Market Data

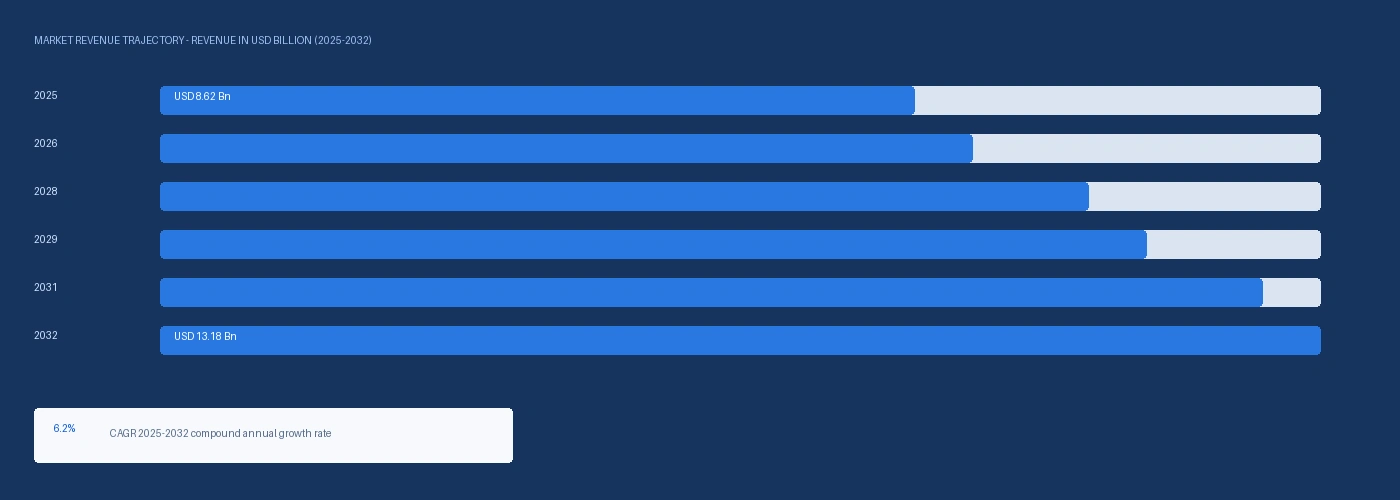

The global automotive sealants market size was USD 8.62 Billion in 2025 and is expected to register a revenue CAGR of 6.2% during the forecast period. Market revenue growth is supported by EV battery enclosure sealing demand from CATL, BYD, Toyota, and Volkswagen battery platforms requiring thermally conductive silicone and PU sealants with electrical insulation resistance and electrolyte chemical compatibility at IP67 water ingress protection specifications that command USD 28 to USD 46 per kilogram versus USD 6 to USD 12 per kilogram for conventional body-in-white seam sealants, Henkel LOCTITE SI 5950 silicone sealant availability for electric vehicles confirmed in August 2023, and Sika's Q4 2024 opening of a new adhesives and sealants manufacturing facility in Pune, India. Henkel AG reported its Adhesive Technologies division generated revenues of EUR 11.3 Billion in fiscal year 2024, with automotive sealants within its transportation adhesive and sealant category contributing as one of the highest-growth product lines on EV battery enclosure and lightweight body structure bonding demand. Sika AG reported record total revenues of CHF 11.76 Billion in fiscal year 2024 across its construction and industry segments, with its automotive sealant and adhesive business serving OEM body-in-white, glazing, and battery enclosure applications growing at above-plan rates in China and Europe on EV platform production ramp-up at BYD, SAIC, and Stellantis programmes. For instance, in Q1 2025, Henkel, Germany, announced a strategic partnership with a leading Chinese electric vehicle manufacturer to co-develop advanced adhesives and sealants for battery pack and lightweight structure applications, confirming Henkel's position as the primary EV-specific sealant development partner for Chinese OEM programmes. These are some of the key factors driving revenue growth of the market.

Silicone sealants account for approximately 34% to 38% of global automotive sealant revenue by product type, anchored by their use in automotive glazing bonding and sealing at windscreen and rear window installations and the growing EV battery enclosure application where Henkel LOCTITE SI 5950 and Dow SYLGARD silicone sealant formulations provide thermal cycling and electrical insulation performance that polyurethane and acrylic alternatives cannot achieve within EV specification limits. Polyurethane sealants represent the second-largest product segment at approximately 28% to 32% of total automotive sealant revenue, with reactive two-component PU systems from Sika, Bostik, and Dow used in direct glazing applications at OEM windscreen installation facilities. 3M launched a new range of automotive seam sealants in July 2024 targeting both OEM production body shops and refinish body shop applications, expanding its automotive sealant portfolio. Avery Dennison Corporation entered a partnership with Yiannimize in February 2025 for developing new automotive sealant ranges for North American consumers.

