Market Data

The global bio-based, biodegradable A/B polyurethane system market size was USD 892.4 Million in 2025 and is expected to register a revenue CAGR of 5.4% during the forecast period. An A/B polyurethane system is a two-component reactive system in which Part A contains the polyol blend -- potentially incorporating bio-based natural oil polyols, biomass-balanced polyether polyols, or bio-synthetic polyols from vegetable or algae feedstocks -- and Part B contains the isocyanate component, typically MDI or TDI potentially including bio-circular mass-balance attributed grades from Covestro or BASF. Market revenue growth is supported by the US market for bio-based and biodegradable A/B polyurethane systems being valued at USD 289.86 million in 2024 growing at a CAGR of 4.2% per Grand View Research industry assessment based on primary market analysis of US market participants, implying a global market approximately 3.1 times the US value at approximately USD 900 million given that the US accounts for approximately 32% of global PU system consumption and the US and European markets are the primary geographies for bio-attributed A/B system adoption, Algenesis Corporation at La Jolla, California commercially deploying its patented Soleic bioPU A/B system -- comprising the Soleic Part A bio-based polyol blend derived from algae and plant oils and the paired Part B bio-based isocyanate component under DOE green-flow chemistry development -- in footwear midsole and insole flexible foam applications with 52% bio-content, backyard compostability certification, 50% LCA greenhouse gas reduction versus petroleum PU per Algenesis disclosures, and currently deployed at footwear brands including RhinoShield case applications and expanding into breathable waterproof textiles and injection-moulded consumer goods, and RAMPF Holding GmbH and Co. KG at Grafenberg, Germany and Recticel NV at Brussels, Belgium formulating and supplying bio-attributed two-component PU system solutions for automotive, industrial, and bedding foam applications respectively from bio-based polyol Part A components incorporating Cargill BiOH, BASF Sovermol, and Covestro Desmophen eco-grade feedstocks. For instance, in Q4 2024, Recticel NV, Belgium, unveiled its first fully bio-based polyurethane foam product specifically developed for the bedding industry and targeting eco-conscious consumers and mattress manufacturers in European markets requiring EN 16785 bio-based content certification, the first commercially available fully bio-based flexible foam product from a European foam converter targeting the premium bedding segment under EU CSRD supply chain documentation requirements. These are some of the key factors driving revenue growth of the market.

The conventional A/B polyurethane system segment -- which includes systems formulated with petroleum-based polyols and standard MDI or TDI isocyanates but containing some bio-based content through natural oil polyol incorporation or ISCC PLUS mass-balance attribution -- accounted for approximately 87.8% of the US bio-based and biodegradable A/B PU system market revenue in 2024 per Grand View Research primary market data, with the fully bio-based or biodegradable bioplastic A/B system segment at 12.2% of US market value. This market structure reflects the commercial reality that most A/B PU system formulators are incorporating partial bio-based content into existing formulations -- typically 5% to 25% natural oil polyol replacement of petroleum polyether polyol in Part A -- rather than converting to fully bio-based A/B systems that require complete reformulation and end-use requalification. Building and construction accounted for the largest A/B PU system end-use revenue channel through spray-applied rigid foam insulation systems, cast elastomers for waterproofing membranes, and two-component adhesive systems for structural bonding where bio-based polyol Part A components from Cargill BiOH and BASF Sovermol replace 10% to 20% of petroleum polyol without requiring changes to Part B MDI or application equipment. The footwear sector is the fastest-growing A/B PU system end use, driven by Algenesis Soleic bioPU deployment in midsoles and insoles and BASF's July 2024 launch of certified traceability for bio-based footwear PU solutions covering the integrated Part A bio-polyol and Part B isocyanate supply chain from feedstock to foamed shoe component.

However, the bio-based, biodegradable A/B polyurethane system market is constrained by the formulation complexity of substituting bio-based polyols into established A/B PU system formulations, as natural oil polyols have different functionality, viscosity, reactivity profiles, and water content management requirements than petroleum polyether polyols that require A/B ratio adjustment, catalyst reformulation, and processing parameter modification at A/B system mixing and dispensing equipment operating at metered ratio tolerances of plus or minus 1% to 3%. Each reformulated bio-based A/B PU system requires customer re-approval for end-use performance specifications -- automotive substrate adhesion, foam compression set, rigid foam thermal conductivity, elastomer Shore hardness -- creating a qualification cycle of 6 to 18 months per application that restricts rapid market penetration even where bio-based raw material availability is not the binding constraint. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated MDI and TDI pricing at the Part B isocyanate component level by approximately 10% to 14% above the 2024 baseline from naphtha feedstock cost increases at Covestro, BASF, and Wanhua isocyanate production, increasing the total A/B system cost for both standard and bio-attributed configurations without differentially favouring bio-based adoption. These factors substantially limit bio-based, biodegradable A/B polyurethane system market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

