Market Data

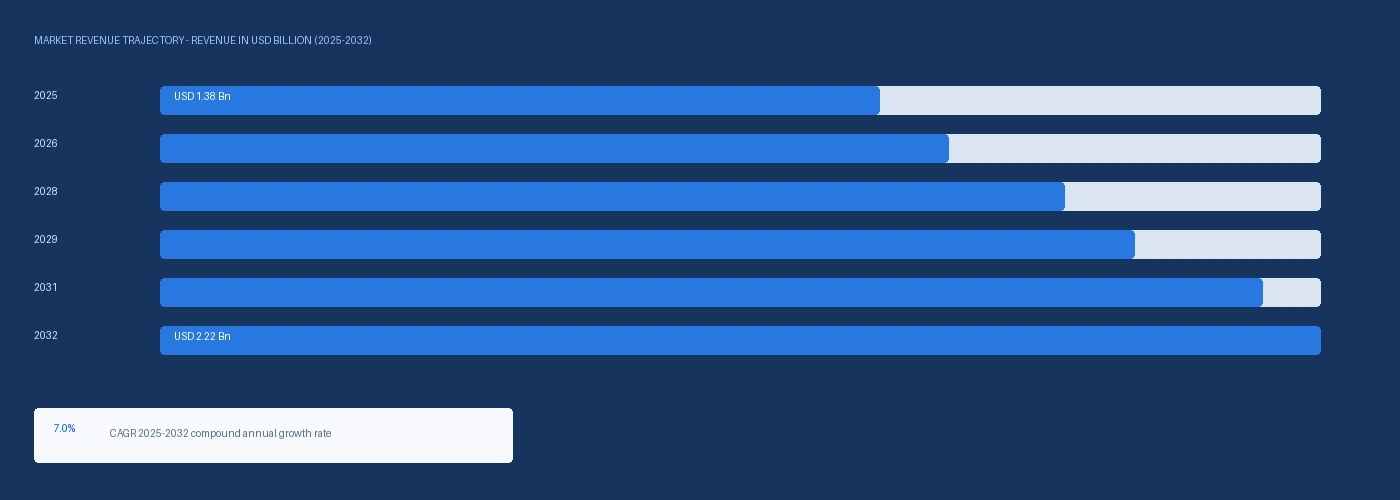

The global aviation adhesives and sealants market size was USD 1.38 Billion in 2025 and is expected to register a revenue CAGR of 7.0% during the forecast period. Market revenue growth is supported by commercial aircraft fleet expansion with IATA confirming approximately 26,000 commercial aircraft in active service globally in 2024 each requiring polysulfide fuel tank sealant replacement at scheduled maintenance intervals of 6 to 12 years at OEM-specified intervals, PPG Industries investing USD 9.8 million in 2024 expanding its Texas production capacity for aerospace adhesives and opening a new Singapore ester-synthesis plant in 2024 to 2025 serving Asia-Pacific aviation MRO demand, and Airbus delivering a record 766 commercial aircraft in 2024 per Airbus investor communications with each aircraft requiring adhesive and sealant systems at structural bonding, fuel tank sealing, cabin interior, and window bonding positions. Boeing and Airbus commercial aircraft programmes incorporating 50% or more composites by weight per IATA technical data on Boeing 787 and Airbus A350 platforms require composite structural adhesive in primary load-bearing applications including wing skin-to-spar bonding, fuselage frame-to-skin attachment, and nacelle component assembly where metal-to-metal fastening alone is structurally insufficient. H.B. Fuller secured a multi-year contract to supply specialised sealants for the Airbus A320neo programme in Q2 2024, supporting both OEM production and MRO applications and confirming the long-term contracted revenue structure of aviation sealant supply to major commercial aircraft programmes. For instance, in February 2024, PPG Industries, United States, launched PR-2940 and PR-2936 aerospace adhesive products, with PR-2936 combining shim and sealant functionality for attaching aircraft outer skins to internal structures and enabling weight reduction, improved bonding performance, and enhanced manufacturing efficiency for OEM and MRO applications at commercial and military aircraft programmes. These are some of the key factors driving revenue growth of the market.

