Market Data

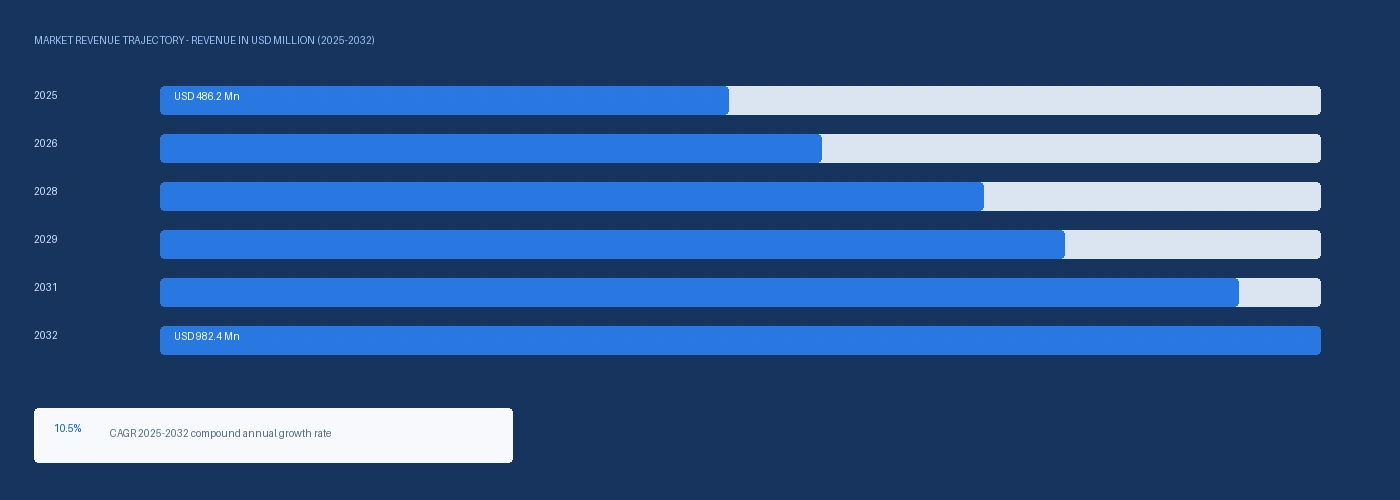

The global bio-based polycarbonate market size was USD 486.2 Million in 2025 and is expected to register a revenue CAGR of 10.5% during the forecast period. Market revenue growth is supported by Covestro AG regularly supplying Makrolon RE polycarbonates with renewable-attributed raw material content of up to 89% under ISCC PLUS mass balance certification from bio-waste and bio-residues, Covestro announcing at Chinaplas 2024 the debut of Makrolon RP polycarbonate using chemically recycled feedstock from post-consumer waste via Neste-provided high-quality recycled feedstock converted to phenol and acetone by Borealis before synthesis into PC at Covestro's production site, and EU Corporate Sustainability Reporting Directive Scope 3 Category 1 purchased goods emissions disclosure requirements from fiscal year 2024 mandating that automotive OEM procurement teams document bio-attributed or recycled material carbon content in polycarbonate components across automotive interior, glazing, and LED lighting systems. Covestro AG, headquartered in Leverkusen, Germany and generating EUR 14.2 billion in 2024 total sales per its annual financial report, is the global number two in polycarbonate with approximately 1,600 kilotonnes annual MDI capacity across nine sites and a polycarbonate business within its Solutions and Specialties segment generating EUR 7.03 billion in segment revenue in 2024. Covestro's Makrolon RE series implements mass balance according to the ISCC PLUS standard with renewable feedstock attributed from bio-waste and residues, delivering up to 89% allocated certified materials and a significantly reduced carbon footprint while maintaining identical material properties and processing characteristics to fossil-based Makrolon grades. Deutsche Telekom confirmed specification of Covestro's renewable-attributed Makrolon RE solution for its GreenMagenta product programme, establishing Makrolon RE as the certified bio-circular polycarbonate in commercial electronics sustainability programmes at major European telecommunications equipment OEMs. Covestro also announced plans to expand its Hebron, Ohio site in the United States with a low triple-digit million euro investment to increase polycarbonate compounding capacity within its Solutions and Specialties segment, with construction scheduled to begin in 2025 and operations starting by end of 2026, targeting differentiated polycarbonate markets in North America where CSRD-equivalent sustainability documentation requirements from European OEM parent companies are pulling bio-circular PC specification. For instance, in April 2024, Covestro, Germany, debuted Makrolon RP polycarbonate at Chinaplas 2024 in Shanghai, the first product in Covestro's portfolio based on chemically recycled attributed material from post-consumer waste via mass balance, produced in cooperation with Neste and Borealis for high-purity applications including automotive and electronics, marking the first commercial introduction of chemically recycled-attributed polycarbonate from the world's leading PC producer. These are some of the key factors driving revenue growth of the market.

