Market Data

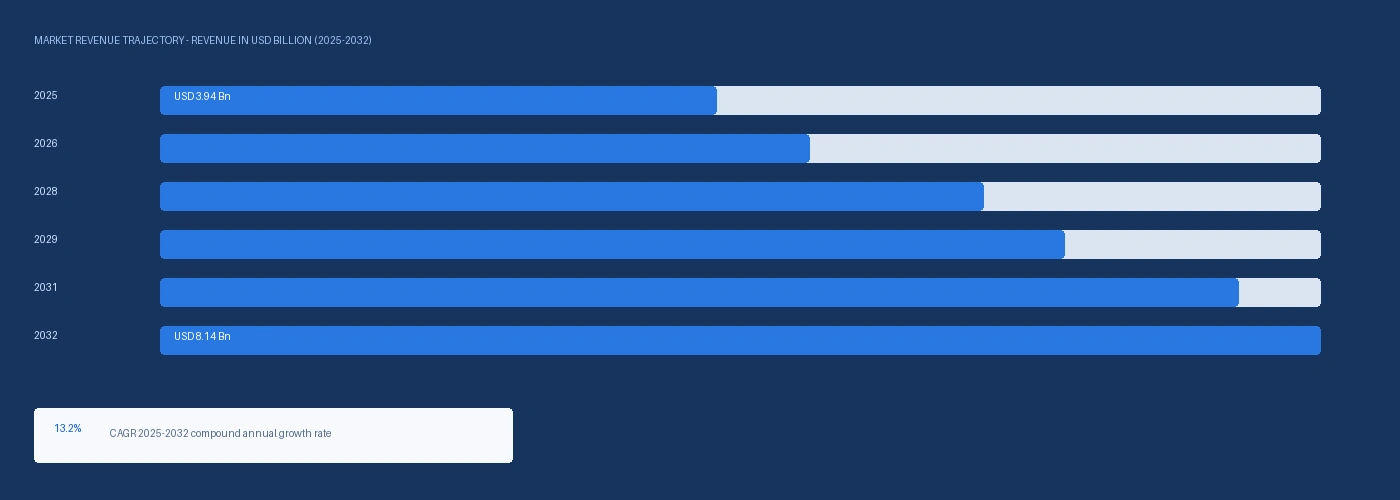

The global biopesticides market size was USD 3.94 Billion in 2025 and is expected to register a revenue CAGR of 13.2% during the forecast period. Market revenue growth is supported by the European Union Farm to Fork Strategy target of a 50% reduction in chemical pesticide use and risk by 2030, EPA biopesticide registration acceleration under the Endangered Species Protection Program compelling US growers to substitute registered conventional chemistries with approved biopesticide alternatives, and the structural expansion of certified organic acreage globally that mandates biopesticide-compatible crop protection inputs across grower supply chains. The EPA maintained approximately 430 registered biopesticide active ingredients across approximately 1,400 biopesticide products as of Q1 2026, the largest regulatory approval base of any major agricultural market globally, confirming the commercial foundation for US market growth. The USDA National Agricultural Statistics Service confirmed US certified organic acreage at approximately 5.5 million acres in 2023, growing at approximately 6% to 8% per year, each additional acre representing a crop protection spending shift away from conventional synthetic chemistries toward microbial and biochemical alternatives. Corteva Agriscience disclosed biologicals at approximately 8% to 10% of its crop protection division revenue in its 2024 Annual Report, equivalent to approximately USD 290 million to USD 360 million, with double-digit segment growth disclosed as a stated strategic priority and biologicals identified as the fastest-growing crop protection sub-category within the Corteva portfolio. Bayer AG disclosed biologicals as a growth priority within Crop Science in its 2024 Annual Report, with a EUR 500 million to EUR 600 million biologicals revenue target disclosed for 2026 against an estimated EUR 280 million to EUR 320 million contribution in 2023 and 2024, implying a compound growth rate in biologicals at Bayer alone materially above the company-wide crop science division growth rate. For instance, in March 2025, Corteva Agriscience, United States, announced a collaboration agreement with Symborg S.L., Spain, for the global commercialisation of Symborg's mycorrhizal bioprotection technology targeting soil-borne pathogen suppression in row crop and specialty crop markets, expanding Corteva's biological crop protection portfolio into soil inoculant-based disease management at commercial scale for the first time. These are some of the key factors driving revenue growth of the market.

