Market Data

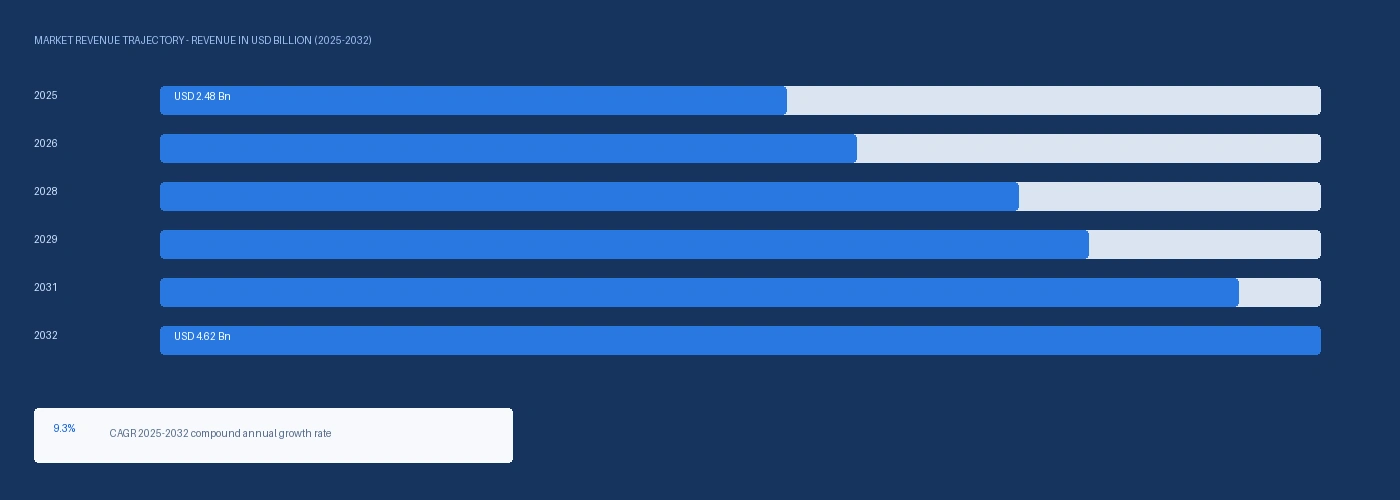

The global aviation carbon fiber market size was USD 2.48 Billion in 2025 and is expected to register a revenue CAGR of 9.3% during the forecast period. Market revenue growth is supported by commercial aviation consuming approximately 28,000 metric tonnes of carbon fiber in 2024 led by the Boeing 787 Dreamliner and Airbus A350 programmes both incorporating over 50% composites by weight per industry data, Hexcel Corporation reporting full-year 2024 commercial aerospace sales of USD 1,194.2 million at 11.8% growth per its fourth quarter and full-year 2024 results announcement, and Toray Industries expanding PAN-based carbon fiber capacity in Japan in July 2025 to serve aerospace and automotive clients, including aviation carbon fiber supply obligations under its long-term supply agreements with Boeing and Airbus. Hexcel Corporation generated total 2024 net sales of USD 1.903 billion, with commercial aerospace representing 63% of revenue at USD 1.194 billion, space and defense at 30%, and industrial at 7%, with widebody aircraft programmes including Boeing 787 and Airbus A350 leading commercial aerospace growth. Airbus delivered a record 766 aircraft in 2024, including A350 widebody deliveries contributing above-average carbon fiber intensity at 53% composites by weight per Airbus A350 technical documentation. Hexcel signed a supply agreement with Boeing for next-generation aircraft programs integrating advanced composites in June 2025, confirming continuation of its position as a primary carbon fiber and prepreg supplier to Boeing commercial aircraft programmes through the next single-aisle aircraft development cycle. For instance, in June 2025, Hexcel Corporation, United States, signed a supply agreement with Boeing Company for next-generation aircraft programs integrating advanced composite carbon fiber and prepreg materials, reinforcing Hexcel's position as the dominant composite material supplier for the most commercially significant aircraft programmes in its order book. These are some of the key factors driving revenue growth of the market.

