Market Data

The global bipolar forceps market size was USD 2.23 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period. Market revenue growth is supported by increasing global surgical procedure volumes driven by aging population demographics and expanding access to surgical care in emerging market healthcare systems, the structural shift from reusable to disposable bipolar forceps in neurosurgery and gynecology driven by hospital infection control protocol intensification following the COVID-19 pandemic and Joint Commission reprocessing compliance requirements, and Medtronic's LigaSure bipolar vessel sealing system expanding clinical adoption in colorectal, bariatric, and thyroid surgery where its advanced bipolar vessel sealing capability enables minimally invasive procedures with reduced blood loss and shortened operative time relative to conventional clip and tie hemostasis. Medtronic disclosed in its Surgical Innovations segment that LigaSure bipolar vessel sealing represented one of its highest-volume advanced energy product lines in its Medical Surgical Portfolio, with estimated global LigaSure revenue of approximately USD 180 million to USD 240 million and Malis bipolar neurosurgery system revenue of approximately USD 80 million to USD 120 million confirming Medtronic's leadership in both general surgical bipolar sealing and neurosurgical bipolar precision applications. Johnson and Johnson's Ethicon ENSEAL bipolar tissue sealing device generated estimated revenue of approximately USD 200 million to USD 280 million in bipolar-specific advanced energy applications in its MedTech segment, competing with Medtronic LigaSure in minimally invasive general and gynecological surgery procedures where bipolar vessel sealing replaces conventional mechanical fastening with documented clinical evidence for reduced intraoperative blood loss. B. Braun Melsungen's Aesculap bipolar electrosurgery product line generated estimated EUR 80 million to EUR 120 million in bipolar forceps and coagulation system revenue from its comprehensive neurosurgical, general surgical, and gynecological bipolar forceps portfolio distributed through its global Aesculap surgical instrument network reaching more than 60 countries. For instance, in March 2025, Medtronic, United States, received FDA 510(k) clearance for its next-generation LigaSure Montana bipolar vessel sealing instrument for use in thoracoscopic and robotic-assisted thoracic surgery procedures, expanding the LigaSure clinical indication from its established colorectal and gynecological surgery applications into thoracic surgery where conventional clip ligation of pulmonary vessels requires additional operative steps that bipolar vessel sealing can replace in video-assisted thoracoscopic surgery. These are some of the key factors driving revenue growth of the market.

Bipolar vessel sealing systems including Medtronic LigaSure and Johnson and Johnson ENSEAL accounted for approximately 34% to 38% of total bipolar forceps market revenue in 2025, representing the highest average selling price segment at approximately USD 180 to USD 450 per disposable handpiece in hospital group purchasing organisation contract pricing, and the fastest-growing product category as minimally invasive surgical procedure volume growth in colorectal, gynecological, bariatric, and thyroid surgery generates above-trend volume growth for advanced bipolar sealing relative to conventional bipolar coagulation in open surgery. Reusable bipolar forceps from Aesculap B. Braun, Sutter Medizintechnik, Erbe Elektromedizin, and Integra LifeSciences Malis brand remain the dominant product type by unit volume in neurosurgery and ophthalmic surgery where precision tip geometry and tungsten-silver alloy construction provide the delicate tissue coagulation performance that disposable bipolar forceps do not yet replicate at equivalent precision, with Malis bipolar forceps maintaining gold standard clinical positioning in neurosurgical specialty across a half-century of neurosurgeon training and preference reinforcement. ConMed Corporation disclosed in its 2024 Annual Report that its electrosurgery segment contributed approximately USD 80 million to USD 120 million in bipolar forceps and generator system revenue, with laparoscopic bipolar forceps for gynecological and general surgical applications growing above-trend in North American ambulatory surgical centre adoption. Erbe Elektromedizin at Tubingen, Germany is estimated at approximately EUR 60 million to EUR 90 million in bipolar coagulation system revenue from its VIO 3 electrosurgical generator and bipolar instruments platform supplying European hospital electrosurgery equipment procurement.

