Market Data

The global bioherbicides market size was USD 3.28 Billion in 2025 and is expected to register a revenue CAGR of 13.4% during the forecast period. Market revenue growth is supported by confirmation that more than 250 weed species now resist at least one synthetic herbicide mode of action costing growers USD 43 billion per year in lost yield and additional inputs, providing a structural commercial case for bioherbicides that operate through biochemical pathways distinct from conventional synthetic herbicide modes of action, Brazil's bio-input sales reaching BRL 5 billion equivalent to approximately USD 1 billion in 2024 with soybean crops alone accounting for over half of domestic biological herbicide volumes as Brazilian farmers integrate bioherbicides into cropping programmes to maintain export certifications and avoid maximum residue limit violations in European and North American destination markets, and the US EPA's Biopesticides and Pollution Prevention Division providing streamlined registration pathways for biologically derived herbicide active substances that reduce the regulatory timeline and cost compared to new synthetic herbicide active substance registration, accelerating the commercialisation timeline for bioherbicide startups and specialty agricultural biologicals companies. Marrone Bio Innovations, acquired by Bioceres Crop Solutions and maintaining its biologicals-exclusive positioning, holds approximately 14% to 17% market share in bioherbicides through its plant alkaloid and microbial strain-based product lines targeting broadleaf weeds in specialty crops, with over 20 registered bioherbicide products in more than 10 countries per company disclosures and international licensing arrangements advancing its distribution reach. Bayer CropScience AG holds approximately 8% to 10% global bioherbicide market share with over 30 bioherbicide patents filed by 2024 and 15 global registrations, collaborating with research institutions and startups to advance bioherbicide development alongside its conventional herbicide portfolio as part of its broader integrated weed management strategy. Harpe Bioherbicide Solutions confirmed completion of over 1,000 greenhouse and field trials on more than 30 resistant weed species by 2024 while advancing EPA registration filings, demonstrating the commercial development momentum in bioherbicide products targeting herbicide-resistant weed populations. For instance, in April 2024, Seipasa, Spain, readied a novel bioherbicide following joint research with the Polytechnic University of Valencia to address declining synthetic herbicide options in EU markets under regulatory restrictions, confirming European company investment in bioherbicide development as the EU Farm to Fork Strategy targets 50% reduction in pesticide use and risk by 2030. These are some of the key factors driving revenue growth of the market.

Brazil's role in bioherbicide market development is structurally important because the country's bio-input market reached BRL 5 billion in 2024 under the national biological input regulatory framework coordinated by the Brazilian Ministry of Agriculture, Livestock and Food Supply, with soybean production systems accounting for over half of domestic biological herbicide volumes and representing the first large-scale demonstration that bioherbicides can be integrated into major commodity crop programmes at scale comparable to conventional herbicide use rates. The US bioherbicide market reached approximately USD 761.6 million in 2024 with the United States accounting for approximately 78.7% of the North American bioherbicides market, driven by organic farming certification requirements that prohibit synthetic herbicide use, retailer sustainability programmes at Walmart, Target, and Whole Foods requiring residue-free produce supplier documentation, and US EPA biopesticide registration pathways that have approved a growing portfolio of microbial and biochemical weed control products under reduced-risk criteria. FMC Corporation and Micropep Technologies announced a collaboration in December 2022 to develop peptide-based micro RNA bioherbicides that silence specific weed gene expression without chemical residues, confirming that bioherbicide technology is advancing from established mycoherbicide and allelopathic extract products into RNA-based precision weed gene silencing approaches that could enable species-specific weed control impossible with broad-spectrum synthetic herbicides. These are some of the key factors driving revenue growth of the market.