Toray Industries leads global aviation carbon fiber production with approximately 7% market share in 2024 per competitive structure data, operating its T-series intermediate-modulus and M-series high-modulus carbon fiber production in Japan, France, and the United States under long-term supply agreements with Boeing and Airbus. Toray's T800 and T1000 intermediate-modulus carbon fiber grades are specified in primary structural applications at Boeing 787 fuselage barrel segments and wing panels, with Toray's Boeing supply agreement covering multi-year volume allocations that represent the largest single supply commitment in the aviation carbon fiber market. Hexcel Corporation is Toray's primary competitor in the vertically integrated prepreg segment, with Hexcel producing carbon fiber from its own PAN precursor at Decatur Alabama and converting to unidirectional and woven prepreg at multiple facilities, supplying over 80% of Airbus commercial aircraft carbon fiber requirements per published data. Mitsubishi Chemical Group, Teijin Carbon, and SGL Carbon SE are the secondary tier of aviation carbon fiber producers, each with material supply positions at specific aircraft programmes or sub-system applications.

However, Boeing's supply chain challenges in 2024 delayed planned production rate increases at the 737 MAX and 787 programmes, creating carbon fiber demand below the production rate trajectories that Hexcel, Toray, and Solvay had planned capacity allocation for, with Hexcel citing supply chain challenges at major customers as a constraint on 2024 revenue growth despite its 11.8% commercial aerospace growth outperforming the rate of aircraft deliveries. Next-generation single-aisle aircraft programme carbon fiber content is not guaranteed, with Hexcel's VP of Product Management warning at the Carbon Fiber 2024 Conference in Charleston that composite content on the next single-aisle platform is not assured and will depend on cost, maintenance, and sustainability factors, creating a programme-level uncertainty for carbon fiber producers whose growth models assume composite intensification at every new aircraft programme. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated commercial aviation fuel costs, reducing airline operating margins and creating pressure on Boeing and Airbus delivery schedules from airline financial planning adjustments that flow into OEM production rate decisions and downstream carbon fiber demand timing. These factors substantially limit aviation carbon fiber market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Boeing 787 and Airbus A350 widebody programmes each incorporate over 50% composites by weight and consume approximately 25 to 35 metric tonnes of carbon fiber per aircraft, making each delivered widebody the largest single-unit carbon fiber consumption event in commercial manufacturing. Hexcel's 2024 full-year commercial aerospace growth of 11.8% was led by widebody programmes per its earnings commentary, with the 787 and A350 contributing the majority of commercial aerospace carbon fiber growth even as Boeing 737 MAX rates were constrained. Airbus 766 aircraft deliveries in 2024 including A350 widebodies, and Boeing's targeting approximately 10% commercial aerospace revenue growth for 2025 per Hexcel's 2025 guidance, confirms continued positive widebody composite material demand trajectory into 2026. Hexcel's approximately 5,900 employees across 20 manufacturing plants generating USD 1.9 billion in 2024 sales confirms its position as the dominant integrated carbon fiber-to-composite supply chain producer serving commercial aviation. Advanced Air Mobility and UAV Programmes Adding New Carbon Fiber Demand Categories Electric vertical take-off and landing aircraft programmes at Joby Aviation, Archer Aviation, and Wisk Aero require high-strength-to-weight-ratio carbon fiber structures for airframe efficiency at power budgets that are critically sensitive to structural mass, with each kilogram of airframe mass reduction enabling proportional reduction in battery size and extension of practical range. Hexcel's positioning in October 2024 at Carbon Fiber 2024 Conference for advanced air mobility electric aircraft markets with high-rate composite manufacturing confirms its strategy of capturing the emerging AAM carbon fiber demand category as a parallel market to traditional commercial aircraft composite requirements. Military UAV programmes including the US Air Force Collaborative Combat Aircraft and NATO equivalent programmes require advanced carbon fiber composite primary structures for stealth signature management and structural mass optimisation, with Hexcel's space and defense segment at 30% of 2024 revenue confirming the defence and UAV carbon fiber demand contribution.