The EU Corporate Sustainability Reporting Directive mandatory from January 2024 for large EU-listed companies requires value chain Scope 3 greenhouse gas reporting that creates documented bio-content demand at the A/B PU system level for furniture, automotive, construction, and footwear brands who specify polyurethane systems to tier one manufacturing suppliers. System formulators including RAMPF and Recticel who can provide ISO 14044 lifecycle assessment data, ISCC PLUS bio-circular attribution documentation, and EN 16785 bio-based content certification for their A/B PU systems are gaining specification preference with European OEM customers implementing CSRD supply chain documentation programmes. The EU Extended Producer Responsibility legislation for textiles and footwear expected from 2027 will require documented material content and end-of-life pathway information that biodegradable A/B PU systems with compostability certification provide more readily than non-degradable petroleum PU foam and elastomer systems. Algenesis Soleic bioPU system -- fully backyard compostable with third-party certification -- is directly aligned with the EU EPR footwear biodegradability documentation requirements, providing a competitive commercial advantage for footwear brand customers implementing EPR preparation programmes ahead of the 2027 implementation. Footwear and Consumer Goods Brand Sustainability Commitments Driving Fully Bio-based A/B System Pilots Algenesis Soleic bioPU system deployment in footwear midsoles and insoles -- confirming 52% bio-content, backyard compostability, and 50% LCA GHG reduction -- represents the only commercially available fully biodegradable A/B polyurethane system for flexible foam applications as of 2025, positioning Algenesis as the only supplier able to meet footwear brand sustainability requirements for fully compostable bio-based PU foam where the US Department of Energy grant of USD 5 million for bio-based isocyanate scale-up from algae oils supports progression toward 100% bio-content Soleic. Adidas, Nike, Puma, and On Running have each publicly committed to bio-based or recycled content targets for footwear components by 2025 to 2030 in their published sustainability reports, creating brand-level demand pull for fully bio-based A/B PU midsole system supply that Algenesis is uniquely positioned to address at the biodegradable end of the sustainability requirement spectrum. Consumer goods applications for injection-moulded products including phone cases -- where Algenesis is expanding Soleic from current flexible foam to rigid injection-moulded grades -- represent an adjacent A/B PU system channel where consumer electronics brands including RhinoShield have already adopted Soleic, confirming technology transfer from footwear foam to rigid consumer goods moulding.

Incorporating bio-based polyols into Part A of an established A/B PU system requires reformulation of the entire system chemistry because natural oil polyols from soybean, castor, or palm oil feedstocks have primary hydroxyl functionality of 2 to 4 versus polyether polyol functionality of 2 to 8, limiting crosslink density and affecting rigid foam thermal conductivity and compression strength, elastomer hardness and tear resistance, and coating adhesion and chemical resistance in ways that require catalyst adjustment, chain extender incorporation, and processing parameter modification. System formulators including RAMPF and BASF PU systems technical groups estimate that each new bio-based Part A formulation requires 3 to 12 months of laboratory development followed by 6 to 18 months of customer application qualification testing before commercial deployment, creating a total 9 to 30 month development timeline per bio-attributed A/B system product that restricts annual new product introduction rates. Fully biodegradable A/B PU systems -- where Part A bio-polyol is hydrolytically labile to enable composting degradation -- must balance biodegradation rate under ISO 14855 composting conditions against in-service hydrolysis resistance requirements for automotive humidity, construction moisture, and footwear sweat exposure, a balance that Algenesis Soleic has achieved for soft foam footwear applications but that remains unvalidated for rigid construction foam or high-humidity automotive interior applications. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated Part B isocyanate costs by approximately 10% to 14% above the 2024 baseline, increasing total A/B system cost and reducing the pricing bandwidth available to A/B system formulators to absorb the additional bio-based polyol premium in the Part A component without passing the full bio-attributed premium to customers. These factors substantially limit bio-based, biodegradable A/B polyurethane system market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Conventional A/B Systems (partial bio-content), Bioplastic A/B Systems (fully bio-based or biodegradable) | Conventional A/B Systems (partial bio-content) |

| Application | Flexible Foam, Rigid Foam, Coatings and Adhesives, Elastomers, Spray Applied Systems, Cast Systems | Flexible Foam |

| End Use | Automotive, Building and Construction, Furniture and Bedding, Footwear, Industrial, Consumer Goods | Automotive |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Conventional A/B Systems segment is expected to account for a significantly large revenue share in the global bio-based, biodegradable A/B polyurethane system market during the forecast period.