Microbial pesticides accounted for approximately 55% to 60% of total biopesticide market revenue in 2025 per EPA registration category analysis, with Bacillus thuringiensis products representing the single largest active ingredient category across registered products in the United States and European Union. Koppert Biological Systems, headquartered in Berkel en Rodenrijs, Netherlands, generated estimated annual revenue of approximately EUR 350 million to EUR 420 million in fiscal year 2023 per Dutch Chamber of Commerce filings, with biopesticides accounting for approximately 60% to 65% of total Koppert revenue from its Trichoderma, Beauveria bassiana, Bacillus subtilis, and predatory insect and mite product lines. UPL Limited disclosed its Natural Plant Protection division at approximately USD 240 million to USD 280 million revenue in its 2024 Annual Report, with growth accelerating in European markets following the EU active substance review programme removing approximately 80 conventional active substances from EU authorisation since 2012, increasing the total addressable market for biopesticide alternatives in EU member state crop protection programmes. Valent BioSciences, a subsidiary of Sumitomo Chemical, is estimated at approximately USD 180 million to USD 220 million revenue from biopesticide product lines based on Sumitomo Chemical 2024 agricultural segment disclosures, supplying microbial insecticides including DiPel Bacillus thuringiensis products and Mycotrol Beauveria bassiana to North American and European professional grower markets. Indian listed biopesticide producers including Biostadt India Limited, with disclosed biopesticide segment revenue of approximately INR 310 crore in fiscal year 2025, and PI Industries with biological product line contributions disclosed in its annual report, confirm that Asian domestic production is scaling independently of multinational company expansion in the region.

However, biopesticide efficacy in high-disease-pressure field conditions remains inconsistent relative to synthetic conventional chemistries in commodity row crop markets, where yield protection requirements create a performance risk tolerance that limits full substitution without integrated resistance management programmes that support continued conventional pesticide use alongside biopesticide incorporation. Supply chain constraints for live microbial organism-based products, including cold chain management requirements, shelf-life limitations of approximately six to twelve months for many liquid Bacillus and Trichoderma formulations, and fermentation production capacity bottlenecks at commercial contract manufacturers, constrain the speed at which market supply can expand to meet accelerating regulatory and organic market demand. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated synthetic fertiliser and agrochemical input costs through natural gas and naphtha feedstock disruption, creating inflationary pressure across the broader crop protection sector that has diverted grower capital allocation from premium-priced biopesticide adoption toward essential conventional input maintenance in cost-constrained commodity grain and oilseed operations. These factors substantially limit biopesticides market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

