Market Data

The global 1 hexene market size was USD 138.3 Million in 2025 and is expected to register a revenue CAGR of 5.2% during the forecast period. Market revenue growth is supported by metallocene LLDPE C6 comonomer adoption in US stretch film and flexible packaging that is converting conventional C4 comonomer LLDPE at above-plan rates, Chevron Phillips AlphaHex on-purpose 1-hexene capacity additions responding to C6 comonomer film demand growth, and agricultural film demand expansion in Mediterranean, North African, and Central Asian protected cultivation markets. Chevron Phillips Chemical Q4 2024 expansion of its AlphaHex selective trimerisation facility at Cedar Bayou, Texas added approximately 25,000 metric tonnes per year of on-purpose 1-hexene, the latest in a series of AlphaHex expansions collectively making Cedar Bayou the primary on-purpose 1-hexene production site globally. Berry Global disclosed in its Q1 2026 sustainability report that approximately 35% of its North American stretch film capacity had converted to mLLDPE C6 grades, driven by 15% to 25% gauge reduction material savings and improved load retention performance versus conventional LLDPE C4. The American Chemistry Council confirmed US LLDPE production consumed approximately 280,000 to 320,000 metric tonnes of 1-hexene annually in 2024, with C6 comonomer holding the largest share of the US LLDPE comonomer market. AlphaHex on-purpose 1-hexene at Cedar Bayou produces above 90% C6 1-hexene isomeric selectivity using selective ethylene trimerisation over chromium-phosphine catalyst systems, providing a narrower isomeric distribution valued in mLLDPE metallocene catalyst applications over the broader SHOP-derived 1-hexene distribution. ExxonMobil Chemical confirmed a 20% gauge reduction for its Exceed mLLDPE C6 stretch film application at a major US flexible packaging converter in March 2025, the first publicly documented gauge reduction claim for an ExxonMobil mLLDPE C6 stretch film application. For instance, in Q4 2024, Chevron Phillips Chemical, United States, announced a capacity expansion of its AlphaHex on-purpose 1-hexene facility at Cedar Bayou, Texas adding approximately 25,000 metric tonnes per year of selective 1-hexene production capacity, responding to growing US LLDPE film market demand for C6 comonomer grades in metallocene LLDPE stretch film and agricultural film applications. These are some of the key factors driving revenue growth of the market.

Polymer-grade 1-hexene from the AlphaHex on-purpose route at Chevron Phillips Cedar Bayou was indicatively priced at USD 1,240 per metric tonne in North America in Q2 2026, a USD 60 per metric tonne premium above SHOP-derived polymer-grade 1-hexene at USD 1,180 per metric tonne in North America, reflecting the higher isomeric selectivity value in mLLDPE applications. Both grades rose approximately 8.8% against Q2 2025 levels in North America, with the increase driven by the mLLDPE adoption-led demand pull from Berry Global's 35% capacity conversion and ExxonMobil Chemical Exceed mLLDPE production expansion. European SHOP-derived 1-hexene from Ineos Oligomers Hull was indicatively priced at USD 1,340 per metric tonne in Q2 2026, a USD 160 per metric tonne premium above North American SHOP pricing, reflecting ethylene feedstock cost elevation at European crackers from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026. Asian 1-hexene LLDPE comonomer pricing was stable at USD 980 per metric tonne in Q2 2026, reflecting Sinopec Zhejiang SHOP-equivalent C6 domestic supply additions that have reduced Chinese LLDPE producer dependence on Western imports. LyondellBasell disclosed in its January 2025 advanced polymer solutions briefing that its mLLDPE C6 Hostalen ACP grade had achieved specification approval at three major European stretch film converters, confirming the European commercial adoption pathway for metallocene C6 LLDPE in logistics packaging where gauge reduction economics are driving converter specification changes.

