Market Data

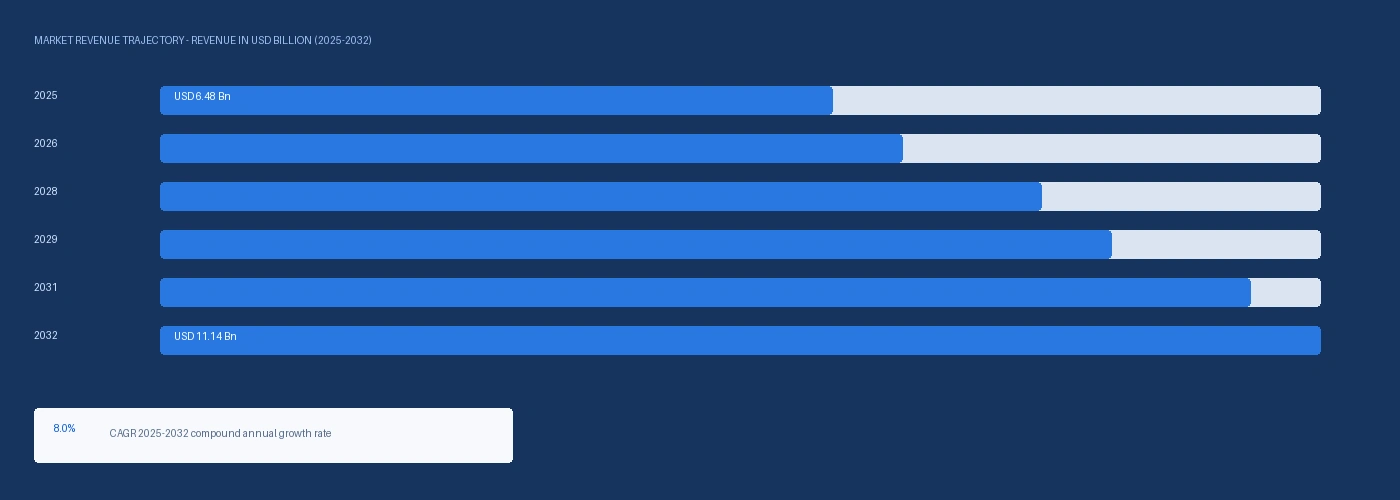

The global automotive specialty coating market size was USD 6.48 Billion in 2025 and is expected to register a revenue CAGR of 8.0% during the forecast period. Market revenue growth is supported by EV battery thermal management coating demand from CATL and BYD battery cell and module surface insulation applications requiring thermally conductive but electrically insulating ceramic and polymer coatings at USD 42 to USD 68 per kilogram versus USD 4 to USD 12 per kilogram for conventional underbody anti-corrosion coatings, ADAS radar-transparent coating demand from automotive bumper and fascia applications requiring dielectric properties that preserve 77 GHz millimetre-wave radar transmission for autonomous driving sensor systems, and electric motor laminate coating demand from EV traction motor stator lamination electrical insulation applications at Axalta Voltatex and BASF Voltasurf insulating varnish product lines. Axalta Coating Systems confirmed in its Q1 2025 earnings that it had won Edison Awards and a BIG Innovation Award for technology advancements in automotive materials and electrical systems, with Axalta's Voltatex electric motor insulation coating nominated for the award in recognition of its above-conventional-temperature thermal class H and class C insulation performance at EV traction motor stator winding applications. PPG Industries disclosed its low-temperature curing expanded bake ENVIRO-PRIME electrocoat coating can be applied to heavy EV assemblies with a savings of 20 kilowatt-hours of energy and 4 kilograms of carbon emissions per vehicle produced versus conventional high-temperature OEM electrocoat cure cycles. For instance, in March 2025, BASF SE, Germany, confirmed commercial qualification of a radar-transparent coating grade at its Schwarzheide coating facility for automotive bumper ADAS applications, enabling 77 GHz millimetre-wave radar transmission at above 95% signal efficiency while providing UV stability and paint adhesion performance required for OEM exterior colour-matched bumper production at European automotive manufacturers including BMW and Mercedes-Benz. These are some of the key factors driving revenue growth of the market.

