Market Data

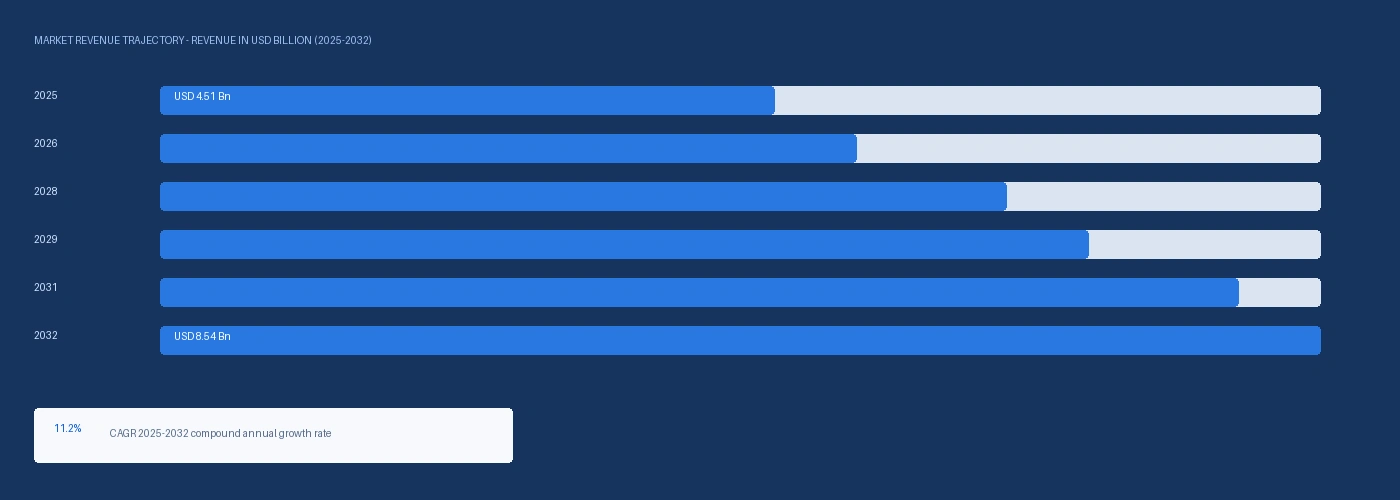

The global biostimulant market size was USD 4.51 Billion in 2025 and is expected to register a revenue CAGR of 11.2% during the forecast period. Market revenue growth is supported by EU Regulation 2019/1009 establishing biostimulants as a defined product category within the EU fertilising products regulation from July 2022, creating a harmonised EU single market regulatory framework that enables commercial-scale investment in biostimulant product development and marketing across EU member states without individual national registration in each market, accelerating the conversion of fragmented national biostimulant programmes into scalable pan-European commercial products. Syngenta's acquisition of Valagro in 2020 for approximately EUR 470 million, generating estimated biostimulant revenue of approximately USD 180 million to USD 220 million in 2024, confirmed that multinational agrochemical companies are committing acquisition-scale capital to biostimulant portfolio integration as the Farm to Fork Strategy 20% fertiliser use reduction target creates structural demand for nutrient use efficiency tools that biostimulants specifically address without reducing crop yield. Novozymes BioAg, with estimated biostimulant revenue of approximately USD 80 million to USD 110 million in 2024 from its rhizobia, mycorrhizae, and plant growth-promoting rhizobacteria product lines, confirmed above-plan microbial biostimulant volume growth in Latin American soybean and European cereal markets where nitrogen use efficiency programmes are creating structural demand for biological nitrogen fixation enhancement tools that reduce synthetic nitrogen fertiliser application rates. UPL Limited disclosed its biostimulant-attributed product contribution at approximately USD 120 million to USD 160 million in its 2024 Annual Report, with foliar amino acid and seaweed extract biostimulants growing in European and Asian specialty crop markets where growers operating under integrated crop management programmes are specifying biostimulants as a documented nutrient efficiency component of their farm management plans. For instance, in March 2025, Corteva Agriscience, United States, announced a collaboration agreement with Symborg S.L., Spain, for global commercialisation of Symborg mycorrhizal bioprotection technology, the first major US agrochemical company collaboration with a European mycorrhizal biostimulant developer for global commercial deployment, confirming that the strategic value of microbial biostimulant IP is attracting multinational partnership investment at terms previously reserved for conventional chemistry acquisition programmes. These are some of the key factors driving revenue growth of the market.