However, 1-hexene pricing is structurally linked to SHOP process ethylene oligomerisation economics and Sasol Fischer-Tropsch co-production rates rather than standalone hexene demand signals, meaning that 1-hexene spot price can diverge materially from underlying demand conditions when SHOP operators adjust LAO production rates in response to ethylene margin conditions or when Sasol Fischer-Tropsch operations are affected by operational events. Chinese SHOP-equivalent domestic 1-hexene supply from Sinopec at Zhejiang and CNOOC at Guangdong is reducing Chinese LLDPE dependence on imports and creating a downward pricing reference in Asian spot markets at USD 980 per metric tonne that is approximately USD 200 per metric tonne below North American SHOP-derived pricing. These factors substantially limit 1 hexene market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Metallocene LLDPE incorporating 1-hexene comonomer provides superior puncture resistance and elongation at break that allows film gauge reduction of 15% to 25% relative to conventional Ziegler-Natta LLDPE C4 grades while maintaining or exceeding load retention performance on wrapped pallets. Berry Global's Q1 2026 disclosure of 35% North American stretch film capacity converted to mLLDPE C6 grades, driven by gauge reduction material savings and improved load retention, confirms that the mLLDPE C6 transition is a commercially motivated conversion at scale, not a marginal trend. ExxonMobil Chemical confirmed a 20% gauge reduction case for its Exceed mLLDPE C6 grade at a major US stretch film converter in March 2025. LyondellBasell mLLDPE C6 Hostalen ACP achieved specification approval at three European stretch film converters in January 2025. At a film gauge reduction of 20%, each converted tonne of stretch film capacity requires approximately 20% less resin per wrapped pallet, reducing material cost per pallet equivalent and making the mLLDPE C6 premium over conventional LLDPE C4 commercially self-funding in logistics packaging economics. AlphaHex on-purpose 1-hexene from Chevron Phillips Chemical produces above 90% C6 isomeric selectivity without the full SHOP LAO co-production distribution, allowing Cedar Bayou to expand C6 supply in direct response to mLLDPE film demand growth without simultaneously adding surplus C8 through C20 LAO volumes. The Q4 2024 AlphaHex expansion adding 25,000 metric tonnes per year is the latest in a series of selective expansions at Cedar Bayou that have collectively made it the primary on-purpose 1-hexene source globally, with each AlphaHex expansion responding to documented demand pull from US LLDPE film converters specifying C6 comonomer for performance film applications. Agricultural film demand from Spain, Italy, Turkey, and Morocco is growing with the expansion of protected cultivation in Mediterranean agricultural regions, with the FAO confirming global agricultural plastic consumption exceeding 6.5 million metric tonnes annually in its 2024 assessment and LLDPE accounting for approximately 45% of that volume, of which a growing proportion incorporates 1-hexene comonomer for UV stability and mechanical performance in multi-year greenhouse covering applications. US Domestic C6 Supply Security from AlphaHex Decoupling LLDPE from SHOP Volatility AlphaHex selective trimerisation at Chevron Phillips Cedar Bayou decouples US C6 1-hexene supply from the ethylene oligomerisation economics and LAO co-production distribution constraints of SHOP technology, providing LLDPE producers a supply channel whose volume can expand specifically in response to C6 demand growth. The American Chemistry Council confirmed C6 as the preferred LLDPE comonomer in over 60% of US film-grade LLDPE production in 2024, and the AlphaHex series of capacity expansions represents a producer capital commitment to serving this demand base with a dedicated on-purpose supply source. Dow's Q4 2025 commercial launch of its Elite AT performance LLDPE C6 metallocene grade targeting US agricultural film markets, citing superior mechanical performance at reduced gauge, is a demand-side validation of the C6 comonomer supply investment rationale that Chevron Phillips has been executing through repeated AlphaHex expansions.

