Market Data

The global automotive rubber molding market size was USD 44.86 Billion in 2025 and is expected to register a revenue CAGR of 4.8% during the forecast period. Market revenue growth is supported by EV thermal management system silicone and FKM hose demand at CATL, BYD, and LG Energy Solution battery cooling circuit specifications exceeding EPDM temperature and chemical resistance limits, Freudenberg Sealing Technologies next-generation rubber gasket development for bio-based fuel compatibility confirmed in November 2024, and NOK Corporation high-precision rotary oil seal introduction for electric drivetrains at the Automotive Engineering Exposition 2024 in Yokohama. Freudenberg Group reported in its 2024 annual review that its Freudenberg Sealing Technologies division generated above-plan growth in EV thermal management sealing components, with automotive silicone and FKM hose and gasket demand from European and Asian EV platform programmes driving revenue growth that partially offset sequential decline in ICE powertrain rubber component volumes. NOK Corporation disclosed that its high-precision rotary oil seal for electric drivetrains launched at the Yokohama Automotive Engineering Exposition in July 2024 had been nominated for OEM qualification at five Asian EV platform programmes in China and South Korea. Trelleborg AB completed the acquisition of a mid-sized Asian rubber molding firm in September 2024 to strengthen production capacity in Southeast Asia. For instance, in November 2024, Freudenberg Sealing Technologies, Germany, announced the development of next-generation rubber gaskets with enhanced resistance to bio-based fuels and high-temperature environments, targeting European automakers testing B20 and B30 biodiesel blends and E85 ethanol content fuels where conventional NBR and EPDM gasket materials swell and degrade at accelerated rates. These are some of the key factors driving revenue growth of the market.

EPDM remains the largest volume rubber material at approximately 42% to 46% of total material consumption by volume, serving door seal strips, window channels, weatherstripping, cooling system hoses, and underbonnet sealing in ICE vehicles. Silicone rubber consumption in automotive applications is growing at the fastest rate by value, driven by EV battery cooling circuit coolant hose specifications requiring continuous operating temperature above 150 degrees Celsius and glycol coolant chemical resistance that EPDM at its 120 to 130 degree Celsius practical limit cannot consistently provide. FKM fluorocarbon rubber demand from EV drivetrain shaft seal and battery electrolyte containment applications is expanding at Freudenberg, NOK, and Trelleborg, with FKM at USD 22,000 to USD 28,000 per metric tonne representing the highest-value material in the automotive rubber molding portfolio. Cooper-Standard Automotive disclosed in its 2024 sustainability report that its FluidPower EV hose product line incorporating silicone and fluorosilicone formulations had secured OEM qualification at three North American EV battery cooling circuit programmes.

