Market Data

The global below grade waterproofing membranes market size was USD 4.22 Billion in 2025 and is expected to register a revenue CAGR of 5.2% during the forecast period. The 2025 market estimate is grounded in Sika AG's 2024 Annual Report disclosing total construction chemicals and industry market volume of more than CHF 110 billion with Sika holding approximately 11% market share as the global market leader, which at Sika's 2024 net sales of CHF 11,763.1 million implies a total addressable market from which waterproofing is one of Sika's six primary target segments, with below-grade waterproofing representing the largest and most technically complex segment within Sika's waterproofing portfolio. Sika AG's 2025 Annual Report confirmed acquisition of a leading manufacturer of bituminous waterproofing membranes based in Riyadh Saudi Arabia, directly citing Sika's intent to significantly strengthen its position in the fast-growing Saudi and GCC construction markets where below-grade waterproofing specification is structurally driven by saline groundwater and sabkha soil conditions requiring positive-side membrane protection at all below-grade building foundations and infrastructure structures. Oriental Yuhong commenced construction of a new facility in Houston Texas in August 2024 including Phase One production lines for TPO waterproof membranes and a North American R&D centre, representing the largest Chinese waterproofing manufacturer's direct manufacturing entry into the North American market for below-grade and roofing membrane products. W.R. Meadows Inc. launched Meadow-Pruf Co-Spray in December 2024, a liquid waterproofing membrane designed for below-grade vertical applications with cold-weather performance capability, confirming continued North American product development activity in the liquid-applied below-grade segment. International Building Code Section 1805 mandates waterproofing or dampproofing at all below-grade structures, establishing a regulatory demand floor in the North American market independent of construction cycle variations. For instance, Sika AG, Switzerland, acquired American Hydrotech Inc. in July 2021 to expand its below-grade horizontal and plaza deck waterproofing position in North America, confirming Sika's strategic commitment to below-grade waterproofing as a primary growth segment within its broader construction chemicals portfolio. These are some of the key factors driving revenue growth of the market.

Saint-Gobain S.A., following its acquisition of GCP Applied Technologies in 2022, operates Bituthene self-adhesive rubberised asphalt and modified bitumen below-grade waterproofing membrane systems and Voltex bentonite geosynthetic clay liner waterproofing panels, with GCP Applied Technologies having been the North American market leader in positive-side below-grade waterproofing specification for over four decades before its integration into Saint-Gobain's specialty construction products platform. SOPREMA Group at Strasbourg France is a leading European waterproofing membrane producer supplying below-grade, roofing, and facade membrane systems, having acquired Sika's waterproofing business in March 2022 for EUR 1.3 billion, establishing SOPREMA as one of the most significant post-acquisition waterproofing businesses in Europe. BASF's MasterSeal spray-applied polyurethane membrane systems for below-grade vertical applications, Mapei S.p.A.'s Mapelastic cementitious waterproofing systems, and Carlisle Companies' proprietary below-grade membrane product ranges represent the secondary competitive tier in the global below-grade waterproofing membranes market. Penetron Admix crystalline waterproofing admixture was specified in September 2024 for below-grade concrete infrastructure protection against elevated groundwater levels, confirming growing crystalline admixture adoption alongside external membrane systems at below-grade structural concrete applications.

However, below-grade waterproofing membrane applications are specification-driven through engineer-of-record material selection processes requiring listing against ASTM standards, ICC evaluation service reports, and project-specific hydrostatic pressure performance data that create 12 to 24 month sales cycles from material qualification to project purchase order, making revenue timing unpredictable relative to construction project start schedules. Chinese residential real estate construction volume declined materially through 2024 as Evergrande and Country Garden Group restructuring processes reduced new housing starts, with National Bureau of Statistics China data showing residential floor area under construction declining approximately 10% to 15% in 2024 from 2023 levels, directly reducing below-grade basement waterproofing membrane consumption from the largest single regional below-grade market. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated SBS and APP bituminous modifier polymer production costs through styrene-butadiene and polypropylene feedstock increases from naphtha cost elevation, adding approximately USD 0.18 to USD 0.28 per square metre to bituminous modified sheet membrane production cost in Q2 2026. These factors substantially limit below grade waterproofing membranes market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Sika AG's 2024 Annual Report establishing total construction chemicals and industry market volume at more than CHF 110 billion, with only a combined approximately 40% market share held by the ten largest companies, confirms the fragmented and growth-opportunity-rich structure of the broader market in which below-grade waterproofing participates. Sika's 2025 Annual Report confirming acquisition of a bituminous waterproofing manufacturer in Riyadh Saudi Arabia directly signals growth investment in GCC below-grade construction markets driven by Saudi Vision 2030 infrastructure and commercial real estate development, NEOM gigaproject underground infrastructure, and Riyadh Metro Phase 2 tunnel construction generating below-grade waterproofing membrane demand at positive-side specifications required by GCC saline groundwater and sabkha soil conditions. The US Bipartisan Infrastructure Law allocating USD 1.2 trillion in infrastructure investment including subway rehabilitation, road tunnel reconstruction, and underground utility corridor construction generates North American below-grade waterproofing specification demand above the residential and commercial building construction baseline through to 2030. Subway and Metro Infrastructure Expansion Driving Specification-Grade Tunnel Waterproofing Demand Urban metro and subway network expansion in China, India, and the Middle East generates below-grade waterproofing membrane demand at engineer-of-record specification grade, with each kilometre of cut-and-cover subway tunnel consuming approximately 8,000 to 12,000 square metres of below-grade waterproofing membrane at positive-side application. IBC Section 1805 establishes the US code requirement baseline for below-grade waterproofing at commercial and residential construction, with analogous codes in the EU (EN 13967 polymer-modified bituminous sealing sheets, EN 13984 PE sheets) and India (IS 3067) providing regulatory demand floors. Oriental Yuhong's Houston facility commenced August 2024 indicates Chinese manufacturer confidence in sustained North American below-grade construction activity and represents the first direct-manufacturing competitive threat from Chinese producers in the North American specification-grade below-grade waterproofing market.