The European Union Farm to Fork Strategy, establishing a legally binding target of 50% reduction in chemical pesticide use and risk by 2030, is the most consequential demand driver for European biopesticide market growth across the forecast period. The European Commission confirmed in its 2024 progress report that EU member states must submit national action plans with quantified biopesticide adoption pathways by Q1 2026 as a condition of continued Common Agricultural Policy subsidy access, creating a direct financial incentive for grower adoption that is independent of agronomic preference. EFSA approved approximately 28 new biopesticide active substances between 2022 and 2024, the highest two-year approval rate in European regulatory history, reducing the registration timeline gap between biopesticide and conventional pesticide authorisation and making the European market more accessible for new product launches. Syngenta Group disclosed its Bioprotection segment in its 2023 Annual Report with revenue estimated at approximately USD 320 million to USD 380 million, reflecting the company's strategic investment in biological crop protection products targeted at European growers operating under increasing conventional pesticide restriction conditions. The Sustainable Use Regulation under review by the European Parliament as of Q1 2026 would extend Farm to Fork pesticide reduction targets to national crop-specific pesticide use plans, further accelerating the structural demand shift from conventional to biopesticide-compatible crop protection programmes in the EU's 165 million hectare agricultural land base. EPA Biopesticide Registration Acceleration and US Organic Acreage Expansion Driving North American Volume The US EPA Biopesticides and Pollution Prevention Division processed approximately 430 active ingredient registrations and approximately 1,400 product registrations as of Q1 2026, with the average registration timeline for biopesticide active ingredients at approximately 12 to 18 months versus 36 to 48 months for conventional pesticide registrations, reflecting the EPA's reduced data requirement framework for biopesticide applicants that accelerates commercial product launches. The EPA's Endangered Species Protection Program is requiring growers in protected species buffer zones to substitute conventional organophosphate and carbamate active substances with approved biopesticide alternatives for certain crop protection applications, creating a regulatory compulsion for biopesticide adoption in key US fruit and vegetable growing regions in California, Florida, and the Pacific Northwest. USDA NASS confirmed US certified organic acreage at approximately 5.5 million acres in 2023, growing at approximately 6% to 8% per year, translating to approximately 330,000 to 440,000 additional acres of mandatory biopesticide-compatible crop protection demand annually. Certis Biologicals, operating within the Mitsui corporate structure, generated estimated revenue of approximately USD 120 million to USD 150 million in 2024 from its US market biopesticide portfolio including Bacillus subtilis, nuclear polyhedrosis virus, and spinosad products targeted at US specialty crop growers. The US Inflation Reduction Act conservation programme funding allocated approximately USD 19.5 billion to USDA agricultural conservation programmes through 2031, with a proportion supporting organic transition and integrated pest management adoption that provides cost-share funding for grower biopesticide purchases under EQIP and CSP programme structures.

Biopesticide efficacy against high disease and insect pest pressure in commercial commodity row crop environments remains inconsistent relative to synthetic alternatives in field conditions that do not meet optimal temperature, humidity, and UV exposure requirements for microbial product activity, limiting full substitution in corn, soybean, and wheat production systems that account for the majority of global pesticide application volume. Shelf-life constraints for liquid Bacillus thuringiensis, Trichoderma, and Beauveria bassiana formulations at approximately six to twelve months from manufacturing date require cold chain management infrastructure at distribution and retail levels that adds cost and logistical complexity beyond the capabilities of the cooperative and independent agrodealer networks serving smallholder growers in India, sub-Saharan Africa, and Southeast Asia. Fermentation manufacturing capacity for commercial-scale microbial biopesticide production is concentrated at a small number of contract manufacturers in North America and Europe, including Fermic in Mexico and Novozymes fermentation facilities, creating potential supply bottlenecks when multiple product launches and regulatory mandates simultaneously pull fermentation capacity across the biopesticide industry. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated synthetic pesticide and fertiliser input costs through naphtha and natural gas feedstock disruption, diverting cost-pressured commodity row crop growers toward essential conventional input budget maintenance rather than discretionary biopesticide programme adoption, particularly in North American corn and soybean markets where biopesticide penetration remains below 5% of total crop protection spend. These factors substantially limit biopesticides market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Microbial Pesticides, Biochemical Pesticides, Plant-Incorporated Protectants (PIPs), Semiochemicals | Microbial Pesticides |

| Mode of Action | Contact, Systemic, Stomach Poison, Repellent/Deterrent | Contact |

| Crop Type | Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Others | Fruits and Vegetables |

| Application | Foliar Spray, Soil Treatment, Seed Treatment, Post-Harvest | Foliar Spray |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Microbial Pesticides segment is expected to account for a significantly large revenue share in the global biopesticides market during the forecast period.