However, EV platform body architecture uses greater proportions of structural adhesive bonded aluminium and carbon fibre composite panels that reduce the number of body seam sealant application points below the equivalent ICE vehicle body manufacturing process. Automotive sealant production cost is affected by silicone monomer and polyurethane isocyanate feedstock cost volatility, with the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevating methanol and isocyanate precursor costs at European silicone sealant and PU sealant manufacturers, adding approximately USD 140 to USD 240 per metric tonne to automotive sealant active material cost in Q2 2026. These factors substantially limit automotive sealants market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EV battery pack enclosure sealing requires sealant performance specifications including electrical insulation resistance above 10 megaohms at 500 volts DC to prevent battery short-circuit through the sealant layer, thermal stability from minus 40 degrees Celsius to plus 180 degrees Celsius through battery thermal cycling, and electrolyte chemical resistance to lithium salt electrolyte formulations that degrade conventional acrylic and butyl sealants. Henkel's LOCTITE SI 5950 silicone sealant for EV applications, commercially available from August 2023, was specifically formulated to provide heat resistance, chemical resistance, vibration damping, and adhesion to aluminium housing and glass lid battery module substrates. Each BEV requires approximately 40 to 120 metres of battery enclosure perimeter sealant application at USD 28 to USD 46 per kilogram, generating USD 1,200 to USD 5,400 per vehicle of EV battery sealant content versus USD 80 to USD 160 per vehicle of conventional body-in-white seam sealant at OEM production rates. Sika's strategic partnership with ElringKlinger in Q3 2024 to co-develop high-performance gasket and sealant systems for electric powertrains combines Sika specialty sealant chemistry with ElringKlinger powertrain engineering for multi-material battery housing substrate compatibility. Sika India Expansion and Asia-Pacific OEM Production Growth Driving Automotive Sealant Volume Sika AG opened a new adhesives and sealants manufacturing facility in Pune, India in Q4 2024 to produce automotive sealants and adhesives for the rapidly growing Indian vehicle production market, where OICA confirmed Indian passenger vehicle production of approximately 5.8 million units in 2024 at a growth rate of approximately 8% year over year. Chinese OEM production expansion at BYD, SAIC, Geely, and Changan is driving EV-specific battery enclosure sealant demand in Asia-Pacific, with Henkel's Q1 2025 strategic partnership with a Chinese EV manufacturer for co-development of EV battery and lightweight structure sealants confirming the Chinese EV OEM market as the primary growth driver for Henkel's automotive sealant business in Asia-Pacific through 2028.

Electric vehicle body-in-white construction incorporates greater proportions of structural adhesive bonded aluminium multi-material panels that reduce the number of spot-weld flanges and body seam joints requiring sealant application compared to conventional all-steel ICE vehicle body construction, as structural adhesive bonding replaces the weld-flange seam sealant application that generates the majority of body-in-white seam sealant volume at conventional ICE production facilities. The structural adhesive displacement of seam sealant application points is estimated to reduce body-in-white seam sealant consumption by approximately 15% to 25% per EV platform versus equivalent ICE platform. Polyurethane isocyanate and silicone methanol feedstock cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has added approximately USD 140 to USD 240 per metric tonne to automotive sealant raw material cost at European Henkel and Sika production facilities. These factors substantially limit automotive sealants market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Silicone Sealants, Polyurethane Sealants, Epoxy Sealants, Acrylic Sealants, Butyl Sealants | Silicone Sealants |

| Application | Body-in-White, Powertrain and Drivetrain, Glazing, Battery Enclosure Sealing, Underbody Acoustic | Body-in-White |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles | Passenger Cars |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Silicone Sealants segment is expected to account for a significantly large revenue share in the global automotive sealants market during the forecast period.

This report evaluates product type across Silicone Sealants, Polyurethane Sealants, Epoxy Sealants, Acrylic Sealants, Butyl Sealants for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Body-in-White, Powertrain and Drivetrain, Glazing, Battery Enclosure Sealing, Underbody Acoustic for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

