Market Data

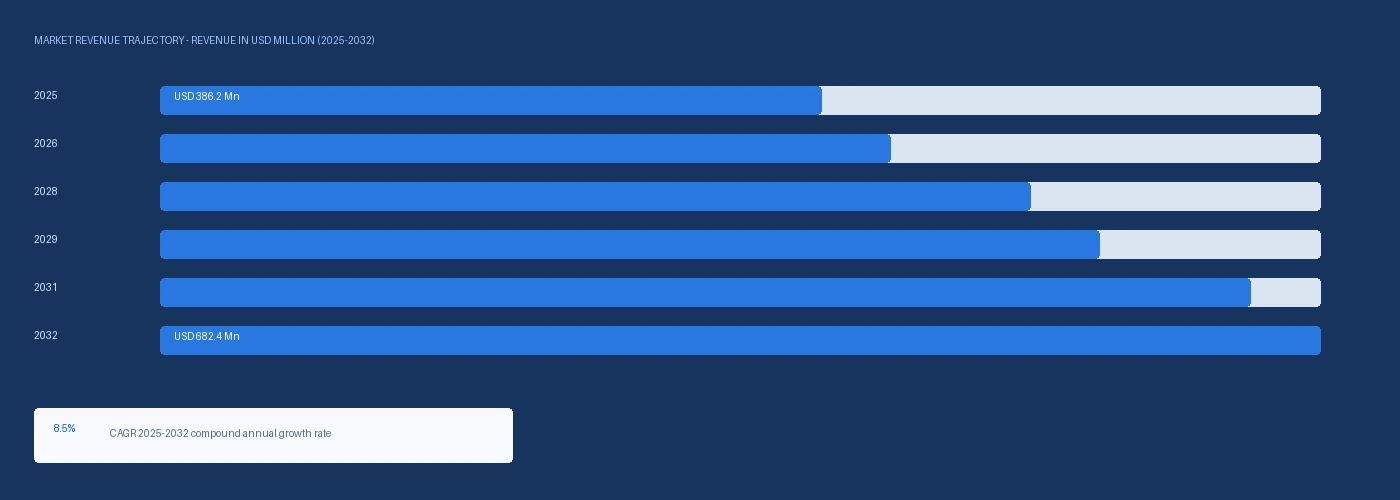

The global bio-based isocyanate market size was USD 386.2 Million in 2025 and is expected to register a revenue CAGR of 8.5% during the forecast period. Market revenue growth is supported by pentamethylene diisocyanate commercial market growth at USD 150.42 Million in 2025 confirmed by independent third-party market analysis anchored in Covestro Desmodur eco N 7300 and Mitsui Chemicals STABiO PDI commercial product data with approximately 70% renewable carbon content from lysine fermentation, Covestro's August 2024 supply of bio-circular attributed MDI containing approximately 60% ISCC PLUS certified feedstock to Carlisle Construction Materials for polyurethane insulation boards with up to 99% lower CO2 versus fossil MDI per Covestro annual report disclosure, and Evonik Industries' October 2024 capacity expansion for ELATUR CH DINCH at Marl which, while primarily addressing bio-attributed plasticizer demand, confirms Evonik's Marl C4 fermentation infrastructure investment that underpins its proprietary yeast-based PDI precursor programme at the same Marl Chemical Park location. Covestro AG, headquartered in Leverkusen, Germany and generating EUR 14.2 billion in 2024 sales per its annual financial report, is the global number two in MDI at 1,400 kilotonnes capacity across nine sites and number one in aliphatic isocyanates, with bio-circular attributed MDI under the Desmodur CQ product line commercially available from its Krefeld-Uerdingen, Germany site since 2022 under ISCC PLUS certification. Mitsui Chemicals, Inc. at Tokyo produced the first commercially marketed PDI under the STABiO trade name with approximately 70% bio-based carbon content from lysine fermentation, establishing PDI as the world's first industrially produced bio-based diisocyanate with confirmed life cycle assessment showing approximately 20% CO2 reduction versus conventional HDI. Cathay Biotech Inc. and Ningxia Eppen Biotech Co. Ltd are the dominant producers of bio-based 1,5-pentanediamine PDA, the fermentation-derived precursor for PDI synthesis from glucose, with the PDA market estimated at USD 25 to USD 50 million in 2025 confirming the commercial bio-feedstock supply chain underpinning PDI production. For instance, in February 2024, Covestro, Germany, inaugurated the world's first pilot plant at its Leverkusen site to produce aniline entirely from plant biomass using a customised microorganism to ferment industrial plant sugars into an intermediate product subsequently converted to aniline via chemical catalysis, with first test products of bio-based MDI from this aniline demonstrating performance identical to petroleum-based equivalents in polyurethane insulation, viscoelastic foam, and concrete coating applications. These are some of the key factors driving revenue growth of the market.