This report evaluates type across Microbial Pesticides, Biochemical Pesticides, Plant-Incorporated Protectants (PIPs), Semiochemicals for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates mode of action across Contact, Systemic, Stomach Poison, Repellent/Deterrent for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates crop type across Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses, Others for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Foliar Spray, Soil Treatment, Seed Treatment, Post-Harvest for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

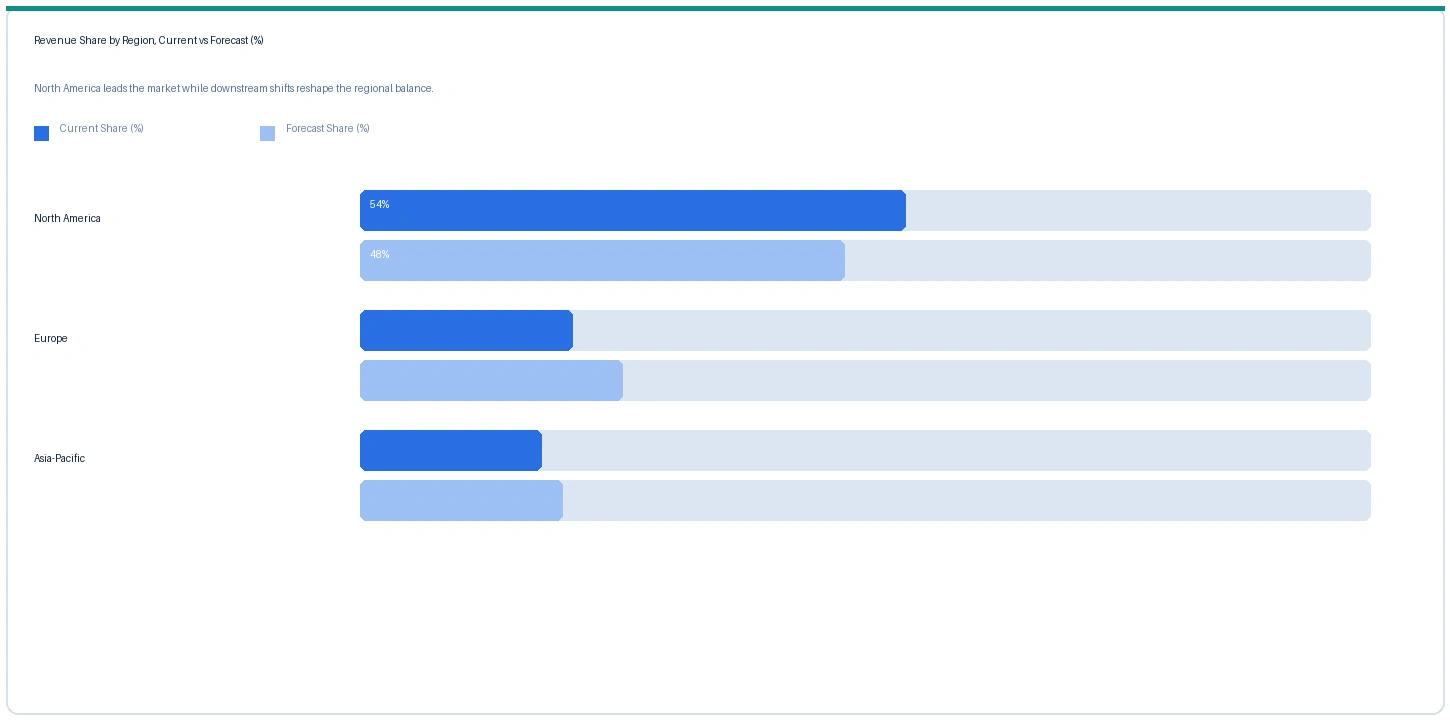

North America market accounted for largest revenue share over other regional markets in the global biopesticides market in 2025. Based on regional analysis, the biopesticides market in North America accounted for the largest revenue share in 2025. The United States EPA biopesticide registration base of approximately 430 active ingredients and 1,400 products is the most extensive regulatory approval framework for biopesticide commercial products in any major agricultural market globally, creating a product availability foundation that supports North American grower adoption across specialty crop, row crop, and organic production systems. Corteva Agriscience disclosed biologicals at approximately 8% to 10% of its Crop Protection division revenue in its 2024 Annual Report, with biologicals identified as the fastest-growing crop protection sub-category at its Iowa-based commercial operations. Valent BioSciences DiPel and Javelin Bacillus thuringiensis products are among the most widely distributed commercial biopesticide brands in North American professional grower markets, distributed through a national network of agricultural cooperative and independent agrodealer channels. US certified organic acreage at approximately 5.5 million acres in 2023 per USDA NASS, growing at 6% to 8% annually, provides the structurally expanding organic production base that mandates biopesticide-compatible crop protection across an increasing land area independent of conventional market adoption cycles.

The market in Europe is expected to register the second largest revenue share in the global biopesticides market. The EU Farm to Fork Strategy 50% pesticide reduction target and the removal of approximately 80 conventional active substances from EU authorisation since 2012 have created the regulatory environment driving European biopesticide adoption at rates materially above the global average. Koppert Biological Systems, headquartered in the Netherlands, generated estimated revenue of approximately EUR 350 million to EUR 420 million in fiscal year 2023, with European commercial agricultural and protected horticulture markets accounting for the majority of its biocontrol and biopesticide product distribution through national dealer networks across Germany, France, Spain, Italy, and the Netherlands. BASF Agricultural Solutions disclosed its biological pest management portfolio, including Nemasys nematicide products and Velondis Metarhizium