Chinese residential real estate construction volume declining approximately 10% to 15% in 2024 per National Bureau of Statistics China data from Evergrande and Country Garden restructuring directly reduces the largest single regional below-grade waterproofing membrane consumption market. The 12 to 24 month engineer-of-record specification and approval cycle for below-grade waterproofing materials at commercial and infrastructure construction projects creates revenue timing uncertainty for membrane manufacturers who invest in specification activity without assured revenue within budget year cycles. The US-Iran conflict and Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated SBS and APP bitumen modifier polymer costs, adding approximately USD 0.18 to USD 0.28 per square metre to bituminous modified sheet membrane production cost in Q2 2026 that cannot be immediately recovered at fixed-price project commitments. These factors substantially limit below grade waterproofing membranes market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Membrane Type | Sheet-Based, Liquid-Applied, Bentonite GCL, Crystalline Waterproofing | Sheet-Based |

| Position | Positive-Side, Negative-Side, Blind-Side | Positive-Side |

| Material | Bituminous, PVC, HDPE, Polyurethane, Cementitious | Bituminous |

| End Use | Commercial, Residential, Infrastructure, Industrial | Commercial |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Sheet-Based Membrane segment is expected to account for a significantly large revenue share in the global below grade waterproofing membranes market during the forecast period.

This report evaluates membrane type across Sheet-Based, Liquid-Applied, Bentonite GCL, Crystalline Waterproofing for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates position across Positive-Side, Negative-Side, Blind-Side for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates material across Bituminous, PVC, HDPE, Polyurethane, Cementitious for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Commercial, Residential, Infrastructure, Industrial for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

