Market Data

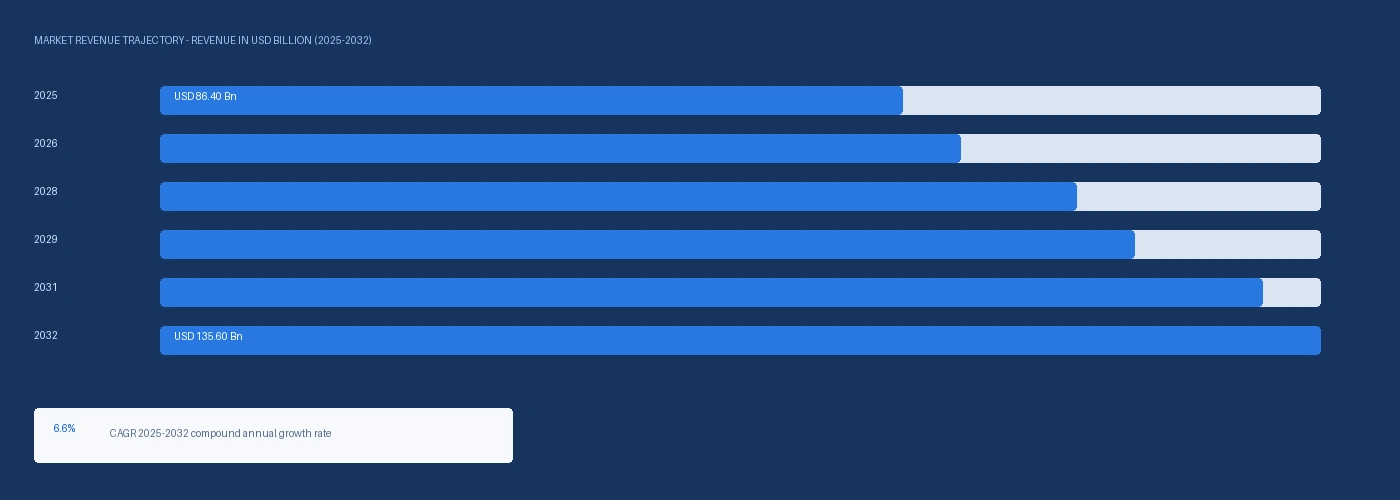

The global automotive steel market size was USD 86.40 Billion in 2025 and is expected to register a revenue CAGR of 6.6% during the forecast period. Market revenue growth is supported by advanced high-strength steel penetration in automotive body structures exceeding 28% of total automotive steel usage in 2024 per industry data versus approximately 18% in 2018, World Steel Association confirming approximately 1,892 million metric tonnes of global crude steel production in 2023 with automotive accounting for approximately 210 million metric tonnes, and India's passenger vehicle production growing toward 5.5 million units in fiscal year 2025 per the Society of Indian Automobile Manufacturers SIAM driving Indian steel demand from domestic producers ArcelorMittal Nippon Steel India and JSW Steel. OICA confirmed global vehicle production of approximately 92 million units in 2024, with passenger vehicles each containing between 800 and 1,000 kilograms of steel per unit representing 55% to 65% of total vehicle weight. ArcelorMittal committed to supply 12 million metric tonnes of reduced-carbon steel by 2030 utilising hydrogen-based direct reduction per its 2024 Sustainability Report, positioning itself for the decarbonisation transition that European automotive OEM Scope 3 carbon reporting requirements are beginning to price into steel procurement. POSCO launched a new electric arc furnace facility in South Korea in Q2 2024 to enhance its capacity for low-carbon steel production supporting its HyREX hydrogen-based ironmaking decarbonisation strategy. For instance, in March 2024, ArcelorMittal, Luxembourg, introduced a new high-strength dual-phase steel product for the automotive industry, developed to provide enhanced performance in safety, fuel efficiency, and lightweight construction, as part of its push to support sustainable automotive manufacturing meeting stricter regulatory requirements for fuel economy and emissions compliance. These are some of the key factors driving revenue growth of the market.