The majority of global 1-hexene supply outside of Chevron Phillips AlphaHex and Sasol Fischer-Tropsch comes from SHOP process LAO production where C6 hexene is one of many co-produced chain lengths at approximately 25% to 30% of total SHOP LAO output by volume. SHOP operators set overall production rates based on total LAO demand portfolio economics, meaning that an isolated C6 demand increase does not trigger a corresponding capacity expansion because co-produced C4, C8, C10, and C12 through C20 fractions must also find demand at profitable pricing. This structural rigidity means 1-hexene spot supply can tighten independently of overall SHOP capacity utilisation if specific chain length demand patterns shift, creating price volatility that is difficult for LLDPE procurement teams to predict from observable demand indicators. Chinese domestic 1-hexene supply from Sinopec at Zhejiang and CNOOC at Guangdong has added an estimated combined 40,000 to 60,000 metric tonnes per year of SHOP-equivalent C6 capacity, creating an Asian spot price reference at USD 980 per metric tonne in Q2 2026 that is approximately USD 200 per metric tonne below North American SHOP-derived pricing and compresses the economics for Western LAO producers attempting to serve Asian LLDPE comonomer demand. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated European ethylene feedstock costs at Ineos Oligomers Hull through naphtha cracker cost elevation, contributing to the USD 160 per metric tonne Europe-North America 1-hexene price premium in Q2 2026, widened from approximately USD 120 per metric tonne in Q2 2025. US AlphaHex on-purpose production at Chevron Phillips Cedar Bayou uses domestic ethane-based ethylene supply that is more insulated from Hormuz naphtha economics, maintaining the US cost competitiveness advantage and reinforcing the European import dependence on US AlphaHex and North American SHOP sources for premium-purity mLLDPE C6 comonomer applications. These factors substantially limit 1 hexene market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Grade | Polymer Grade, Chemical Grade | Polymer Grade |

| Production Route | Ethylene Oligomerisation (SHOP), Fischer-Tropsch Derived, On-Purpose AlphaHex | Ethylene Oligomerisation (SHOP) |

| Application | LLDPE and mLLDPE Comonomer, HDPE Comonomer, Poly-1-Hexene Polymer, Chemical Intermediate | LLDPE and mLLDPE Comonomer |

| End Use | Packaging Films, Blow Moulding, Pipes and Fittings, Agriculture, Industrial | Packaging Films |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Polymer Grade segment is expected to account for a significantly large revenue share in the global 1 hexene market during the forecast period.

This report evaluates grade across Polymer Grade, Chemical Grade for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates production route across Ethylene Oligomerisation (SHOP), Fischer-Tropsch Derived, On-Purpose AlphaHex for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across LLDPE and mLLDPE Comonomer, HDPE Comonomer, Poly-1-Hexene Polymer, Chemical Intermediate for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Packaging Films, Blow Moulding, Pipes and Fittings, Agriculture, Industrial for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

