Market Data

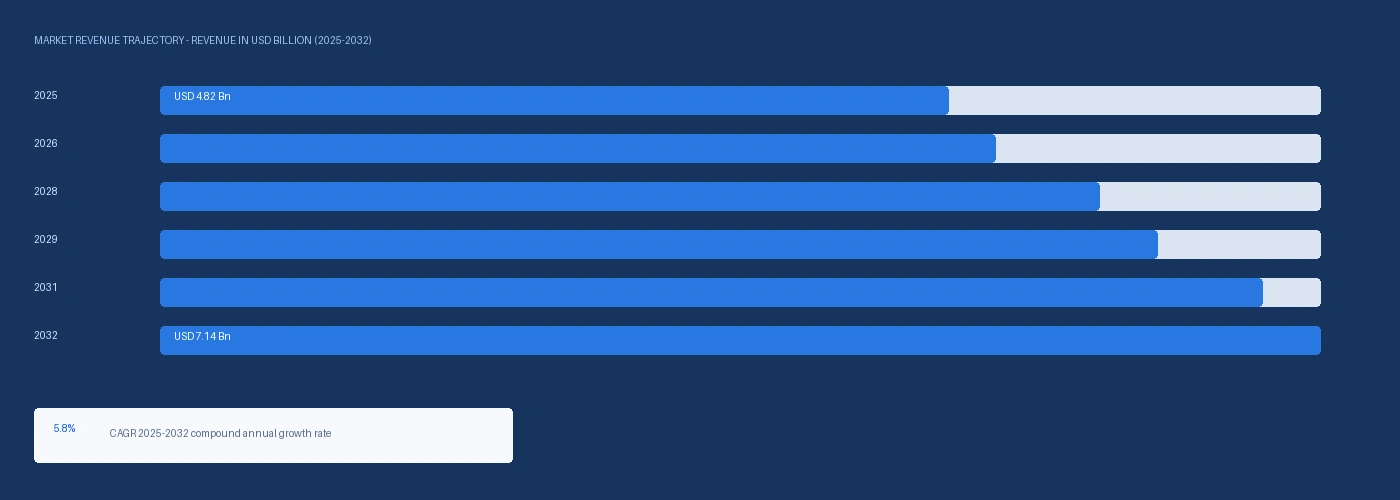

The global automotive stainless steel tube market size was USD 4.82 Billion in 2025 and is expected to register a revenue CAGR of 5.8% during the forecast period. Market revenue growth is supported by Euro 7 emission standard requirements for higher-temperature and higher-corrosion-resistance stainless steel exhaust tube grades at positions downstream of gasoline particulate filters and selective catalytic reduction systems where condensate chemistry is more aggressive than under Euro 6d conditions, Outokumpu Annual Report 2024 confirming global stainless steel cold-rolled flat product market of approximately 33.3 million tonnes with automotive as a primary end-use segment, and EV coolant circuit tube demand growing at above-average rates as battery thermal management systems require austenitic 304 and 316L grade stainless steel tubes for glycol-water coolant loop integrity at battery operating temperatures of minus 40 to plus 60 degrees Celsius. OICA confirmed global passenger vehicle production of approximately 92 million units in 2024, with each ICE vehicle incorporating approximately 4 to 8 kilograms of stainless steel tube in exhaust systems depending on vehicle class, plus additional stainless tube content in fuel lines, brake lines, and cooling circuits. Sandvik AB developed a new line of austenitic stainless steel tubes specifically designed for EV battery pack cooling systems in 2023, achieving a 24% weight reduction compared to conventional stainless tube designs through modified wall thickness and alloy optimisation, targeting the growing EV battery thermal management tube market. Outokumpu's Circle Green low-emission stainless steel, with a carbon footprint of 0.5 kg CO2 equivalent per kilogram versus the global stainless steel average of 7 kg CO2 equivalent per kilogram per its 2024 Annual Report, is qualifying at automotive OEM tier-one exhaust and fluid system tube producers who face Scope 3 embodied carbon reporting requirements from German and French OEM sustainability programmes. For instance, in 2023, Outokumpu, Finland, partnered with an Asian electric vehicle OEM to develop stainless steel tube grades for EV battery cooling systems, with the collaboration resulting in a 36% increase in qualified stainless tube supply to the partnered OEM's battery thermal management production programme. These are some of the key factors driving revenue growth of the market.

