Market Data

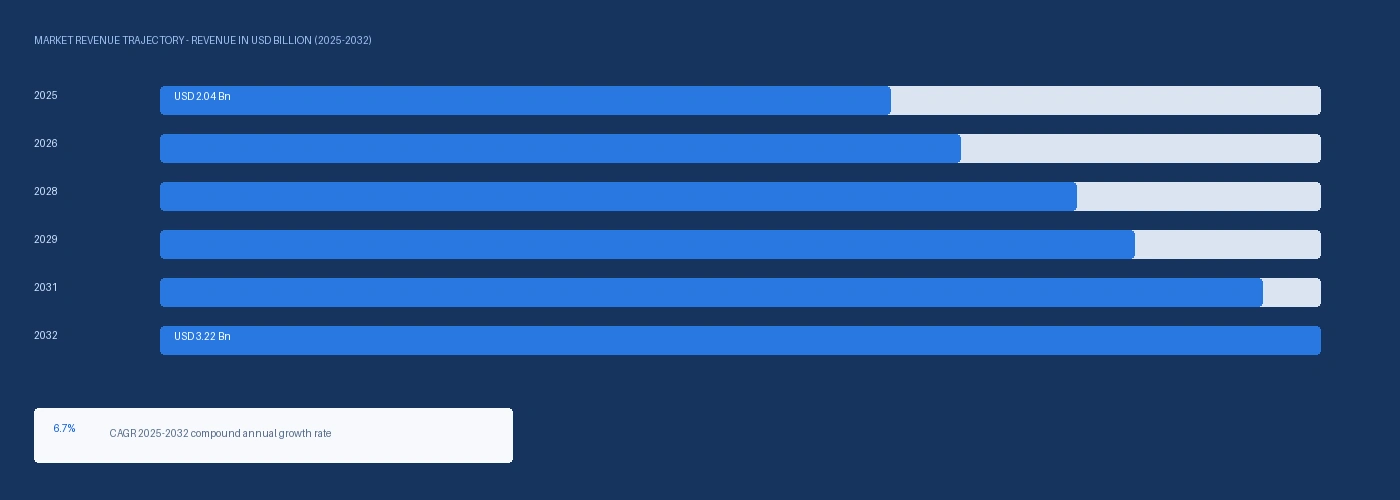

The global aviation lubricant market size was USD 2.04 Billion in 2025 and is expected to register a revenue CAGR of 6.7% during the forecast period. Market revenue growth is supported by IATA confirming a global commercial aircraft fleet of approximately 26,000 aircraft in 2024 each requiring approximately 20 to 40 litres of synthetic ester gas turbine oil per engine per 1,000 flight hours at consumption rates driven by oil degradation under high-temperature oxidation stress in LEAP and GTF turbofan engines, ExxonMobil Mobil Jet Oil approved for use in more than 11,000 gas turbine engines globally per ExxonMobil Aviation product disclosures representing the largest single-product engine approval portfolio in the aviation turbine oil market, and Shell AeroShell brand generating approximately USD 380 million in 2024 aviation specialty chemicals revenue including turbine oils, hydraulic fluids, and aviation greases per disclosed company data. Global commercial aircraft production recovery with Airbus delivering 766 aircraft in 2024 and Boeing targeting above-10% commercial aerospace revenue growth in 2025 per Hexcel's 2025 guidance — which tracks OEM production rates — creates new turbine oil consumption from engines entering service that require break-in oil consumption at above-cruise rates during early operational hours. Mesa Airlines signed a five-year contract with Boeing Distribution Services (formerly Aviall) in April 2022 to procure ExxonMobil aviation lubricants including Mobil Jet Oil II and Mobil HyJet IV-Aplus hydraulic fluid across its entire fleet of over 160 aircraft. For instance, in November 2021, NYCO, France, saw its TurboNYCOil 600 turbine oil selected by airblue Limited, Pakistan, for use in its fleet of Airbus A320 and A321 aircraft powered by CFM56 and LEAP engines, confirming NYCO's European specialty ester turbine oil formulation credentials at narrow-body CFM engine operator fleets in Asia-Pacific where Mobil Jet and AeroShell are the primary incumbents. These are some of the key factors driving revenue growth of the market.