PPG Industries' AeroShell brand generated approximately USD 380 million in aviation specialty chemicals revenue in 2024 per disclosed company data, covering aviation sealants, lubricants, and coatings, with aerospace sealants representing a significant portion of this revenue through its PR-1422, PR-1750, and PR-2940 polysulfide and epoxy sealant families qualified at Boeing, Airbus, Lockheed Martin, and Northrop Grumman programmes. Henkel's LOCTITE EA 9396 and LOCTITE EA 9480 aerospace-grade structural adhesives are qualified for primary load-bearing composite bonding at Boeing 787, Airbus A350, and military aircraft platforms, with Henkel expanding its aerospace adhesive portfolio in 2024 through strategic acquisitions enhancing high-temperature-resistant epoxy formulations per company communications. Huntsman Corporation supplies Araldite 2011 and 2021 epoxy adhesive systems for composite wing structure and panel bonding at major aircraft OEMs, with the company targeting weight reduction and structural integrity optimisation in OEM collaboration programmes. Solvay Group provides Cytec 5275-1 and 9235 aerospace-grade structural film adhesives for primary composite load-bearing applications at Boeing and Airbus wing and fuselage programmes. North America accounted for approximately 47% of total aviation adhesive and sealant market revenue in 2024, reflecting the concentration of Boeing commercial aircraft production in Everett Washington and North Charleston South Carolina, Lockheed Martin and Northrop Grumman defence programmes, and the largest MRO services network globally.

However, the aircraft maintenance cycle that drives polysulfide fuel tank sealant replacement demand is linked to airline financial performance and fleet utilisation rates, with airlines deferring non-mandatory MRO work during revenue downturns that can delay resealing programmes by 12 to 24 months beyond scheduled intervals without immediate airworthiness impact, creating demand cyclicality linked to air traffic economics that is not present in ground vehicle adhesive markets. Chromate-free aerospace sealant reformulation requirements, with REACH and US EPA restrictions on hexavalent chromium corrosion inhibitor content in aerospace sealants used in contact with aluminium alloy structures, require reformulation investment at PPG, Henkel, and regional sealant producers that adds regulatory compliance cost to new aircraft programme qualification activities. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated commercial aviation fuel costs through crude oil disruption, reducing airline operating margins and creating pressure on discretionary MRO scheduling that can defer fuel tank resealing and cabin interior adhesive replacement programmes in price-sensitive airline markets. These factors substantially limit aviation adhesives and sealants market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

IATA's commercial aircraft fleet of approximately 26,000 units in 2024 generates recurring MRO adhesive and sealant demand through regulatory maintenance intervals that require fuel tank polysulfide sealant replacement every 6 to 12 years depending on aircraft type and operator cycle count, window bonding silicone sealant replacement at cabin refurbishment every 8 to 12 years, and structural adhesive inspection and spot repair at scheduled heavy maintenance C-check and D-check intervals every 6 to 12 years. Airbus delivering 766 aircraft in 2024 and Boeing targeting production rate increases in 2025 after supply chain challenges per Hexcel Corporation's 2024 full-year results commentary on commercial aerospace growth creates OEM adhesive demand on top of the MRO base. The aviation MRO market is projected to exceed USD 110 billion annually by 2030 per aviation industry forecasts, with adhesives and sealants representing approximately 1.3% to 1.8% of total MRO spend across commercial, defence, and general aviation segments. Composite-Intensive Next-Generation Aircraft Programmes Requiring Structural Film Adhesives Boeing 787 Dreamliner and Airbus A350 XWB platforms incorporate over 50% composites by weight, with carbon fibre reinforced polymer primary structures including fuselage barrels, wing skins, and tail surfaces requiring structural film adhesives at bonded joint interfaces where fastener-only attachment is structurally insufficient. Hexcel Corporation's 2024 full-year results confirmed commercial aerospace sales of USD 1,194.2 million, representing 11.8% growth, with the Boeing 787 and Airbus A350 widebody programmes leading growth. Each composite-intensive widebody aircraft requires approximately 200 to 400 kilograms of structural adhesive in bonded primary structure applications at substantially higher per-kilogram pricing of USD 80 to USD 220 per kilogram compared to automotive structural adhesive at USD 5,000 to USD 7,000 per metric tonne equivalent. PPG's 3D-printed sealant gaskets and pre-formed sealant components showcased at MRO Americas 2024 demonstrate additive manufacturing approaches to reducing sealant application labour requirements and material waste in aircraft manufacturing and maintenance.