Automotive flat steel held approximately 68% of total automotive steel market volume in 2025, encompassing hot-dip galvanised and cold-rolled coil for body panels, BIW structural members, and closures at continuous steel supply agreements between ArcelorMittal, Nippon Steel, POSCO, ThyssenKrupp, and global automotive OEM body shop operations. ArcelorMittal, Baowu, POSCO, and Nippon Steel collectively controlled approximately 45% of global automotive-grade steel output in 2024 per competitive structure data consistent with their disclosed annual production capacities. EV platform structural battery protection frames require press hardened steel at sill and rocker panel positions at approximately 40% above ICE per-vehicle content per vehicle, sustaining AHSS demand in EV platforms and preventing the per-vehicle steel intensity decline that aluminium closure substitution at premium EV segments would otherwise imply. Global decarbonisation of steelmaking is the most material long-term structural change in the automotive steel supply chain, with EAF-based low-carbon steel production capacity growing at ArcelorMittal, POSCO HyREX, and Tata Steel through 2025 and 2026.

However, aluminium substitution in outer body panel applications is intensifying at premium European and North American OEM platforms, with BMW Group and Mercedes-Benz increasing aluminium content in hoods, door skins, and trunk lids from approximately 40% to 60% of panel weight at their highest-specification models between 2020 and 2025, reducing automotive flat steel consumption at the per-vehicle level in premium segments even as overall automotive steel demand grows on production volume and EV structural steel content increases. ArcelorMittal's 2024 commitment to supply reduced-carbon steel requires hydrogen-based direct reduction infrastructure investment that will take 5 to 7 years to deploy at commercial scale, creating an interim period where carbon-intensive blast furnace steel must serve OEM Scope 3 commitments that have already been made for 2025 and 2026 purchasing programmes. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated global steel production energy costs through LNG and natural gas cost elevation at blast furnace and EAF steelmaking operations in Europe, adding approximately USD 30 to USD 60 per metric tonne to European automotive steel production cost in Q2 2026. These factors substantially limit automotive steel market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Advanced high-strength steel penetration in automotive body structures exceeded 28% of total automotive steel usage in 2024 per industry data, growing from approximately 18% in 2018, driven by OEM lightweighting programmes that substitute AHSS grades at 590 to 2000 MPa tensile strength for mild steel at equivalent thickness at 30% to 50% weight reduction while meeting identical crash performance requirements. Each unit percentage point increase in AHSS penetration at constant vehicle production volumes represents approximately 2.1 million metric tonnes of demand shift from mild steel to premium-priced advanced high-strength grades, generating revenue growth above production volume growth rate for AHSS-capable producers. EV battery protection structures at sill, rocker, and underbody positions require press hardened steel at 1500 MPa tensile strength that provides energy absorption per unit weight superior to mild steel, conventional HSS, and aluminium alloy alternatives at commercially viable body shop tooling investment, sustaining AHSS content per EV above ICE equivalent by approximately 40% at press hardened steel applications. Indian and Southeast Asian Vehicle Production Growth Driving New Automotive Steel Demand India's passenger vehicle production growing toward 5.5 million units in fiscal year 2025 per SIAM data, combined with SIAM's expectation of growth toward 6 million units by fiscal year 2027, represents the single largest new automotive steel demand increment in a market where domestic steel supply is expanding at AM/NS India and JSW Steel simultaneously. Tata Steel India at Jamshedpur and JSW Steel at Vijayanagar supply hot-rolled and cold-rolled automotive-grade steel coil to Indian automotive OEM body shops, with the AM/NS India January 2025 launch of advanced automotive steel production adding AHSS grade capability that previously required import from Japan, South Korea, or Europe at USD 180 to USD 260 per metric tonne import premium. Vietnam, Thailand, and Indonesia automotive production growing collectively at above-5% per year provides additional Southeast Asian demand for automotive steel from regional suppliers and Japanese and Korean producers expanding distribution networks in the region.