However, bioherbicides typically demonstrate slower weed kill speed than synthetic herbicides, with mycoherbicide and bacterial bioherbicide products often requiring 7 to 21 days for visible weed control compared to 3 to 7 days for glyphosate and other conventional synthetic herbicides, making bioherbicide adoption challenging in high-value cropping systems where rapid weed elimination is required to prevent yield loss from weed competition in the critical canopy closure period. Field performance consistency of bioherbicides is sensitive to temperature, humidity, and UV exposure at application, with performance variability across different growing conditions a key limitation cited by growers in extension trials, particularly in arid and semi-arid environments where the moisture requirements of mycoherbicide spore germination are not consistently met during field application windows. These factors substantially limit bioherbicides market growth over the forecast period.

Industry Trends & Market Dynamics

More than 250 weed species now resistant to at least one synthetic herbicide mode of action and Harpe Bioherbicide Solutions completing over 1,000 trials on 30 resistant weed species while advancing EPA registration confirm that herbicide resistance has moved from an agronomic inconvenience to a structural market access problem that bioherbicides are uniquely positioned to address through entirely different biochemical pathways

More than 250 weed species now resist at least one synthetic herbicide mode of action globally, costing growers USD 43 billion per year in lost yield and additional weed control inputs as resistance mechanisms spread through weed populations exposed to repeated applications of the same active substance classes. Glyphosate-resistant goosegrass confirmed in Japan via EPSPS gene mutations in 2024, palmer amaranth with multiple resistance mechanisms across the US cotton and soybean belt, and waterhemp with resistance to five or more herbicide modes of action in the US corn-soybean rotation system represent the weed species where bioherbicide efficacy on resistant biotypes provides growers with a weed control option that does not accelerate the resistance mechanisms that have made synthetic herbicides ineffective. Bioherbicides operate through living organisms or biologically derived compounds that suppress weed growth through mechanisms including pathogen infection of weed tissue, release of phytotoxic secondary metabolites, or competitive allelopathy, providing biochemical modes of action distinct from all synthetic herbicide mode-of-action classes and therefore not subject to cross-resistance with existing synthetic herbicide resistance. Harpe Bioherbicide Solutions' confirmation of efficacy on more than 30 resistant weed species across over 1,000 greenhouse and field trials by 2024, while advancing EPA registration filings, provides the most commercially advanced evidence base for bioherbicide efficacy specifically on herbicide-resistant weed populations that is the most commercially valuable attribute for growers managing resistance in their fields. EU Farm to Fork 50% Pesticide Reduction Target and Brazil Bio-Input Framework Driving Regulatory-Backed Market Development The European Commission's Farm to Fork Strategy, adopted as part of the European Green Deal, targets a 50% reduction in the use and risk of synthetic pesticides including herbicides by 2030 compared to the 2015 to 2017 average, creating a regulatory framework in which EU member states are progressively restricting synthetic herbicide approvals and extending biologically based weed control product registrations to maintain effective weed management options for European farmers. EU Regulation 2019/1009, which establishes a harmonised framework for EU fertilising products and supports biological input products, and updated EU biopesticide approval guidelines that provide dedicated assessment criteria for microbial and biochemical weed control products, are creating the regulatory infrastructure for bioherbicide market development in the European Union as synthetic herbicide active substances face increasing non-renewal at EU re-evaluation. Brazil's Ministry of Agriculture, Livestock and Food Supply coordinates the national biological input framework under which bio-input sales reached BRL 5 billion in 2024, with soybean biological herbicide integration driven by export market maximum residue limit compliance requirements for Brazilian soybeans sold to European Union and Chinese buyers who specify maximum residue limits below what intensive synthetic herbicide use programmes generate. India's Central Insecticides Board regulates bioherbicide approvals under revised biological input guidelines introduced after 2020, creating a domestic registration pathway for bioherbicide products in Indian crop protection markets where organic farming certification programmes and government pesticide use reduction initiatives are creating initial commercial demand for biological weed control alternatives.