Electric motor insulating varnish and laminate coatings represent the fastest-growing specialty coating segment by value within the automotive market, with EV traction motor stator lamination requiring Class H at 180 degrees Celsius or Class C at 220 degrees Celsius insulating varnish at Axalta Voltatex, Elantas, and Hitachi Chemical product formulations that command pricing of USD 48 to USD 86 per kilogram versus USD 8 to USD 18 per kilogram for conventional automotive anti-corrosion primers. The IEA confirmed approximately 17 million EV and PHEV units sold in 2024, with each BEV traction motor requiring approximately 0.8 to 1.6 kilograms of insulating varnish per motor at Class H or Class C specification. BASF SE's Voltasurf product line for EV motor and battery surface applications and Axalta's Edison Award-nominated Voltatex electric motor insulation coating platform confirm the two primary European automotive coating suppliers as the leading commercial qualification holders for EV motor insulating varnish. Coating Technologies Group confirmed in its 2024 North America operations briefing that its EV-specific thermal spray ceramic coating for battery module surfaces had received OEM qualification at two North American EV platform programmes.

However, radar-transparent coating development for ADAS bumper applications faces a design constraint that conventional automotive OEM exterior coating processes impose: standard two-component polyurethane clearcoat at 30 to 60 micron dry film thickness attenuates 77 GHz millimetre-wave radar signal by approximately 1 to 3 decibels per coating layer, and accumulated attenuation through base coat, clearcoat, and bumper substrate composite stack can reduce radar detection range by 8% to 15% at maximum stack thickness. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated titanium dioxide and specialty ceramic filler costs for thermally conductive automotive specialty coatings, adding approximately USD 180 to USD 320 per metric tonne to EV battery thermal management coating raw material costs at European producers in Q2 2026. These factors substantially limit automotive specialty coatings market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EV traction motors operate at continuous winding temperatures of 150 to 200 degrees Celsius in performance and commercial vehicle applications, requiring Class H at 180 degrees Celsius or Class C at 220 degrees Celsius insulating varnish on stator copper windings and lamination stacks that prevent winding-to-lamination short circuit from thermal degradation of the insulation system over the 8 to 12 year service life required by automotive OEM warranty programmes. Axalta Voltatex insulating varnish, which won Edison Award recognition in Q1 2025, holds OEM qualification at multiple European and Asian traction motor producers for Class H and Class C applications. Each EV traction motor consuming approximately 0.8 to 1.6 kilograms of insulating varnish at USD 48 to USD 86 per kilogram generates USD 38 to USD 138 per motor of insulating varnish content, and premium dual-motor EV platforms at BMW, Porsche, and Lucid Motors double this per-vehicle specialty coating content. The IEA EV production scenario of 35 million EV units per year by 2030, with approximately 1.3 motors per vehicle on average, implies global EV motor insulating varnish demand reaching approximately 36,000 to 73,000 metric tonnes per year by 2030. ADAS Radar-Transparent Coating and Hydrophobic Sensor Protection Coating Demand from Autonomous Driving System Penetration Automotive radar-based ADAS systems including adaptive cruise control, automatic emergency braking, and lane change assist require 77 GHz millimetre-wave radar sensors mounted behind painted bumpers and fascia panels whose coating stack must preserve above-95% radar signal transmission efficiency. BASF confirmed commercial qualification of its radar-transparent coating at Schwarzheide in March 2025 for BMW and Mercedes-Benz ADAS bumper applications, the first German OEM-qualified radar-transparent automotive coating. OICA confirmed EV and ADAS sensor package penetration in approximately 68% of new global passenger car registrations at Level 2 or above in 2024, establishing ADAS sensor coating as a mainstream rather than premium application within the automotive specialty coating addressable market.