anisopliae fungal insecticide products, within its European and global crop protection strategy in its 2024 Annual Report, confirming that integrated biopesticide product development is a stated priority within BASF's European regulatory strategy response. EFSA approval of approximately 28 new biopesticide active substances between 2022 and 2024 is reducing the registration timeline gap that historically disadvantaged biopesticide products relative to conventional chemistries in EU member state national authorisation timelines.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global biopesticides market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period. India's Pradhan Mantri Fasal Bima Yojana crop insurance scheme and the Ministry of Agriculture and Farmers Welfare National Mission on Sustainable Agriculture are driving biopesticide adoption in Indian smallholder fruit, vegetable, and cotton farming systems, with the Ministry confirming in its 2024-25 annual report that biopesticide-compatible integrated pest management has been adopted on approximately 4.2 million hectares under national mission programmes. Biostadt India Limited, a listed Indian biopesticide manufacturer, disclosed biopesticide segment revenue of approximately INR 310 crore in fiscal year 2025, confirming the commercial scale of domestic Indian biopesticide manufacturing that is expanding in parallel with government subsidy-linked adoption programmes. Chinese Ministry of Agriculture and Rural Affairs biopesticide substitution mandates, targeting replacement of high-toxicity conventional pesticide active substances with biopesticide alternatives across designated high-risk crop-pest combinations, are creating demand from China's approximately 165 million smallholder farming households through provincial agricultural extension service channels. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated synthetic pesticide input costs in Asian agricultural markets through naphtha and natural gas feedstock disruption at GCC-sourced agrochemical ingredient manufacturers, modestly improving the relative cost competitiveness of domestically produced microbial biopesticide alternatives in India and China.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Bacillus thuringiensis (liquid) | North America | USD 28/kg | USD 25/kg | Rising | Valent/Certis ref |

| Trichoderma harzianum (WP) | Europe | USD 42/kg | USD 38/kg | Rising | Koppert/BASF ref |

| Beauveria bassiana (SC) | North America | USD 38/kg | USD 34/kg | Rising | Certis Biologicals |

| Bacillus subtilis (WP) | Asia-Pacific | USD 22/kg | USD 19/kg | Rising | Domestic Indian prod. |

| Pheromone mating disruption | Europe | USD 180/ha | USD 162/ha | Rising | Suterra/Koppert ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and agricultural chemical trade publication monitoring. Biopesticide products are priced per kilogram of formulated product and are not exchange traded. Prices vary by active ingredient, formulation type, certification status, contract volume, and regional registration conditions.