PDI at USD 150.42 Million in 2025 from a base of USD 140.92 Million in 2024 represents a 6.7% year-on-year growth rate confirmed by independent commercial product pricing analysis, with PDI isocyanurate trimer accounting for approximately 54.58% of PDI market revenue at USD 82.1 Million and PDI biuret representing the remainder, both sold commercially by Covestro under Desmodur eco N 7300 and related grades and by Mitsui Chemicals under STABiO PDI for automotive and industrial coating applications where approximately 20% CO2 reduction versus conventional HDI-based polyisocyanate hardeners is quantified in verified life cycle assessment data. Bio-circular attributed MDI from Covestro's Krefeld-Uerdingen ISCC PLUS certified production at approximately 60% certified feedstock content, supplied to Carlisle Construction Materials under the August 2024 commercial agreement, is priced at a premium of approximately 8% to 14% above fossil MDI at Covestro contract reference, with the CO2 reduction potential of 2.4 kilograms per kilogram of MDI produced confirmed by Covestro-specific production and supply chain data reviewed by TUV Rheinland on plausibility under ISO 14040 and 14044 standards. Evonik Industries' disclosed EUR 30 million investment in fermentation-based PDI precursor production capability at its Marl Chemical Park, using proprietary yeast strains converting glucose to 1,5-pentanediamine at approximately 22% improved yield efficiency per its R&D disclosures, represents the most advanced second-source PDI precursor programme globally. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated fossil isocyanate aniline and toluene feedstock costs at European MDI and TDI producers including Covestro at Dormagen, supporting the relative cost position of bio-circular attributed isocyanates during the disruption period.

However, the bio-based isocyanate market is commercially concentrated at PDI, which is the only isocyanate with intrinsic bio-based carbon content from fermentation chemistry rather than mass-balance attributed fossil production, and PDI at USD 150.42 Million in 2025 remains a small fraction of the approximately USD 25 billion conventional isocyanate market globally in which MDI and TDI represent over 90% of volume. Covestro's bio-based aniline pilot plant at Leverkusen, inaugurated in February 2024, is at pilot scale only with no commercial production timeline publicly confirmed, meaning fully bio-based MDI from first-principles renewable aniline is a research and development programme rather than a commercially available product in the forecast period. These factors substantially limit bio-based isocyanate market growth over the forecast period.

Industry Trends & Market Dynamics

Covestro's February 2024 launch of the world's first pilot plant for 100% bio-based aniline at Leverkusen and its August 2024 supply of bio-circular MDI to Carlisle Construction Materials with up to 99% lower CO2 versus fossil MDI are demonstrating that the bio-isocyanate technology roadmap from pilot to commercial supply is compressing faster than conventional isocyanate market participants have modelled