The accumulated signal attenuation through a full OEM exterior coating stack of primer, basecoat, and clearcoat above a plastic bumper substrate can reduce 77 GHz radar detection range by 8% to 15% at maximum film thickness specifications, creating an engineering design constraint that requires radar-transparent coating development to simultaneously satisfy OEM paint quality specifications including gloss, distinctness of image, and chip resistance while maintaining dielectric properties within the radar system attenuation budget. BASF's March 2025 qualification achievement confirms the dielectric constraint is solvable within OEM paint specifications, but the solution requires specialty low-dielectric-constant resin and filler systems that command a material premium of approximately USD 12 to USD 24 per kilogram above conventional automotive clearcoat formulations. Titanium dioxide and specialty ceramic filler costs for thermally conductive EV battery coating applications were elevated approximately USD 180 to USD 320 per metric tonne in Q2 2026 from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026. These factors substantially limit automotive specialty coatings market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Thermal Management Coatings, Anti-Corrosion Coatings, Radar-Transparent Coatings, Hydrophobic and Self-Cleaning, Acoustic Damping, Electric Motor Insulating Varnish | Thermal Management Coatings |

| Vehicle Type | Passenger Cars, Commercial Vehicles, Electric Vehicles | Passenger Cars |

| Application | Exterior (ADAS Sensors, Anti-Chip), Interior, Powertrain and Engine, Battery and EV Systems (Motor Varnish, Battery Thermal) | Exterior (ADAS Sensors, Anti-Chip) |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Anti-Corrosion Coatings segment is expected to account for a significantly large revenue share in the global automotive specialty coatings market during the forecast period.

This report evaluates type across Thermal Management Coatings, Anti-Corrosion Coatings, Radar-Transparent Coatings, Hydrophobic and Self-Cleaning, Acoustic Damping, Electric Motor Insulating Varnish for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Commercial Vehicles, Electric Vehicles for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Exterior (ADAS Sensors, Anti-Chip), Interior, Powertrain and Engine, Battery and EV Systems (Motor Varnish, Battery Thermal) for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

