Market Data

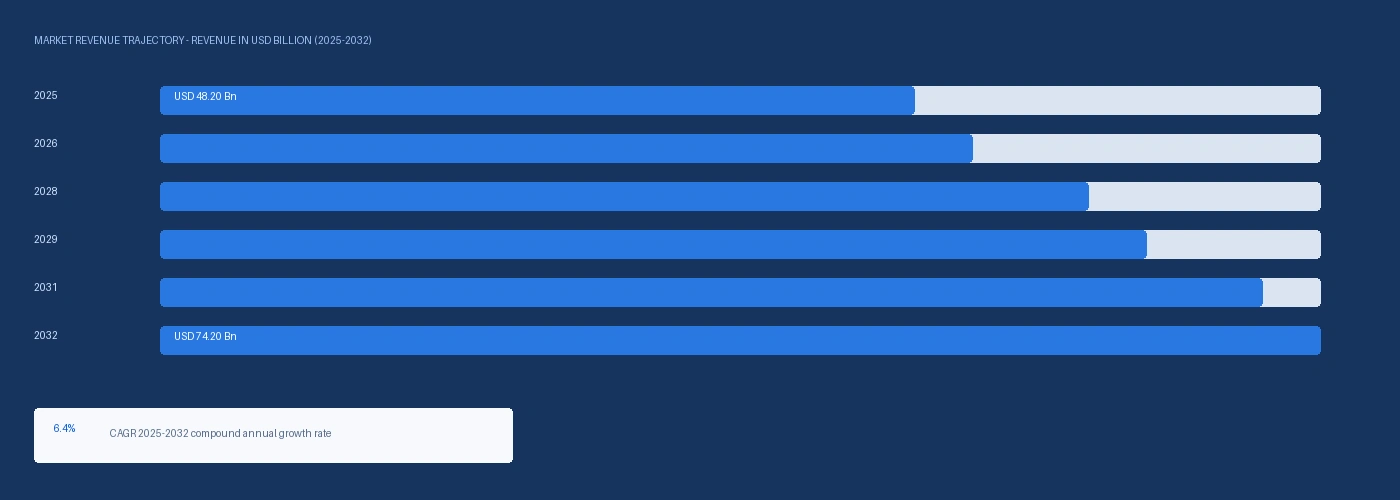

The global benzene market size was USD 48.20 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period. The 2025 market estimate is grounded in confirmed primary capacity data anchoring global benzene production volume in the 55 to 60 million metric tonne range — with BASF SE starting its 1 million tonne per year integrated cracker-styrene complex at Zhanjiang China in November 2025, ExxonMobil announcing expansion of light crude oil processing capacity by 250,000 barrels per day at its Beaumont Texas integrated refining and petrochemicals complex in March 2023 generating additional catalytic reforming-based benzene co-production, and Sinopec's SECCO joint venture at Shanghai confirmed at 4.2 million metric tonnes per year total petrochemical production capacity including benzene — and average 2025 benzene pricing in the USD 800 to USD 1,000 per metric tonne range per ICIS European and Asian spot price data, with ICIS confirming European benzene spot offers reaching up to USD 1,550 per tonne for May 2026 loading as Hormuz-related naphtha cost increases tightened the European market. BASF SE and Encina Development Group LLC signed an extended supply agreement in June 2024 for ISCC PLUS-certified circular benzene derived from post-consumer end-of-life plastics processed through chemical recycling, with BASF incorporating circular benzene into its production processes to strengthen its circular economy raw material credentials under EU chemical regulation frameworks. Bodal Chemicals Ltd announced the start-up of new specialty benzene downstream projects with 63,000 metric tonne per year capacity in March 2024, expanding Indian benzene derivative processing capability for pharmaceutical and agrochemical intermediates. For instance, in June 2024, Encina Development Group LLC, United States, an ISCC PLUS-certified circular chemical producer, and BASF SE, Germany, signed a partnership for an extended supply deal of chemically recycled circular benzene from post-consumer end-of-life plastics, with BASF incorporating circular-based raw materials into its production processes as part of its commitment to reduce carbon emissions and support the circular economy. These are some of the key factors driving revenue growth of the market.