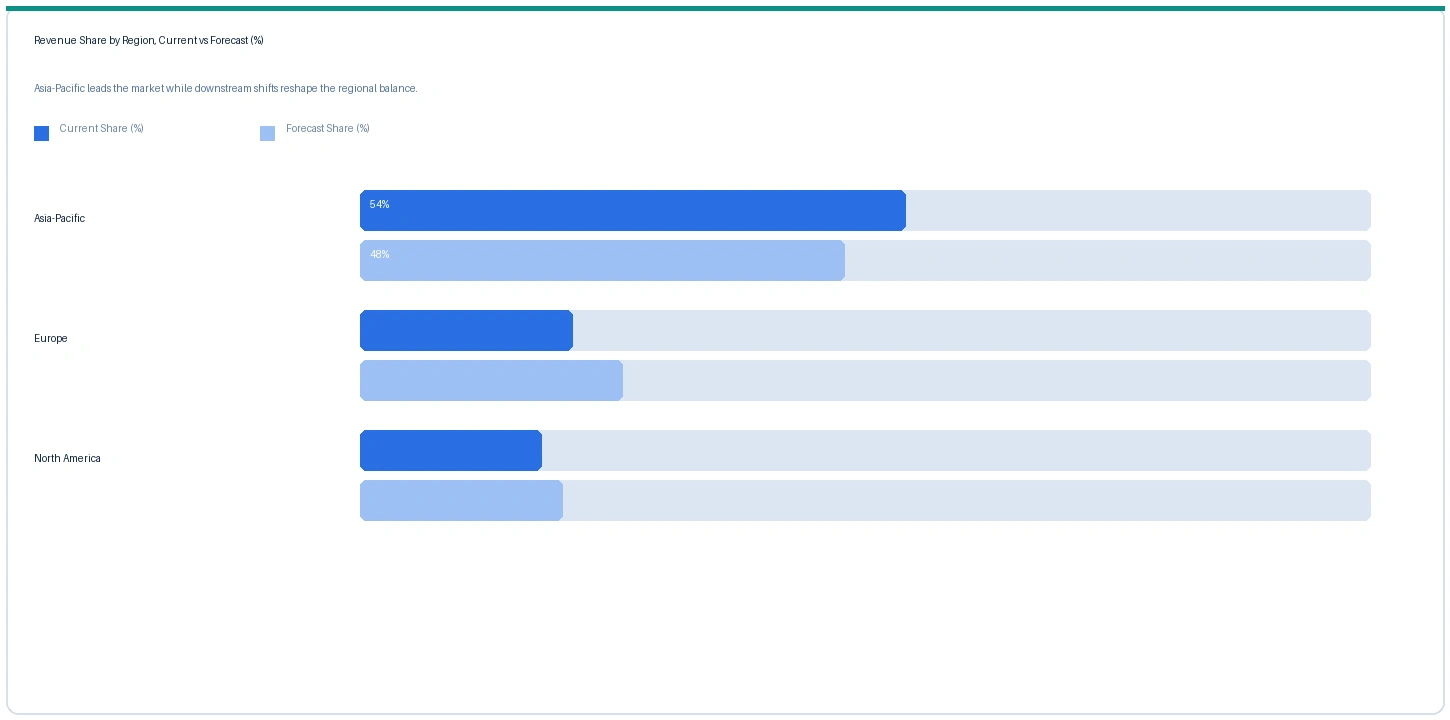

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive sealants market in 2025. Based on regional analysis, the automotive sealants market in Asia-Pacific accounted for largest revenue share in 2025. China's automotive production of approximately 31 million vehicles in 2024 per OICA, including the world's largest EV production volume at approximately 10 million BEV units, generates the largest single-country automotive sealant consumption base globally. Henkel's Q1 2025 strategic partnership with a Chinese EV OEM for co-development of EV battery and lightweight structure sealants and Sika's Q4 2024 Pune, India manufacturing facility opening confirm that both primary automotive sealant suppliers are investing in Asia-Pacific production and OEM partnership capacity.

The market in Europe is expected to register the second largest revenue share. Henkel Adhesive Technologies at Dusseldorf and Sika AG's European industrial division anchor the European automotive sealant supply market, with Henkel holding OEM qualification at Volkswagen, BMW, Mercedes-Benz, and Stellantis European vehicle production body-in-white and glazing operations and Sika holding direct glazing and body acoustic seam sealing positions at Toyota European Manufacturing and Ford Cologne.