However, reprocessing cost and clinical workflow disruption associated with disposable bipolar forceps conversion in hospital systems with established reusable bipolar instrument sterilisation and maintenance infrastructure represent adoption barriers that limit conversion speed even where infection control evidence and risk management rationale favour single-use alternatives, as the per-procedure disposable bipolar forceps cost of USD 80 to USD 450 per unit represents a direct supply cost increase above the amortised cost of reusable bipolar forceps at approximately USD 8 to USD 25 per reprocessing cycle. Price competition from Chinese and Indian surgical instrument manufacturers including Lepu Medical and Bharat Surgical offering bipolar forceps at 40% to 60% price discounts below European and US branded products is compelling European hospital group purchasing organisations to include lower-cost alternatives in procurement frameworks, compressing branded manufacturer margin sustainability in standard bipolar forceps categories while premium advanced bipolar sealing systems maintain pricing through clinical differentiation. Robotic-assisted surgery platform integration, while providing a growth driver for bipolar energy instruments compatible with Intuitive Surgical da Vinci robotic system end-effectors, also concentrates procurement power at Intuitive Surgical through proprietary end-effector compatibility requirements that limit non-Intuitive bipolar instrument adoption at robotic surgery programmes. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated stainless steel, tungsten wire, and medical device component supply chain costs through elevated energy costs at European surgical instrument manufacturing facilities in Germany and France, adding approximately 3% to 6% to European precision bipolar forceps manufacturing cost and sustaining premium pricing for European-manufactured precision bipolar instruments relative to Asian alternatives. These factors substantially limit bipolar forceps market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Joint Commission Standard IC.02.02.01 in the United States and EU Medical Device Regulation 2017/745 reprocessing documentation requirements have intensified hospital infection control protocols for reusable surgical instruments, creating institutional risk management preference for single-use alternatives in applications where reprocessing compliance documentation and contamination liability are identified as material operating risks. The Association of periOperative Registered Nurses and the American College of Surgeons have published guidance on single-use electrosurgical instrument adoption in cases involving patients with prior prion disease exposure, neurodegenerative disease history, or unexplained neurological symptoms, creating clinical protocols at US academic medical centres that mandate single-use bipolar forceps in designated patient categories and generate recurrent disposable bipolar procurement at above-average per-procedure cost. Medtronic's disposable bipolar forceps product line and B. Braun Aesculap's single-use bipolar range have both expanded product catalogues in the 2024 to 2026 period to address hospital conversion programmes, with disposable bipolar forceps growing at approximately 12% to 15% per year against approximately 3% to 5% for reusable equivalent categories. EU MDR 2017/745 reprocessing labelling requirements effective May 2024 require manufacturers of reusable surgical instruments to provide detailed reprocessing validation data that increases compliance burden for smaller reusable bipolar forceps manufacturers, creating a regulatory incentive for hospital procurement to consolidate on validated-reprocessing documented manufacturers or convert to single-use alternatives with simpler post-use disposal protocols. Minimally Invasive Surgery Growth and Emerging Market Hospital Infrastructure Investment Global minimally invasive surgical procedure volume is growing at approximately 6% to 8% per year per WHO surgical care programme data, driven by patient preference for shorter recovery times, laparoscopic and robotic technique adoption at community hospitals expanding access to minimally invasive procedures beyond academic medical centre concentration, and clinical evidence for superior outcomes in colorectal, gynecological, urological, and thoracic surgery supported by above-trend laparoscopic and robotic procedure volume growth. Laparoscopic bipolar forceps for gynecological procedures including hysterectomy, myomectomy, and endometriosis excision are among the highest-volume single-use bipolar products in North American ambulatory surgical centres, with ConMed laparoscopic bipolar and Medtronic LigaSure lap instruments growing above-trend as ambulatory centre procedure volume shifts procedures from inpatient hospital operating rooms to ambulatory settings where single-use instrument cost is directly passed through procedure facility fees. Emerging market hospital infrastructure investment in China, India, Brazil, the Gulf Cooperation Council, and Southeast Asia is expanding the surgical procedure base at rates above high-income market growth, with Chinese hospital electrosurgery equipment procurement from domestic manufacturers including Lepu Medical and Zhejiang Zheda Roper generating growing bipolar forceps volume at price points accessible to tier 2 and tier 3 Chinese hospital procurement budgets. India's National Health Mission hospital infrastructure programme and private hospital expansion at Apollo Hospitals, Fortis Healthcare, and Manipal Health Enterprises are growing India's addressable bipolar forceps market at approximately 9% to 12% per year per Ministry of Health and Family Welfare hospital infrastructure data.