This report evaluates product type across Conventional A/B Systems (partial bio-content), Bioplastic A/B Systems (fully bio-based or biodegradable) for polyurethanes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Flexible Foam, Rigid Foam, Coatings and Adhesives, Elastomers, Spray Applied Systems, Cast Systems for polyurethanes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive, Building and Construction, Furniture and Bedding, Footwear, Industrial, Consumer Goods for polyurethanes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for polyurethanes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

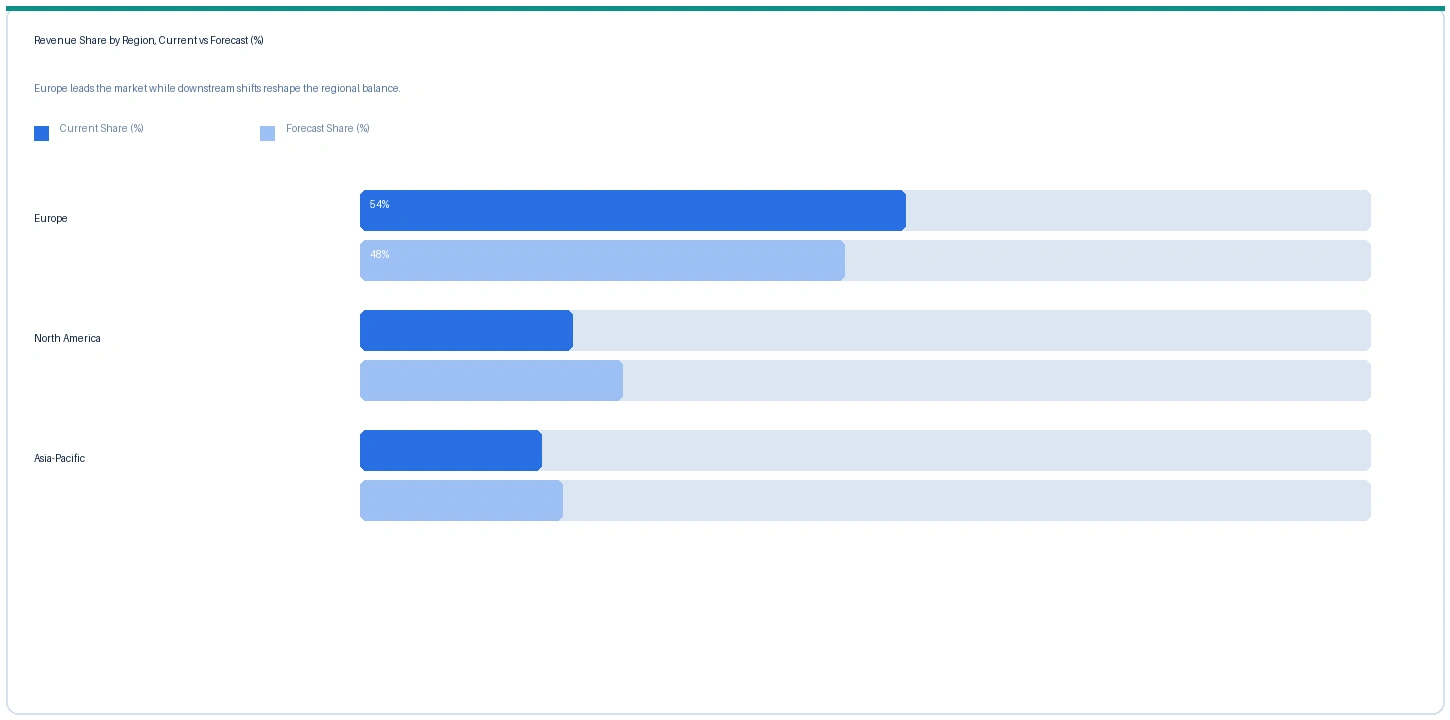

Europe market accounted for largest revenue share over other regional markets in the global bio-based, biodegradable A/B polyurethane system market in 2025. Based on regional analysis, the bio-based and biodegradable A/B polyurethane system market in Europe accounted for largest revenue share in 2025. EU CSRD mandatory Scope 3 reporting from January 2024 creates the concentrated European demand for bio-attributed A/B PU systems with supply chain documentation. Recticel NV at Brussels unveiled its first fully bio-based PU foam product for the bedding industry in Q4 2024. RAMPF Holding at Grafenberg, Germany formulates bio-attributed A/B PU systems for automotive, industrial, and specialty applications using bio-based polyol Part A components. Covestro Desmophen eco-grade polyols and BASF Sovermol natural oil polyols are the primary Part A bio-polyol feedstocks for European system formulators serving automotive and construction A/B PU system applications. EU Green Building and BREEAM certification schemes create specification preference for bio-based content spray-applied and cast rigid foam insulation A/B PU systems.