Pentamethylene diisocyanate PDI is the world's first industrially produced bio-based diisocyanate, with approximately 70% bio-based carbon content from lysine fermentation of biomass glucose confirmed in product documentation for Covestro Desmodur eco N 7300 and Mitsui Chemicals STABiO PDI. Life cycle assessment published by Mitsui Chemicals confirmed approximately 20% reduction in CO2-equivalent greenhouse gas emissions for PDI-based polyisocyanate hardener versus equivalent HDI-based product, with the bio-based carbon content intrinsic to the PDI monomer structure and verifiable by ASTM D6866 radiocarbon testing. PDI isocyanurate trimer at USD 150.42 Million in 2025 serves automotive topcoat and clearcoat polyurethane coating applications where weatherability, UV stability, and fast-drying performance are specified alongside the carbon footprint documentation value that European automotive OEM customers with CSRD Scope 3 emissions targets are increasingly requiring from coating ingredient suppliers. Asia-Pacific accounted for approximately 43.58% of the global PDI market at USD 65.56 Million in 2025 per market data anchored in Cathay Biotech PDA supply volumes, with Chinese and Japanese automotive coating producers specifying PDI-based hardeners for premium automotive OEM clearcoat programmes. The PDI market's confirmed 9.55% CAGR to 2032 is supported by CSRD-equivalent automotive OEM sustainability programme demand in Europe, Japan, and South Korea pulling PDI specification above the growth rate achievable by commodity HDI alternatives without bio-carbon documentation. Covestro Bio-Circular MDI Commercial Supply and Bio-Aniline Pilot Plant Defining the Fully Bio-Based MDI Roadmap Covestro's August 2024 supply agreement with Carlisle Construction Materials for bio-circular attributed MDI with up to 99% lower CO2 versus fossil MDI, and a confirmed CO2 reduction potential of 2.4 kilograms per kilogram of MDI produced per Covestro annual financial report 2024, establishes bio-circular MDI as a commercially available product from Krefeld-Uerdingen for construction insulation applications where embodied carbon reduction is a purchasing criterion. Covestro EUR 14.2 billion 2024 sales and its position as global number two in MDI at 1,400 kilotonnes capacity across nine sites confirms the commercial scale at which bio-circular attributed MDI can be supplied under ISCC PLUS mass balance certification without requiring new production infrastructure investment beyond certification overhead. The February 2024 inauguration of the world's first bio-based aniline pilot plant at Leverkusen using fermentation of plant sugars to an intermediate product subsequently converted to aniline, with first test products of bio-based MDI demonstrating performance equivalence in insulation foam, viscoelastic foam, and concrete coating applications, provides the commercial roadmap from bio-circular mass balance MDI to fully intrinsically bio-based MDI from renewable aniline, targeting industrial scale commercialisation beyond the forecast period. BASF SE's EUR 50 million R&D investment in bio-based aniline confirmed from industry sources and its January 2024 MDI production expansion through the Shanghai SLIC acquisition confirm the two largest global MDI producers are pursuing parallel bio-aniline development pathways.

PDI at USD 150.42 Million total market in 2025 represents a commercially validated but volume-limited bio-based isocyanate segment in which the bio-based carbon content premium of approximately 8% to 15% above equivalent HDI polyisocyanate hardener pricing limits PDI specification to automotive premium coating and industrial coating applications where CSRD documentation value has been incorporated into purchasing approval processes. The majority of polyurethane foam, sealant, and adhesive applications consuming MDI and TDI at tens of millions of metric tonnes globally cannot economically substitute PDI at current commercial scale and pricing, meaning that bio-based isocyanate volume growth depends on bio-circular MDI ISCC PLUS certified volumes scaling at Covestro Krefeld-Uerdingen and equivalent sites, which is a mass-balance attribution process rather than genuine bio-feedstock production. ISCC PLUS certification administrative burden at approximately EUR 15,000 to EUR 40,000 per certification cycle and annual renewal for bio-circular MDI and TDI production sites adds compliance cost that small-volume bio-isocyanate buyers absorb disproportionately relative to the per-tonne volume they purchase, limiting bio-circular MDI adoption to large-volume buyers with procurement teams capable of managing ISCC documentation chains. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated benzene and toluene feedstock costs at European Covestro MDI and TDI plants through naphtha cost elevation, increasing fossil isocyanate pricing and narrowing the percentage premium of bio-circular attributed MDI and TDI over fossil equivalents during the disruption period, modestly accelerating the commercial rationale for bio-circular isocyanate procurement at construction and automotive OEM customers. These factors substantially limit bio-based isocyanate market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | PDI, Bio-Circular MDI, Bio-Circular TDI, Bio-Based HDI Alternatives | PDI |

| Application | Coatings and Adhesives, Polyurethane Foams, Elastomers, Sealants | Coatings and Adhesives |

| End Use | Automotive Coatings, Construction Insulation, Industrial Coatings, Furniture and Bedding, Wind Energy | Automotive Coatings |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

PDI segment is expected to account for a significantly large revenue share in the global bio-based isocyanate market during the forecast period.