Hexcel's VP warning at Carbon Fiber 2024 Conference that composite content on the next single-aisle aircraft is not guaranteed reflects the fundamental uncertainty facing carbon fiber producers whose 2030+ growth projections depend on continued composite intensification across all new aircraft programmes. Cost, maintenance repairability, and sustainability certification of thermoplastic composites versus thermoset prepreg systems are the three factors that could reduce carbon fiber content on the next-generation single-aisle relative to the A350 or 787 composite percentage benchmarks. Boeing's supply chain challenges delaying 737 MAX and 787 production rate increases in 2024 created carbon fiber demand timing uncertainty below Hexcel's planned allocation capacity, contributing to Hexcel's decision to repurchase USD 252 million of stock in the first three quarters of 2024 as capital allocation reflecting near-term demand moderation. The US-Iran conflict and Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated commercial aviation fuel costs, reducing airline operating margins and potentially deferring new aircraft order conversions or delivery acceptance scheduling that would affect carbon fiber demand timing. These factors substantially limit aviation carbon fiber market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Fiber Type | PAN-Based Carbon Fiber, Pitch-Based Carbon Fiber, Rayon-Based Carbon Fiber | PAN-Based Carbon Fiber |

| Form | Prepreg, Dry Fiber, Chopped Fiber, Carbon Fiber Tape | Prepreg |

| Application | Fuselage, Wing Structures, Nacelle and Engine Components, Interior, Landing Gear Doors | Fuselage |

| Aircraft Type | Commercial Narrowbody, Commercial Widebody, Business Aviation, Military Aircraft, UAV | Commercial Narrowbody |

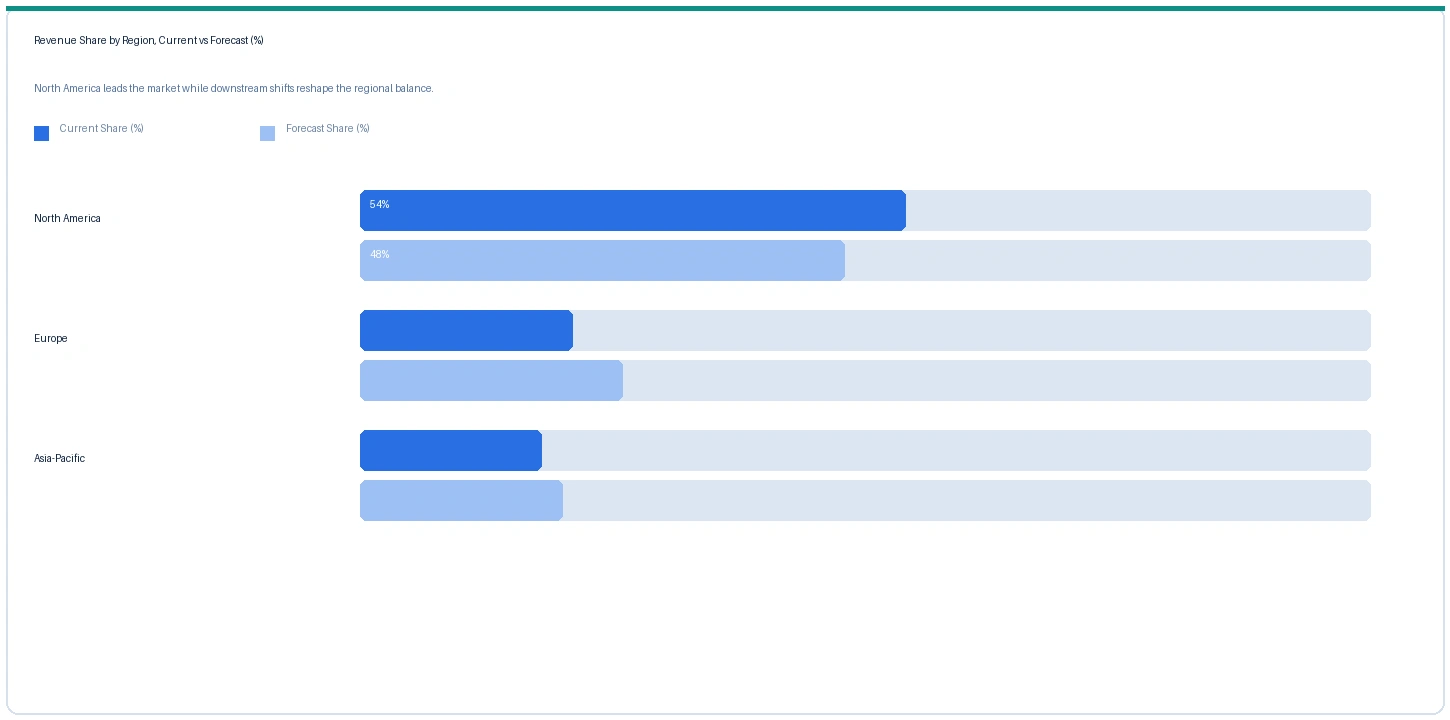

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

PAN-Based Carbon Fiber segment is expected to account for a significantly large revenue share in the global aviation carbon fiber market during the forecast period.