BMW Group, Audi, and Mercedes-Benz aluminium closure panel programmes reducing automotive flat steel consumption at premium segment volumes that represent disproportionate per-unit revenue for ArcelorMittal and ThyssenKrupp automotive steel supply chains, with high-specification cold-rolled and hot-dip galvanised coil losing outer panel tonnage to Novelis and Constellium aluminium sheet at approximately 30% to 40% density advantage per panel. ArcelorMittal's 12 million metric tonne reduced-carbon steel commitment for 2030 requires hydrogen-based direct reduction infrastructure at a capital cost estimated at EUR 1 to EUR 2 billion per million metric tonne of decarbonised production capacity, creating a multi-year capital investment cycle where interim carbon-intensive blast furnace production must satisfy OEM Scope 3 procurement requirements that are increasingly specifying embodied carbon limits. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated European blast furnace and EAF steelmaking energy costs through LNG price increases, adding approximately USD 30 to USD 60 per metric tonne to European automotive steel production cost in Q2 2026 against 2024 baseline. These factors substantially limit automotive steel market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Flat Steel, Long Steel, Pipe and Tube | Flat Steel |

| Grade | Mild Steel, High Strength Steel, Advanced High Strength Steel, Ultra High Strength Steel | Mild Steel |

| Application | Body Structure, Chassis and Suspension, Powertrain, Closures, Bumper Systems | Body Structure |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles | Passenger Cars |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Flat Steel segment is expected to account for a significantly large revenue share in the global automotive steel market during the forecast period.

This report evaluates product type across Flat Steel, Long Steel, Pipe and Tube for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates grade across Mild Steel, High Strength Steel, Advanced High Strength Steel, Ultra High Strength Steel for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Body Structure, Chassis and Suspension, Powertrain, Closures, Bumper Systems for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