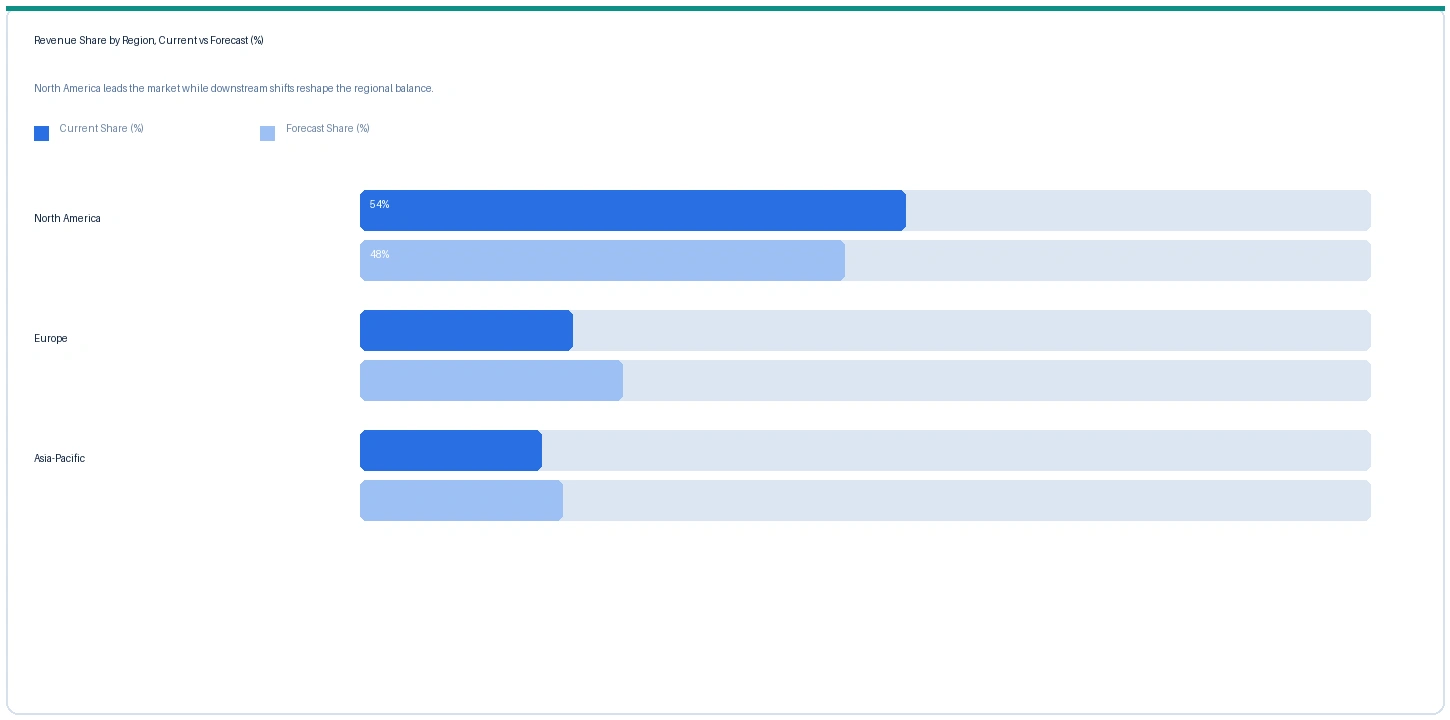

Regional Insights

North America market accounted for largest revenue share over other regional markets in the global 1 hexene market in 2025. Based on regional analysis, the 1 hexene market in North America accounted for largest revenue share in 2025. Chevron Phillips Chemical AlphaHex at Cedar Bayou and ExxonMobil Chemical SHOP at Baytown collectively make the US the most developed integrated C6 comonomer supply market globally, with the American Chemistry Council confirming C6 as the preferred LLDPE comonomer in over 60% of US film-grade LLDPE production in 2024 and annual consumption of approximately 280,000 to 320,000 metric tonnes. Berry Global's 35% North American stretch film capacity conversion to mLLDPE C6 and ExxonMobil Exceed grade market penetration at US packaging converters confirm that US mLLDPE C6 adoption is the highest globally and that AlphaHex supply security for US mLLDPE producers is a commercial priority. Chevron Phillips Q4 2024 AlphaHex expansion adds approximately 25,000 metric tonnes per year of dedicated C6 supply in direct response to this mLLDPE demand pull.

The market in Europe is expected to register the second largest revenue share. Ineos Oligomers at Hull supplies SHOP-derived 1-hexene to European LLDPE producers including Borealis, LyondellBasell Basell, and SABIC Polymers, with European C6 and C8 comonomers used in a mixture relative to the North American C6-dominant preference. LyondellBasell mLLDPE C6 Hostalen ACP achieving specification approval at three European stretch film converters in January 2025 confirms the European commercial adoption pathway for metallocene C6, which will pull incremental C6 demand as conversion accelerates through 2026 and 2027. European 1-hexene at USD 1,340 per metric tonne in Q2 2026 carries a USD 160 premium above North American levels from Ineos Oligomers Hull ethylene feedstock cost elevation via Hormuz-driven naphtha prices.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global 1 hexene market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period. Sinopec at Zhejiang and CNOOC at Guangdong commissioned SHOP-equivalent C6 fraction capacity adding an estimated 40,000 to 60,000 metric tonnes per year of domestic Chinese polymer-grade 1-hexene that reduced Chinese LLDPE producer dependence on imports. Asian LLDPE comonomer pricing at USD 980 per metric tonne in Q2 2026 is stable from these domestic supply additions. Chinese LLDPE film production grew approximately 9% in 2024 per CPCIF data, with C6 comonomer LLDPE gaining share from C4 butene grades in food packaging film applications, creating demand growth that is partially met by domestic Sinopec and CNOOC supply and partially by residual imports from ExxonMobil and Ineos under term agreements.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| 1-Hexene (AlphaHex, polymer grade) | North America | USD 1,240/MT | USD 1,140/MT | Rising | Chevron Phillips ref |

| 1-Hexene (SHOP, polymer grade) | North America | USD 1,180/MT | USD 1,080/MT | Rising | ExxonMobil ref |

| 1-Hexene (SHOP, polymer grade) | Europe | USD 1,340/MT | USD 1,220/MT | Rising | Ineos Oligomers ref |

| 1-Hexene (SHOP, polymer grade) | Asia-Pacific | USD 980/MT | USD 920/MT | Stable | Chinese domestic ref |

| LLDPE C6 Film Grade | North America | USD 1,380/MT | USD 1,260/MT | Rising | Resin benchmark |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and polyethylene trade publication monitoring. 1-Hexene is traded under term and spot contracts. Prices vary by production route, purity grade, contract volume, and regional supply balance.