Mycoherbicide and bacterial bioherbicide products typically require 7 to 21 days for visible weed control after field application as the biological agent colonises and develops in weed tissue, compared to 3 to 7 days for conventional glyphosate and post-emergence synthetic herbicides, making bioherbicide adoption challenging in corn, soybean, and wheat production systems where weed control in the first 30 days post-emergence is critical to preventing yield loss from weed competition before canopy closure. Performance variability across temperature, humidity, and UV conditions creates inconsistent field results particularly in arid environments where mycoherbicide spore germination requires moisture conditions not consistently present at application timing windows, reducing grower confidence in bioherbicide reliability compared to conventional herbicides whose performance is weather-independent within normal application ranges. The production shelf life of microbial bioherbicide formulations is shorter than synthetic herbicide concentrates, typically 12 to 24 months refrigerated versus 3 to 5 years at ambient temperature for conventional herbicides, adding cold chain distribution cost and inventory management complexity for agricultural input distributors handling bioherbicide products alongside conventional agrochemical portfolios. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated fermentation substrate and bioreactor energy costs for microbial bioherbicide producers in Europe and Asia from elevated natural gas and LNG prices, adding approximately USD 8 to USD 15 per litre of microbial bioherbicide concentrate to production cost above the 2024 baseline. These factors substantially limit bioherbicides market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Mycoherbicides, Bacterial Bioherbicides, Phytotoxin-Based Bioherbicides, Allelopathic Extract Bioherbicides | Mycoherbicides |

| Application | Agricultural Crops, Turf and Ornamental Grass, Non-Crop Areas and Rights-of-Way, Aquatic Weed Management | Agricultural Crops |

| Crop Type | Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Specialty Crops, Pasture and Forage | Cereals and Grains |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Mycoherbicides segment is expected to account for a significantly large revenue share in the global bioherbicides market during the forecast period.

This report evaluates type across Mycoherbicides, Bacterial Bioherbicides, Phytotoxin-Based Bioherbicides, Allelopathic Extract Bioherbicides for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Agricultural Crops, Turf and Ornamental Grass, Non-Crop Areas and Rights-of-Way, Aquatic Weed Management for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates crop type across Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Specialty Crops, Pasture and Forage for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