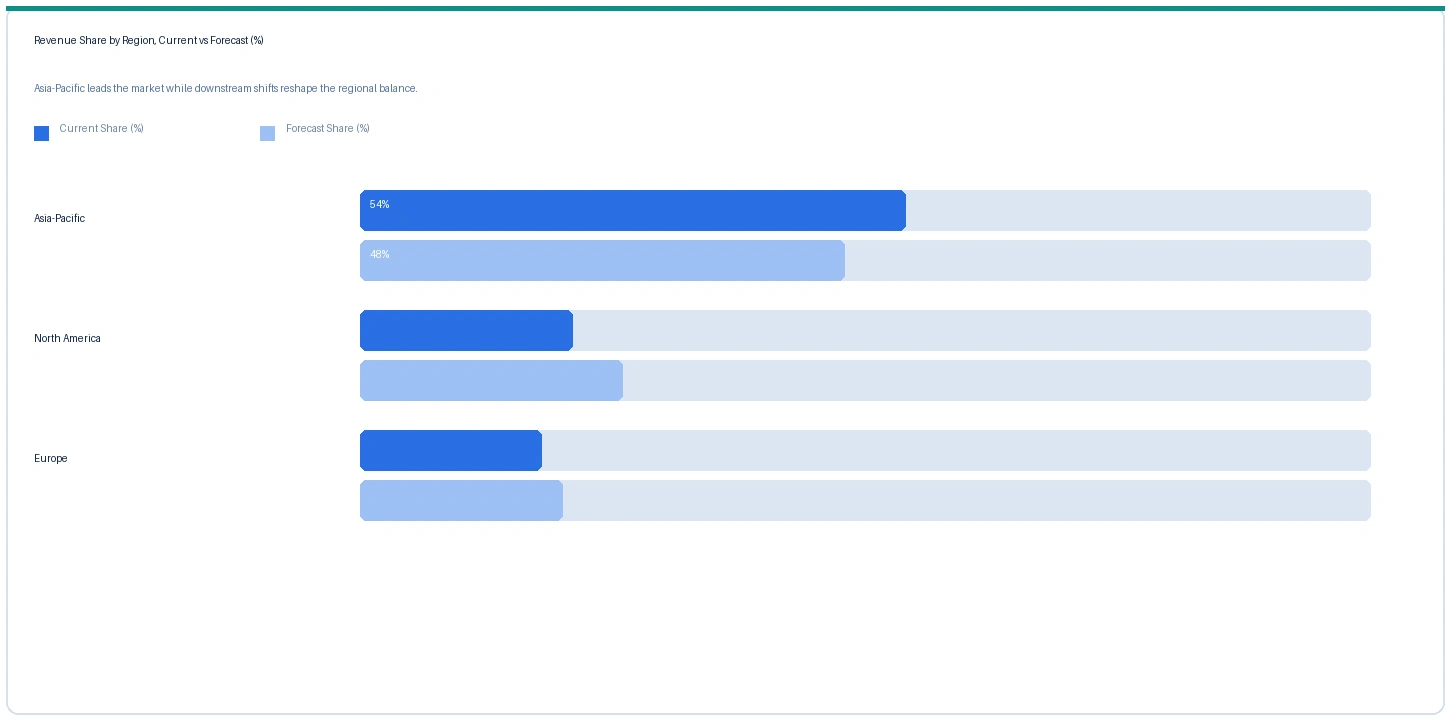

Asia-Pacific market accounted for largest revenue share over other regional markets in the global below grade waterproofing membranes market in 2025. Based on regional analysis, the below grade waterproofing membranes market in Asia-Pacific accounted for largest revenue share in 2025 at approximately 45% of global revenue. China is the single largest national market driven by urban metro network expansion and commercial high-rise below-grade car park construction. Oriental Yuhong (Beijing Oriental Yuhong Waterproof Technology Co. Ltd.) is China's largest domestic waterproofing manufacturer, expanding internationally with its Houston Texas facility commenced August 2024. Sika's 2024 Annual Report confirmed Asia-Pacific as a primary growth region within its construction chemicals portfolio at its current CHF 11,763.1 million total net sales.

North America market is expected to register steady revenue growth in the global below grade waterproofing membranes market during the forecast period. The market in North America is driven by US Bipartisan Infrastructure Law funding for subway rehabilitation, road tunnel reconstruction, and underground utility corridor construction generating above-baseline below-grade waterproofing demand, and IBC Section 1805 mandating waterproofing at all below-grade structures providing a regulatory demand floor. GCP Applied Technologies (now Saint-Gobain) Bituthene and Voltex systems, Sika Americas, and W.R. Meadows are the primary North American below-grade waterproofing specification players, with Oriental Yuhong's August 2024 Houston facility representing the first direct Chinese-manufactured product entry into the North American market.

Europe market accounted for second largest revenue share in the global below grade waterproofing membranes market in 2025. The market in Europe is driven by EN 13967 and EN 13984 code requirements, SOPREMA Group's European leadership following its EUR 1.3 billion acquisition of Sika's waterproofing business in March 2022, and Sika AG's European operations at Baar Switzerland. European below-grade waterproofing demand is supported by Northern and Central European groundwater management and energy-efficient building renovation programmes requiring below-grade moisture control.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Self-Adhered Modified Bitumen Sheet (4mm) | North America | USD 8.60/m² | USD 7.90/m² | Rising | GCP Bituthene / Sika ref |

| HDPE Sheet Membrane (1.5mm) | Europe | USD 6.40/m² | USD 5.90/m² | Stable | SOPREMA / Carlisle ref |

| Liquid-Applied PU Membrane (spray) | Asia-Pacific | USD 10.20/m² | USD 9.40/m² | Rising | BASF MasterSeal / Sika ref |

| Bentonite GCL (Voltex type) | North America | USD 7.60/m² | USD 7.00/m² | Stable | Saint-Gobain GCP ref |

| Crystalline Waterproofing Admixture | Global | USD 4.40/m² | USD 4.00/m² | Rising | Penetron ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts and construction specification project price monitoring. Prices represent installed material supply cost per square metre excluding labour at specification-grade products.