Humic and fulvic acids accounted for approximately 28% to 32% of total biostimulant market revenue in 2025, representing the largest type segment by volume at competitive pricing of approximately USD 0.80 to USD 3.20 per kilogram of active humic substance supplied from leonardite, lignite, and composted biomass extraction facilities concentrated in China, the United States, and Spain. Chinese humic acid producers including Haihang Group, Shandong Runke, and Inner Mongolia Yuanye collectively generate an estimated USD 280 million to USD 360 million in biostimulant-attributed humic acid revenue, establishing China as the dominant global humic substance production base at commodity pricing that European and North American integrated biostimulant formulators must compete against on value-added formulation rather than active ingredient cost. Seaweed extract biostimulants from Acadian Seaplants at approximately CAD 130 million to CAD 170 million total revenue and BioAtlantis at approximately EUR 20 million to EUR 35 million represent the primary commercially established seaweed biostimulant supply base, with asco and sargassum seaweed extract hormone active compounds including cytokinins, auxins, and betaines providing plant stress tolerance and root development benefits that are increasingly documented in peer-reviewed field trial literature required by EU Regulation 2019/1009 efficacy claim substantiation. Protein hydrolysate and amino acid biostimulants from Bioiberica at approximately EUR 80 million to EUR 110 million and Ilsa Group at approximately EUR 45 million to EUR 65 million supply European horticulture, viticulture, and olive production with free amino acid foliar formulations documented in Italian, Spanish, and French national biostimulant regulatory approval frameworks that preceded EU 2019/1009 and have now been integrated into the harmonised EU product category.

However, the biostimulant market remains characterised by highly variable efficacy documentation across product types and crop applications, with EU Regulation 2019/1009 Annex II efficacy claim substantiation requirements calling for statistically robust field trial data across representative agronomic conditions that many established biostimulant products have not yet generated to the required regulatory standard, creating commercial uncertainty for growers and distributors evaluating biostimulant programme investment. Chinese commodity humic acid production at low-cost extraction pricing of approximately USD 0.80 to USD 1.40 per kilogram is entering European and North American markets through trading intermediaries and private label formulation channels, compressing margins for value-added humic acid biostimulant formulators who cannot differentiate on active ingredient origin and quality sufficiently to sustain premium pricing against commodity Chinese supply. Microbial biostimulant shelf-life constraints, cold chain requirements for live bacterial inoculant products, and rhizobium compatibility restrictions with commonly used seed treatment fungicides and insecticides limit the adoption of microbial biostimulant seed treatment programmes in conventional production systems where existing pesticide seed treatment protocols conflict with live bacterial viability requirements. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated synthetic fertiliser input costs through natural gas and ammonia production cost disruption, improving the relative economics of biostimulant-based nutrient use efficiency programmes for cost-pressured European and Asian grain producers but simultaneously reducing grower capital available for discretionary biostimulant programme adoption beyond minimum fertiliser input maintenance. These factors substantially limit biostimulant market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EU Regulation 2019/1009 on fertilising products, fully applicable from July 2022, established biostimulants as Product Function Category 6 within the EU fertilising products framework, creating for the first time a defined EU-harmonised product category that enables single market commercialisation of biostimulant products without individual national authorisation in each of the 27 EU member states. The European Biostimulant Industry Council confirmed that the harmonised EU framework reduced average time to market for new biostimulant product launches from 24 to 36 months under fragmented national systems to 12 to 18 months under the EU 2019/1009 unified conformity assessment pathway, enabling commercial-scale investment in biostimulant R&D pipelines that previously could not justify the capital outlay against uncertain and fragmented national regulatory timelines. The Farm to Fork Strategy target of 20% reduction in fertiliser use by 2030 without commensurate yield reduction explicitly identifies biostimulants as the primary tool for maintaining crop productivity under reduced synthetic fertiliser inputs, creating a policy mandate that national governments are incorporating into agri-environment scheme payment structures and advisory service recommendations. Corteva Agriscience's Symborg collaboration and Bayer CropScience's biostimulant portfolio investment confirm that the regulatory framework is generating multinational programme commitment at a scale that will professionalise product development standards, distribution network investment, and grower adoption programme infrastructure across European markets where biostimulant penetration remains below 15% of addressable crop acreage. Multinational Agrochemical Acquisition and Distribution Integration Accelerating Commercial Adoption Syngenta's EUR 470 million acquisition of Valagro in 2020 and the subsequent integration of Valagro's seaweed, amino acid, and microbial biostimulant portfolio into Syngenta's global agrochemical distribution network reaching more than 90 countries represents the most commercially significant biostimulant market consolidation event to date, confirming that established agrochemical distribution infrastructure is the primary commercial barrier to biostimulant adoption scale that multinational acquisitions directly address. Corteva Agriscience disclosed in its 2024 Annual Report that its biological crop protection and biostimulant combined portfolio contribution had reached approximately USD 370 million to USD 460 million, with the biological and biostimulant combined segment identified as the fastest-growing crop protection and crop nutrition sub-category across the Corteva product portfolio. BASF Agricultural Solutions confirmed biostimulant product lines including Comcat plant activator and Kelmin seaweed extract product at estimated EUR 120 million to EUR 160 million in 2024 biostimulant revenue, integrated into BASF's global crop protection distribution infrastructure that enables biostimulant products to reach grower markets through established distributor networks rather than requiring separate biostimulant-specific commercial development. Novozymes BioAg and Chr. Hansen's merger creating dsm-firmenich's bio-based Agriculture division provides a combined microbial biostimulant commercial portfolio with global distribution reach that standalone Novozymes or Chr. Hansen could not replicate independently, confirming industry structure consolidation as a commercial driver for biostimulant market development.