Covestro's Makrolon RE product family encompasses Makrolon RE, Makroblend RE, Bayblend RE, and Apec RE product brands, providing bio-circular polycarbonate in standard, blend, and high-heat grades that cover automotive interior trim, electronics housings, medical device casings, and outdoor glazing applications where conventional fossil polycarbonate is the incumbent material. The EPEAT electronics product sustainability assessment tool certified by the US Green Electronics Council recognises ISCC PLUS certified renewable-attributed polycarbonate content as a qualifying environmental attribute, creating a procurement specification pathway for bio-circular PC in IT hardware, telecommunications equipment, and consumer electronics at companies targeting EPEAT Gold registration for their product lines. SABIC has produced bio-circular polycarbonate under its LNP Elcrin iQ series using ISCC PLUS mass balance attribution from bio-waste feedstock, supplying automotive, electronics, and medical device OEMs with bio-attributed engineering-grade polycarbonate blends where ISCC PLUS certification provides the chain-of-custody documentation required for CSRD supplier emissions data packages. Mitsubishi Chemical Group, within its Engineering Plastics division, has developed bio-based polycarbonate grades from isosorbide-based diol monomers derived from corn starch glucose hydrogenation as part of its Durabio engineering bioplastic range, providing a genuinely intrinsically bio-based polycarbonate route distinct from mass-balance attributed fossil production, with Durabio positioned in optical and high-clarity applications where isosorbide-based PC provides higher Abbe number and improved UV resistance compared to bisphenol A-based fossil polycarbonate. These are some of the key factors driving revenue growth of the market.

However, bio-based polycarbonate is commercially concentrated in mass-balance attributed ISCC PLUS certified grades rather than intrinsically bio-based polycarbonate from bio-derived bisphenol A or alternative bio-based diol monomers, meaning that the bio-carbon content in current commercial bio-circular PC is a mathematical chain-of-custody attribution rather than a physically traceable renewable molecule in the polymer chain, which creates ongoing questions from life-cycle assessment auditors and CSRD disclosers about whether mass-balance bio-circular PC meets the full scientific rigour required for Scope 3 Category 1 bio-based material attribution. Covestro's bio-based aniline pilot plant at Leverkusen, inaugurated in February 2024 as the world's first pilot for renewable aniline production from plant biomass, remains at pilot scale only with no confirmed commercial production timeline, meaning that a fully intrinsically bio-based bisphenol A pathway for conventional PC synthesis is a research-stage programme rather than a commercially available alternative in the current forecast period. These factors substantially limit bio-based polycarbonate market growth over the forecast period.

Industry Trends & Market Dynamics

Covestro Makrolon RE supplying Deutsche Telekom GreenMagenta products with up to 89% renewable-attributed certified content and Makrolon RP debuting at Chinaplas 2024 using chemically recycled feedstock via Neste and Borealis confirm that bio-circular polycarbonate is reaching qualified engineering applications a full procurement cycle ahead of when automotive OEM CSRD deadlines make it a mandatory specification