The per-procedure cost of disposable bipolar forceps at USD 80 to USD 450 per unit versus amortised reusable bipolar forceps at approximately USD 8 to USD 25 per reprocessing cycle represents a 4 to 18 times direct cost premium per procedure that hospital supply chain directors and group purchasing organisation negotiators must justify through documented infection control risk reduction or clinical outcome improvement evidence before approving disposable bipolar conversion programmes at hospital system scale. National Health Service hospital procurement in the UK, German Diagnosis-Related Group reimbursement structure, and French T2A tariff-based hospital financing systems do not provide direct reimbursement uplift for single-use bipolar instrument substitution in most elective surgical categories, creating a reimbursement funding gap that hospital operating budgets must absorb without corresponding revenue increase per procedure. Chinese bipolar forceps manufacturers offering products at 40% to 60% price discounts below Medtronic, B. Braun, and Erbe reference pricing are achieving listing in European hospital group purchasing frameworks through CE marking under EU MDR 2017/745 and are gaining volume at cost-constrained European hospital systems that are not able to maintain premium pricing commitments in surgical instrument category price negotiations. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated medical grade stainless steel, tungsten wire, and polyimide insulation material costs through energy cost increases at European precision manufacturing facilities in Germany, Austria, and France, adding approximately 3% to 6% to precision bipolar forceps manufacturing cost that European branded manufacturers are absorbing in margin compression rather than passing through in full to hospital procurement pricing under long-term GPO contract structures. These factors substantially limit bipolar forceps market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product | Reusable Bipolar Forceps, Disposable Bipolar Forceps, Bipolar Vessel Sealing Systems, Laparoscopic Bipolar Forceps, Micro and Neurosurgical Bipolar Forceps | Reusable Bipolar Forceps |

| Application | Neurosurgery, General Surgery, Gynecology, Urology, Cardiovascular Surgery, ENT, Ophthalmology, Orthopedics | Neurosurgery |

| End Use | Hospitals, Ambulatory Surgical Centers, Specialty Clinics | Hospitals |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Bipolar Vessel Sealing Systems segment is expected to account for a significantly large revenue share in the global bipolar forceps market during the forecast period.

This report evaluates product across Reusable Bipolar Forceps, Disposable Bipolar Forceps, Bipolar Vessel Sealing Systems, Laparoscopic Bipolar Forceps, Micro and Neurosurgical Bipolar Forceps for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Neurosurgery, General Surgery, Gynecology, Urology, Cardiovascular Surgery, ENT, Ophthalmology, Orthopedics for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Hospitals, Ambulatory Surgical Centers, Specialty Clinics for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

