Market Data

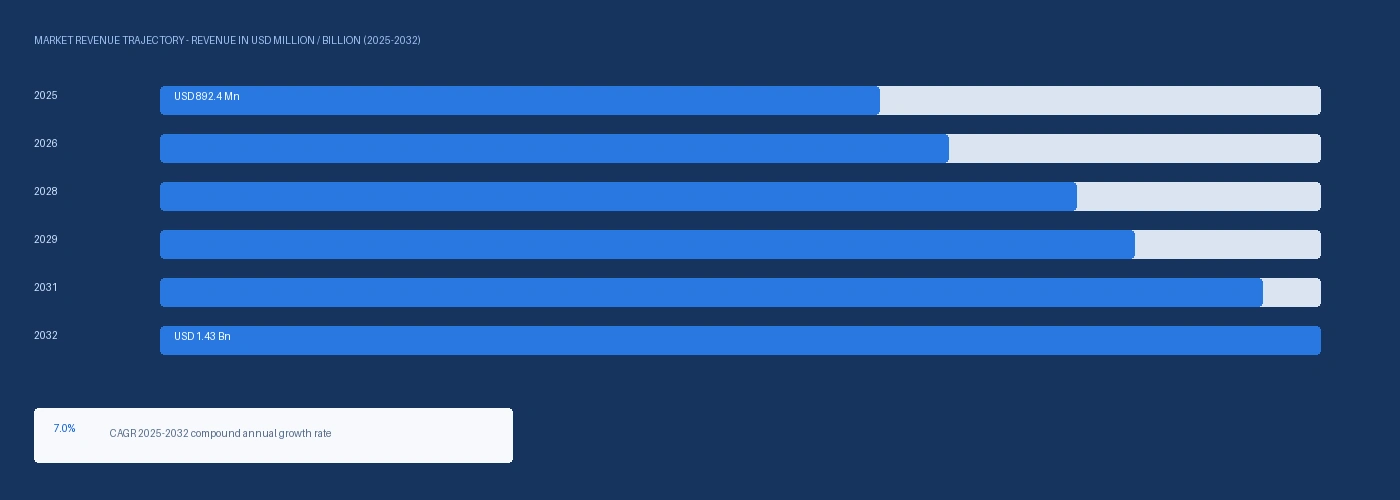

The global bio plasticizer market size was USD 892.4 Million in 2025 and is expected to register a revenue CAGR of 7.0% during the forecast period. Market revenue growth is supported by EU REACH Annex XVII restriction of four phthalates including DEHP, DBP, BBP, and DIBP at 0.1% by weight in plasticised articles converting voluntary phthalate substitution into a compliance obligation at medical device, toy, packaging, and consumer goods manufacturers across European and North American supply chains, Cargill's integrated soybean oil-to-ESBO production capability following its September 2021 acquisition of Arkema's epoxides business in Kankakee, Illinois providing the most cost-integrated ESBO supply chain globally for food packaging and medical device PVC stabiliser applications, and Evonik Oxeno's October 2024 announcement of a significant capacity expansion for ELATUR CH and ELATUR DINCD at its Marl Chemical Park facility confirming producer capital commitment to growing bio-attributed DINCH demand from sensitive application PVC manufacturers. The American Chemistry Council confirmed US plasticizer consumption in PVC applications at approximately 1.1 million metric tonnes in 2024, of which bio-based and non-phthalate alternatives captured an estimated 14% to 17% of volume as REACH-equivalent state regulations in California and Washington extended phthalate restriction obligations to US consumer goods manufacturers supplying EU-market customers. ECHA REACH Annex XVII confirmed that the restriction on DEHP, DBP, BBP, and DIBP in plasticised materials at 0.1% by weight in articles applies from January 2020 onward for consumer applications and extended to medical devices under the EU Medical Devices Regulation with SCHEER completing its benefit-risk assessment in 2023. Jungbunzlauer, headquartered in Basel, Switzerland, produces citrate ester bio plasticizers including triethyl citrate, acetyl triethyl citrate, and acetyl tributyl citrate from citric acid derived by fermentation at its Austrian and Swiss production facilities, supplying medical PVC tubing manufacturers and toy producers who cannot use DEHP and require citrate-based alternatives with documented biocompatibility. For instance, in October 2024, Evonik Industries, Germany, announced a significant capacity expansion for its ELATUR CH and ELATUR DINCD phthalate-free plasticizers at its Marl Chemical Park facility, adding bio-attributed mass-balance certified production capability for pharmaceutical and sensitive-application PVC manufacturers requiring REDcert2-documented bio-based plasticizer supply under the BASF and Evonik Oxeno BMB product certification frameworks. These are some of the key factors driving revenue growth of the market.