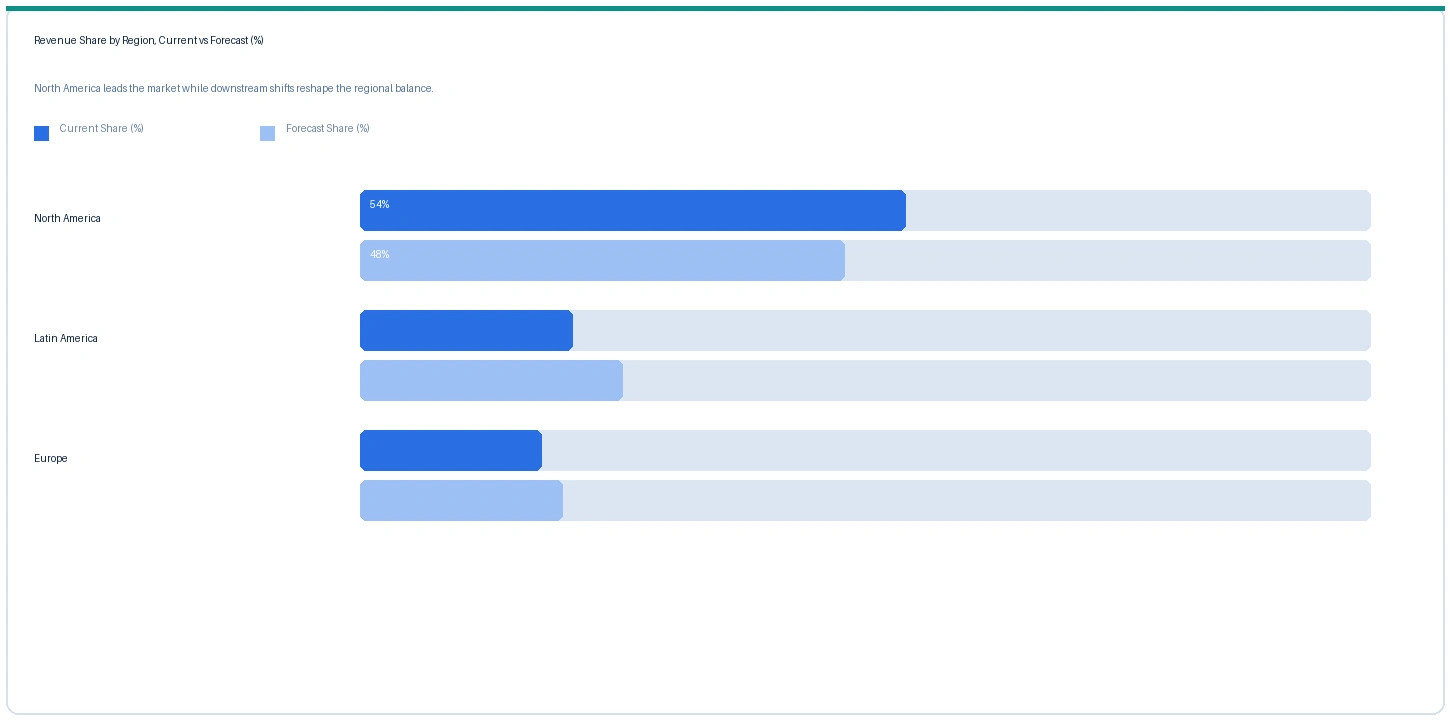

North America market accounted for largest revenue share over other regional markets in the global bioherbicides market in 2025. Based on regional analysis, the bioherbicides market in North America accounted for largest revenue share in 2025 at approximately 35% of global revenue. The US bioherbicide market reached approximately USD 761.6 million in 2024 with the US accounting for approximately 78.7% of the North American market, supported by US EPA Biopesticides and Pollution Prevention Division streamlined registration pathways, established organic farming certification requirements under the USDA National Organic Program prohibiting synthetic herbicides, and Marrone Bio Innovations, Harpe Bioherbicide Solutions, and Certis Biologicals commercial product portfolios serving North American specialty crop and commodity crop growers. The US confirmed herbicide resistance in palmer amaranth, waterhemp, and Japanese stiltgrass across major row crop states, creating structural commercial demand for bioherbicide resistance management tools.

Latin America market is expected to register the fastest revenue growth rate in the global bioherbicides market during the forecast period. The market in Latin America is expected to register the fastest revenue growth rate over the forecast period, driven by Brazil's bio-input market reaching BRL 5 billion equivalent to approximately USD 1 billion in 2024 under the national biological input regulatory framework, with soybean biological herbicide integration driven by EU and China maximum residue limit compliance requirements for Brazilian soy exports. Brazil had the most comprehensive government-supported biological input development programme globally in 2024 per the Brazilian Ministry of Agriculture framework, with producer cooperatives and major agrochemical distributors actively incorporating bioherbicide products into integrated weed management programmes for soybean, corn, and sugarcane production systems.

The market in Europe is expected to register the third largest revenue share with accelerating growth through the forecast period from EU Farm to Fork Strategy regulatory pressure. Seipasa Spain's April 2024 bioherbicide registration programme following research with the Polytechnic University of Valencia, Belchim Crop Protection Belgium's bioherbicide portfolio, and Koppert Biological Systems Netherlands' expansion into biological weed management products confirm European commercial development momentum. EU Regulation EU 2019/904 and the Farm to Fork 50% pesticide use reduction target create the policy framework driving bioherbicide adoption as synthetic herbicide options narrow through non-renewal at EU re-evaluation. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated fermentation energy costs for European microbial bioherbicide producers through elevated natural gas prices.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Mycoherbicide (Colletotrichum-based) | North America | USD 38/ha | USD 34/ha | Rising | Commercial formulation ref |

| Bacterial bioherbicide (Harpe-type) | North America | USD 44/ha | USD 40/ha | Rising | Pre-commercial ref |

| Phytotoxin bioherbicide (plant extract) | Europe | USD 52/ha | USD 47/ha | Rising | EU organic crop ref |

| Allelopathic extract formulation | Asia-Pacific | USD 28/ha | USD 25/ha | Rising | Rice crop ref |

| Synthetic glyphosate (benchmark) | Global | USD 8/ha | USD 7/ha | Stable | Conventional ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty materials trade publication monitoring.