Airline operating margin sensitivity to jet fuel prices creates cyclical risk in discretionary MRO scheduling, with fuel tank resealing programmes deferred beyond regulatory intervals by airlines managing cash flow in high-fuel-cost operating environments. The US-Iran conflict and Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated Brent crude oil prices and derived jet fuel costs, reducing airline operating margins in Q2 2026 and creating pressure on MRO budget allocation that can delay non-mandatory resealing and cabin interior adhesive work. REACH restriction on hexavalent chromium corrosion inhibitors in aerospace sealants effective in Europe from 2024 requires reformulation at PPG, Henkel, and regional aerospace sealant producers at qualification cost of USD 2 to USD 5 million per aircraft programme per sealant product, creating a compliance cost cycle that precedes commercial introduction of chromate-free replacements. These factors substantially limit aviation adhesives and sealants market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Resin Type | Epoxy, Polysulfide, Polyurethane, Silicone, Acrylic | Epoxy |

| Application | Structural Bonding, Fuel Tank Sealing, Cabin Interior, Engine and Nacelle, Window Bonding | Structural Bonding |

| Aircraft Type | Commercial Narrowbody, Commercial Widebody, Business Aviation, Military Aircraft, Helicopter | Commercial Narrowbody |

| End Use | OEM, MRO | OEM |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Epoxy Resin segment is expected to account for a significantly large revenue share in the global aviation adhesives and sealants market during the forecast period.

This report evaluates resin type across Epoxy, Polysulfide, Polyurethane, Silicone, Acrylic for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Structural Bonding, Fuel Tank Sealing, Cabin Interior, Engine and Nacelle, Window Bonding for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates aircraft type across Commercial Narrowbody, Commercial Widebody, Business Aviation, Military Aircraft, Helicopter for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across OEM, MRO for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