Epoxidised soybean oil accounts for approximately 34% of total global bio plasticizer volume in 2025, with Cargill at Kankakee, Illinois and CHS Inc. in the United States operating the largest integrated soybean oil-to-ESBO production units globally following Cargill's Arkema epoxides acquisition. ESBO was indicatively priced at USD 1,140 per metric tonne in Asia-Pacific and USD 1,280 per metric tonne in Europe in Q2 2026, increases of approximately 7.5% and 8.5% respectively against Q2 2025 levels, driven by FDA 21 CFR 178 food contact compliance demand for ESBO as a PVC gasket plasticiser and heat stabiliser in metal can closures and the ECHA Medical Devices Regulation SCHEER assessment increasing documented DEHP alternatives requirements in EU healthcare PVC. Citrate ester bio plasticizers including acetyl tributyl citrate commanded USD 2,640 per metric tonne in Europe in Q2 2026, a USD 1,360 per metric tonne premium above ESBO reflecting the pharmaceutical and toy REACH compliance certification premium and the Jungbunzlauer fermentation-derived citric acid feedstock cost structure at its Ludenburg, Austria facility. BASF SE launched its Hexamoll DINCH BMB, Palatinol N BMB, Palatinol 10-P BMB, and Plastomoll DOA BMB bio-attributed plasticizer range under REDcert2 mass balance certification, with feedstock substitution from bio-naphtha or biogas from organic waste and vegetable oils, confirmed as commercially available across European markets by Q1 2025. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated soybean oil logistics and energy costs in the US Midwest through diesel price pass-through, contributing to ESBO price increases and reinforcing the domestic bio-manufacturing investment rationale for BASF and Evonik Oxeno at their European Marl and Ludwigshafen facilities.

However, the bio plasticizer market is constrained by soybean oil price volatility that has ranged from approximately USD 780 to USD 1,280 per metric tonne between 2022 and 2025 per USDA Economic Research Service commodity price series, creating ESBO production cost uncertainty of approximately USD 180 to USD 350 per metric tonne of finished ESBO that makes long-term fixed-price supply contracts difficult for Cargill, CHS, and Asian ESBO producers to offer at commercial pricing below the risk management threshold of medical device and food packaging buyers. Regulatory complexity in Asia-Pacific, where China GB standards for PVC plasticizers and Japan METI chemical substance controls have not adopted REACH-equivalent phthalate restriction timelines, creates a two-tier market in which Asian LLDPE and PVC compounders continue purchasing lower-cost DEHP and DINP while EU-export-facing manufacturers absorb the bio plasticizer premium, constraining the pace of Asian volume growth below the European conversion rate. These factors substantially limit bio plasticizer market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