Stainless steel exhaust tube for automotive passenger cars uses primarily ferritic grades 409 (11% chromium), 439 (17% chromium), 441 (17-18% chromium with niobium and titanium stabilisation), and 444 (18-19% chromium with molybdenum) with grade selection determined by position in the exhaust system, operating temperature range, and condensate chemistry from fuel type and catalytic converter technology. Seamless stainless steel tubes accounted for approximately 56% of the automotive stainless steel tube market by volume in 2024 per industry data, driven by their dominance in fuel system, brake line, and high-pressure hydraulic applications where seam integrity at elevated pressure is required under automotive safety specifications. Tubacex S.A., headquartered in Llodio, Spain, supplies precision seamless stainless steel tubes for automotive fuel injection systems and hydraulic brake circuits to European Tier 1 automotive fluid system manufacturers including Bosch, Continental, and Robert Bosch GmbH. Centravis, headquartered in Nikopol, Ukraine, supplies cold-drawn seamless austenitic and duplex stainless steel tubes for European automotive fluid system applications, with its EU export customer base maintained through alternative logistics routes since 2022.

However, EV powertrain elimination of combustion exhaust systems removes the exhaust tube content from each BEV platform, with OICA confirming approximately 17 million EVs produced in 2024 at zero exhaust system stainless steel content per vehicle, creating a structural volume headwind as EV production grows toward 35% of global vehicle sales by 2030 per IEA projections that will reduce per-vehicle stainless tube content across the global fleet average. Nickel price volatility, with LME nickel trading between USD 12,000 and USD 20,000 per metric tonne through 2024 on Indonesian production and speculative position unwinding, creates input cost uncertainty at austenitic 304 and 316L grade stainless steel tube producers whose nickel content at 8% to 12% by weight represents a significant proportion of total production cost that is difficult to fully pass through to OEM annual supply agreements. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated LNG energy costs at Outokumpu's Tornio, Finland melt shop and European stainless tube producers, adding approximately EUR 8 to EUR 14 per MWh above 2024 baseline to electric arc furnace steelmaking energy cost. These factors substantially limit automotive stainless steel tube market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Regulation (EU) 2024/1257 Euro 7 emission standards, effective for new type approvals from July 2025, introduce cold-start performance requirements at minus 10 degrees Celsius and real-driving emissions test cycles with more aggressive throttle transients that generate higher peak exhaust gas temperatures and more frequent thermal cycling in the exhaust system than Euro 6d RDE tests. Extended thermal cycling between ambient cold-soak temperatures of minus 10 to minus 30 degrees Celsius and peak exhaust gas temperatures above 900 degrees Celsius at turbocharged DI gasoline engines requires stainless exhaust tube grades with higher chromium content and improved thermal fatigue resistance than 409 grade provides, favouring 441 and 444 high-chromium ferritic grades at front pipe and catalyst substrate carrier positions. Outokumpu's 4C54 ferritic grade (18% chromium, silicon-stabilised) and its 4509 and 4521 high-chromium ferritic grades are being actively qualified at European exhaust Tier 1 manufacturers including Eberspacher, Tenneco, and Faurecia for Euro 7 rear silencer and GPF housing applications. EV battery thermal management stainless tube demand is growing at approximately 18% to 22% per year as each BEV requires 1.5 to 3.5 kilograms of austenitic 304 or 316L stainless tube in the battery coolant loop, glycol-water supply and return manifolds, and chiller plate connection circuits. Bharat Stage VI and China 6b Exhaust System Upgrades Driving Asian Stainless Tube Demand India's Bharat Stage VI emission standard and China's China 6b real-driving emissions standard both require catalytic converter and diesel particulate filter integration in exhaust systems that operate at higher temperatures and more demanding thermal cycles than predecessor standards, requiring upstream ferritic stainless steel grades with improved high-temperature oxidation resistance. India's Society of Indian Automobile Manufacturers SIAM confirmed passenger vehicle production of approximately 4.5 million units in fiscal year 2025, with BSVI-compliant exhaust systems consuming higher-grade ferritic stainless tube at catalytic converter substrate carrier positions. Jindal Stainless, India's largest stainless steel producer, confirmed expanding production of automotive exhaust-grade ferritic stainless steel coil and tube at its Hisar facility in 2024, targeting domestic Tier 1 exhaust suppliers manufacturing BSVI-compliant exhaust systems for Maruti Suzuki, Tata Motors, and Hyundai India.