EU Regulation 2019/1009 Annex II efficacy claim substantiation requirements for Plant Biostimulant Product Function Category 6 require statistically robust replicated field trial data demonstrating documented plant growth, yield, or quality responses attributable to the biostimulant treatment across representative agronomic conditions in the EU crop systems and climate zones relevant to the labelled efficacy claim, a scientific substantiation standard that the majority of established biostimulant products marketed under prior national registration frameworks have not yet generated to the EU 2019/1009 required evidentiary level, creating a compliance investment requirement estimated at EUR 150,000 to EUR 400,000 per efficacy claim substantiation dossier that significantly burdens smaller biostimulant producers relative to multinational companies with established field trial infrastructure. Chinese commodity humic acid extraction at leonardite and lignite mining-integrated production facilities generates humic substance at approximately USD 0.80 to USD 1.40 per kilogram of humic substance active content, delivered to European formulators through trading intermediary channels at prices approximately 40% to 60% below European-produced humic acid from Tradecorp and Compo Expert, eroding the margin sustainability of European humic acid biostimulant producers who cannot differentiate on quality parameters that current EU 2019/1009 product category specifications do not yet include meaningful quality grading criteria for. Microbial biostimulant seed treatment compatibility with standard organophosphate, triazole, and neonicotinoid seed treatment pesticide actives is limited for many Rhizobium and Bacillus strains, with compatibility matrices published by Novozymes BioAg and Lallemand Plant Care confirming that fewer than 60% of commercial seed treatment pesticide combinations maintain microbial viability above commercially effective inoculant counts after co-application, limiting the practical adoption of combined biological and chemical seed treatment programmes at conventional production system scale. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated synthetic nitrogen fertiliser costs through natural gas feedstock disruption at European and Asian ammonia producers, diverting cost-pressured grain producers toward minimum fertiliser input maintenance expenditure rather than biostimulant programme investment in commodity cereal and oilseed production markets. These factors substantially limit biostimulant market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Humic and Fulvic Acids, Seaweed Extracts, Protein Hydrolysates and Amino Acids, Microbial Biostimulants (PGPR/Mycorrhizae), Inorganic Mineral Biostimulants, Others | Humic and Fulvic Acids |

| Application Method | Foliar Spray, Soil Application, Seed Treatment, Fertigation | Foliar Spray |

| Crop Type | Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Turf and Ornamentals, Others | Fruits and Vegetables |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Humic and Fulvic Acids segment is expected to account for a significantly large revenue share in the global biostimulant market during the forecast period.