BASF's Zhanjiang 1 million tonne per year cracker-styrene complex started November 2025 is the single largest new benzene-to-styrene capacity addition in 2025 and positions BASF to capture the benzene-to-styrene margin from captive benzene production rather than purchasing merchant benzene at market prices, with the integrated complex targeting Chinese domestic polystyrene and styrene-butadiene demand growth. Sinopec's SECCO Shanghai joint venture at 4.2 million metric tonnes per year total petrochemical production including benzene, toluene, ethylene, propylene, polyethylene, polypropylene, styrene, polystyrene, acrylonitrile, butadiene, and other derivatives represents China's largest single-site integrated benzene production and conversion operation. ExxonMobil's March 2023 Beaumont Texas expansion adding 250,000 barrels per day of light crude processing capacity generates additional reformate-stream benzene co-production at US Gulf Coast, with Beaumont's integrated refinery-petrochemicals complex allowing internal benzene conversion to ethylbenzene and cyclohexane downstream derivatives. ICIS benzene spot pricing data confirmed European benzene-naphtha spreads in the USD 335 to USD 440 per metric tonne range during 2024 to 2025, with Brent crude oil fluctuating between approximately USD 70 and USD 90 per barrel, creating benzene cash cost pressure at non-integrated European producers purchasing naphtha at market prices.

However, benzene is classified as a Group 1 human carcinogen by the International Agency for Research on Cancer, with occupational exposure limits of 1 ppm 8-hour time-weighted average under EU Directive 2017/164 and 0.5 ppm under OSHA PEL in the US, imposing handling, monitoring, and worker protection costs at all benzene production, transport, and use facilities that add regulatory compliance cost above non-carcinogenic aromatic solvent alternatives. ICIS confirmed benzene-naphtha spreads compressed from USD 440 to USD 335 per metric tonne during 2024 to 2025, with Brent crude fluctuating between USD 70 and USD 90 per barrel creating naphtha feedstock cost pressure on non-integrated European benzene producers whose production economics are fully exposed to naphtha price oscillations without internal cracker feedstock offset. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated naphtha feedstock costs at European benzene producers through GCC naphtha export restriction, with ICIS reporting European benzene offers reaching USD 1,550 per tonne in Q2 2026 with bid-offer spreads widening to USD 280 per tonne as transatlantic arbitrage reopened with ICIS shipping data confirming at least 14,500 tonnes shipped from Antwerp to the US on 30 April 2026. These factors substantially limit benzene market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

BASF's November 2025 start-up of its 1 million tonne per year Zhanjiang cracker-styrene complex is the single largest new benzene-to-styrene capacity addition in 2025, confirming Asia-Pacific as the primary geography for new integrated benzene capacity investment aligned with styrene demand growth from polystyrene packaging, ABS automotive interior, and styrene-butadiene rubber applications in the region. Sinopec's SECCO joint venture at 4.2 million metric tonnes per year total petrochemical capacity including benzene and styrene at Shanghai represents China's established benzene production and conversion scale. ExxonMobil's March 2023 Beaumont Texas 250,000 barrel per day expansion adds incremental catalytic reforming-based benzene co-production at the US Gulf Coast, reinforcing North American integrated producer capacity. BASF's Encina circular benzene supply agreement in June 2024 establishes the first commercially contracted ISCC PLUS-certified circular benzene supply at scale at an integrated European producer, positioning BASF for EU circular economy regulation compliance requirements. Bodal Chemicals Downstream Expansion and Pharmaceutical Derivative Demand Growing Bodal Chemicals Ltd announced the start-up of new specialty benzene downstream projects at 63,000 metric tonne per year capacity in March 2024, expanding Indian benzene derivative processing capability for pharmaceutical and agrochemical intermediate applications at dyes, intermediates, and specialty chemicals manufacturing facilities in Gujarat. Benzene-derived aniline, cyclohexane, and phenol are used in paracetamol, aspirin, nylon API synthesis intermediates, and specialty pharmaceutical chemistry, with pharmaceutical derivative growth benefiting from Indian and Chinese generic pharmaceutical manufacturing expansion targeting export markets.