Each BEV produced in place of an ICE vehicle eliminates approximately 4 to 8 kilograms of exhaust system stainless steel tube content per vehicle, representing a structural demand headwind from the IEA Stated Policies scenario of approximately 35% EV share by 2030. At 17 million EVs produced in 2024 per OICA data, the market is already absorbing approximately 68,000 to 136,000 metric tonnes of exhaust stainless tube demand displacement annually relative to an all-ICE production scenario, partially offset by EV battery cooling tube demand of approximately 25,500 to 59,500 metric tonnes at 1.5 to 3.5 kg per EV. LME nickel price volatility between USD 12,000 and USD 20,000 per metric tonne in 2024, driven by Indonesian nickel sulphate production expansion and speculative position management at the London Metal Exchange, creates input cost instability at 304 and 316L austenitic stainless tube producers that translates into alloy surcharge uncertainty in annual OEM supply agreements. The US-Iran conflict and Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated EAF steelmaking energy costs at Outokumpu Tornio and European stainless tube producers through LNG price increases, adding approximately USD 20 to USD 40 per metric tonne to European stainless tube production cost in Q2 2026. These factors substantially limit automotive stainless steel tube market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Welded Stainless Steel Tube, Seamless Stainless Steel Tube | Welded Stainless Steel Tube |

| Grade | Ferritic (409/439/441/444), Austenitic (304/316L), Duplex | Ferritic (409/439/441/444) |

| Application | Exhaust System, Fuel and Motor System, Cooling System, Brake Lines, Structural | Exhaust System |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles | Passenger Cars |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Seamless Stainless Steel Tube segment is expected to account for a significantly large revenue share in the global automotive stainless steel tube market during the forecast period.

This report evaluates product type across Welded Stainless Steel Tube, Seamless Stainless Steel Tube for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates grade across Ferritic (409/439/441/444), Austenitic (304/316L), Duplex for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Exhaust System, Fuel and Motor System, Cooling System, Brake Lines, Structural for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