Biopesticide product prices are rising across all key categories and regions in Q2 2026, driven by fermentation capacity utilisation above 85% at major contract manufacturers including Fermic in Mexico and Novozymes biological production facilities, increasing raw material costs for fermentation substrates including molasses and corn steep liquor from elevated agricultural commodity prices, and the conversion of EU Farm to Fork regulatory pressure into committed volume purchase orders from European grower cooperatives and integrated fresh produce supply chains that are pulling formulated product from a manufacturing base that has not expanded at equivalent rates. Bacillus thuringiensis liquid product prices rose approximately 12% from USD 25 per kilogram in Q2 2025 to USD 28 per kilogram in Q2 2026 in North American markets, reflecting contracted volume commitments from US certified organic grower associations and from EPA Endangered Species Protection Programme buffer zone compliance purchase requirements at California vegetable operations. European Trichoderma harzianum prices rose approximately 10.5% against Q2 2025, with Koppert and BASF Agricultural Solutions supply commitments to EU member state grower cooperatives under national action plan adoption programmes absorbing available commercial supply from established production facilities. Asian domestic Bacillus subtilis pricing from Indian manufacturers rose approximately 15.8% against Q2 2025, reflecting growing domestic demand from government-subsidised biopesticide adoption programmes without commensurate domestic fermentation capacity expansion.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the biopesticides market, the Hormuz disruption operates through two distinct channels. The primary channel is synthetic agrochemical input cost elevation: conventional pesticide active ingredient manufacturing in India, China, and Europe relies on naphtha-derived solvents and intermediate chemicals whose costs are elevated by the Hormuz-driven naphtha price increase, raising the total cost of synthetic pesticide programmes to growers and marginally improving the relative cost competitiveness of microbial biopesticide alternatives in integrated pest management programme economics at the farm gate. The secondary channel is agricultural energy and fertiliser cost inflation: elevated LNG prices from the Hormuz disruption are increasing natural gas costs for nitrogen fertiliser production in Europe and South Asia, compressing grower operating margins in commodity grain and oilseed production systems and redirecting grower capital allocation toward essential input maintenance, which limits discretionary spending on premium-priced biopesticide programme adoption in cost-sensitive commodity markets. The net effect is modestly positive for biopesticide adoption in high-value specialty crop markets where the relative cost advantage over synthetic alternatives is improving, and mildly negative in commodity row crop markets where grower budget pressure is deferring non-essential input category investment.

Company Insights

The two key dominant companies in the biopesticides market are Koppert Biological Systems and Valent BioSciences, recognised for their leadership in commercial-scale microbial biopesticide manufacturing and distribution, their established grower and commercial agriculture market relationships spanning multiple crop categories and regions, and their technical depth in biological active ingredient development and regulatory registration across major global agricultural markets.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 3.94 Billion |

| Market Size 2032 | USD 8.14 Billion |

| CAGR | 13.2% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Mode of Action, By Crop Type, By Application, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Netherlands, Spain, Italy, China, India, Japan, Brazil, Argentina, South Africa, Morocco |

| Companies Profiled | Koppert Biological Systems, Valent BioSciences, Certis Biologicals, Bayer AG, Corteva Agriscience, Syngenta Group, BASF SE, UPL Limited, Andermatt Group, Marrone Bio Innovations (Bioceres), Biostadt India, BioWorks, FMC |

| Key Data Sources | EPA FIFRA biopesticide registration database Q1 2026, USDA NASS organic acreage statistics 2023, EFSA active substance approval records 2022-2024, Corteva and Bayer 2024 Annual Reports, Koppert Dutch Chamber of Commerce filings, IBMA biocontrol market assessment 2023, FAO pesticide market analysis, IMF March 2026 Hormuz statement, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 268 |

| Published | Q2 2026 |

| SKU | NXC-AC-001 |

Scope & Methodology

Primary Research

Secondary Research