IARC Group 1 benzene carcinogen classification and EU Directive 2017/164 (1 ppm OEL) and OSHA PEL (0.5 ppm) occupational exposure limit regulations impose continuous benzene monitoring, specialised vapour-tight loading and unloading equipment, medical surveillance programmes, and personal protective equipment costs at all benzene handling facilities. ICIS confirmed benzene-naphtha spreads compressed from USD 440 to USD 335 per metric tonne during 2024 to 2025, reducing non-integrated European producer margins. The US-Iran conflict and Strait of Hormuz disruption confirmed by the IMF in March 2026 elevated naphtha feedstock costs at European producers, compressing spreads below 2025 baseline levels while simultaneously producing European benzene spot price elevation to USD 1,550 per tonne offers per ICIS Q2 2026 reporting, creating a bifurcated market favouring integrated producers over non-integrated merchant benzene facilities. These factors substantially limit benzene market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Production Process | Catalytic Reforming, Steam Cracking, Toluene Disproportionation, Hydrodealkylation | Catalytic Reforming |

| Derivative | Ethylbenzene, Cumene, Cyclohexane, Nitrobenzene, Alkylbenzene, Maleic Anhydride | Ethylbenzene |

| End Use | Plastics and Polymers, Rubber, Pharmaceuticals, Agrochemicals, Paints and Coatings | Plastics and Polymers |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Catalytic Reforming segment is expected to account for a significantly large revenue share in the global benzene market during the forecast period.

This report evaluates production process across Catalytic Reforming, Steam Cracking, Toluene Disproportionation, Hydrodealkylation for aromatics, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates derivative across Ethylbenzene, Cumene, Cyclohexane, Nitrobenzene, Alkylbenzene, Maleic Anhydride for aromatics, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Plastics and Polymers, Rubber, Pharmaceuticals, Agrochemicals, Paints and Coatings for aromatics, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for aromatics, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