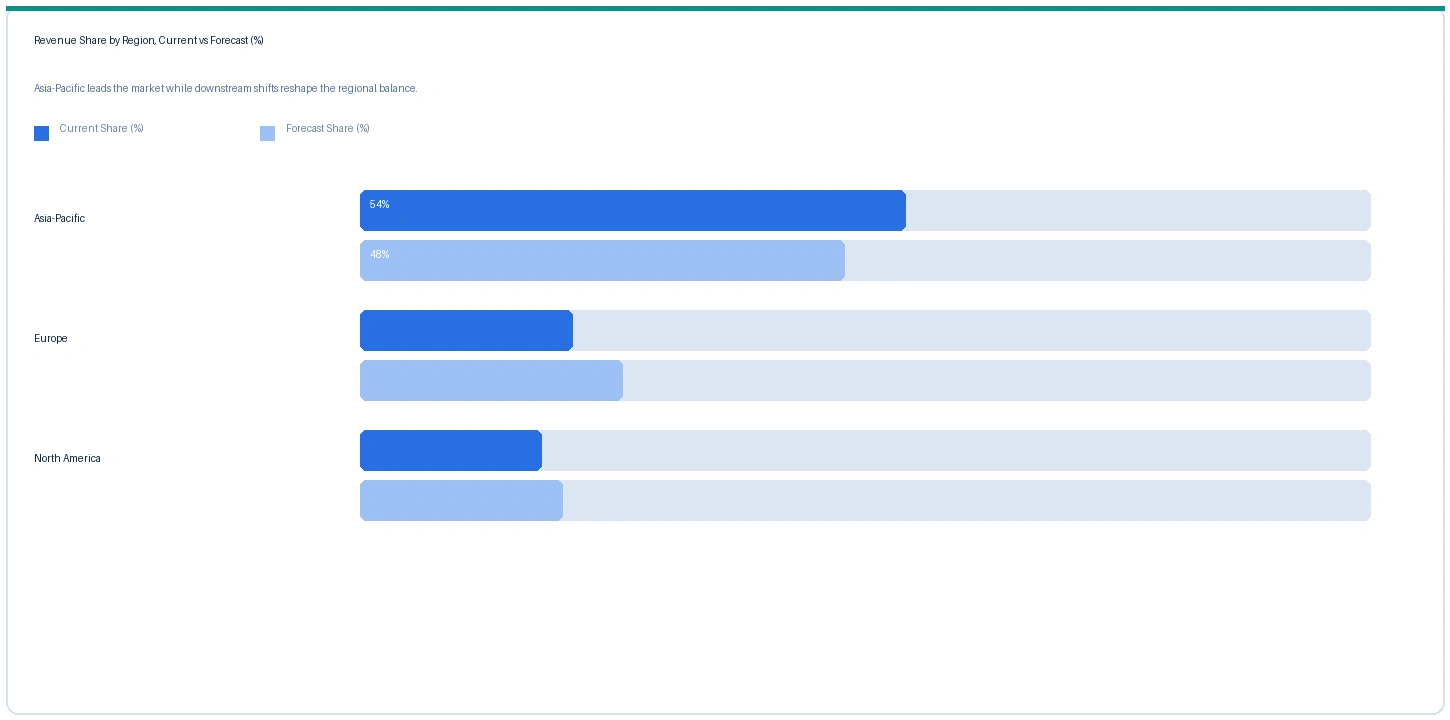

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive steel market in 2025. Based on regional analysis, the automotive steel market in Asia-Pacific accounted for largest revenue share in 2025. China alone accounted for approximately 45% to 50% of global automotive steel consumption, with Baowu Group (including Baosteel), HBIS Group, Ansteel Group, and POSCO Zhangjiagang supplying above-30-million-unit annual Chinese vehicle production. Japan's NSSMC, JFE Steel, and Kobe Steel supply Japanese OEM body shops at Toyota, Honda, and Nissan assembly operations. South Korea's POSCO supplies Hyundai Motor Group and Korean export markets with advanced automotive steel grades including GIGA STEEL press hardened steel.

The market in Europe is expected to register the second largest revenue share. ArcelorMittal European Flat Products at Gent Belgium, Fos-sur-Mer France, and Eisenhuttenstadt Germany, ThyssenKrupp Steel Europe at Duisburg, voestalpine Stahl at Linz Austria, and Tata Steel at Ijmuiden Netherlands supply European automotive body shops. European automotive steel commands the highest per-unit value globally on premium AHSS grades and hot-dip galvanised quality specifications. EU CO2 fleet average regulations sustaining lightweighting investment at European OEM programmes create structural demand for premium AHSS at ArcelorMittal and ThyssenKrupp.

North America market is expected to register steady revenue growth in the global automotive steel market during the forecast period. The market in North America is anchored in ArcelorMittal AM/NS Calvert Alabama following June 2025 full acquisition, Cleveland-Cliffs, Nucor Corporation, and Nippon Steel following its June 2025 acquisition of US Steel, supplying Ford, General Motors, Stellantis, Toyota, Honda, and Volkswagen North American body shop operations. Section 232 tariffs on imported steel from Canada and Mexico create competitive dynamics between domestic and regional producers.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Hot-Dip Galvanised CR (automotive grade) | Europe | USD 860/MT | USD 800/MT | Rising | ArcelorMittal / ThyssenKrupp ref |

| Hot-Dip Galvanised CR (automotive grade) | Asia-Pacific | USD 740/MT | USD 700/MT | Stable | POSCO / Baowu ref |

| Dual Phase DP 780 (AHSS) | Europe | USD 940/MT | USD 880/MT | Rising | Grade premium ref |

| Press Hardened Steel Usibor 1500 | Europe | USD 1,240/MT | USD 1,140/MT | Rising | ArcelorMittal ref |

| EAF Low-Carbon Steel (reference) | Europe | USD 920/MT | USD 880/MT | Rising | Green premium +EUR 60-80 |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, CRU Group steel pricing methodology references, and automotive OEM supply chain monitoring. Prices represent delivered ex-works at European and Asian steel service centres for automotive OEM supply agreements.