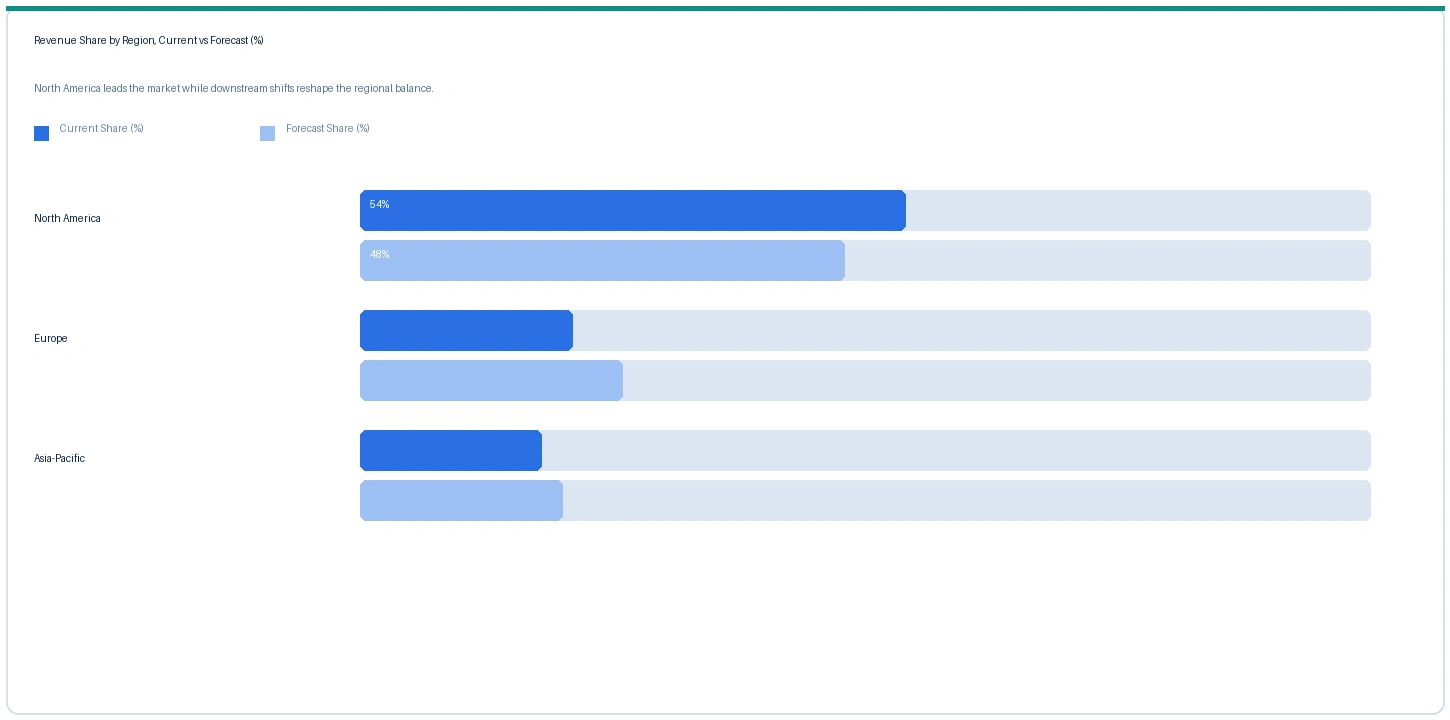

North America market accounted for largest revenue share over other regional markets in the global aviation adhesives and sealants market in 2025. Based on regional analysis, the aviation adhesives and sealants market in North America accounted for largest revenue share in 2025, at approximately 47% of global revenue. North America's dominance reflects Boeing's commercial aircraft production at Everett Washington and North Charleston South Carolina consuming structural film adhesive and fuselage sealants, Lockheed Martin F-35 and other defence aircraft programmes consuming structural adhesives and military specification sealants, and the largest commercial aviation MRO network globally concentrated at US airline hub maintenance bases. PPG's Texas adhesive production expansion in 2024 and its established qualification at Boeing programmes reinforces North American supply chain concentration for aviation sealants.

Europe market accounted for second largest revenue share in the global aviation adhesives and sealants market in 2025. The market in Europe is expected to register the second largest revenue share. Airbus deliveries of 766 commercial aircraft in 2024 from Toulouse France and Hamburg Germany final assembly lines generate OEM adhesive and sealant demand from Henkel, Solvay, and Huntsman European aviation adhesive operations. Lufthansa Technik, Air France Industries KLM Engineering and Maintenance, and Iberia MRO represent major European MRO adhesive and sealant consumption centres for commercial fleet maintenance.

Asia-Pacific market is expected to register rapid revenue growth in the global aviation adhesives and sealants market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate, driven by IATA projecting Asia-Pacific to account for the largest share of global air passenger growth through 2032 at above-5% annual passenger traffic growth rates, generating fleet expansion at Chinese, Indian, Japanese, Korean, and Southeast Asian airlines that requires new aircraft OEM adhesive content and growing MRO demand as Asian fleet ages into first maintenance cycle. PPG's Singapore ester-synthesis plant opening in 2024 to 2025 directly targets the growing Asia-Pacific aviation MRO sealant market.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Polysulfide Fuel Tank Sealant (2-part) | North America | USD 48,200/MT | USD 44,800/MT | Rising | PPG PR-1750 ref |

| Epoxy Structural Film Adhesive | North America | USD 124,000/MT | USD 116,000/MT | Rising | Hexcel / Solvay ref |

| Silicone Window and Cabin Sealant | Europe | USD 28,400/MT | USD 26,200/MT | Rising | Henkel / Dow ref |

| Epoxy Paste Adhesive (aerospace) | Asia-Pacific | USD 38,600/MT | USD 35,800/MT | Rising | PPG PR-2940 ref |

| Polyurethane Cabin Interior Adhesive | Global | USD 22,800/MT | USD 21,200/MT | Rising | H.B. Fuller ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, aviation adhesive and sealant producer commercial disclosures, and aviation MRO procurement monitoring. Aviation adhesive and sealant prices vary substantially by product specification, aircraft programme qualification status, and supply agreement structure.