North American polymer-grade 1-hexene prices rose approximately 8.8% across both AlphaHex and SHOP-derived grades in Q2 2026 against Q2 2025, driven by mLLDPE C6 adoption pull from Berry Global's 35% stretch film capacity conversion and ExxonMobil Exceed mLLDPE market penetration tightening allocation from Cedar Bayou and Baytown SHOP production. European SHOP-derived 1-hexene at Ineos Oligomers Hull rose 9.8% from USD 1,220 per metric tonne in Q2 2025 to USD 1,340 per metric tonne in Q2 2026, with the USD 160 per metric tonne Europe-North America premium widened from USD 120 per metric tonne in Q2 2025 reflecting Hormuz-driven European ethylene feedstock cost elevation. Asian LLDPE comonomer-grade 1-hexene pricing is stable at USD 980 per metric tonne as Sinopec Zhejiang and CNOOC Guangdong domestic supply additions offset regional demand growth. AlphaHex selectivity premium over SHOP-derived 1-hexene is stable at USD 60 per metric tonne in North America, reflecting the consistent value placed on above-90% isomeric selectivity by mLLDPE metallocene catalyst system operators who see reduced catalyst inhibition and improved film property consistency from the narrower isomeric distribution.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 1 hexene market, the Hormuz disruption affects SHOP-derived 1-hexene production in Europe through naphtha feedstock cost elevation at Ineos Oligomers Hull and at European naphtha crackers supplying ethylene to SHOP operators. The USD 160 per metric tonne Europe-North America 1-hexene price differential in Q2 2026, widened from USD 120 per metric tonne in Q2 2025, partially reflects this Hormuz-driven European ethylene cost elevation. US AlphaHex on-purpose 1-hexene at Chevron Phillips Cedar Bayou uses domestic ethane-based ethylene supply that is more insulated from Hormuz naphtha economics, reinforcing the US cost advantage and the concentration of mLLDPE C6 grade availability at US-origin sources. The disruption is also creating food supply security pressures in GCC and North African markets that are reinforcing government policy support for domestic food production through protected cultivation, which incrementally supports agricultural LLDPE C6 film demand in European and North African greenhouse covering markets supplied from Ineos Oligomers and Chevron Phillips 1-hexene sources.

Company Insights

The two key dominant companies in the 1 hexene market are Chevron Phillips Chemical and Ineos Oligomers, recognised for their leadership in on-purpose AlphaHex 1-hexene technology and SHOP-derived 1-hexene production respectively, their established supply relationships with North American and European LLDPE producers, and their contrasting production route strategies defining the competitive dynamic between on-purpose selective C6 production and SHOP co-production economics.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 138.3 Million |

| Market Size 2032 | USD 197.2 Million |

| CAGR | 5.2% |

| Units | Revenue in USD Million |

| Segments Covered | By Grade, By Production Route, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, UK, Germany, France, China, Japan, South Korea, Saudi Arabia, South Africa, Brazil, Spain, Italy |

| Companies Profiled | Chevron Phillips Chemical, Ineos Oligomers, ExxonMobil Chemical, Sasol, Sinopec, CNOOC, SABIC, LyondellBasell, Borealis, Mitsui Chemicals |

| Key Data Sources | American Chemistry Council LLDPE comonomer data, Berry Global Q1 2026 stretch film conversion disclosure, ExxonMobil Chemical Exceed 20% gauge reduction case, LyondellBasell Hostalen ACP converter qualification disclosure, FAO agricultural plastics assessment, Chevron Phillips Chemical AlphaHex capacity expansion announcements, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 252 |

| Published | Q2 2026 |

| SKU | NXC-PC-009 |

Scope & Methodology

Primary Research

Secondary Research