This report evaluates fiber type across PAN-Based Carbon Fiber, Pitch-Based Carbon Fiber, Rayon-Based Carbon Fiber for carbon fibre & composites, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates form across Prepreg, Dry Fiber, Chopped Fiber, Carbon Fiber Tape for carbon fibre & composites, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Fuselage, Wing Structures, Nacelle and Engine Components, Interior, Landing Gear Doors for carbon fibre & composites, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates aircraft type across Commercial Narrowbody, Commercial Widebody, Business Aviation, Military Aircraft, UAV for carbon fibre & composites, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for carbon fibre & composites, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

North America market accounted for largest revenue share over other regional markets in the global aviation carbon fiber market in 2025. Based on regional analysis, the aviation carbon fiber market in North America accounted for largest revenue share in 2025. Boeing's Everett Washington 787 final assembly and North Charleston South Carolina 787 and 737 MAX production consume the largest single-site concentration of aviation carbon fiber prepreg globally. Hexcel operates US PAN fiber production at Decatur Alabama and prepreg facilities at Burlington Vermont, Lancaster California, and Salt Lake City Utah. Lockheed Martin F-35 production at Fort Worth Texas and Northrop Grumman B-21 Raider composite structures at Palmdale California represent major military aviation carbon fiber consumption. US space and defence at 30% of Hexcel's 2024 revenue confirms the weight of North American military composite demand.

Europe market accounted for second largest revenue share in the global aviation carbon fiber market in 2025. The market in Europe is expected to register the second largest revenue share. Airbus final assembly at Toulouse and Hamburg consumes carbon fiber prepreg from Hexcel's Dagneux France and Thame UK facilities, with Toray's European sales office covering A350 PAN fiber requirements. Safran's CFM LEAP fan blade composite production at its French facilities is supplied by Hexcel as the primary carbon fiber and prepreg source for the world's highest-volume commercial aircraft engine fan blade programme. SGL Carbon SE at Meitingen Germany and Muenchsmunster Germany produces PAN-based carbon fiber for Airbus A320neo stabiliser and nacelle structural applications.

Asia-Pacific market is expected to register rapid revenue growth in the global aviation carbon fiber market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate. Toray's primary PAN fiber production at Ehime Japan and its capacity expansion announced July 2025 are located in the region, with the company supplying Boeing and Airbus programmes through long-term agreements. COMAC C919 and C929 aircraft programmes in China are generating domestic Chinese aviation carbon fiber demand at AVIC Composite Corporation and Zhongfu Shenying Carbon Fiber Co., with Zhongfu Shenying opening a new 12,000-tonne annual capacity production facility in April 2025. Teijin Carbon Japan supplies aviation carbon fiber through its Renegade Materials aerospace prepreg operations.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Aerospace Epoxy Prepreg (UD, carbon) | North America | USD 96/kg | USD 88/kg | Rising | Hexcel ref |

| Aerospace Epoxy Prepreg (UD, carbon) | Europe | USD 102/kg | USD 94/kg | Rising | Hexcel / Solvay ref |

| Intermediate-Modulus PAN Fiber (T800) | Global | USD 38/kg | USD 34/kg | Rising | Toray ref |

| High-Modulus PAN Fiber (M55J, space) | Global | USD 280/kg | USD 262/kg | Rising | Pitch/PAN specialty ref |

| Recycled CF (rCF, aviation spec) | Global | USD 22/kg | USD 19/kg | Rising | Nandina REM ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, Hexcel investor presentations, and aerospace composite material procurement monitoring. Aviation carbon fiber pricing reflects aerospace qualification and performance specification premiums substantially above industrial grade carbon fiber pricing.