However, the structural shift from ICE to BEV powertrains reduces total rubber component content per vehicle at the powertrain level, as a battery electric vehicle incorporates approximately 35% to 45% fewer engine management and powertrain sealing rubber components than an equivalent ICE platform, partially offsetting the per-component value increase from EV-specific silicone and FKM specifications. Natural rubber commodity price volatility between USD 1,200 and USD 2,400 per metric tonne across the 2022 to 2025 period per International Rubber Study Group data creates production cost uncertainty at NR-based automotive rubber component manufacturers. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated synthetic rubber feedstock costs at EPDM and NBR producers, with propylene and acrylonitrile costs rising approximately USD 60 to USD 120 per metric tonne at European rubber compound manufacturers. These factors substantially limit automotive rubber molding market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Battery electric vehicle thermal management systems operate coolant circuits at up to 180 degrees Celsius peak with glycol-water coolant at concentrations that create hydrolysis degradation in standard EPDM hose formulations beyond the 120 to 130 degree practical temperature limit. CATL disclosed in its 2024 annual report that its CTP 3.0 battery platform required thermal management hose specifications at 165 degrees Celsius continuous operating temperature with Novec 7000 dielectric coolant compatibility for immersion-cooled battery module designs, specifications that require silicone rubber or fluorosilicone hose construction. The IEA confirmed approximately 17 million EV and PHEV units sold globally in 2024, with each BEV requiring an estimated 8 to 14 metres of thermal management hose per vehicle at average silicone hose value of USD 18 to USD 26 per metre. Trelleborg secured a major EV battery pack module sealing contract in January 2025 from a leading European EV manufacturer, confirming entry into the highest-value sealing specification tier in current automotive rubber programs. EV Drivetrain FKM Shaft Seal and Battery Electrolyte Containment Demand Growth EV drivetrain reduction gear and motor shaft seals require FKM fluorocarbon rubber formulations resistant to synthetic transmission fluids and coolant electrolyte environments at motor shaft locations that conventional ACM or NBR shaft seal materials are not chemically compatible with. NOK Corporation's July 2024 high-precision rotary oil seal for electric drivetrains, introduced at the Yokohama Automotive Engineering Exposition and nominated for qualification at five Asian EV OEM programmes, represents the first NOK product platform specifically designed for EV drivetrain shaft sealing with IP67 and IP68 ingress protection ratings combined with FKM chemical resistance. FKM at USD 22,000 to USD 28,000 per metric tonne generates approximately 10 to 15 times the revenue per kilogram of rubber consumed compared to EPDM at USD 1,840 to USD 2,260 per metric tonne, creating a revenue mix improvement at EV-focused rubber component manufacturers that offsets some of the powertrain rubber content reduction from ICE-to-BEV platform transitions.

A battery electric vehicle incorporates approximately 35% to 45% fewer powertrain and engine management rubber sealing components than an equivalent internal combustion engine platform, as the absence of an engine block, cylinder head gaskets, camshaft seals, injection system O-rings, exhaust rubber isolation mounts, and multiple coolant circuit hose connections removes rubber component content that generates above-average revenue per vehicle at EPDM and NBR rubber molding suppliers. Cooper-Standard Automotive disclosed in its 2024 investor communications that EV platform content per vehicle from its product portfolio was approximately 18% to 25% below equivalent ICE platform content. Natural rubber price volatility between USD 1,200 and USD 2,400 per metric tonne across 2022 to 2025 per International Rubber Study Group data creates production cost uncertainty for NR-based engine mounts and suspension bushings. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated propylene and acrylonitrile feedstock costs for EPDM and NBR synthetic rubber compound producers in Europe and Asia, adding approximately USD 60 to USD 120 per metric tonne to rubber compound material cost at European automotive molding plants. These factors substantially limit automotive rubber molding market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Sealing Products, Damping and Vibration Control, Hoses and Fluid Management, Gaskets and O-Rings | Sealing Products |

| Material | EPDM, NBR (Nitrile), Silicone, FKM (Fluorocarbon), NR (Natural Rubber) | EPDM |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles | Passenger Cars |

| Application | Powertrain, Body and Chassis, Interior and HVAC, Battery and EV Systems | Powertrain |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Sealing Products segment is expected to account for a significantly large revenue share in the global automotive rubber molding market during the forecast period.

This report evaluates product type across Sealing Products, Damping and Vibration Control, Hoses and Fluid Management, Gaskets and O-Rings for rubber & elastomers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates material across EPDM, NBR (Nitrile), Silicone, FKM (Fluorocarbon), NR (Natural Rubber) for rubber & elastomers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles for rubber & elastomers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Powertrain, Body and Chassis, Interior and HVAC, Battery and EV Systems for rubber & elastomers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for rubber & elastomers, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