North America market accounted for second largest revenue share in the global bio-based, biodegradable A/B polyurethane system market in 2025. The market in North America is expected to register the second largest revenue share. The US market was valued at USD 289.86 million in 2024 at 4.2% CAGR per Grand View Research primary market assessment, representing approximately 32% of global A/B bio-attributed PU system revenue. Future Foam's September 2024 commercial bedding foam launch using BASF BMB Lupranate T80 Part B TDI with bio-polyol Part A represents the most commercially significant US bio-attributed A/B PU system deployment to date. Cargill BiOH soy polyol Part A incorporation in Carpenter Co. flexible foam A/B systems for La-Z-Boy and bedding brand customers anchors the natural oil polyol A/B system market. Algenesis Soleic bioPU A/B system at La Jolla, California is the only fully biodegradable compostable A/B PU system commercially deployed in the US footwear and consumer goods markets.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global bio-based, biodegradable A/B polyurethane system market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate. China's footwear manufacturing sector -- producing approximately 60% of global footwear volume per year -- is the largest addressable market for bio-attributed A/B PU midsole and adhesive systems globally. Wanhua Chemical's Q4 2024 bio-based PU adhesive launch for footwear confirms that Chinese A/B system suppliers are adding bio-attributed Part A and Part B components for export-market customers requiring EU Scope 3 documentation. Japan's Mitsubishi Chemical Group BENEBiOL high-biomass polycarbonatediol is enabling Japanese TPU A/B system formulators to supply high bio-content coating and adhesive A/B systems for automotive and consumer goods markets. South Korean automotive and electronics manufacturers are early adopters of bio-attributed two-component PU system solutions under Korean Green New Deal and automotive supply chain sustainability frameworks.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Soleic bioPU A/B (52% bio, compostable) | North America | USD 8.40/kg system | USD 7.60/kg | Rising | Algenesis footwear ref |

| Partially bio A/B system (15-20% NOP Part A) | North America | USD 2.84/kg system | USD 2.58/kg | Rising | RAMPF / converter ref |

| Bio-attributed rigid foam A/B (ISCC Plus) | Europe | EUR 2.62/kg system | EUR 2.38/kg | Rising | Building insulation ref |

| BMB TDI-based flexible foam A/B (bedding) | North America | USD 3.40/kg system | USD 3.08/kg | Rising | Future Foam BMB ref |

| Standard fossil A/B flexible foam (reference) | Global | USD 2.24/kg system | USD 2.04/kg | Rising | Reference benchmark |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, A/B PU system formulator commercial disclosures, and polyurethane system trade publication monitoring. A/B PU system prices vary substantially by bio-content level, end-use application, certification status, and minimum order quantity. Prices are shown per kilogram of mixed A/B system at standard A/B ratio.

Algenesis Soleic bioPU A/B system pricing for footwear midsole flexible foam rose approximately 10.5% from USD 7.60 per kilogram system in Q2 2025 to USD 8.40 per kilogram in Q2 2026, maintaining a 3.75 times premium above standard fossil A/B flexible foam at USD 2.24 per kilogram. The premium reflects 52% certified bio-content, PFAS-free formulation, backyard compostability certification, and the production cost structure of Algenesis' current artisanal-scale algae and plant oil polyol synthesis, which has not yet achieved the scale manufacturing cost reduction required for broad footwear brand commercialisation. Partially bio-attributed A/B systems incorporating 15% to 20% natural oil polyol in the Part A component rose approximately 10.1% against Q2 2025, reflecting bio-based polyol Part A cost increases from soybean oil feedstock cost elevation from Midwest agricultural energy and Hormuz crude disruption pass-through and Part B MDI or TDI cost increases of 10% to 14% above 2024 baseline. Bio-attributed rigid foam A/B systems for European building insulation with ISCC PLUS Part A polyol documentation rose approximately 10.1% in Europe from Covestro Desmophen eco-grade and BASF Sovermol Part A cost elevation. The BASF BMB Lupranate T80-based bedding flexible foam A/B system rose approximately 10.4% against Q2 2025 from BMB TDI pricing increases and bio-polyol Part A cost pass-through. Hormuz-driven Part B isocyanate cost increases of 10% to 14% above 2024 baseline are applying uniform upward pressure across all A/B system configurations regardless of bio-content level in the Part A component.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the bio-based and biodegradable A/B polyurethane system market, the Hormuz disruption affects both the Part A polyol component and the Part B isocyanate component of A/B system economics, but through different supply chain mechanisms. Part B MDI and TDI cost increases of approximately 10% to 14% above the 2024 baseline from aniline and toluene feedstock cost elevation at Covestro, BASF, and Wanhua isocyanate production facilities are applying uniform upward cost pressure to all A/B PU systems regardless of Part A bio-content level. Part A natural oil polyol cost increases from soybean oil and castor oil feedstock agricultural energy cost pass-through add a secondary cost layer to bio-attributed A/B systems but are less severe than the naphtha-derived petrochemical cost increases affecting Part B. The net structural effect on the conventional versus bioplastic A/B system split is neutral to marginally positive for bioplastic systems in the near term: the premium of fully bio-based A/B systems above conventional systems has not widened significantly because both are exposed to Part B isocyanate cost elevation through the same supply chain. Separately, the Hormuz disruption is accelerating EU and US domestic bio-based chemical supply chain investment rationale under energy security and supply chain resilience policy frameworks, which over the 2026 to 2028 period should provide additional policy support for the domestic bio-isocyanate development programmes including Algenesis DOE grant that underpin the future fully bio-based A/B system commercial availability.