ECHA REACH Annex XVII Entry 51 restricts DEHP, DBP, BBP, and DIBP at 0.1% by weight individually or in combination in any plasticised material in articles placed on the EU market, with the restriction applying from January 2020 for consumer applications and extending progressively to food contact, medical devices, and electrical equipment under coordinated EU regulatory frameworks. SCHEER published its benefit-risk assessment on DEHP in medical devices in 2023, confirming that non-phthalate alternatives including citrate esters and ESBO are technically viable for the majority of flexible PVC medical device applications, removing the primary technical uncertainty that had allowed medical device manufacturers to claim exemption under the 2015 Medical Devices Directive. The ECHA investigation report published in November 2023 under the EU Chemicals Strategy for Sustainability examined PVC plasticiser applications, confirming the regulatory review basis for potential further restrictions that are driving European PVC compounders to qualify bio-based alternatives ahead of potential future restriction entries affecting DINP and DPHP that currently hold primary plasticiser status. The American Chemistry Council confirmed that REACH-equivalent state regulations in California under Proposition 65 and Washington under the Children's Safe Products Act have extended phthalate restriction obligations to US manufacturers producing consumer goods for European market export, creating a demand pull for ESBO and citrate ester bio plasticizers at US-based PVC compounders serving dual US-EU supply chains. Cargill Integrated Soybean Oil-to-ESBO Value Chain Enabling Cost-Competitive Supply for Food Packaging Cargill's September 2021 acquisition of Arkema's epoxides business including the Kankakee, Illinois production facility gave Cargill end-to-end production capabilities from commodity soybean oil procurement through ESBO synthesis and downstream bio-based plasticizer and polyol formulation at a single integrated site, the first strategic move by a major agricultural commodity processor to capture the full value chain from soy crushing to specialty plasticizer production. Cargill's domestic soybean oil supply chain from its North American crushing network reduces ESBO production cost relative to non-integrated producers, providing a structural pricing advantage that has enabled Cargill to offer ESBO for food packaging PVC gasket and FDA 21 CFR 178-compliant heat stabiliser applications at competitive pricing against Asian ESBO importers. FDA 21 CFR 178 food contact substance regulations permit ESBO as a plasticiser and stabiliser in PVC food contact articles at specified migration limits, with Cargill's Kankakee ESBO carrying the documentation package required for US food packaging compliance that Asian ESBO producers often cannot supply without additional third-party migration testing. The USDA Economic Research Service confirmed US soybean production at approximately 4.46 billion bushels in the 2024 to 2025 marketing year, providing the domestic feedstock availability that supports Cargill's Kankakee integrated production model at the scale required for national food packaging customers.

USDA Economic Research Service data shows US soybean oil prices ranged from approximately USD 0.58 to USD 0.94 per pound between 2022 and 2025, equivalent to USD 1,280 to USD 2,070 per metric tonne, creating a variable ESBO production cost structure where each USD 100 per metric tonne movement in soybean oil translates to approximately USD 110 to USD 130 per metric tonne of ESBO production cost impact. ESBO pricing in Asia-Pacific at USD 1,140 per metric tonne in Q2 2026 does not provide adequate margin for ESBO producers to offer soybean oil price floor guarantees on annual supply agreements, forcing medical device and food packaging buyers to carry commodity price risk in their bio plasticizer procurement or negotiate quarterly pricing reset structures that reduce budget certainty. The ECHA November 2023 investigation report on plasticisers in PVC acknowledged that the EU regulatory process for potential further phthalate restrictions beyond the four currently in Annex XVII Entry 51 would follow the standard restriction development timeline of three to five years, meaning that Chinese, South Korean, and Indian PVC compounders operating below EU REACH compliance jurisdiction face no immediate regulatory driver to incur the bio plasticizer cost premium. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated US Midwest diesel and agricultural energy costs, increasing soybean cultivation and transport costs that are flowing through to soybean oil procurement pricing at Cargill Kankakee and domestic ESBO producers, adding an estimated USD 30 to USD 60 per metric tonne to ESBO production cost above the 2024 baseline and sustaining the upward Q2 2026 ESBO pricing trajectory. These factors substantially limit bio plasticizer market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | ESBO, Citrate Esters, Succinic Acid Esters, Castor Oil-Based, Bio-Attributed DINCH/DINCD | ESBO |

| Application | Flexible PVC, Packaging Films, Medical Devices, Cables and Wires, Consumer Goods, Coated Fabrics | Flexible PVC |

| End Use | Packaging, Building and Construction, Automotive, Healthcare, Consumer Goods, Agriculture | Packaging |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

ESBO segment is expected to account for a significantly large revenue share in the global bio plasticizer market during the forecast period.