EU Corporate Sustainability Reporting Directive Scope 3 Category 1 purchased goods and services emissions disclosure requirements from fiscal year 2024 require large European companies to document carbon footprint data from suppliers on a per-product basis, creating a formal procurement value for ISCC PLUS certified bio-circular polycarbonate whose mass-balance bio-waste attribution reduces declared Scope 3 Category 1 carbon intensity per kilogram of PC component relative to fossil-based polycarbonate without functional reformulation or equipment investment. European automotive OEMs including BMW Group, Volkswagen Group, and Stellantis have disclosed Scope 3 Category 1 reduction targets in their 2024 sustainability reports, with purchased material bio-attributed and recycled carbon substitution identified as near-term levers ahead of capital-intensive manufacturing decarbonisation investments. Deutsche Telekom's confirmed specification of Covestro Makrolon RE for its GreenMagenta product programme demonstrates the commercial pathway from CSRD Scope 3 disclosure requirement to bio-circular PC purchase order at telecommunications electronics OEM level, providing a reference procurement case that other European electronics manufacturers implementing CSRD reporting are beginning to replicate. The EPEAT Gold registration pathway for electronics products recognising ISCC PLUS certified renewable-attributed PC content creates a parallel commercial pull in North American and global electronics procurement where EPEAT criteria govern government, corporate, and institutional purchasing specifications at approximately 65 countries' federal procurement offices. Covestro Makrolon RP Chemically Recycled PC Debut and EU End-of-Life Vehicle Directive Expanding Bio-Circular PC Automotive Addressable Market Covestro's April 2024 debut of Makrolon RP at Chinaplas 2024, the first polycarbonate based on chemically recycled attributed material from post-consumer waste via mass balance produced using Neste recycled feedstock converted to phenol and acetone by Borealis, expands the bio-circular polycarbonate addressable market beyond bio-waste attributed renewable content to chemically recycled post-consumer waste attribution, enabling automotive and electronics OEMs to simultaneously address CSRD recycled content reporting requirements alongside bio-based content targets using Covestro's RE and RP series in the same compounded PC product family. The EU End-of-Life Vehicle Directive currently under revision is expected to establish mandatory recycled content requirements for plastics in new vehicles, creating a regulatory framework that will pull bio-circular and recycled-attributed polycarbonate into automotive design specifications as a compliance material rather than a voluntary sustainability upgrade. Covestro confirmed plans to expand polycarbonate compounding capacity at its Hebron, Ohio site with a low triple-digit million euro investment, construction beginning 2025 and operations starting by end of 2026, targeting North American automotive and electronics OEM customers where CSRD-equivalent sustainability documentation requirements from European parent companies are pulling bio-circular PC specification into North American platform design cycles.

Bio-circular PC under ISCC PLUS mass balance is produced from bio-waste and residue feedstock where the renewable material enters the chemical production chain and is mathematically attributed to specific end products rather than physically traceable as a renewable molecule in the bisphenol A or carbonate monomer. This attribution methodology, while accepted under ISCC PLUS and recognised by EPEAT and CSRD frameworks, is subject to increasing scrutiny from life-cycle assessment auditors and corporate sustainability verification specialists who argue that mass-balance attribution does not constitute physical bio-based content for purposes of Product Environmental Footprint calculations under the EU Green Claims Directive. Fully intrinsically bio-based PC from bio-derived bisphenol A requires bio-based aniline or acetone, with Covestro's Leverkusen bio-aniline pilot plant inaugurated February 2024 at pilot scale only and no commercial-scale bio-aniline production timeline confirmed as of Q2 2026. Mitsubishi Chemical Durabio isosorbide-based PC provides the only commercially available intrinsically bio-based polycarbonate from fully renewable monomers, but isosorbide-based PC has lower heat deflection temperature and different optical characteristics than bisphenol A-based PC, limiting its substitution to optical and specialty applications rather than the mainstream automotive and electronics PC market that drives bio-circular PC volume. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated bisphenol A and phenol feedstock costs at European PC producers through naphtha and benzene cost increases, adding approximately USD 60 to USD 100 per metric tonne to conventional fossil PC production cost above the 2024 baseline and partially narrowing the premium of bio-circular Makrolon RE above fossil Makrolon grades. These factors substantially limit bio-based polycarbonate market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Makrolon RE Renewable-Attributed PC, Bio-Circular PC, Isosorbide-Based PC, Partially Bio-Based PC Blends | Makrolon RE Renewable-Attributed PC |

| Application | Automotive Glazing and Interior Components, Electronics and Electrical Housings, Optical Media, Medical Devices, Construction Glazing | Automotive Glazing and Interior Components |

| End Use | Automotive OEM, Consumer Electronics, Healthcare, Building and Construction, Industrial | Automotive OEM |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Makrolon RE Renewable-Attributed PC segment is expected to account for a significantly large revenue share in the global bio-based polycarbonate market during the forecast period.