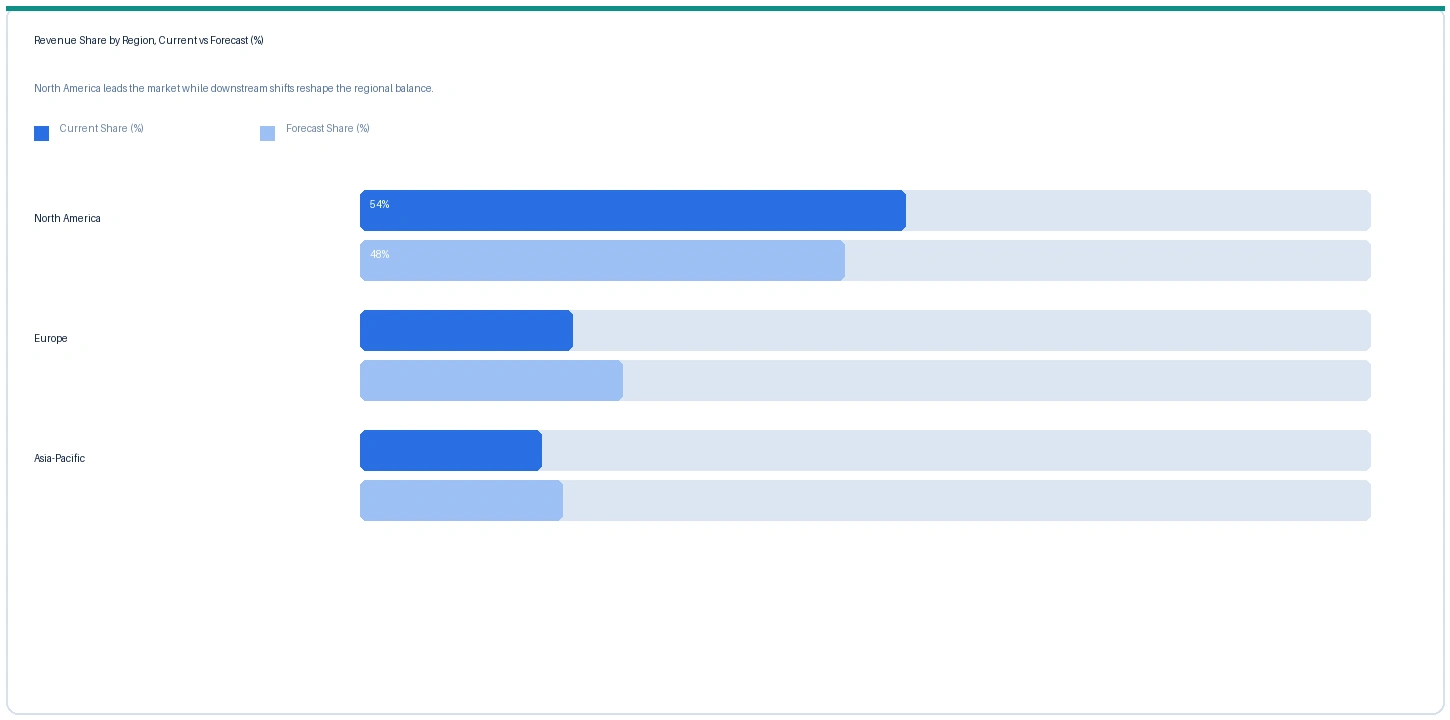

North America market accounted for largest revenue share over other regional markets in the global bipolar forceps market in 2025. Based on regional analysis, the bipolar forceps market in North America accounted for the largest revenue share in 2025. North American hospital group purchasing organisations including Vizient, Premier, and Healthtrust negotiate advanced bipolar sealing contracts at above-global-average unit pricing that sustains North American revenue leadership despite Asia-Pacific accounting for the largest global surgical volume by procedure count. Medtronic US commercial operations, Johnson and Johnson Ethicon, and ConMed represent the primary North American bipolar forceps market participants, with Integra LifeSciences Malis bipolar neurosurgery systems dominating the US academic medical centre neurosurgical bipolar market through long-established neurosurgeon preference and training programme integration. FDA 510(k) clearance requirements and US MDR device reporting obligations create a regulatory framework that favours established US and European medical device brands over Chinese manufacturers seeking US market entry at the commodity bipolar forceps tier.

The market in Europe is expected to register the second largest revenue share in the global bipolar forceps market. Germany, France, UK, and the Netherlands represent the primary European bipolar forceps consumption markets, with B. Braun Aesculap, Erbe Elektromedizin, Sutter Medizintechnik, and KLS Martin Group operating the primary European bipolar forceps manufacturing base at their German production facilities. EU MDR 2017/745 reprocessing compliance documentation requirements have increased the regulatory burden for reusable bipolar forceps manufacturers, driving hospital procurement interest in single-use alternatives from Medtronic and B. Braun that reduce reprocessing validation documentation requirements. European National Health Service and statutory health insurance hospital procurement frameworks operate on DRG-based reimbursement structures that do not directly increase bipolar forceps reimbursement for single-use product adoption, limiting conversion speed despite clinical infection control preference for single-use alternatives.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global bipolar forceps market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period. China's hospital infrastructure expansion programme targeting tier 2 and tier 3 hospital surgical capability development, India's National Health Mission hospital investment, South Korean private hospital sector expansion, and Australian private hospital procedure volume growth are collectively driving Asia-Pacific bipolar forceps market growth at above-global-average rates. Domestic Chinese bipolar forceps manufacturers including Lepu Medical and Zhejiang Zheda Roper are capturing growing domestic hospital volume at price points below international branded products, with CE-marked and NMPA-approved domestic products gaining procurement listing at Chinese public hospital group purchasing programmes. Olympus Corporation's endoscopic bipolar products for Japanese and Korean hospital electrosurgery supply and Takasago's Japanese domestic neurosurgical bipolar instruments contribute to Japanese and Korean bipolar market revenue from domestic manufacturer supply independent of European and US branded product imports.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| LigaSure bipolar vessel sealer (5mm) | North America | USD 342/unit | USD 318/unit | Rising | Medtronic GPO ref |

| ENSEAL bipolar tissue sealer | North America | USD 298/unit | USD 276/unit | Rising | J&J Ethicon GPO ref |

| Reusable Aesculap bipolar (titanium) | Europe | USD 1,840/set | USD 1,720/set | Rising | B.Braun Aesculap ref |

| Disposable laparoscopic bipolar | North America | USD 124/unit | USD 114/unit | Rising | ConMed/Microline ref |

| Chinese OEM bipolar forceps (std) | Asia-Pacific | USD 18/unit | USD 16/unit | Rising | Domestic ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, hospital group purchasing organisation contract disclosures, and medical device trade publication monitoring. Bipolar forceps prices vary by product type, clinical application, hospital contract tier, and regional reimbursement structure. GPO contract pricing is indicative; list prices may be materially higher.