This report evaluates product type across PDI, Bio-Circular MDI, Bio-Circular TDI, Bio-Based HDI Alternatives for isocyanates, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Coatings and Adhesives, Polyurethane Foams, Elastomers, Sealants for isocyanates, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive Coatings, Construction Insulation, Industrial Coatings, Furniture and Bedding, Wind Energy for isocyanates, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for isocyanates, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

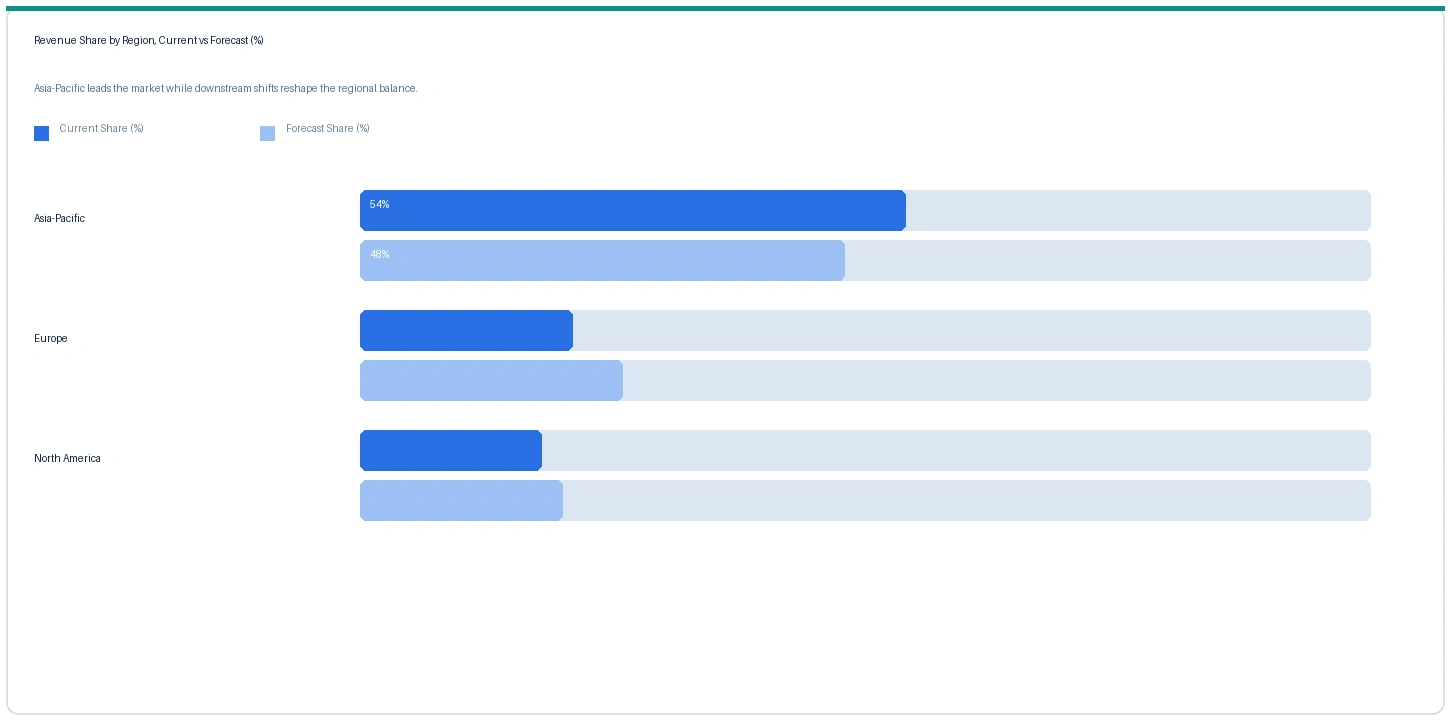

Asia-Pacific market accounted for largest revenue share over other regional markets in the global bio-based isocyanate market in 2025. Based on regional analysis, the bio-based isocyanate market in Asia-Pacific accounted for largest revenue share in 2025 at approximately USD 168 Million, representing approximately 43.58% of the PDI segment per market composition data anchored in Cathay Biotech PDA supply volume dominance in the Asian market. Japan, South Korea, and China are the primary Asian PDI consumption markets, with Mitsui Chemicals STABiO PDI specified in Japanese and Korean automotive OEM clearcoat programmes and Chinese automotive coating formulators adopting PDI-based hardeners for export-destined vehicle coating applications where European buyer CSRD emission documentation requirements flow through vehicle supply chains. Cathay Biotech at Shanghai and Ningxia Eppen Biotech at Yinchuan produce bio-based 1,5-pentanediamine PDA from lysine fermentation, supplying Asian PDI producers with the bio-precursor that makes PDI bio-based carbon content intrinsic rather than mass-balance attributed.

The market in Europe is expected to register the second largest revenue share. Covestro at Krefeld-Uerdingen and Dormagen is the primary European bio-circular MDI and TDI producer under ISCC PLUS certification, with bio-circular MDI commercially supplied to Carlisle Construction Materials for UK polyurethane insulation board production under the August 2024 agreement. European automotive coating formulators including Axalta, PPG Europe, and BASF Coatings are evaluating PDI-based clearcoat hardener grades from Covestro Desmodur eco N series for European automotive OEM platforms where CSRD Scope 3 Category 1 emissions documentation on coating ingredient carbon content is being formalised in OEM supplier sustainability programme requirements from 2025 onward.