This report evaluates product type across Makrolon RE Renewable-Attributed PC, Bio-Circular PC, Isosorbide-Based PC, Partially Bio-Based PC Blends for bioplastics & recycled, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Automotive Glazing and Interior Components, Electronics and Electrical Housings, Optical Media, Medical Devices, Construction Glazing for bioplastics & recycled, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive OEM, Consumer Electronics, Healthcare, Building and Construction, Industrial for bioplastics & recycled, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for bioplastics & recycled, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

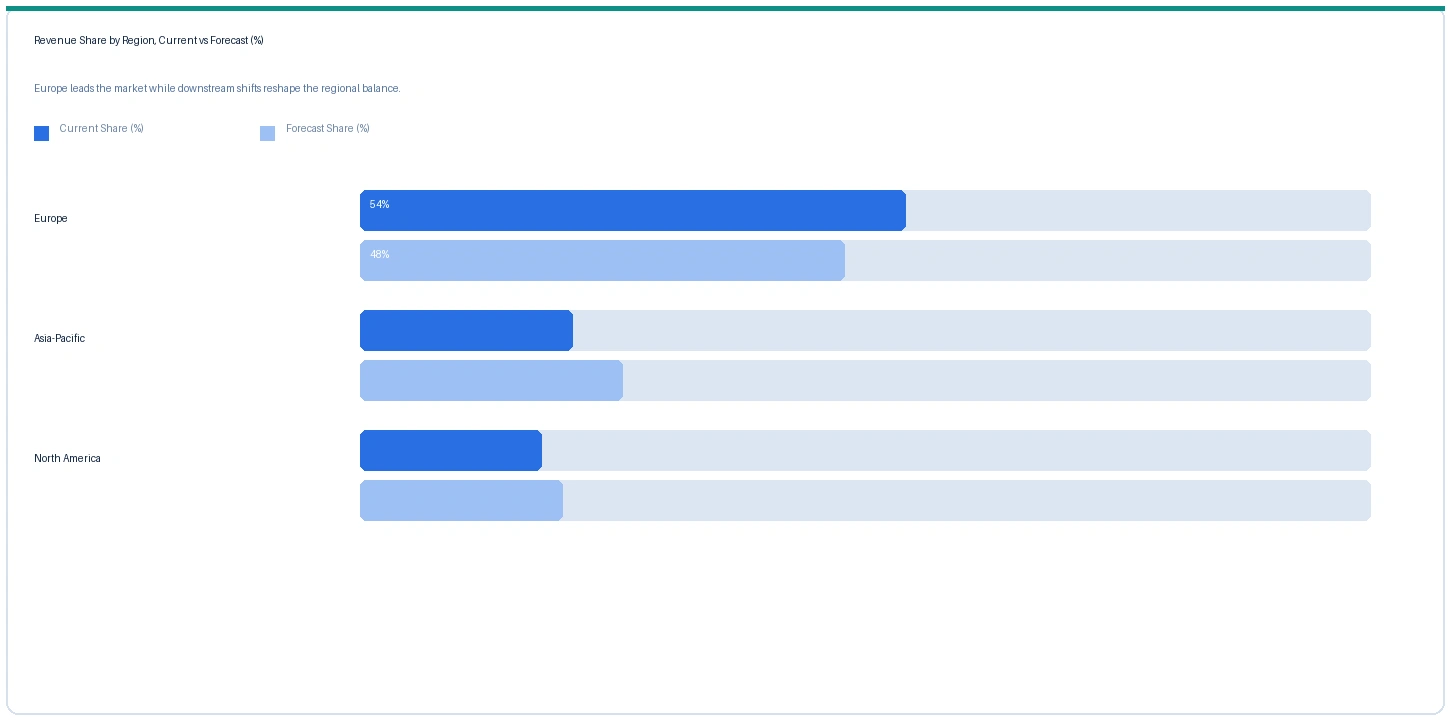

Europe market accounted for largest revenue share over other regional markets in the global bio-based polycarbonate market in 2025. Based on regional analysis, the bio-based polycarbonate market in Europe accounted for largest revenue share in 2025 at approximately 44% of global revenue. Covestro at Leverkusen and Krefeld-Uerdingen produces Makrolon RE and RP for European automotive and electronics OEM customers under ISCC PLUS certification from German and European production sites, with CSRD Scope 3 Category 1 disclosure requirements from fiscal year 2024 creating formal procurement pull for bio-circular PC in European automotive Tier 1 supply chains and consumer electronics manufacturing. Deutsche Telekom's confirmed Makrolon RE specification for GreenMagenta products and SABIC's LNP Elcrin iQ bio-circular PC supply to European automotive and medical OEMs confirm Europe as both the primary bio-circular PC production and consumption geography.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global bio-based polycarbonate market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period at approximately 14.2% CAGR. Covestro's April 2024 debut of Makrolon RP at Chinaplas 2024 in Shanghai targeting high-purity automotive and electronics applications in China and Covestro's expansion plans at its Shanghai production site confirmed in its 2024 annual financial results confirm Asia-Pacific as a priority growth market for bio-circular PC. Chinese and Japanese electronics OEMs implementing CSRD-equivalent sustainability reporting for their European customers and Japanese automotive OEMs at Toyota, Honda, and Nissan implementing supplier Scope 3 data collection programmes are creating demand for ISCC PLUS certified bio-circular PC through supply chain sustainability requirements that flow back to Asian PC compounders.

North America market accounted for second largest revenue share in the global bio-based polycarbonate market in 2025. The market in North America is expected to register the second largest revenue share. Covestro's announced expansion at Hebron, Ohio to increase differentiated polycarbonate compounding capacity within its Solutions and Specialties segment, with construction beginning 2025 and operations by end of 2026, confirms North American bio-circular PC supply expansion at the commercial scale required to serve automotive and electronics OEM customers where European parent company CSRD reporting requirements are pulling bio-circular PC into North American platform specifications. SABIC's LNP Elcrin iQ bio-circular PC blends and Mitsubishi Chemical Durabio optical grades supply North American medical device and electronics OEMs.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Makrolon RE (89% renewable, standard) | Europe | USD 3,840/MT | USD 3,520/MT | Rising | Covestro ref |