Mycoherbicide application cost per hectare rose approximately 11.8% from USD 34 per hectare in Q2 2025 to USD 38 per hectare in Q2 2026, reflecting rising fermentation production costs from elevated natural gas energy prices at European and North American bioreactor facilities linked to the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, combined with increasing US grower demand in markets with confirmed glyphosate-resistant weed populations pulling available mycoherbicide supply above production expansion rates. Bacterial bioherbicide pre-commercial pricing rose approximately 10% to USD 44 per hectare as Harpe Bioherbicide Solutions advanced EPA registration filings and commercial preparation following its 1,000-plus trial programme, with pricing reflecting the premium resistance management value over conventional herbicides rather than production cost parity. Phytotoxin-based bioherbicides in European organic crop markets rose approximately 10.6% to USD 52 per hectare from EU Farm to Fork demand growth. The synthetic glyphosate benchmark remained stable at approximately USD 7 to USD 8 per hectare from continued Chinese generic glyphosate oversupply, sustaining the price premium of bioherbicides over conventional alternatives that limits adoption in purely price-sensitive commodity crop programmes.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the bioherbicides market, the Hormuz disruption operates primarily through elevated natural gas prices at European and North American bioreactor fermentation facilities that produce microbial bioherbicide concentrate, adding approximately USD 8 to USD 15 per litre of microbial bioherbicide concentrate to production cost above the 2024 baseline from increased fermentation energy costs. GCC agricultural markets dependent on imported bioherbicide products from North America and Europe face elevated logistics costs of approximately 8% to 12% on delivered bioherbicide product cost from Hormuz-linked shipping cost increases, creating a modest incentive for GCC agricultural ministries to develop domestic biological input registration frameworks and local production partnerships to reduce import dependence for biological crop protection inputs.

Company Insights

The two key dominant companies in the bioherbicides market are Marrone Bio Innovations (Bioceres Crop Solutions) and Bayer CropScience AG, recognised for their commercial leadership, certified production scale, and global customer reach.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