North America market is expected to register steady revenue growth in the global automotive sealants market during the forecast period. The market in North America is anchored in body-in-white seam sealing at Ford, General Motors, Stellantis, and Toyota North American production facilities, with Henkel, 3M, and Sika the primary OEM qualified sealant suppliers. The Inflation Reduction Act battery manufacturing investment at Panasonic Kansas, Toyota Battery Manufacturing North Carolina, and Stellantis-Samsung SDI Indiana generates battery enclosure sealant demand from 2026 as those facilities reach battery pack assembly production.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| EV Battery Enclosure Silicone | Global | USD 38/kg | USD 35/kg | Rising | Henkel LOCTITE / Dow ref |

| Automotive Glazing PU Sealant | Europe | USD 14/kg | USD 13/kg | Rising | Sika Sikaflex ref |

| Body-in-White Seam Sealant | North America | USD 7.40/kg | USD 6.80/kg | Rising | Henkel / 3M ref |

| Underbody Acoustic Sealant | Europe | USD 5.20/kg | USD 4.80/kg | Stable | Bostik / BASF ref |

| Butyl Window Sealant (OEM) | Asia-Pacific | USD 4.60/kg | USD 4.20/kg | Stable | Toyota / Honda ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, OEM supply chain disclosures, and specialty chemical trade publication monitoring.

EV battery enclosure silicone sealant prices rose approximately 8.6% from USD 35 per kilogram in Q2 2025 to USD 38 per kilogram in Q2 2026, driven by silicone monomer and methanol feedstock cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, and by growing EV battery enclosure demand from BYD, CATL, Volkswagen, and Toyota BEV platform ramp-ups tightening allocation from the primary EV-qualified sealant formulation suppliers Henkel, Sika, and Dow. The EV battery enclosure-to-body-in-white sealant price premium of approximately USD 30.60 per kilogram in Q2 2026 reflects the electrical insulation, thermal cycling, and electrolyte resistance specification requirements. Automotive glazing PU sealant rose approximately 7.7% in Europe on isocyanate feedstock cost elevation, while body-in-white seam sealant in North America rose approximately 8.8% from USD 6.80 to USD 7.40 per kilogram on acrylic and polyurethane raw material cost increases.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive sealants market, the Hormuz disruption operates through two feedstock cost pathways. The primary pathway is polyurethane isocyanate cost elevation at European PU sealant producers: MDI and TDI isocyanate production in Saudi Arabia and UAE is exported through Hormuz transit routes to European and Asian automotive PU sealant manufacturers including Henkel at Dusseldorf and Sika at Zurzach, adding approximately USD 140 to USD 240 per metric tonne to European automotive PU and epoxy sealant raw material cost in Q2 2026. The secondary pathway is silicone monomer methanol cost elevation at silicone sealant producers, as methanol feedstock from GCC chemical plants to Shin-Etsu Chemical and Dow silicone monomer production has been partially disrupted, adding approximately USD 80 to USD 140 per metric tonne to EV battery enclosure silicone sealant compound cost.

Company Insights

The two key dominant companies in the automotive sealants market are Henkel AG and Sika AG, recognised for their integrated automotive sealant formulation, OEM qualification, and production service capabilities spanning body-in-white seam sealing, direct glazing, battery enclosure sealing, and powertrain sealant applications across global OEM vehicle production operations.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 8.62 Billion |

| Market Size 2032 | USD 13.18 Billion |

| CAGR | 6.2% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product Type, By Application, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Switzerland, China, Japan, South Korea, India, Brazil, Mexico, Saudi Arabia, UAE |

| Companies Profiled | Henkel LOCTITE Teroson, Sika AG, 3M, Bostik Arkema, Dow, BASF SE, H.B. Fuller, Huntsman, Permatex, Lord Corporation, Evonik, Momentive |

| Key Data Sources | Henkel AG FY2024 Adhesive Technologies EUR 11.3 Billion revenue, Sika AG FY2024 annual report CHF 11.76 Billion record revenue, Henkel LOCTITE SI 5950 product launch documentation August 2023, Sika Pune facility Q4 2024, CATL 2024 annual report battery module sealing specifications, OICA 2024 vehicle production statistics, IEA Global EV Outlook 2025, Dow USD 40 Million China expansion August 2023, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 260 |

| Published | Q2 2026 |

| SKU | NXC-AU-004 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 15 expert interviews conducted between January and May 2026 with automotive sealant product management and OEM key account managers at European and Asian sealant suppliers, EV battery enclosure sealant technical leads at Henkel and Sika, OEM body-in-white engineering and materials specification leads at European passenger car manufacturers, and EV battery module assembly quality engineers at Asian battery manufacturers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Henkel AG FY2024 annual report Adhesive Technologies EUR 11.3 Billion revenue data, Sika AG FY2024 annual report CHF 11.76 Billion record revenue and automotive industry segment data, Henkel LOCTITE SI 5950 EV silicone sealant product launch documentation August 2023, Sika Q4 2024 Pune manufacturing facility opening disclosure, Sika-ElringKlinger EV powertrain partnership announcement Q3 2024, Dow USD 40 Million China capacity expansion announcement August 2023, CATL 2024 annual report battery platform specifications, OICA 2024 global vehicle production data, IEA Global EV Outlook 2025, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.