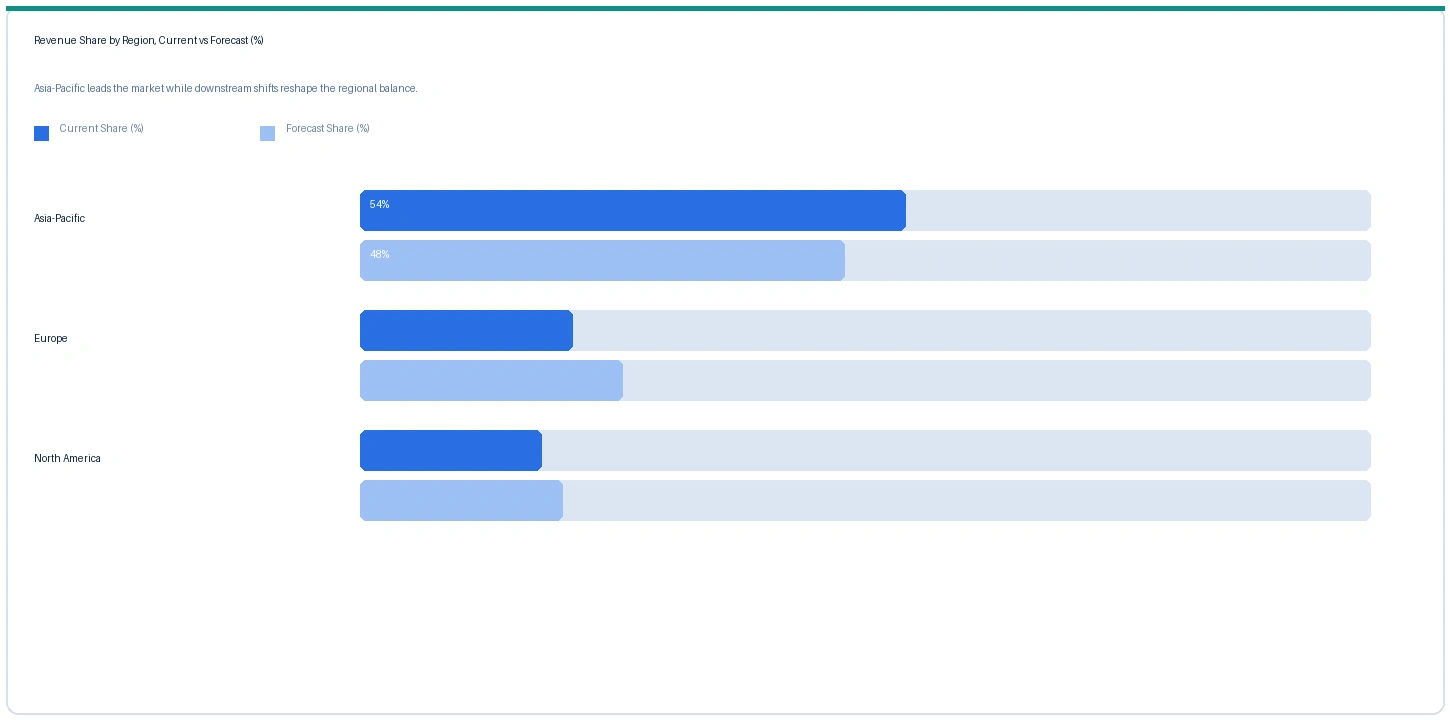

Regional Insights

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive rubber molding market in 2025. Based on regional analysis, the automotive rubber molding market in Asia-Pacific accounted for largest revenue share in 2025. Japan's NOK Corporation is the world's largest automotive rubber sealing product manufacturer, with annual sealing product revenues contributing approximately 12% of the global automotive rubber molding revenue, produced at NOK facilities in Japan, Thailand, and China. China's Zhongding Group has emerged as the largest Chinese domestic rubber molding supplier, with automotive sealing and hose product revenues estimated above USD 1.8 Billion in 2024 serving domestic Chinese OEM programmes. Sumitomo Riko Company supplies automotive anti-vibration rubber mounts, hoses, and sealing components to Toyota Motor Corporation under sole-source and preferred supplier arrangements at Toyota global production operations.