This report evaluates type across Humic and Fulvic Acids, Seaweed Extracts, Protein Hydrolysates and Amino Acids, Microbial Biostimulants (PGPR/Mycorrhizae), Inorganic Mineral Biostimulants, Others for agrochemicals, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application method across Foliar Spray, Soil Application, Seed Treatment, Fertigation for agrochemicals, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates crop type across Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Turf and Ornamentals, Others for agrochemicals, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for agrochemicals, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

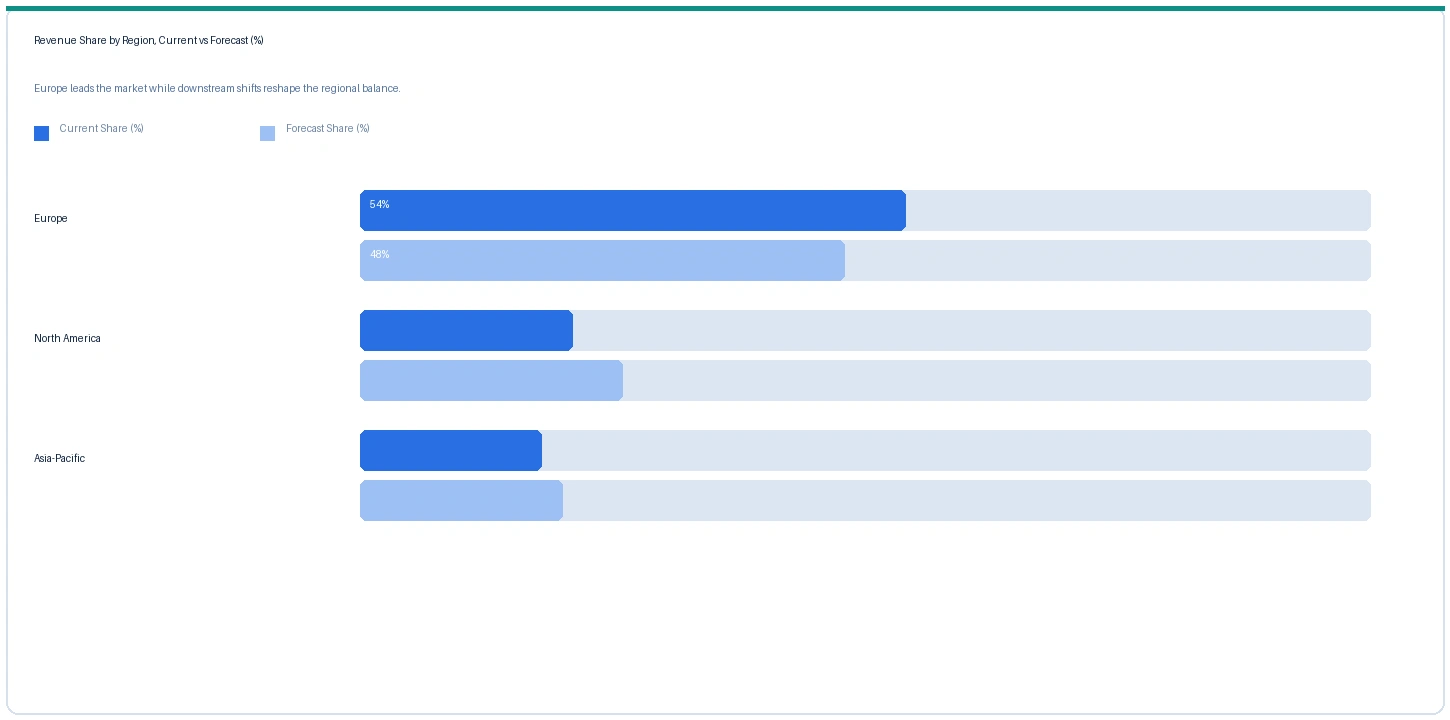

Europe market accounted for largest revenue share over other regional markets in the global biostimulant market in 2025. Based on regional analysis, the biostimulant market in Europe accounted for the largest revenue share in 2025. EU Regulation 2019/1009 creating a defined harmonised biostimulant product category, Farm to Fork 20% fertiliser reduction targets, European agri-environment scheme payment structures rewarding biostimulant-supported reduced input farming, and the concentration of high-value horticulture and viticulture in Italy, Spain, France, and Greece that creates favourable per-hectare biostimulant programme economics collectively establish Europe as the world's most commercially developed biostimulant market. The European Biostimulant Industry Council confirmed European market size at approximately EUR 600 million to EUR 800 million in 2023 biostimulant product sales, growing at approximately 10% to 12% per year, accounting for approximately 17% to 20% of the global biostimulant market by value. Italy leads European biostimulant consumption with the most established national regulatory approval history pre-EU 2019/1009, largest concentration of intensive horticulture, and the most developed biostimulant agronomic advisory infrastructure through its national network of technical agricultural consultancies.

The market in North America is expected to register the second largest revenue share in the global biostimulant market. US biostimulant market growth is supported by USDA NRCS EQIP conservation programme cost-share payments for nutrient management plans incorporating biostimulants, increasing organic acreage creating mandatory biostimulant-compatible crop nutrition programmes, and multinational distribution infrastructure investment