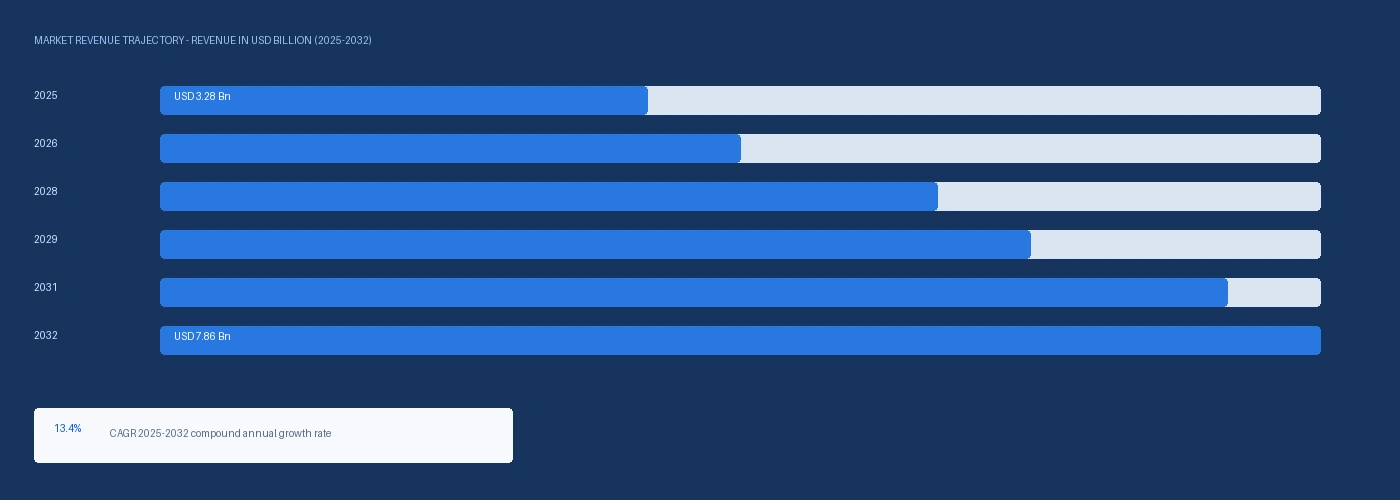

| Market Size 2025 | USD 3.28 Billion |

| Market Size 2032 | USD 7.86 Billion |

| CAGR | 13.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Application, By Crop Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Brazil, Germany, France, Netherlands, Spain, UK, China, India, Japan, Australia |

| Companies Profiled | Marrone Bio Innovations, Bayer CropScience, Harpe Bioherbicide Solutions, Belchim Crop Protection, Koppert Biological Systems, Seipasa, Certis Biologicals, FMC Corporation, BioHerbicides Australia |

| Key Data Sources | 250+ weed species resistant to at least one herbicide mode of action and USD 43 billion annual grower cost confirmed, Harpe Bioherbicide Solutions 1,000+ trials on 30 resistant species and EPA registration filing confirmed, Brazil bio-input BRL 5 billion USD 1 billion 2024 confirmed from Brazilian Ministry of Agriculture, US bioherbicide USD 761.6 million 2024, Bayer 30+ bioherbicide patents and 15 global registrations by 2024, Marrone Bio Innovations 20+ registered bioherbicide products 10+ countries, Seipasa April 2024 bioherbicide registration programme, FMC Micropep December 2022 RNA bioherbicide collaboration, Bayer March 2025 Vyconic soybean launch, EU Farm to Fork 50% pesticide reduction target, India Central Insecticides Board revised biological guidelines post-2020, IMF March 2026 Strait of Hormuz statement, 12 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 268 |

| Published | Q2 2026 |

| SKU | NXC-PC-023 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 12 expert interviews conducted between January and May 2026. Supply-side contacts included bioherbicide product managers and commercial agronomists at North American and European biological weed management companies, bioherbicide fermentation production managers, and EPA biopesticide registration specialists with experience in mycoherbicide and bacterial bioherbicide submissions. Demand-side contacts included agronomists and crop production specialists at Brazilian soybean and corn operations integrating bioherbicides for export MRL compliance, organic farm managers in the United States and Europe specifying bioherbicide programmes for certification compliance, and integrated pest management consultants evaluating bioherbicide resistance management tools for conventional commodity crop programmes. Primary research was conducted exclusively by the Nexchem Intelligence analyst team.

Secondary research sources include Harpe Bioherbicide Solutions 1,000+ trial programme and EPA registration filing confirmation, Seipasa April 2024 bioherbicide registration announcement with Polytechnic University of Valencia, Marrone Bio Innovations April 2024 next-generation bioherbicide launch, Bayer March 2025 Vyconic soybean launch and bioherbicide integration strategy, FMC Corporation and Micropep Technologies December 2022 RNA bioherbicide collaboration, Brazil Ministry of Agriculture biological input framework BRL 5 billion 2024 bio-input market, EU Farm to Fork Strategy 50% pesticide reduction target, India Central Insecticides Board revised biological input guidelines post-2020, US EPA Biopesticides and Pollution Prevention Division streamlined registration framework, confirmed 250+ herbicide-resistant weed species USD 43 billion annual cost data, and the IMF March 2026 Strait of Hormuz statement. No figures from syndicated market research publishers are used as source data.