This report evaluates product type across ESBO, Citrate Esters, Succinic Acid Esters, Castor Oil-Based, Bio-Attributed DINCH/DINCD for plasticisers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Flexible PVC, Packaging Films, Medical Devices, Cables and Wires, Consumer Goods, Coated Fabrics for plasticisers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Packaging, Building and Construction, Automotive, Healthcare, Consumer Goods, Agriculture for plasticisers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for plasticisers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

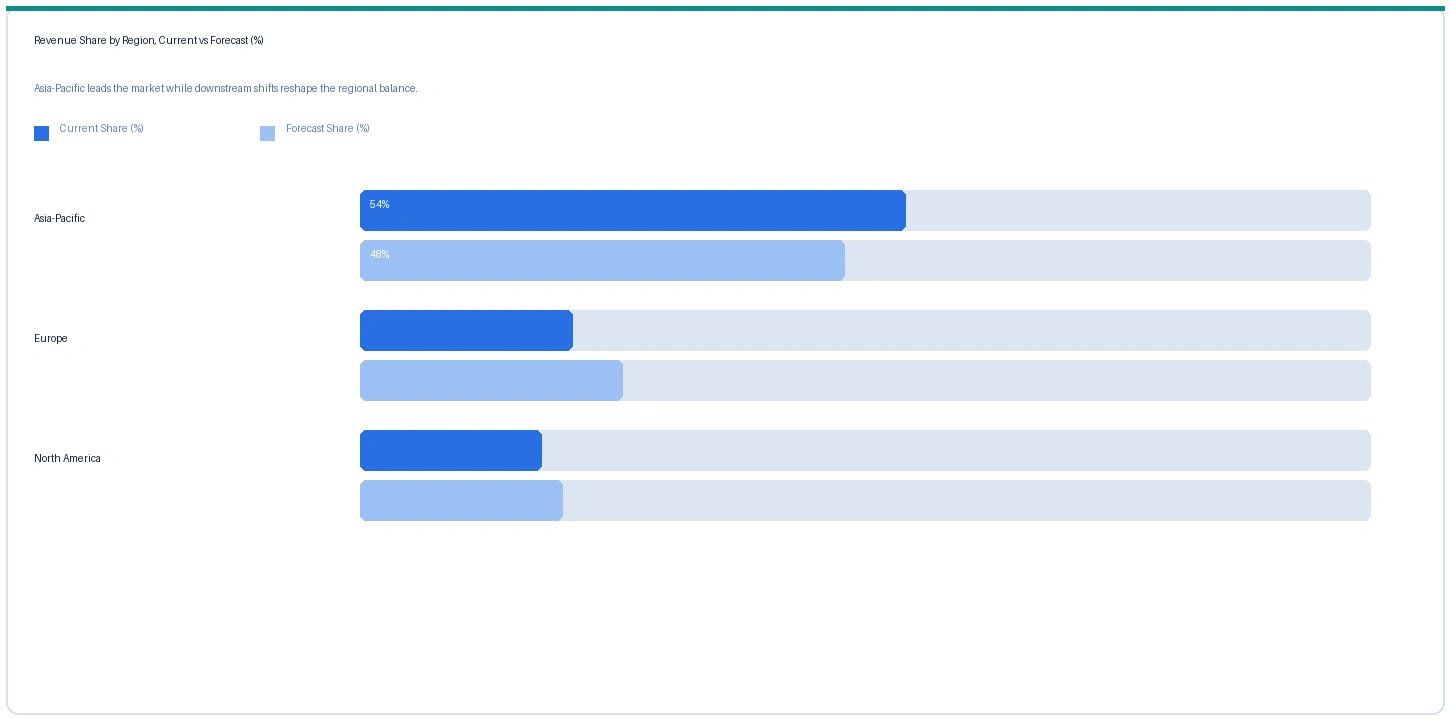

Asia-Pacific market accounted for largest revenue share over other regional markets in the global bio plasticizer market in 2025. Based on regional analysis, the bio plasticizer market in Asia-Pacific accounted for largest revenue share in 2025. China dominates Asia-Pacific bio plasticizer consumption, with Hebei Jingu Plasticizer and Shandong Longkou Longda Chemical among the primary domestic ESBO producers supplying Chinese PVC compounders producing food packaging for EU-export programmes requiring REACH food contact compliance documentation. Chinese PVC film production for food and consumer goods packaging consumed an estimated 65,000 to 85,000 metric tonnes of bio plasticizers including ESBO in 2024, sourced predominantly from domestic Hebei and Shandong province producers at USD 1,060 per metric tonne in Q2 2025 for food-grade ESBO. Japanese medical device PVC manufacturers including Terumo Corporation and Nipro Corporation are the primary Asian demand source for citrate ester bio plasticizers, sourcing Jungbunzlauer ATBC and ATEC through Japanese specialty chemical distributors for PVC tubing and IV bag production under Japan MHLW medical device material compliance requirements that restrict DEHP in specific blood-contact device categories.

The market in Europe is expected to register the second largest revenue share in the global bio plasticizer market. EU REACH Annex XVII Entry 51 is the primary structural demand driver for European bio plasticizer consumption, with BASF SE BMB plasticizers, Evonik Oxeno ELATUR CH, and Jungbunzlauer citrate esters supplying European PVC compounders reformulating away from DEHP and DBP across flooring, medical, packaging, and consumer goods PVC applications. Evonik Oxeno's October 2024 capacity expansion for ELATUR CH at Marl marks the first disclosed European phthalate-free