LigaSure 5mm bipolar vessel sealer disposable handpiece prices rose approximately 7.5% from USD 318 per unit in Q2 2025 to USD 342 per unit in Q2 2026 in North American GPO contract pricing, driven by above-plan LigaSure clinical adoption in robotic-assisted colorectal and thoracic surgery procedure volumes expanding the commercial indication base, and by Medtronic March 2025 FDA clearance for LigaSure Montana thoracoscopic extension generating incremental procedure volume at GPO price tier. J&J Ethicon ENSEAL bipolar tissue sealer rose approximately 7.9% to USD 298 per unit in Q2 2026 on gynecological laparoscopic hysterectomy volume growth at ambulatory surgical centres. Reusable Aesculap B. Braun bipolar forceps set pricing rose approximately 7.0% in Europe to USD 1,840 per set from USD 1,720 per set in Q2 2025, driven by stainless steel and tungsten alloy raw material cost elevation at Aesculap's Tuttlingen, Germany precision manufacturing operations from energy cost increases sustained by the Strait of Hormuz supply disruption. Disposable laparoscopic bipolar in North America rose approximately 8.8% to USD 124 per unit on ambulatory surgical centre volume growth and hospital GPO contract tier escalation clauses triggered by procedure volume thresholds. Chinese OEM standard bipolar forceps rose approximately 12.5% to USD 18 per unit from USD 16 per unit in Asia-Pacific, the fastest proportional increase in the peer group, driven by Chinese stainless steel and medical grade polymer input cost elevation and above-plan Chinese hospital procurement demand tightening domestic supply at mid-tier manufacturers.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the bipolar forceps market, the Hormuz disruption affects production economics at European precision surgical instrument manufacturers in Germany, Austria, and France through elevated natural gas and electricity costs at precision metal machining facilities, with German industrial energy prices approximately 15% to 20% above the 2024 baseline in Q2 2026 from LNG supply disruption adding to manufacturing cost at Aesculap's Tuttlingen, Erbe Elektromedizin's Tubingen, and Sutter Medizintechnik's Freiburg precision machining operations. Medical grade stainless steel, tungsten alloy wire, and polyimide insulation material costs are elevated approximately 3% to 8% from the broader global raw material and energy cost inflation sustained by the Hormuz disruption, flowing through to reusable bipolar forceps manufacturing cost increases of approximately 4% to 7% at European precision manufacturers in Q2 2026. GCC hospital capital equipment procurement disruption from the broader US-Iran conflict environment is adding uncertainty to UAE and Saudi Arabian hospital electrosurgery programme upgrade timelines, with some GCC private hospital networks deferring capital equipment commitments pending geopolitical stability assessment, modestly constraining Middle East and Africa bipolar forceps volume growth projections for H2 2026.

Company Insights

The two key dominant companies in the bipolar forceps market are Medtronic and Johnson and Johnson (Ethicon), recognised for their leadership in advanced bipolar vessel sealing systems with broad clinical indication coverage across minimally invasive surgical specialties, their established hospital group purchasing organisation contract infrastructure, and their technical leadership in robotic surgical platform-compatible bipolar sealing instrument development.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 2.23 Billion |

| Market Size 2032 | USD 3.24 Billion |

| CAGR | 6.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, UK, France, Netherlands, Japan, China, India, South Korea, Australia, Brazil, UAE, Saudi Arabia |

| Companies Profiled | Medtronic, J&J Ethicon, B. Braun Aesculap, Erbe Elektromedizin, ConMed, Integra LifeSciences, Olympus, Stryker, KLS Martin, Sutter Medizintechnik, Kirwan Surgical, Bowa-Electronic, Richard Wolf, Microline Surgical |

| Key Data Sources | Medtronic FY2024 Annual Report Surgical Innovations segment, J&J 2024 Annual Report MedTech ENSEAL disclosure, B. Braun 2024 annual revenue and Aesculap product disclosures, ConMed 2024 Annual Report electrosurgery segment, Medtronic FDA 510(k) LigaSure Montana clearance March 2025, Erbe Elektromedizin VIO 3 European launch Q4 2024, WHO 2023 global surgical volume statistics, Joint Commission IC.02.02.01 reprocessing standards, IMF March 2026 Hormuz statement, 17 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 256 |

| Published | Q2 2026 |

| SKU | NXC-MD-001 |

Scope & Methodology

Primary Research

Secondary Research