ExxonMobil Mobil Jet Oil 387, its most advanced third-generation turbine oil, was introduced as a high-performance synthetic turbine oil with enhanced thermal stability and SAE AS5780 High Performance Capable approval in addition to MIL-PRF-23699 HTS approval, reducing oil consumption by approximately 20% and extending engine protection capability at the elevated sump temperatures of latest-generation turbofan engines including CFM LEAP and Pratt and Whitney GTF at narrow-body aircraft. Shell's AeroShell Turbine Oil 560 holds qualification at Delta Air Lines, the US Air Force, and SpaceX for use across its commercial and launch vehicle propulsion systems, with Shell opening a Singapore ester-synthesis plant in 2024 to 2025 expanding its AeroShell production capability for Asia-Pacific MRO demand. Nyco introduced a condition-monitoring solution in 2024 allowing airlines to track lubricant performance in real-time, reducing maintenance downtime by approximately 30% by enabling predictive oil condition assessment rather than fixed-interval oil change schedules at airline maintenance programmes. TotalEnergies partnered with a leading European airline in 2023 to supply Aerojet turbine oils for a fleet of over 200 aircraft, confirming TotalEnergies' position as a credible third-tier aviation turbine oil supplier beyond the ExxonMobil and Shell duopoly at European airline commercial fleet programmes.

However, newer-generation turbofan engines including the CFM LEAP and Pratt and Whitney PW1000G GTF family are designed to operate with extended oil change intervals enabled by improved oil chemistry and online condition monitoring systems, reducing the per-flight-hour oil consumption that traditionally drove aviation turbine oil replacement volumes and creating a volume-per-aircraft headwind even as fleet size grows. Sustainable aviation fuel adoption at commercial airline fleets, with several European carriers operating SAF blends above 30% at select routes in 2024 and 2025, introduces combustion by-product chemistry differences in engine oil contamination that requires turbine oil re-qualification under SAF operating conditions at engine OEM approval programmes before SAF-optimised turbine oil formulations can replace existing approvals. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated commercial aviation jet fuel prices, reducing airline profitability and creating pressure on maintenance scheduling that can defer non-mandatory oil change intervals and reduce aviation lubricant consumption volume per fleet-hour in affected markets. These factors substantially limit aviation lubricant market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

IATA projects Asia-Pacific to account for the largest share of global air passenger traffic growth through 2032, with China, India, and Southeast Asian airline fleets expanding at above-5% annual rates that require proportional growth in aviation turbine oil, hydraulic fluid, and grease consumption at new aircraft entering service and growing MRO maintenance programmes. Shell's Singapore ester-synthesis plant opening in 2024 to 2025 and PPG's Singapore aviation chemical plant in 2025 confirm that aviation lubricant producers are positioning capacity specifically to serve the Asia-Pacific MRO market growth trajectory. ExxonMobil's Mobil Jet Oil approval across more than 11,000 gas turbine engines provides a revenue base that grows proportionally with every new CFM56, LEAP, and GE90/GE9X engine entering service that carries an ExxonMobil approved oil specification, creating automatic demand expansion as fleet grows without requiring new product qualifications at new aircraft types. IndiGo in India, Air Asia in Southeast Asia, and Lion Air Group in Indonesia collectively represent the fastest-growing turbine oil volume consumption centres in commercial aviation through 2030. Next-Generation Engine Oil Technology and Condition Monitoring Creating Premium Market Migration ExxonMobil's Mobil Jet Oil 387, approved under SAE AS5780 HPC and MIL-PRF-23699 HTS specifications, provides measurable improvements in thermal oxidative stability at CFM LEAP and GTF operating conditions compared to legacy Type II turbine oils, with ExxonMobil laboratory testing showing 40% advantage in high-temperature bulk oil stability versus competitive HTS oils and approximately 20% reduction in oil consumption versus previous generation products. NYCO's 2024 introduction of real-time condition monitoring capability for its TurboNYCOil product range represents the first commercial deployment of in-service oil analysis integrated with digital maintenance management systems at airline level, enabling extended oil analysis intervals and condition-based maintenance scheduling that replaces fixed-interval oil sampling and analysis. SAF-optimised turbine oil formulations under development at ExxonMobil, Shell, and TotalEnergies for next-generation engine operating conditions under sustainable aviation fuel combustion chemistry represent a premium product migration opportunity as SAF adoption increases at European airline fleets from 2025 to 2030 under CORSIA and EU SAF mandate requirements.