plasticizer capacity investment specifically citing sensitive-application PVC demand growth as the primary commercial rationale, confirming that European bio plasticizer demand is material enough to justify producer capital expenditure at the Marl C4 chemistry complex. The German PVC plasticizer market, the largest in Europe, consumed an estimated 180,000 to 220,000 metric tonnes of total plasticizer in 2024, of which bio-based and non-phthalate alternatives captured an estimated 18% to 24% driven by construction-grade flexible PVC reformulation and medical device compliance conversions.

North America market is expected to register steady revenue growth in the global bio plasticizer market during the forecast period. The market in North America is anchored in ESBO for food packaging applications and citrate esters for medical devices, with Cargill at Kankakee, Illinois as the primary integrated domestic ESBO producer and Vertellus and Jungbunzlauer North American distribution serving medical and toy citrate ester demand. The American Chemistry Council confirmed that REACH-equivalent state regulations in California and Washington are driving reformulation at US manufacturers supplying EU-export consumer goods, creating a compliance-driven demand pull for ESBO and citrate ester bio plasticizers at US PVC compounders that parallels the European REACH-driven substitution dynamic. US Inflation Reduction Act domestic bio-manufacturing investment provisions provide tax incentive support for ESBO capacity investment at domestic sites, reinforcing Cargill's Kankakee strategic position and providing a medium-term policy tailwind for US bio plasticizer supply chain investment.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| ESBO (food-grade) | Asia-Pacific | USD 1,140/MT | USD 1,060/MT | Rising | CHS / Cargill ref |

| ESBO (food-grade) | Europe | USD 1,280/MT | USD 1,180/MT | Rising | Cargill Europe ref |

| Citrate Esters (ATBC) | Europe | USD 2,640/MT | USD 2,440/MT | Rising | Jungbunzlauer ref |

| Bio-Attr. DINCH (mass-bal.) | Europe | USD 2,980/MT | USD 2,740/MT | Rising | BASF / Evonik ref |

| Soybean Oil (benchmark) | Global | USD 960/MT | USD 890/MT | Stable | CBOT feedstock ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty chemical trade publication monitoring. Bio plasticizers are traded under term and spot contracts. Prices vary by product type, certification status, purity grade, contract volume, and regional supply-demand balance.

