wesseling and BASF Ludwigshafen extraction volumes, with spot market premiums above contract reference rates reaching 18% to 22% in tight supply periods during Q1 2026. Asian prices are rising on elevated naphtha feedstock costs at Japanese, South Korean, and Taiwanese cracker operators following the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which has restricted GCC naphtha transit and added approximately USD 40 to USD 60 per metric tonne to Asian cracker feedstock cost relative to the 2025 baseline. North American polymer-grade pricing is rising at a slower rate than Europe and Asia, supported by domestic Arlanxeo and ExxonMobil contract structures that provide quarterly price stability relative to monthly European spot reference adjustments.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 1,3-butadiene market, the primary Hormuz impact is a USD 40 to USD 60 per metric tonne increase in naphtha procurement cost at Asian cracker operators in Japan, South Korea, and Taiwan who source GCC naphtha through Hormuz transit routes. This feedstock cost increase flows through to butadiene co-production economics within one to two cracker billing cycles, sustaining the Asian polymer-grade price increases documented in the price tracker. Secondary impacts include elevated European LNG energy costs at cracker sites in Germany and the Netherlands, adding approximately EUR 8 to EUR 14 per MWh to cracker energy cost relative to the 2024 baseline and reinforcing the utilisation reduction incentives that are tightening European butadiene supply. The policy response in both the US and EU is investment in domestic petrochemical feedstock security, which provides a medium-term capital expenditure tailwind for European naphtha cracker operators who maintain production through the current margin cycle.

Company Insights

The two key dominant companies in the 1,3 butadiene market are Arlanxeo and LG Chem, recognised for their integrated production capacity spanning butadiene extraction through synthetic rubber polymerisation, their long-term offtake relationships with global tire manufacturers, and their technical leadership in solution SBR and polybutadiene grades for high-performance tire compound applications.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 46.87 Billion |

| Market Size 2032 | USD 78.27 Billion |

| CAGR | 7.6% |

| Units | Revenue in USD Billion |

| Segments Covered | By Grade, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, China, Japan, South Korea, India, Brazil, Saudi Arabia, UAE |

| Companies Profiled | Arlanxeo, LG Chem, Sinopec, PetroChina, LyondellBasell, BASF SE, INEOS, Braskem, JSR Corporation, Zeon, Trinseo, ExxonMobil Chemical, SK Innovation, Wanhua Chemical |

| Key Data Sources | IEA Chemicals Outlook 2025, OICA vehicle production data, China Rubber Industry Association, American Chemistry Council, Arlanxeo and LG Chem annual reports, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 268 |

| Published | Q2 2026 |

| SKU | NXC-PC-001 |

Scope & Methodology

Primary Research

Secondary Research