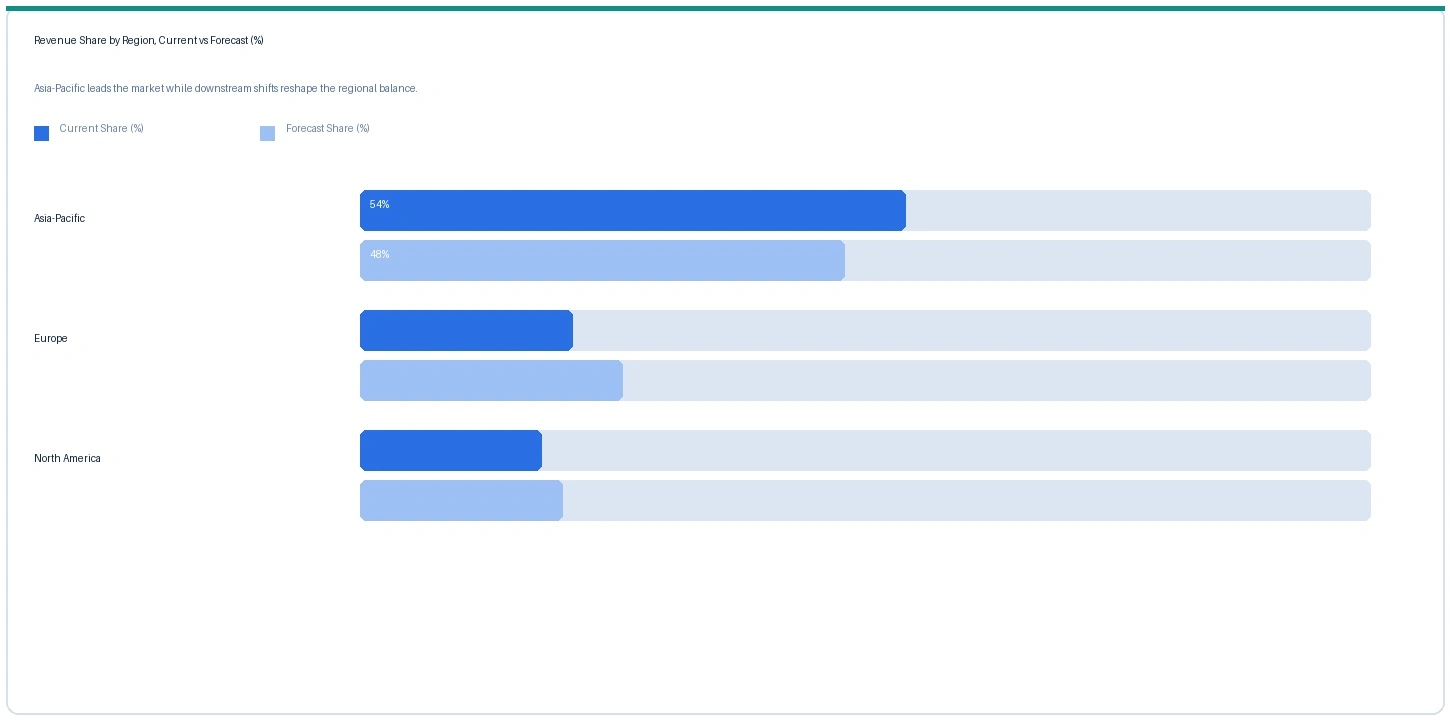

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive specialty coatings market in 2025. Based on regional analysis, the automotive specialty coatings market in Asia-Pacific accounted for largest revenue share in 2025. China's dominance in EV production at approximately 10 million BEV units in 2024 makes it the world's largest single-country market for EV motor insulating varnish and EV battery thermal management coatings, with Axalta Voltatex and BASF Voltasurf supplied to Chinese traction motor producers through their local distribution and direct account management operations. Japan contributes precision electric motor insulating varnish demand at Toyota, Honda, and Denso motor operations, with Hitachi Chemical and Elantas holding established insulating varnish qualification positions at Japanese traction motor OEM accounts.

Europe market accounted for second largest revenue share in the global automotive specialty coatings market in 2025. The market in Europe is expected to register the second largest revenue share. PPG Industries, BASF SE, and Axalta Coating Systems hold primary OEM qualification positions at European passenger car electrocoat, anti-corrosion, and specialty coating applications. BASF's March 2025 radar-transparent coating commercial qualification at European OEM bumper programmes and Axalta's Edison Award recognition for Voltatex electric motor insulating varnish confirm both companies' EV specialty coating strategy execution at European OEM programme level.

North America market is expected to register steady revenue growth in the global automotive specialty coatings market during the forecast period. The market in North America is anchored in OEM electrocoat anti-corrosion coatings at Ford, General Motors, Stellantis, and Toyota North American assembly operations, with PPG ENVIRO-PRIME and Axalta Aqua EC providing the primary electrocoat qualified products. Inflation Reduction Act EV manufacturing tax credits supporting battery assembly at Panasonic Kansas, Toyota Battery Manufacturing North Carolina, and Stellantis-Samsung SDI Indiana generate EV motor insulating varnish and battery thermal management coating demand as those facilities reach traction motor and battery pack assembly production between 2026 and 2028.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| EV Motor Insulating Varnish (Class H) | Europe | USD 72/kg | USD 66/kg | Rising | Axalta Voltatex ref |

| Battery Thermal Management Coating | Global | USD 54/kg | USD 50/kg | Rising | PPG / BASF ref |

| Radar-Transparent Clearcoat | Europe | USD 34/kg | USD 31/kg | Rising | BASF Schwarzheide ref |

| OEM Electrocoat (anti-corrosion) | North America | USD 5.60/kg | USD 5.20/kg | Stable | PPG ENVIRO-PRIME ref |

| Acoustic Damping Coating | Global | USD 8.40/kg | USD 7.80/kg | Stable | 3M / Henkel ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, OEM coating specification engineers, and specialty coating supplier commercial disclosures.