Polysulfide fuel tank sealant prices in North America rose approximately 7.6% in Q2 2026 against Q2 2025, driven by thiokol polysulfide polymer raw material cost increases from elevated propylene and chlorine feedstock pricing, combined with chromate-free reformulation capital cost amortisation beginning to flow through to list pricing at PPG and Henkel 2025 to 2026 contract renewal cycles. Epoxy structural film adhesive prices rose approximately 6.9% on bisphenol A and dicyandiamide hardener feedstock cost increases. Silicone window and cabin sealant prices in Europe rose approximately 8.4% on elevated silicon metal and methanol costs at European silicone polymer producers.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the aviation adhesives and sealants market, the Hormuz disruption operates through two channels. The direct channel is jet fuel cost elevation from Brent crude oil price increases driven by the Hormuz disruption, reducing airline operating margins and creating airline MRO budget pressure that can defer non-mandatory fuel tank resealing and cabin interior adhesive replacement programmes at cost-constrained operators in Southeast Asia, Middle East, and South Asia whose fuel costs represent a higher proportion of total operating cost than at European or North American carriers with longer-term fuel hedges in place. The indirect channel is polysulfide polymer feedstock cost elevation through propylene and chlorine petrochemical pricing increases from naphtha cost elevation at Asian crackers exposed to Hormuz-disrupted GCC naphtha supply, adding approximately USD 1,800 to USD 3,200 per metric tonne to polysulfide fuel tank sealant raw material cost at PPG and Henkel in Q2 2026.

Company Insights

The two key dominant companies in the aviation adhesives and sealants market are PPG Industries Inc. and Henkel AG, recognised for their comprehensive product portfolios covering fuel tank polysulfide sealing, structural composite bonding, cabin interior adhesives, and engine nacelle sealants, their established multi-decade qualification at Boeing and Airbus commercial aircraft programmes, and their technical leadership in chromate-free reformulation and automated sealant application system development.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 1.38 Billion |

| Market Size 2032 | USD 2.22 Billion |

| CAGR | 7.0% |

| Units | Revenue in USD Billion |

| Segments Covered | By Resin Type, By Application, By Aircraft Type, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Netherlands, Japan, China, Singapore, India, Brazil, UAE |

| Companies Profiled | PPG Industries, Henkel AG, H.B. Fuller, Huntsman Corporation, Solvay S.A., 3M, DuPont, Hernon Manufacturing, Bostik, Sika AG, Royal Adhesives and Sealants, Chemique Adhesives |

| Key Data Sources | PPG Industries PR-2940/PR-2936 adhesive launch February 2024, PPG USD 9.8M Texas capacity expansion 2024, PPG Singapore plant 2025, H.B. Fuller Airbus A320neo sealant contract Q2 2024, Hexcel Corporation 2024 full-year results commercial aerospace sales, IATA commercial aircraft fleet data 2024, Airbus 2024 delivery record of 766 aircraft, Boeing production rate recovery guidance 2025, Henkel AG Annual Report 2024, IMF March 2026 Strait of Hormuz statement, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 256 |

| Published | Q2 2026 |

| SKU | NXC-AV-001 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 16 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included aviation adhesive and sealant commercial leads at US and European producers, qualification programme engineers at aircraft OEM structural materials teams, and MRO sealant procurement managers at airline engineering organisations. Demand-side contacts included Boeing and Airbus supplier qualification and approval organisation contacts, commercial MRO sealant sourcing managers at major European and Asian airline maintenance operations, and military aircraft structural adhesive procurement officers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include PPG Industries PR-2940 and PR-2936 product launch announcement February 2024, PPG Texas capacity expansion and Singapore plant communications, H.B. Fuller Airbus A320neo sealant contract announcement Q2 2024, Hexcel Corporation 2024 full-year results and SEC 10-K, IATA commercial aircraft fleet data and air traffic statistics 2024, Airbus 2024 delivery record announcement, Henkel AG Annual Report 2024, REACH hexavalent chromium corrosion inhibitor restriction regulation, Boeing production rate guidance communications, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.