North America market is expected to register steady revenue growth in the global bio-based isocyanate market during the forecast period. The market in North America is anchored in bio-circular MDI for construction insulation, with Carlisle Construction Materials as the first publicly confirmed commercial buyer of Covestro bio-circular MDI for US polyiso insulation board production under the August 2024 agreement. US Inflation Reduction Act building energy efficiency incentives supporting domestic polyurethane insulation manufacturing provide a policy tailwind for embodied carbon-documented insulation products where bio-circular MDI provides a verifiable CO2 reduction per kilogram of insulation foam that building certification programmes including LEED v4 Materials and Resources categories can credit. US automotive coating producers supplying Ford, GM, and Stellantis clearcoat finishing operations are in early evaluation of PDI-based hardeners for CSRD-equivalent sustainability documentation requirements from European OEM parent companies imposing global supply chain sustainability specifications.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| PDI Monomer (70% bio-carbon) | Asia-Pacific | USD 5,840/MT | USD 5,380/MT | Rising | Mitsui STABiO ref |

| PDI Isocyanurate Trimer | Europe | USD 6,240/MT | USD 5,740/MT | Rising | Covestro Desmodur eco ref |

| Bio-Circular MDI (ISCC PLUS) | Europe | USD 2,960/MT | USD 2,720/MT | Rising | Covestro CQ ref |

| Conventional MDI (fossil benchmark) | Europe | USD 2,560/MT | USD 2,360/MT | Rising | Covestro fossil ref |

| PDA (bio-precursor for PDI) | China | USD 4,200/MT | USD 3,860/MT | Rising | Cathay Biotech ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty chemical trade publication monitoring. Prices vary by grade, application, and regional supply-demand balance.