| Makrolon RP (chemically recycled) | Asia-Pacific | USD 3,680/MT | USD 3,360/MT | Rising | Covestro CQ ref |

| SABIC LNP Elcrin iQ (bio-circular) | Europe | USD 4,120/MT | USD 3,780/MT | Rising | SABIC ref |

| Mitsubishi Durabio (isosorbide PC) | Asia-Pacific | USD 5,640/MT | USD 5,200/MT | Rising | Specialty bio-PC ref |

| Fossil Makrolon (standard benchmark) | Europe | USD 2,840/MT | USD 2,640/MT | Rising | Conventional ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty materials trade publication monitoring.

Covestro Makrolon RE standard grade with up to 89% renewable-attributed content rose approximately 9.1% from USD 3,520 per metric tonne in Q2 2025 to USD 3,840 per metric tonne in Q2 2026 in Europe, reflecting CSRD Scope 3 Category 1 demand from electronics and automotive OEMs growing faster than Covestro's ISCC PLUS certified supply allocation at current certified feedstock procurement levels. Makrolon RP chemically recycled attributed PC rose approximately 9.5% to USD 3,680 per metric tonne in Asia-Pacific from its April 2024 commercial debut, with Neste recycled feedstock costs elevated by the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 adding approximately USD 80 to USD 120 per metric tonne to Neste's recycled feedstock processing costs from elevated energy inputs. SABIC LNP Elcrin iQ bio-circular PC blend rose approximately 9.0% to USD 4,120 per metric tonne reflecting ISCC PLUS certified supply constraint and automotive OEM CSRD documentation demand. Mitsubishi Chemical Durabio isosorbide-based PC rose approximately 8.5% to USD 5,640 per metric tonne from isosorbide feedstock cost elevation from corn starch-derived glucose hydrogenation input costs increasing from agricultural energy cost pass-through. Conventional fossil Makrolon benchmark rose approximately 7.6% to USD 2,840 per metric tonne from bisphenol A and phenol cost elevation from Hormuz naphtha supply disruption, partially narrowing the Makrolon RE premium percentage from approximately 33% in Q2 2025 to approximately 35% in Q2 2026 as bio-circular demand pull exceeded fossil cost pass-through.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the bio-based polycarbonate market, the Hormuz disruption operates primarily through bisphenol A and phenol feedstock cost elevation at European PC producers through naphtha and benzene supply disruption, adding approximately USD 60 to USD 100 per metric tonne to conventional fossil Makrolon production cost at Covestro Leverkusen and Krefeld-Uerdingen above the 2024 baseline. This fossil feedstock cost elevation partially narrows the percentage premium of Makrolon RE over fossil Makrolon from approximately 33% in Q2 2025 to approximately 35% in Q2 2026, as bio-circular demand pull lifted RE pricing faster than fossil feedstock cost pass-through to fossil PC. Neste's recycled feedstock processing costs for Makrolon RP supply are elevated from increased energy inputs in Neste's Finnish refineries from the GCC LNG supply disruption, adding approximately USD 80 to USD 120 per metric tonne to Neste recycled feedstock cost and contributing to the Makrolon RP Q2 2026 price increase.