European ESBO prices rose approximately 8.5% from USD 1,180 per metric tonne in Q2 2025 to USD 1,280 per metric tonne in Q2 2026, driven by tightening certified ESBO allocation following Cargill's shift of Kankakee output toward higher-margin specialty polyol applications for select customer programmes and the ECHA Medical Devices Regulation SCHEER 2023 assessment increasing ESBO qualification demand at European medical PVC manufacturers. Asian ESBO rose approximately 7.5% to USD 1,140 per metric tonne on the same ECHA-driven European export pull tightening Asian spot availability and US Midwest soybean oil cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which added approximately USD 30 to USD 60 per metric tonne to US soybean oil production and logistics costs through diesel price pass-through to agriculture. European citrate ester ATBC prices rose approximately 8.2% from USD 2,440 per metric tonne in Q2 2025 to USD 2,640 per metric tonne in Q2 2026 at Jungbunzlauer contract reference, reflecting growing medical device REACH compliance substitution demand and the premium positioning of fermentation-derived citric acid feedstock relative to petrochemical-derived plasticizer alternatives. Bio-attributed DINCH under mass balance certification at BASF and Evonik rose approximately 8.8% to USD 2,980 per metric tonne in Europe, confirming that the REDcert2 certified mass balance premium over conventional DINCH has widened alongside BASF BMB product range market penetration at European sensitive-application PVC formulators.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the bio plasticizer market, the Hormuz disruption operates through two distinct mechanisms on the supply side. First, US soybean oil production and logistics costs at Cargill Kankakee and CHS Mankato are elevated through diesel and agricultural energy cost pass-through from Hormuz-driven crude oil price elevation, adding approximately USD 30 to USD 60 per metric tonne to ESBO production cost above the 2024 baseline and sustaining Q2 2026 ESBO price increases. Second, synthetic petrochemical feedstock costs for BASF and Evonik Oxeno conventional DINCH and DINP production at Ludwigshafen and Marl are elevated from naphtha cost increases linked to the Hormuz crude oil disruption, increasing the production cost of the conventional phthalate alternatives and inadvertently narrowing the percentage premium of bio-attributed BMB-certified plasticizers over their conventional non-phthalate counterparts. This feedstock cost convergence is commercially beneficial to BASF and Evonik's bio-attributed product line positioning, as the BMB premium over conventional DINCH contracts at the same time demand for certified bio-origin documentation is growing from EU Chemicals Strategy for Sustainability pressure on PVC supply chains.

Company Insights

The two key dominant companies in the bio plasticizer market are BASF SE and Cargill, recognised for their leadership in bio-attributed DINCH mass balance plasticizer production and integrated soybean oil-to-ESBO production respectively, their established supply relationships with European and North American PVC compounders across food packaging, medical device, and sensitive-application flexible PVC end-uses, and their technical leadership in REACH-compliant phthalate alternative documentation and food contact regulatory compliance.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 892.4 Million |

| Market Size 2032 | USD 1.43 Billion |

| CAGR | 7.0% |

| Units | Revenue in USD Million / Billion |

| Segments Covered | By Product Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Netherlands, China, Japan, South Korea, India, Brazil, South Africa |

| Companies Profiled | BASF SE, Cargill, Jungbunzlauer, Evonik Industries, CHS Inc., Lanxess, Avient Corporation, Emery Oleochemicals, Vertellus, Roquette Freres |

| Key Data Sources | ECHA REACH Annex XVII restriction data, USDA Economic Research Service soybean oil price series, Cargill epoxides acquisition disclosures, Evonik Oxeno October 2024 ELATUR capacity expansion, BASF BMB plasticizer product communications, Cosmetics Europe industry data, American Chemistry Council, FDA 21 CFR 178 food contact regulations, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 262 |

| Published | Q2 2026 |

| SKU | NXC-PC-010 |

Scope & Methodology

Primary Research

Secondary Research