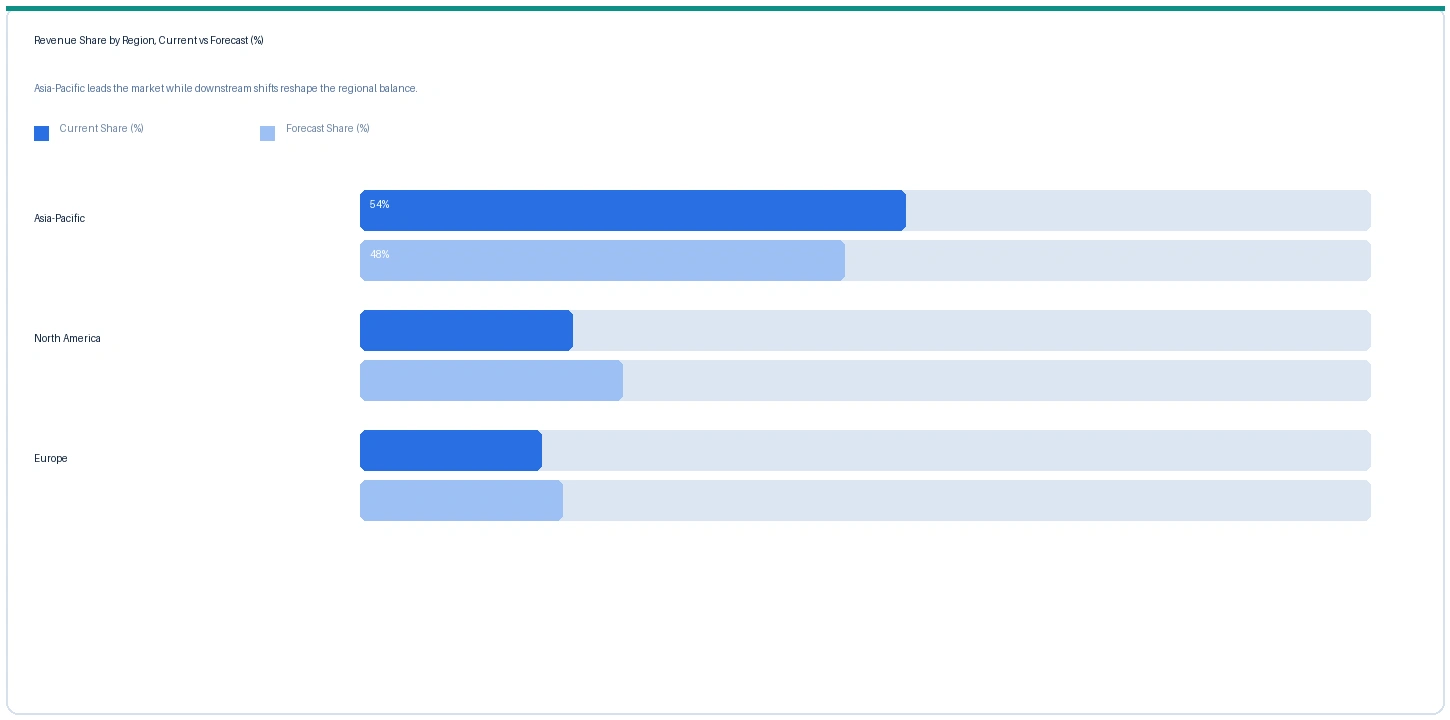

Asia-Pacific market accounted for largest revenue share over other regional markets in the global benzene market in 2025. Based on regional analysis, the benzene market in Asia-Pacific accounted for largest revenue share in 2025. Sinopec's SECCO Shanghai joint venture at 4.2 million metric tonnes per year total petrochemical capacity including benzene, toluene, styrene, and polystyrene represents China's largest single-site integrated benzene production operation. BASF's November 2025 Zhanjiang 1 million tonne per year cracker-styrene start-up adds the single largest new 2025 benzene capacity in China at one integrated facility, directly expanding China's benzene-to-styrene conversion at BASF's Verbund-equivalent integration model.

The market in North America is driven by ExxonMobil's March 2023 Beaumont Texas 250,000 barrels per day light crude processing expansion generating incremental catalytic reforming benzene co-production, Chevron Phillips Chemical Company's integrated benzene and derivatives production, LyondellBasell's North American Gulf Coast operations, and INEOS US benzene production. ICIS shipping data confirmed at least 14,500 tonnes of benzene shipped from Antwerp to the US on 30 April 2026 as transatlantic arbitrage reopened, confirming the US as a net benzene importer requiring European and Asian supply supplementation.

Europe market is expected to register steady demand in the global benzene market during the forecast period. The market in Europe faces margin pressure from ICIS-confirmed benzene-naphtha spread compression from USD 440 to USD 335 per metric tonne during 2024 to 2025, with the Hormuz naphtha cost elevation further compressing non-integrated producer margins in Q2 2026. BASF at Ludwigshafen, INEOS at Grangemouth and Cologne, and TotalEnergies at European facilities are primary European benzene producers. BASF's June 2024 Encina circular benzene supply agreement confirms European integrated producers' strategy of building circular feedstock credentials for EU chemical circular economy regulation positioning.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Benzene Spot (European FOB ARA) | Europe | USD 1,480/MT | USD 1,160/MT | Rising | ICIS Q2 2026 confirmed |

| Benzene Spot (US Gulf Coast) | North America | USD 1,360/MT | USD 1,100/MT | Rising | ICIS USG ref |

| Benzene Spot (Asia FOB Korea) | Asia-Pacific | USD 1,220/MT | USD 1,020/MT | Stable | ICIS Asian ref |

| Circular Benzene (ISCC PLUS cert.) | Europe | USD 1,740/MT | USD 1,480/MT | Rising | BASF/Encina premium ref |

| Naphtha (benchmark reference) | Europe | USD 1,080/MT | USD 800/MT | Rising | ICIS naphtha spread ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts and ICIS benzene market trade reporting. Benzene prices reflect highly liquid global market dynamics with significant regional variation.

European benzene spot prices rose approximately 27.6% in Q2 2026 against Q2 2025 per ICIS market reporting, reaching offered levels of up to USD 1,550 per tonne with bid-offer spreads widening to USD 280 per tonne, driven by naphtha feedstock cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 affecting GCC naphtha export availability, combined with transatlantic arbitrage reopening with ICIS shipping data confirming at least 14,500 tonnes shipped from Antwerp to the US on 30 April 2026. ICIS confirmed benzene-naphtha spreads in the USD 335 to USD 440 per metric tonne range during 2024 to 2025, with Brent crude fluctuating between USD 70 and USD 90 per barrel, providing the pricing context within which the Q2 2026 price spike represents a Hormuz-driven departure from the prior 18-month trend range. Circular benzene at ISCC PLUS certification commands a premium of approximately USD 260 per metric tonne above European conventional spot in Q2 2026 per BASF-Encina supply agreement disclosed value, with the premium growing as EU circular economy regulation creates mandatory certified content requirements.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the benzene market, the Hormuz disruption operates through naphtha feedstock cost elevation as the primary production cost impact channel. GCC naphtha exports from Saudi Aramco and ADNOC to Asian and European cracker operators are restricted by Hormuz disruption, elevating naphtha spot prices and compressing benzene-naphtha spreads at non-integrated European benzene producers fully exposed to naphtha market pricing without internal captive feedstock offset. ICIS reported European benzene spot offers reaching up to USD 1,550 per tonne in Q2 2026 with bid-offer spreads of USD 280 per tonne and transatlantic arbitrage opening with at least 14,500 tonnes shipped from Antwerp to the US on 30 April 2026, confirming the Hormuz-driven European benzene market tightening as naphtha cost elevation both raised production cost and incentivised US-bound export of European benzene supply. BASF's Zhanjiang complex producing captive benzene from its own cracker feedstock, and Sinopec's SECCO operating from integrated domestic Chinese naphtha supply chains, are structurally insulated from the naphtha spot price elevation affecting non-integrated European merchant benzene producers.