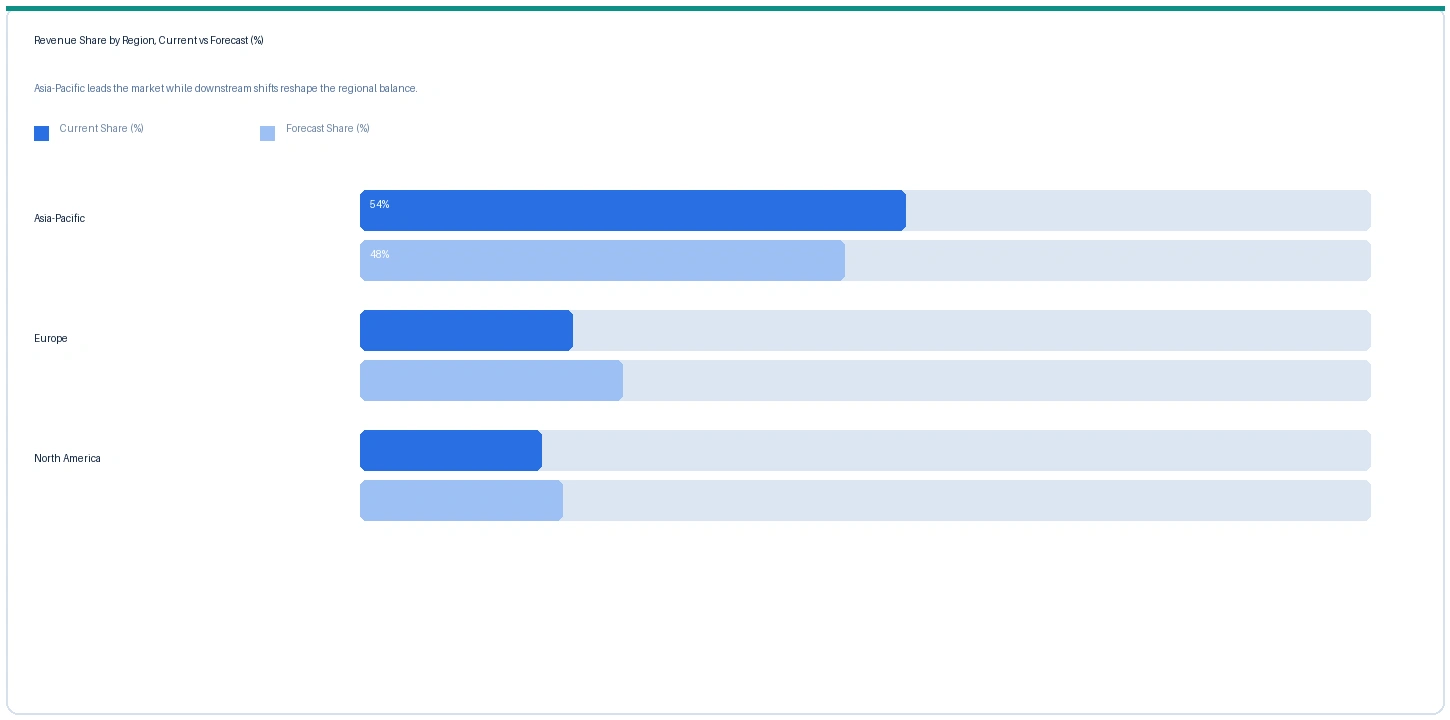

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive stainless steel tube market in 2025. Based on regional analysis, the automotive stainless steel tube market in Asia-Pacific accounted for largest revenue share in 2025. China, Japan, South Korea, and India account for approximately 55% to 60% of global automotive stainless steel tube consumption by volume, driven by the region's dominance in global vehicle production at approximately 55 million units of the 92 million total in 2024. Chinese domestic stainless tube producers including Baosteel Special Steel (now part of Baowu Group) and Shanxi Taigang Stainless Steel Co. supply Chinese automotive exhaust and fluid system Tier 1 manufacturers with ferritic and austenitic grades at costs substantially below European and Japanese equivalent specifications. Jindal Stainless India's expanded production at Hisar directly targets the Indian automotive market growing toward 5.5 million vehicles per year.

Europe market accounted for second largest revenue share in the global automotive stainless steel tube market in 2025. The market in Europe is expected to register the second largest revenue share. Outokumpu at Tornio, Finland and its European flat product distribution network supplies ferritic and austenitic stainless coil to European exhaust and fluid tube producers including Fischer Group, Salzgitter Mannesmann Precision, and Centravis European operations. Euro 7 grade upgrade requirements at European exhaust system Tier 1 manufacturers Eberspacher, Tenneco, and Faurecia are driving specification transitions from 409 to 441 and 444 ferritic grades that command premium pricing versus commodity 409 grade.

North America market is expected to register steady revenue growth in the global automotive stainless steel tube market during the forecast period. The market in North America is anchored in Outokumpu Americas operations, Allegheny Technologies (ATI), and North American Stainless supplying exhaust and fluid system tube to US automotive OEM Tier 1 manufacturers. US EPA Tier 3 vehicle emission standards require three-way catalytic converter integration in all new light-duty vehicles, sustaining exhaust stainless tube demand at approximately 28 million new vehicles per year in the North American market.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Ferritic 409 Exhaust Tube (OD 50mm) | Europe | USD 2,180/MT | USD 2,040/MT | Rising | Outokumpu alloy ref |

| Ferritic 441 Exhaust Tube (OD 60mm) | Europe | USD 2,680/MT | USD 2,480/MT | Rising | Grade upgrade ref |

| Austenitic 304 EV Cooling Tube (OD 22mm) | Asia-Pacific | USD 3,420/MT | USD 3,180/MT | Rising | EV battery loop ref |

| Austenitic 316L Fuel System Tube | Europe | USD 4,240/MT | USD 3,960/MT | Rising | Tubacex ref |

| Ferritic 409 Exhaust Tube (OD 50mm) | Asia-Pacific | USD 1,820/MT | USD 1,700/MT | Stable | Baosteel ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, LME nickel monitoring, Outokumpu alloy surcharge publications, and automotive Tier 1 supply chain monitoring. Prices include base stainless steel coil cost, tube production cost, and delivery to Tier 1 customer.