EV motor insulating varnish at Class H specification rose approximately 9.1% from USD 66 per kilogram in Q2 2025 to USD 72 per kilogram in Q2 2026, driven by above-plan EV traction motor production growth at Toyota, BYD, and Tesla that is tightening allocation from Axalta Voltatex and BASF Voltasurf qualified product ranges at European and Asian motor insulating varnish production operations. Battery thermal management coating rose approximately 8.0% to USD 54 per kilogram in Q2 2026 on ceramic filler cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which has partially restricted TiO2 and specialty aluminium oxide ceramic exports from GCC producers to European coating formulators. Radar-transparent clearcoat rose approximately 9.7% to USD 34 per kilogram in Europe on BASF commercial qualification success at European OEM bumper programmes pulling demand for qualified low-dielectric-constant resin and filler systems. OEM electrocoat anti-corrosion coating pricing is stable in North America at USD 5.60 per kilogram.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive specialty coatings market, the Hormuz disruption operates through titanium dioxide, specialty aluminium oxide, and ceramic precursor feedstock cost elevation at European specialty coating manufacturers. GCC chemical and mineral producers export TiO2 and ceramic precursors through Hormuz transit routes to European and Asian automotive specialty coating formulators, and the Hormuz closure has partially disrupted these export flows, adding approximately USD 180 to USD 320 per metric tonne to EV battery thermal management coating and radar-transparent clearcoat raw material costs at PPG, BASF, and Axalta European specialty coating production in Q2 2026. The secondary Hormuz impact is energy cost elevation at European OEM assembly operations from LNG price increases, reinforcing the commercial value of PPG ENVIRO-PRIME low-temperature cure electrocoat that reduces assembly energy consumption per vehicle.

Company Insights

The two key dominant companies in the automotive specialty coatings market are PPG Industries and BASF SE, recognised for their integrated OEM electrocoat anti-corrosion, radar-transparent ADAS coating, electric motor insulating varnish, and EV thermal management coating product portfolios spanning all automotive specialty coating applications at global OEM qualification levels.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 6.48 Billion |

| Market Size 2032 | USD 11.14 Billion |

| CAGR | 8.0% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Vehicle Type, By Application, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, France, UK, Japan, China, South Korea, India, Brazil, Mexico, Saudi Arabia |

| Companies Profiled | PPG Industries, BASF SE, Axalta Coating Systems, Henkel AG, 3M, AkzoNobel, Elantas Altana, Hitachi Chemical, Coating Technologies Group, Momentive, Dow |

| Key Data Sources | PPG Industries FY2024 annual report and ENVIRO-PRIME EV electrocoat product communications, BASF SE Schwarzheide radar-transparent coating qualification March 2025, Axalta FY2024 annual report and Edison Award Voltatex recognition Q1 2025, IEA Global EV Outlook 2025 motor production scenarios, OICA 2024 ADAS-equipped vehicle registration data, Axalta Q1 2025 earnings disclosure, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 264 |

| Published | Q2 2026 |

| SKU | NXC-AU-005 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 15 expert interviews conducted between January and May 2026 with EV motor insulating varnish product management and technical leads at Axalta and BASF, radar-transparent coating formulation and OEM qualification engineers at BASF Schwarzheide, OEM powertrain engineering specification leads at European EV traction motor producers, ADAS bumper assembly engineering leads at European premium OEM fascia production operations, and automotive electrocoat application engineers at PPG and AkzoNobel OEM account teams. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include PPG Industries FY2024 annual report and ENVIRO-PRIME EV electrocoat product communications, BASF SE Schwarzheide March 2025 radar-transparent coating qualification announcement, Axalta Coating Systems FY2024 annual report and Q1 2025 Edison Award and BIG Innovation Award Voltatex recognition disclosure, IEA Global EV Outlook 2025 traction motor production scenarios, OICA 2024 ADAS-equipped vehicle registration data at Level 2 and above penetration, Coating Technologies Group 2024 North America battery module ceramic coating qualification announcement, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.