CFM LEAP and Pratt and Whitney GTF engines are designed to operate at significantly extended oil analysis intervals relative to their predecessor CFM56 and V2500 engines, with digital oil condition monitoring reducing mandatory oil sampling from every 100 flight hours to every 300 to 500 flight hours at qualified operators, reducing per-aircraft per-year turbine oil volume consumption even as engine sump oil volume remains constant. SAF combustion by-product chemistry in engine oil contamination differs sufficiently from conventional Jet A-1 combustion that engine OEM re-qualification of current turbine oil approvals under representative SAF operating conditions is required before airlines operating SAF blends above 50% can confirm continued oil approval validity, adding regulatory complexity to turbine oil product transitions at SAF-adopting fleets. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated Brent crude and jet fuel prices, reducing airline operating margins at Southeast Asian and Middle Eastern carriers and creating pressure on maintenance scheduling that may defer non-mandatory oil change intervals at cost-constrained operators. These factors substantially limit aviation lubricant market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Gas Turbine Oil, Piston Engine Oil, Hydraulic Fluid, Aviation Grease | Gas Turbine Oil |

| Base Oil Type | Synthetic Ester, Mineral Oil, PAO | Synthetic Ester |

| Aircraft Type | Commercial Aircraft, Military Aircraft, General Aviation, Helicopter | Commercial Aircraft |

| End Use | OEM, Airline, MRO | OEM |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Gas Turbine Oil segment is expected to account for a significantly large revenue share in the global aviation lubricant market during the forecast period.

This report evaluates product type across Gas Turbine Oil, Piston Engine Oil, Hydraulic Fluid, Aviation Grease for refinery products, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates base oil type across Synthetic Ester, Mineral Oil, PAO for refinery products, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates aircraft type across Commercial Aircraft, Military Aircraft, General Aviation, Helicopter for refinery products, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across OEM, Airline, MRO for refinery products, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for refinery products, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