European ferritic 409 exhaust tube prices rose approximately 6.9% in Q2 2026 against Q2 2025, driven by energy cost elevation at European stainless steel melt shop operations from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which restricted GCC LNG exports and elevated European natural gas prices above 2024 baseline by approximately EUR 8 to EUR 14 per MWh. Ferritic 441 grade exhaust tube rose approximately 8.1% in Europe on the combined effect of alloy surcharge increases from higher-chromium content specification and the energy cost elevation at cold-rolling operations. Austenitic 304 EV cooling tube rose approximately 7.5% in Asia-Pacific on growing battery thermal management demand from Chinese EV OEM production expansion at BYD and NIO exceeding regional stainless tube supply additions.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive stainless steel tube market, the Hormuz disruption operates through energy cost elevation at European electric arc furnace stainless steel production. Outokumpu's Tornio melt shop in Finland and European stainless tube cold-rolling operations at Sandvik's tube mills and Tubacex's Llodio facility all consume LNG or grid electricity produced partially from natural gas at prices elevated above 2024 baseline by approximately EUR 8 to EUR 14 per MWh from the Hormuz-disrupted European LNG supply. Additionally, LME nickel prices are partially affected by freight cost increases on Indonesian nickel sulphate exports transiting Strait of Malacca adjacent routes, with LME nickel elevated approximately 4% to 6% above the pre-disruption 2026 baseline in Q2 2026 contributing to austenitic stainless alloy surcharge increases at European tube suppliers.

Company Insights

The two key dominant companies in the automotive stainless steel tube market are Outokumpu Oyj and Sandvik AB, recognised for their technical leadership in automotive-grade ferritic and austenitic stainless steel tube production, their established supply relationships with European automotive exhaust and fluid system Tier 1 manufacturers, and their innovation in EV-specific stainless tube grades for battery thermal management applications.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 4.82 Billion |

| Market Size 2032 | USD 7.14 Billion |

| CAGR | 5.8% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product Type, By Grade, By Application, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Finland, Sweden, Spain, China, Japan, South Korea, India, Brazil |

| Companies Profiled | Outokumpu Oyj, Sandvik AB, Tubacex S.A., Centravis, Fischer Group, Salzgitter Mannesmann Precision, Marcegaglia, POSCO, Nippon Steel, Jindal Stainless, Baosteel, Maxim Tubes, CSM Tube, Tata Steel |

| Key Data Sources | Outokumpu Financial Statements Release 2024, Outokumpu Annual Report 2024 global stainless market data, Sandvik AB Summerill Tube acquisition January 2020, Sandvik EV cooling tube development 2023, Regulation (EU) 2024/1257 Euro 7 emission standards, OICA 2024 global vehicle production statistics, Outokumpu Circle Green carbon footprint data, Jindal Stainless FY2025 expansion announcement, IEA Global EV Outlook 2025, IMF March 2026 Strait of Hormuz statement, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 258 |

| Published | Q2 2026 |

| SKU | NXC-AT-006 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 15 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included automotive stainless steel tube commercial and product management leads at European and Asian producers, alloy surcharge specialists at stainless steel producers, and EV battery cooling tube technical development leads. Demand-side contacts included exhaust system stainless tube procurement managers at European Tier 1 exhaust manufacturers, EV battery thermal management tube specification engineers, and automotive fluid system procurement leads at European and North American Tier 1 brake and fuel system manufacturers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Outokumpu Financial Statements Release 2024 published February 2025, Outokumpu Annual Report 2024 global stainless market data, Sandvik Materials Technology Summerill Tube acquisition announcement January 2020, Sandvik EV cooling tube development communications 2023, Regulation (EU) 2024/1257 Euro 7 emission standards, OICA 2024 global vehicle production statistics, Outokumpu Circle Green low-emission stainless carbon footprint lifecycle assessment data, Jindal Stainless Hisar facility expansion announcement, IEA Global EV Outlook 2025, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.