Aerospace epoxy prepreg prices in North America rose approximately 9.1% in Q2 2026 against Q2 2025, driven by PAN precursor acrylonitrile cost increases from propylene feedstock elevation at Asian crackers affected by the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, combined with growing commercial aerospace demand from Hexcel's guided approximately 10% commercial aerospace revenue growth in 2025 outpacing short-term supply additions. Intermediate-modulus T800 grade PAN fiber rose approximately 11.8% from USD 34 per kilogram in Q2 2025 to USD 38 per kilogram in Q2 2026, reflecting both PAN precursor cost increase and tighter supply allocation as Toray's expanded Japan capacity completed qualification tests but had not yet reached full commercial production at its expanded facility. Recycled carbon fiber from end-of-life aircraft and manufacturing scrap rose approximately 15.8%, confirming growing aviation industry acceptance of rCF in secondary structure and interior applications following Nandina REM's February 2024 launch of high-quality carbon fiber material reclaimed from end-of-life aircraft.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the aviation carbon fiber market, the Hormuz disruption operates through PAN precursor acrylonitrile feedstock cost elevation and demand-side effects on OEM production planning. Acrylonitrile is produced from propylene via the Sohio process, with propylene sourced from naphtha at Asian crackers affected by Hormuz-disrupted GCC naphtha supply, elevating acrylonitrile spot prices by approximately 8% to 12% above 2025 baseline in Q2 2026 and contributing to PAN precursor cost increases at Toray Japan, Hexcel Decatur Alabama, and Asian PAN producers. The demand-side effect operates through commercial aviation fuel cost elevation reducing airline operating margins, creating airline aircraft delivery timing adjustments that produce short-term demand variability for Hexcel and Toray production schedule management while the underlying long-term demand trajectory remains intact on long-term supply agreement commitments.

Company Insights

The two key dominant companies in the aviation carbon fiber market are Hexcel Corporation and Toray Industries Inc., recognised for their vertically integrated carbon fiber-to-composite supply chain positions, their multi-decade OEM qualification at Boeing and Airbus primary structural programmes, and their technical leadership in PAN-based intermediate-modulus fiber and epoxy prepreg systems for commercial and military aviation applications.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 2.48 Billion |

| Market Size 2032 | USD 4.62 Billion |

| CAGR | 9.3% |

| Units | Revenue in USD Billion |

| Segments Covered | By Fiber Type, By Form, By Application, By Aircraft Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, France, UK, Germany, Japan, China, South Korea, Brazil |

| Companies Profiled | Hexcel Corporation, Toray Industries, Teijin Carbon, Mitsubishi Chemical, Solvay, SGL Carbon, Zhongfu Shenying, Zoltek, DuPont, Hyosung, Park Aerospace, Nandina REM |

| Key Data Sources | Hexcel Corporation full-year 2024 results and SEC 10-K (commercial aerospace sales USD 1,194.2 million), Hexcel 2024 Carbon Fiber Conference presentation, Hexcel Boeing supply agreement June 2025, Toray Industries capacity expansion announcement July 2025, Zhongfu Shenying facility opening April 2025, Nandina REM recycled aviation carbon fiber launch February 2024, Arkema-Hexcel thermoplastic out-of-autoclave milestone March 2024, Airbus 2024 delivery record 766 aircraft, IATA commercial fleet data, IMF March 2026 Strait of Hormuz statement, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 264 |

| Published | Q2 2026 |

| SKU | NXC-AV-002 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 16 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included aviation carbon fiber commercial and product management leads at US, European, and Japanese producers, prepreg qualification programme engineers, and advanced air mobility composite supply chain development leads. Demand-side contacts included Boeing and Airbus structural material procurement managers, LEAP engine composite supply chain purchasing leads at Safran, and MRO composite repair procurement managers at major airline maintenance organisations. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Hexcel Corporation full-year 2024 earnings announcement and SEC 10-K, Hexcel Carbon Fiber 2024 Conference presentation October 2024, Hexcel and Boeing supply agreement announcement June 2025, Toray Industries PAN fiber capacity expansion announcement July 2025, Zhongfu Shenying new facility opening announcement April 2025, Nandina REM recycled aviation carbon fiber launch announcement February 2024, Arkema and Hexcel thermoplastic out-of-autoclave structure milestone March 2024, Airbus 2024 aircraft delivery announcement, IATA commercial aircraft fleet statistics 2024, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.