from Corteva, Bayer CropScience, and BASF bringing biostimulant product portfolios into established US agrochemical dealer networks. The US lacks a federal harmonised biostimulant regulatory framework equivalent to EU 2019/1009 as of Q2 2026, with biostimulant products regulated at state level under varying soil amendment, fertiliser, and pesticide classification frameworks that complicate national product launches and limit the commercial investment justification for pan-US biostimulant product development programmes.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global biostimulant market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period. India's National Biostimulant Policy framework under development in 2024 to 2025 and the Ministry of Agriculture and Farmers Welfare organic farming expansion programmes are creating a regulatory and demand foundation for commercial biostimulant adoption in Indian horticulture and cereal markets. China's organic conversion target of 15% organic certified farmland by 2030 and the Ministry of Agriculture and Rural Affairs biostimulant technology promotion programmes are generating domestic demand for humic acid and amino acid biostimulants at volume scales that are simultaneously creating export supply competition in global markets. Japanese precision horticulture and Korean smart farming technology adoption are integrating biostimulant applications into data-driven crop management systems, with Acadian seaweed extract and dsm-firmenich BioAg microbial products gaining specification acceptance in Japanese and Korean protected horticulture operations.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Humic acid (leonardite, granular) | Europe | USD 1.84/kg | USD 1.68/kg | Rising | Tradecorp/Compo ref |

| Seaweed extract (asco, liquid) | North America | USD 8.40/kg | USD 7.80/kg | Rising | Acadian Seaplants ref |

| Amino acid hydrolysate (L-form) | Europe | USD 6.20/kg | USD 5.70/kg | Rising | Bioiberica/Ilsa ref |

| Rhizobium inoculant (liquid) | Latin America | USD 14.60/dose | USD 13.40/dose | Rising | Novozymes BioAg ref |

| Synthetic N fertiliser (benchmark) | Global | USD 380/MT | USD 340/MT | Rising | Urea reference |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and agricultural chemical trade publication monitoring. Biostimulant products are not exchange traded. Prices vary by active ingredient type, efficacy documentation level, formulation grade, and regional distribution margins.