Self-adhered modified bitumen sheet membrane prices in North America rose approximately 8.9% in Q2 2026 against Q2 2025, driven by SBS polymer modifier cost increases from styrene-butadiene feedstock elevation through propylene and butadiene cost increases from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026. Liquid-applied polyurethane membrane prices in Asia-Pacific rose approximately 8.5% on MDI isocyanate feedstock cost elevation. Crystalline waterproofing admixture prices rose approximately 10% globally on growing demand at GCC infrastructure projects combined with Portland cement and chemical admixture raw material cost increases.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the below grade waterproofing membranes market, the Hormuz disruption operates through bituminous membrane raw material cost elevation and GCC construction logistics impact. Bituminous modified sheet membranes using SBS and APP polymer modifiers source styrene-butadiene copolymer and polypropylene feedstock from petrochemical producers exposed to naphtha cost elevation from Hormuz-disrupted GCC naphtha exports, adding USD 0.18 to USD 0.28 per square metre to bituminous modified sheet membrane production cost in Q2 2026. Sika's Riyadh bituminous waterproofing manufacturer acquisition confirmed in its 2025 Annual Report specifically positions Sika to supply GCC construction projects from local production insulated from marine freight disruption and import container insurance premium increases affecting competitor European and Chinese supply chains at GCC project sites.

Company Insights

The two key dominant companies in the below grade waterproofing membranes market are Sika AG and Saint-Gobain S.A. (through GCP Applied Technologies), recognised for their comprehensive below-grade waterproofing system portfolios, their established engineer-of-record specification relationships at commercial, infrastructure, and industrial below-grade construction projects globally, and their technical leadership in crack-bridging and hydrostatic pressure-rated waterproofing membrane development.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 4.22 Billion |

| Market Size 2032 | USD 6.04 Billion |

| CAGR | 5.2% |

| Units | Revenue in USD Billion |

| Segments Covered | By Membrane Type, By Position, By Material, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, UK, Germany, France, Switzerland, China, India, Singapore, Saudi Arabia, UAE, Brazil |

| Companies Profiled | Sika AG, Saint-Gobain/GCP Applied Technologies, SOPREMA Group, Oriental Yuhong, RPM International, BASF SE, Mapei, Carlisle Companies, Minerals Technologies, Fosroc, Kryton International, W.R. Meadows |

| Key Data Sources | Sika AG 2024 Annual Report: CHF 11,763.1M net sales; construction chemicals and industry market >CHF 110 Bn; Sika ~11% market share. Sika AG 2025 Annual Report: acquisition of bituminous waterproofing manufacturer Riyadh Saudi Arabia; GCC market strengthening. Oriental Yuhong Houston Texas facility construction commencement announcement August 2024. W.R. Meadows Meadow-Pruf Co-Spray product launch announcement December 2024. Penetron Admix below-grade specification September 2024. SOPREMA Group acquisition of Sika waterproofing business March 2022 (EUR 1.3 billion). Saint-Gobain GCP Applied Technologies acquisition completion 2022. Sika American Hydrotech acquisition July 2021. US Bipartisan Infrastructure Law infrastructure investment allocation. IBC Section 1805 below-grade waterproofing code requirement. EN 13967 and EN 13984 European waterproofing sheet standards. IMF March 2026 Strait of Hormuz statement. 15 primary expert interviews. |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 252 |

| Published | Q2 2026 |

| SKU | NXC-CM-001 |

Scope & Methodology

Nexchem Intelligence primary research comprised 15 expert interviews between January and May 2026 across a 2x2 supply-side and demand-side grid. Supply-side contacts included below-grade waterproofing membrane manufacturer commercial and technical representatives at North American and European producers, Asian manufacturing expansion project leads, and trained applicator distributor network managers. Demand-side contacts included civil and structural engineer-of-record specification leads at commercial high-rise and infrastructure project design consultancies, below-grade waterproofing specification procurement managers at major construction contractor organisations, and public sector infrastructure procurement managers at metro and tunnel construction authorities. Primary research was conducted exclusively by the Nexchem Intelligence analyst team with no expert network firm involvement.

Secondary research sources include Sika AG 2024 Annual Report (CHF 11,763.1M net sales; construction chemicals market >CHF 110 Bn; Sika ~11% market share), Sika AG 2025 Annual Report (Riyadh bituminous waterproofing manufacturer acquisition; GCC market expansion), Oriental Yuhong Houston facility commencement announcement August 2024, W.R. Meadows Meadow-Pruf Co-Spray product launch announcement December 2024, Penetron Admix below-grade specification announcement September 2024, SOPREMA Group acquisition of Sika waterproofing business March 2022, Saint-Gobain GCP Applied Technologies acquisition completion 2022, Sika American Hydrotech acquisition announcement July 2021, US Bipartisan Infrastructure Law investment allocation data, International Building Code Section 1805 below-grade waterproofing requirements, EN 13967 and EN 13984 European waterproofing standards, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.