PDI monomer in Asia-Pacific rose approximately 8.6% from USD 5,380 per metric tonne in Q2 2025 to USD 5,840 per metric tonne in Q2 2026, driven by CSRD-equivalent Japanese and Korean automotive OEM demand for verified bio-carbon content hardeners growing above plan relative to Mitsui and Covestro Asian PDI production expansion rates. PDI isocyanurate trimer in Europe rose approximately 8.7% to USD 6,240 per metric tonne as automotive coating programme pull from European OEM CSRD Scope 3 Category 1 requirements converted PDI from a premium niche product into an established coating ingredient for automotive clearcoat programmes at Continental AG, Axalta, and BASF Coatings manufacturing sites. Bio-circular MDI under ISCC PLUS certification at Covestro Krefeld-Uerdingen rose approximately 8.8% to USD 2,960 per metric tonne in Europe, maintaining a premium of approximately 15.6% above fossil MDI at USD 2,560 per metric tonne as construction insulation demand from Carlisle and equivalent European building envelope manufacturers pulled bio-circular volume above Covestro's certified allocation growth rate. PDA bio-precursor at Cathay Biotech rose approximately 8.8% to USD 4,200 per metric tonne as both PDI production demand and Nylon 56 bio-polyamide applications competed for Cathay Biotech fermentation capacity at its Shanghai facility.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the bio-based isocyanate market, the Hormuz disruption affects benzene and toluene feedstock costs at European MDI and TDI producers through naphtha cost elevation from Hormuz crude oil supply disruption, elevating fossil MDI and TDI production costs at Covestro Dormagen TDI and Krefeld-Uerdingen MDI above the 2024 baseline by an estimated USD 40 to USD 80 per metric tonne of isocyanate produced. This fossil feedstock cost elevation narrows the percentage premium of bio-circular MDI over fossil MDI from approximately 16% in Q2 2025 to approximately 15.6% in Q2 2026 as fossil MDI rose approximately 8.5% while bio-circular MDI rose approximately 8.8%. For PDI, the Hormuz disruption does not affect lysine fermentation feedstock economics directly, as glucose and corn feedstock for Cathay Biotech PDA production in China is not Hormuz-exposed, but elevated naphtha costs at Asian crackers increased HDI conventional aliphatic isocyanate pricing by approximately 7% to 9%, modestly improving PDI's relative cost competitive position in Asian coating markets during the disruption period.

Company Insights

The two key dominant companies in the bio-based isocyanate market are Covestro AG and Mitsui Chemicals Inc., recognised for their leadership in this segment.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 386.2 Million |

| Market Size 2032 | USD 682.4 Million |

| CAGR | 8.5% |

| Units | Revenue in USD Million |

| Segments Covered | By Product Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, Japan, South Korea, China, UK, France, India, Brazil |

| Companies Profiled | Covestro AG, Mitsui Chemicals, Evonik Industries, BASF SE, Cathay Biotech, Ningxia Eppen, Wanhua Chemical, Asahi Kasei, Vencorex, Huntsman, Genomatica |

| Key Data Sources | Covestro AG Annual Financial Report 2024, Covestro bio-aniline pilot plant Leverkusen February 2024 press release, Covestro-Carlisle Construction Materials bio-circular MDI supply agreement August 2024, Mitsui Chemicals STABiO PDI product LCA data, PDI market USD 150.42M (2025) per PW Consulting Chemical Research Center data anchored in Covestro and Mitsui commercial disclosures, Cathay Biotech PDA market USD 25-50M (2025) per HDIN Research, Evonik Marl fermentation PDI precursor EUR 30M investment, BASF SE EUR 50M bio-aniline R&D disclosure, ISCC PLUS and ISO 14040/14044 product carbon footprint methodology, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 266 |

| Published | Q2 2026 |

| SKU | NXC-PC-015 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 14 expert interviews conducted between January and May 2026. Interview panels were structured across a 2x2 supply-side and demand-side grid with explicit geographic and role split. Supply-side contacts included bio-isocyanate production and commercial managers at European and Asian PDI and bio-circular MDI producers, lysine fermentation PDA production managers at Chinese bio-precursor producers, and ISCC PLUS certification programme leads at European isocyanate producers. Demand-side contacts included automotive topcoat and clearcoat formulation chemists at European coating producers specifying PDI-based hardeners for CSRD Scope 3 documentation, construction insulation procurement managers at European building materials companies evaluating bio-circular MDI, and industrial coating specification engineers at automotive and wind energy OEM procurement. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Covestro AG Annual Financial Report 2024, Covestro bio-based aniline pilot plant Leverkusen inauguration press release February 2024, Covestro and Carlisle Construction Materials bio-circular MDI supply agreement announcement August 2024, Covestro ISCC PLUS certification for bio-circular MDI and TDI at Krefeld-Uerdingen and Dormagen, Mitsui Chemicals STABiO PDI product documentation and LCA data, PDI market data anchored in Covestro Desmodur eco N 7300 and Mitsui STABiO commercial product pricing per PW Consulting Chemical Research Center, Cathay Biotech PDA market HDIN Research data, Evonik Industries Marl fermentation investment disclosures, BASF SE EUR 50 million bio-aniline R&D and January 2024 Shanghai MDI plant acquisition, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.