Company Insights

The two key dominant companies in the bio-based polycarbonate market are Covestro AG and SABIC (Solutions Business), recognised for their commercial leadership, certified production scale, and global customer reach.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 486.2 Million |

| Market Size 2032 | USD 982.4 Million |

| CAGR | 10.5% |

| Units | Revenue in USD Million |

| Segments Covered | By Product Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, Netherlands, France, Japan, South Korea, China, India, Brazil |

| Companies Profiled | Covestro AG, SABIC, Mitsubishi Chemical, Trinseo, Teijin, LG Chem, Chi Mei, Wanhua, Lotte Chemical |

| Key Data Sources | Covestro AG Annual Financial Report 2024, Covestro Makrolon RE ISCC PLUS certification documentation up to 89% renewable-attributed content, Covestro Makrolon RP Chinaplas 2024 debut press release, Covestro Hebron Ohio expansion announcement Q4 2024, Covestro bio-aniline pilot plant Leverkusen February 2024, Deutsche Telekom GreenMagenta Makrolon RE specification, Covestro 2024 annual press release EUR 7.03Bn S&S segment revenue, EPEAT electronics sustainability certification criteria for renewable-attributed PC, EU CSRD Scope 3 Category 1 framework, EU End-of-Life Vehicle Directive revision, IMF March 2026 Strait of Hormuz statement, 13 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 264 |

| Published | Q2 2026 |

| SKU | NXC-PC-019 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 13 expert interviews conducted between January and May 2026. Supply-side contacts included bio-circular polycarbonate product and commercial managers at European PC producers implementing ISCC PLUS mass balance certification, recycled feedstock supply managers at Neste and equivalent renewable chemical producers, and ISCC PLUS certification programme managers for engineering plastic mass balance. Demand-side contacts included sustainability procurement managers at European electronics OEMs specifying ISCC PLUS certified PC for CSRD Scope 3 Category 1 material purchases, automotive Tier 1 polymer procurement engineers qualifying bio-circular PC for CSRD-driven platform design cycles, and life-cycle assessment specialists verifying CSRD Scope 3 material attribution methodologies. Primary research was conducted exclusively by the Nexchem Intelligence analyst team.

Secondary research sources include Covestro AG Annual Financial Report and full year results press release 2024 confirming EUR 14.2 Bn total sales and EUR 7.03 Bn Solutions and Specialties segment revenue, Covestro Makrolon RE ISCC PLUS certification documentation and up to 89% renewable-attributed content specification, Covestro Makrolon RP debut press release Chinaplas 2024 April confirming Neste and Borealis partnership, Covestro Hebron Ohio expansion announcement with operations planned by end 2026, Covestro bio-aniline pilot plant Leverkusen inauguration February 2024, Deutsche Telekom GreenMagenta Makrolon RE specification confirmation, EPEAT electronic product sustainability criteria for renewable-attributed materials, EU Corporate Sustainability Reporting Directive Scope 3 Category 1 framework, EU End-of-Life Vehicle Directive revision timeline, and the IMF March 2026 Strait of Hormuz statement. No figures from syndicated market research publishers are used as source data.