Biostimulant product prices rose across all major categories in Q2 2026 relative to Q2 2025, driven by increased PPWR anticipation-equivalent regulatory demand from EU 2019/1009 compliance programme adoption at European distributors, agricultural raw material and fermentation feedstock cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, and growing demand from Farm to Fork grower programme adoption that is converting discretionary biostimulant use into scheduled programme applications with contracted supply commitments. Humic acid leonardite granular prices rose approximately 9.5% in Europe from USD 1.68 per kilogram in Q2 2025 to USD 1.84 per kilogram in Q2 2026, driven by growing EU 2019/1009 compliant product formulation demand pulling premium-documentation leonardite from established EU-registered sources rather than Chinese commodity supply, and by corn and agricultural energy cost elevation adding logistics cost to US leonardite export supply at Sunflower Humic and Technology and North American Humic. Seaweed extract prices from Acadian Seaplants rose approximately 7.7% in North America on above-plan US horticulture and viticulture biostimulant adoption and growing organic acreage demand. Amino acid hydrolysate prices from Bioiberica and Ilsa rose approximately 8.8% in Europe on protein hydrolysis feedstock cost elevation from elevated European livestock and fish processing by-product commodity prices. Rhizobium inoculant liquid dose pricing from Novozymes BioAg rose approximately 8.9% in Latin America on above-plan Brazilian soybean inoculation adoption and fermentation production cost elevation, with synthetic urea reference pricing rising approximately 11.8% from the Strait of Hormuz natural gas feedstock disruption, widening the cost-benefit advantage of biostimulant nitrogen fixation substitution over synthetic N application in Brazilian soybean economics.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the biostimulant market, the Hormuz disruption creates a dual effect that is net positive for biostimulant adoption economics. The primary impact is synthetic fertiliser cost elevation: natural gas is the primary feedstock for ammonia and synthetic nitrogen fertiliser production, and GCC natural gas export disruption through the Hormuz corridor has elevated European and Asian ammonia and urea production costs, with urea prices rising approximately 11.8% from USD 340 per metric tonne in Q2 2025 to USD 380 per metric tonne in Q2 2026. This cost elevation improves the return-on-investment calculation for biostimulant-based nutrient use efficiency programmes -- each percentage point improvement in nitrogen use efficiency at elevated urea pricing generates greater absolute cost saving per hectare that offsets biostimulant programme cost. The secondary impact is grower budget compression in commodity grain and oilseed production: elevated fertiliser, energy, and logistics costs are compressing operating margins and diverting grower capital toward minimum essential input maintenance, limiting discretionary biostimulant adoption investment in cost-sensitive commodity markets. The net commercial outcome is biostimulant adoption acceleration in high-value horticulture and viticulture where per-hectare economics clearly support programme investment, and adoption deferral in commodity grain and oilseed markets where cost pressure constrains capital for optional programme investment.

Company Insights

The two key dominant companies in the biostimulant market are Valagro (Syngenta) and Novozymes BioAg (dsm-firmenich), recognised for their commercial scale in seaweed extract, amino acid, and microbial biostimulant product portfolios respectively, their established multinational agrochemical distribution integration that enables biostimulant products to reach global grower markets at scale, and their technical leadership in EU 2019/1009 compliant efficacy documentation for key biostimulant product categories.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 4.51 Billion |

| Market Size 2032 | USD 8.54 Billion |

| CAGR | 11.2% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Application Method, By Crop Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, Italy, Spain, Netherlands, UK, China, India, Japan, Brazil, Argentina, South Africa, Morocco |

| Companies Profiled | Valagro/Syngenta, Novozymes BioAg/dsm-firmenich, Acadian Seaplants, UPL, BASF, Bioiberica, Corteva, Bayer CropScience, Tradecorp, Ilsa, Lallemand Plant Care, Rizobacter, Italpollina, Compo Expert, Biolchim |

| Key Data Sources | European Biostimulant Industry Council 2024 annual market report, EU Regulation 2019/1009 EBIC compliance tracking, Syngenta Group 2024 investor disclosures on Valagro integration, Novozymes BioAg 2024 annual investor update Brazilian inoculant volumes, Corteva 2024 Annual Report biological segment, UPL 2024 Annual Report Natural Plant Protection, Acadian Seaplants capacity expansion disclosure Q1 2026, IMF March 2026 Hormuz statement, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 264 |

| Published | Q2 2026 |

| SKU | NXC-AC-002 |

Scope & Methodology

Primary Research

Secondary Research