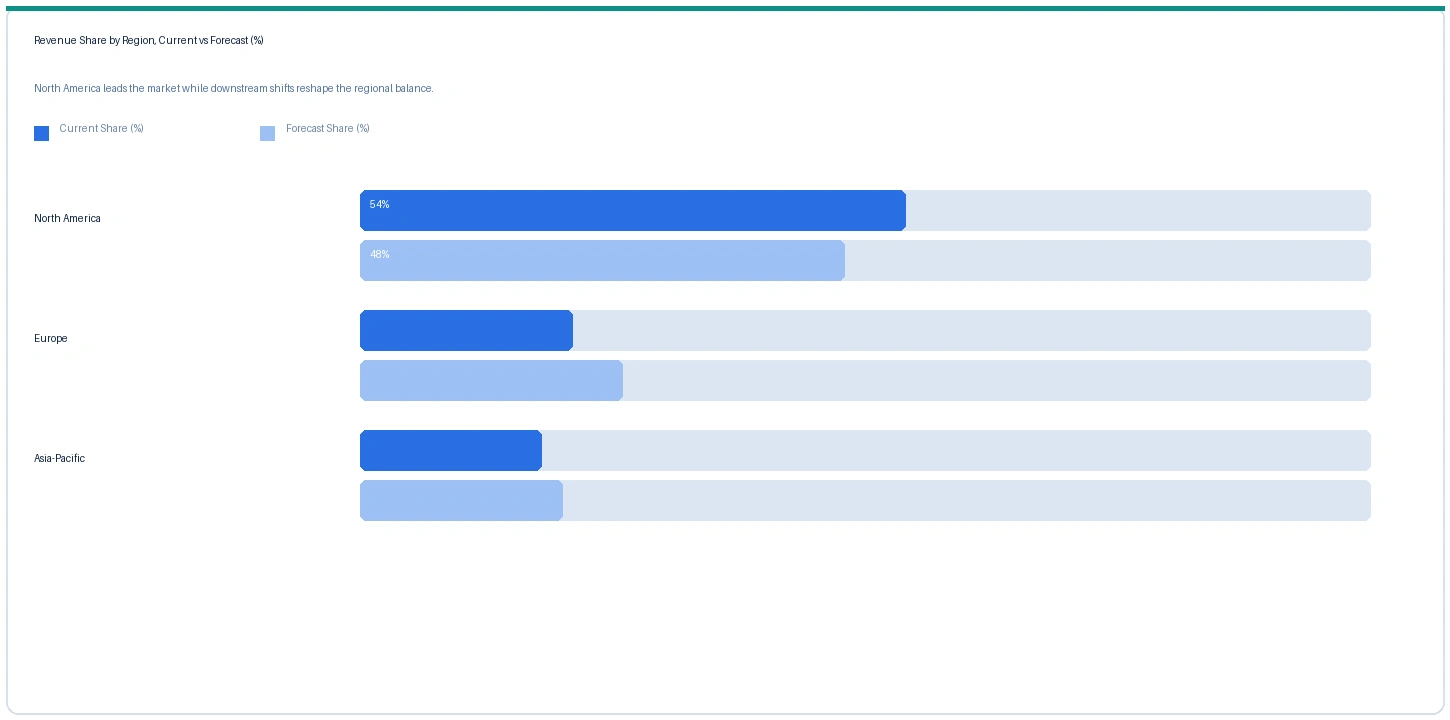

North America market accounted for largest revenue share over other regional markets in the global aviation lubricant market in 2025. Based on regional analysis, the aviation lubricant market in North America accounted for largest revenue share in 2025, at approximately 43% of global demand. North America's dominance reflects the world's largest commercial aircraft fleet concentration at US carriers, the largest military aviation lubricant market globally at the US Air Force, US Navy, and US Army Aviation, and ExxonMobil and Chevron Phillips' home market advantages in aviation lubricant supply to Boeing, Lockheed Martin, Boeing Distribution Services (Aviall), and US airline maintenance organisations. Mesa Airlines' April 2022 five-year ExxonMobil aviation lubricant procurement contract confirms the airline MRO contracting structure that drives durable revenue in the North American market.

The market in Europe is expected to register the second largest revenue share at approximately 29% of global demand. Shell AeroShell and NYCO hold dominant positions in European aviation turbine oil supply, with Shell's AeroShell network serving Lufthansa, Air France-KLM, Ryanair, and easyJet fleet lubricant programmes through its European distribution network. NYCO, headquartered in Tournai Belgium, supplies its TurboNYCOil 600 to CFM56 and LEAP narrow-body operators across Europe and confirmed its Airbus narrow-body fleet credentials at airblue Pakistan in 2021. TotalEnergies' 2023 partnership with a European airline for over 200 aircraft confirms the three-way competitive dynamic between Shell, NYCO, and TotalEnergies in the European commercial turbine oil market.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global aviation lubricant market during the forecast period. The market in Asia-Pacific is expected to register a CAGR of approximately 7.3% over the forecast period, the fastest of all regions, driven by IATA projecting Asia-Pacific to account for the largest share of global air passenger traffic growth through 2032. Shell's Singapore ester-synthesis plant in 2024 to 2025, PPG's Singapore aviation chemical plant in 2025, and the region's established aviation MRO hub at Singapore Changi confirm the infrastructure investment underpinning Asia-Pacific aviation lubricant market growth. China Eastern, China Southern, IndiGo, and Lion Air Group represent among the fastest-growing turbine oil volume consumption centres globally.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Gas Turbine Oil MIL-PRF-23699 Type II | North America | USD 38.4/litre | USD 35.8/litre | Rising | ExxonMobil Mobil Jet II ref |

| Gas Turbine Oil SAE AS5780 HPC (3rd gen) | North America | USD 52.6/litre | USD 48.2/litre | Rising | ExxonMobil Mobil Jet 387 ref |

| Phosphate Ester Hydraulic Fluid | Global | USD 28.4/litre | USD 26.4/litre | Rising | ExxonMobil HyJet IV-A+ ref |

| Aviation Grease (NLGI Grade 2) | Global | USD 22.6/kg | USD 20.8/kg | Rising | AeroShell Grease 64 ref |

| Gas Turbine Oil MIL-PRF-23699 | Europe | USD 42.8/litre | USD 39.6/litre | Rising | NYCO / AeroShell ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, ExxonMobil and Shell Aviation disclosed product pricing references, and airline MRO lubricant procurement monitoring. Aviation lubricant prices vary by product specification, engine OEM approval status, contract volume, and geographic delivery location.