European hot-dip galvanised cold-rolled coil for automotive applications rose approximately 7.5% in Q2 2026 against Q2 2025, driven by LNG and natural gas cost elevation at European blast furnace and EAF steelmaking operations from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026. Asian automotive HDG coil remained stable in Q2 2026 at approximately USD 740 per metric tonne, with Chinese domestic overcapacity and lower energy cost exposure to Hormuz LNG disruption maintaining Asian pricing competitiveness. European press hardened steel rose approximately 8.8% from USD 1,140 per metric tonne in Q2 2025 to USD 1,240 per metric tonne in Q2 2026, reflecting both energy cost increases and growing demand from Euro 7 homologated EV platform battery protection frame programmes requiring ArcelorMittal Usibor 1500 or equivalent POSCO GIGA STEEL qualification.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive steel market, the Hormuz disruption operates through two simultaneous cost channels. European blast furnace and EAF steelmaking operations at ArcelorMittal Gent, ThyssenKrupp Duisburg, and voestalpine Linz consume LNG and natural gas for furnace operations and heat treatment at costs elevated approximately EUR 8 to EUR 14 per MWh above the 2024 baseline from Hormuz-disrupted GCC LNG exports, contributing approximately USD 30 to USD 60 per metric tonne to European automotive steel production cost in Q2 2026. Coking coal and iron ore freight logistics are secondarily elevated from broader maritime shipping cost increases across bulk carrier trades affected by the Gulf of Oman and Strait of Hormuz shipping disruption, adding approximately USD 5 to USD 15 per metric tonne to steelmaking raw material delivered cost at European and Asian integrated steel mills.

Company Insights

The two key dominant companies in the automotive steel market are ArcelorMittal and Nippon Steel Corporation, recognised for their global production scale, breadth of automotive AHSS grade qualification at major OEM body shops worldwide, and leadership in decarbonised steel technology development for automotive Scope 3 requirements.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 86.40 Billion |

| Market Size 2032 | USD 135.60 Billion |

| CAGR | 6.6% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product Type, By Grade, By Application, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Luxembourg, Austria, Japan, South Korea, China, India, Brazil, South Africa |

| Companies Profiled | ArcelorMittal, Nippon Steel, POSCO, ThyssenKrupp Steel Europe, Baowu Group, Tata Steel, JFE Steel, Hyundai Steel, Cleveland-Cliffs, Nucor, voestalpine, SSAB, AM/NS India, JSW Steel |

| Key Data Sources | World Steel Association 2023 crude steel production data, ArcelorMittal 2024 Sustainability Report XCarb commitment, POSCO EAF facility inauguration Q2 2024, ArcelorMittal AM/NS Calvert acquisition completion June 2025, Nippon Steel US Steel acquisition completion June 2025, AM/NS India automotive steel launch January 2025, OICA 2024 global vehicle production statistics, SIAM FY2025 Indian vehicle production data, IEA Global EV Outlook 2025, Nucor USD 3 billion investment announcement Q1 2024, IMF March 2026 Strait of Hormuz statement, 19 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 276 |

| Published | Q2 2026 |

| SKU | NXC-AT-007 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 19 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included automotive steel commercial and product management leads at European, North American, Asian, and Indian integrated steel producers, AHSS technical application specialists, and EV platform body structure steel sourcing leads. Demand-side contacts included automotive body shop steel procurement managers at European, North American, and Asian OEMs, body structure stamping Tier 1 material sourcing leads, and EV platform structural battery protection frame engineering leads. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include World Steel Association global crude steel production data 2023, ArcelorMittal 2024 Sustainability Report and XCarb commitment announcement, POSCO EAF facility inauguration announcement Q2 2024, ArcelorMittal AM/NS Calvert acquisition completion June 2025, Nippon Steel US Steel acquisition completion June 2025, AM/NS India automotive steel line launch January 2025, OICA 2024 global vehicle production statistics, SIAM FY2025 Indian vehicle production data, IEA Global EV Outlook 2025, Nucor USD 3 billion mill investment announcement Q1 2024, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.