Company Insights

The two key dominant companies in the benzene market are BASF SE and Sinopec (China Petroleum and Chemical Corporation), recognised for their vertically integrated petrochemical complex scale spanning naphtha feedstock through benzene production to ethylbenzene and styrene downstream derivatives, their strategic leadership in both conventional benzene capacity expansion and circular benzene supply chain development, and their structural insulation from benzene-naphtha spread compression through captive feedstock integration.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 48.20 Billion |

| Market Size 2032 | USD 74.20 Billion |

| CAGR | 6.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Production Process, By Derivative, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, France, Netherlands, UK, China, Japan, South Korea, India, Saudi Arabia, Brazil |

| Companies Profiled | BASF SE, Sinopec, ExxonMobil, SABIC, Chevron Phillips Chemical, LyondellBasell, INEOS, TotalEnergies, Reliance Industries, Braskem, Formosa Chemicals, Hengli Petrochemical |

| Key Data Sources | BASF SE Zhanjiang cracker-styrene complex 1 Mt/yr start-up November 2025 (company disclosure). BASF SE and Encina Development Group circular benzene supply agreement June 2024 (company announcement). ICIS benzene spot pricing data: European offers up to USD 1,550/tonne May 2026 loading; bid-offer spread USD 280/tonne; benzene-naphtha spread USD 335-440/tonne range 2024-25; Brent crude USD 70-90/bbl during period. ICIS shipping data: 14,500 tonnes benzene Antwerp to US 30 April 2026. Sinopec SECCO joint venture: 4.2 Mt/yr total petrochemical capacity including benzene (SECCO company data). ExxonMobil Beaumont Texas 250,000 bbl/day light crude expansion announcement March 2023. Bodal Chemicals 63,000 MTPA specialty benzene downstream start-up March 2024. EU Directive 2017/164 benzene OEL 1 ppm. OSHA benzene PEL 0.5 ppm. IARC Group 1 benzene carcinogen classification. IMF March 2026 Strait of Hormuz statement. 17 primary expert interviews. |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 268 |

| Published | Q2 2026 |

| SKU | NXC-PC-013 |

Scope & Methodology

Nexchem Intelligence primary research comprised 17 expert interviews between January and May 2026 across a 2x2 supply-side and demand-side grid. Supply-side contacts included benzene production and commercial trading leads at European, North American, and Asian integrated petrochemical producers, benzene arbitrage trading desk contacts at international commodity trading companies, and circular benzene development programme leads. Demand-side contacts included ethylbenzene and styrene production procurement leads at Asian and European polymer producers, cyclohexane and nylon intermediate procurement managers, and pharmaceutical benzene derivative procurement specialists. Primary research was conducted exclusively by the Nexchem Intelligence analyst team with no expert network firm involvement.

Secondary research sources include BASF SE Zhanjiang cracker-styrene complex start-up announcement November 2025, BASF SE and Encina Development Group circular benzene supply agreement announcement June 2024, ICIS benzene spot pricing and European market Q2 2026 reporting confirming European offers up to USD 1,550 per tonne, bid-offer spread USD 280 per tonne, benzene-naphtha spread USD 335 to USD 440 per tonne range during 2024 to 2025, and ICIS shipping data confirming 14,500 tonnes Antwerp to US on 30 April 2026, Sinopec SECCO joint venture 4.2 million tonne per year capacity data, ExxonMobil Beaumont Texas 250,000 barrel per day expansion announcement March 2023, Bodal Chemicals 63,000 MTPA specialty downstream start-up announcement March 2024, EU Directive 2017/164 benzene occupational exposure limit, OSHA benzene PEL, IARC Group 1 benzene carcinogen classification, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.