MIL-PRF-23699 Type II gas turbine oil prices in North America rose approximately 7.3% in Q2 2026 against Q2 2025, driven by synthetic ester base oil production cost increases from dibasic acid and neopentyl glycol polyol feedstock elevation at petrochemical producers affected by naphtha cost increases from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026. Third-generation SAE AS5780 HPC gas turbine oil prices rose approximately 9.1%, reflecting higher formulation complexity and growing demand from latest-generation LEAP and GTF engine operators qualifying for third-generation approvals. European gas turbine oil prices carried a USD 4.4 per litre premium above North American equivalent in Q2 2026, reflecting Shell AeroShell and NYCO European production cost elevation from LNG energy cost increases at European ester synthesis operations.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the aviation lubricant market, the Hormuz disruption operates through two channels. The direct channel is synthetic ester base oil production cost elevation through dibasic acid and neopentyl glycol polyol feedstock cost increases from naphtha price elevation at European and Asian petrochemical producers, adding approximately USD 2.60 to USD 4.80 per litre to European gas turbine oil production cost in Q2 2026 above 2024 baseline and contributing to the 7.3% to 9.1% price increases documented in the price tracker. The indirect channel is commercial aviation jet fuel price elevation from Brent crude disruption reducing airline profitability at Southeast Asian, Middle Eastern, and South Asian carriers whose fuel cost represents above 25% of total operating cost, creating pressure on maintenance scheduling and discretionary oil change intervals that reduces aviation lubricant consumption volume per fleet-hour in affected markets through 2026 and into 2027.

Company Insights

The two key dominant companies in the aviation lubricant market are ExxonMobil Corporation and Shell plc, recognised for their comprehensive engine OEM approval portfolios spanning commercial, military, and general aviation gas turbine engines globally, their established long-term supply relationships with major airline and MRO operators, and their technical leadership in next-generation turbine oil formulation for LEAP, GTF, and SAF-compatible operating conditions.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 2.04 Billion |

| Market Size 2032 | USD 3.22 Billion |

| CAGR | 6.7% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product Type, By Base Oil Type, By Aircraft Type, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, UK, France, Belgium, Germany, Netherlands, Japan, China, Singapore, India, Brazil, UAE, Saudi Arabia |

| Companies Profiled | ExxonMobil Corporation, Shell plc (AeroShell), NYCO, TotalEnergies SE, BP Castrol, Chevron, Phillips 66, Eastman Chemical, Nye Lubricants, LANXESS, FUCHS, Petro-Canada Lubricants |

| Key Data Sources | ExxonMobil Aviation Mobil Jet Oil 11,000+ engine approvals disclosure, ExxonMobil Mobil Jet Oil 387 SAE AS5780 HPC and MIL-PRF-23699 HTS approval, Shell AeroShell Turbine Oil 560 Delta / USAF / SpaceX qualification, Shell Singapore ester-synthesis plant 2024-2025, Mesa Airlines ExxonMobil five-year contract April 2022, NYCO TurboNYCOil 600 airblue selection November 2021, NYCO condition monitoring launch 2024, TotalEnergies European airline partnership 2023, Airbus 2024 delivery record 766 aircraft, IATA fleet data 2024, IMF March 2026 Strait of Hormuz statement, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 254 |

| Published | Q2 2026 |

| SKU | NXC-AV-003 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 15 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included aviation turbine oil commercial and product management leads at US and European producers, synthetic ester base oil technology specialists, and engine OEM lubricant qualification programme contacts. Demand-side contacts included commercial airline lubricant and MRO materials sourcing managers at European, North American, and Asian carrier maintenance organisations, military aviation lubricant procurement officers, and MRO distributor lubricant supply chain managers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include ExxonMobil Aviation Mobil Jet Oil product approval disclosures, ExxonMobil Mobil Jet Oil 387 product communications, Shell AeroShell Turbine Oil 560 product qualification disclosures and Singapore plant communications, Mesa Airlines ExxonMobil contract announcement April 2022, NYCO TurboNYCOil 600 airblue selection announcement November 2021, NYCO condition monitoring product launch 2024, TotalEnergies European airline partnership announcement 2023, Airbus 2024 aircraft delivery record, IATA commercial aircraft fleet data 2024, EU Regulation 2023/2405 ReFuelEU Aviation SAF blend mandate, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.