Company Insights

The two key dominant companies in the bio-based, biodegradable A/B polyurethane system market are Algenesis Corporation and Recticel NV, recognised for their positions as the developer of the only commercially available fully biodegradable compostable A/B bioPU system with 52% bio-content for footwear applications and the first major European foam converter to launch a fully bio-based A/B PU system for bedding, respectively, and their contrasting commercial positions as a technology-led startup with DOE bio-isocyanate scale-up backing and an established European foam converter with CSRD-compliant bio-attributed bedding foam system commercial channel.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 892.4 Million |

| Market Size 2032 | USD 1,286.8 Million |

| CAGR | 5.4% |

| Units | Revenue in USD Million |

| Segments Covered | By Product Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, Belgium, Netherlands, Japan, China, South Korea, Brazil, India |

| Companies Profiled | Algenesis Corporation, Recticel NV, RAMPF Holding, BASF SE, Covestro, Huntsman, Wanhua Chemical, Future Foam, Carpenter Co., Evonik Industries, Selena Group |

| Key Data Sources | GVR primary assessment US bio-based biodegradable A/B PU system market USD 289.86M in 2024 at 4.2% CAGR (conventional segment 87.8%, bioplastic 12.2%), Algenesis USD 5M seed round October 2023 + USD 5M DOE grant Soleic 52% bio-content footwear deployment, Recticel Q4 2024 first fully bio-based bedding PU foam commercial launch, BASF and Future Foam September 2024 BMB TDI bedding foam A/B system, BASF July 2024 certified bio-based footwear PU traceability, Recticel and Selena Q2 2024 spray insulation collaboration, Evonik Q1 2024 bio-based PU precursor pilot plant announcement, Wanhua Q4 2024 bio-based footwear adhesive launch, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 262 |

| Published | Q2 2026 |

| SKU | NXC-PC-020 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 15 expert interviews conducted between January and May 2026. Interview panels were structured across a 2x2 supply-side and demand-side grid with explicit geographic and role split. Supply-side contacts included A/B PU system formulator commercial and technical managers at European and North American system houses, bio-based polyol Part A sourcing leads at A/B system producers, and bio-based isocyanate technology development contacts at Algenesis and Evonik. Demand-side contacts included sustainability procurement and materials development leads at European furniture and bedding brands adopting fully bio-based A/B PU foam systems, footwear brand material sustainability programme managers evaluating compostable midsole A/B PU systems, and building and construction specification managers at European contractor firms implementing BREEAM and Green Building bio-content documentation requirements. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Grand View Research primary market assessment of the US bio-based and biodegradable A/B polyurethane system market at USD 289.86 million in 2024 at 4.2% CAGR with conventional segment at 87.8% and bioplastic segment at 12.2% of US market revenue, Algenesis Corporation seed round announcement October 2023 and DOE grant disclosure for Soleic bioPU A/B system at 52% bio-content in footwear midsoles, Recticel NV Q4 2024 commercial launch announcement for first fully bio-based bedding PU foam, BASF and Future Foam September 24 2024 commercial BMB Lupranate T80 bedding foam launch, BASF July 2024 certified traceability for bio-based footwear PU solutions, Recticel and Selena spray insulation collaboration Q2 2024, Evonik Q1 2024 bio-based PU precursor pilot plant announcement, Wanhua Chemical Q4 2024 bio-based footwear adhesive A/B system launch, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.