Europe market accounted for second largest revenue share in the global automotive rubber molding market in 2025. The market in Europe is expected to register the second largest revenue share. Freudenberg Sealing Technologies at Weinheim, Germany and ElringKlinger at Dettingen, Germany are the primary European advanced automotive sealing manufacturers, with Freudenberg holding qualification positions at Volkswagen, BMW, Mercedes-Benz, and Stellantis for powertrain, battery enclosure, and thermal management rubber sealing applications. Continental AG's ContiTech division produces automotive EPDM hoses, damping products, and sealing components at its Hanover manufacturing operations. ElringKlinger disclosed in its fiscal year 2024 results that EV-specific sealing and thermal management rubber components were growing above plan, driven by Volkswagen Group MEB platform battery enclosure sealing nominations.

North America market is expected to register steady revenue growth in the global automotive rubber molding market during the forecast period. The market in North America is anchored in Cooper-Standard Automotive at Novi, Michigan, Trelleborg at its North American operations, and Parker Hannifin at its O-ring and sealing product divisions. Cooper-Standard disclosed that its FluidPower EV hose product line had secured OEM qualification at three North American EV battery cooling circuit programmes in 2024, representing the first Cooper-Standard EV-specific product line revenue generation from silicone and fluorosilicone thermal management hose.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| EPDM Compound (auto grade) | Europe | USD 2,140/MT | USD 1,980/MT | Rising | ContiTech / Freudenberg ref |

| Silicone Rubber (EV hose grade) | Global | USD 8,640/MT | USD 7,960/MT | Rising | EV thermal mgmt ref |

| FKM Compound (shaft seal grade) | Europe | USD 24,800/MT | USD 22,600/MT | Rising | NOK / Freudenberg ref |

| NBR Compound (O-ring grade) | Asia-Pacific | USD 1,840/MT | USD 1,680/MT | Stable | Chinese producer ref |

| NR (SMR 20 grade, feedstock) | Global | USD 1,640/MT | USD 1,580/MT | Stable | IRSG benchmark |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, rubber compound producer commercial disclosures, and automotive parts trade publication monitoring.

EPDM automotive compound prices rose approximately 8.1% in Europe from USD 1,980 per metric tonne in Q2 2025 to USD 2,140 per metric tonne in Q2 2026, driven by propylene feedstock cost elevation of approximately USD 60 to USD 120 per metric tonne from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which has partially restricted GCC propylene exports to European EPDM producers. Silicone rubber for EV thermal management hose grade rose approximately 8.5% from USD 7,960 per metric tonne in Q2 2025 to USD 8,640 per metric tonne in Q2 2026, driven by above-plan EV battery cooling circuit hose demand growth and by silicone monomer cost elevation from methanol feedstock cost increases. FKM fluorocarbon rubber compound prices rose approximately 9.7% from USD 22,600 per metric tonne in Q2 2025 to USD 24,800 per metric tonne in Q2 2026 on EV drivetrain shaft seal specification growth at NOK, Freudenberg, and Trelleborg, where FKM supply from Chemours, Solvay, and Daikin is the upstream concentration point for a market segment where EV specification pull is growing faster than FKM production capacity additions. NBR compound pricing in Asia-Pacific is stable from Chinese domestic acrylonitrile production partially insulating Asian NBR producers from GCC feedstock disruption, while NR benchmark pricing is stable reflecting balanced Thai and Indonesian production supply against global automotive and industrial demand.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive rubber molding market, the Hormuz disruption operates through EPDM and NBR synthetic rubber feedstock cost elevation. Propylene and acrylonitrile feedstock for EPDM and NBR rubber compound production are partially sourced from GCC petrochemical complexes, and the Hormuz closure has partially restricted these exports to European and Asian rubber compound manufacturers, adding approximately USD 60 to USD 120 per metric tonne to EPDM and NBR compound production cost in Q2 2026. The secondary impact is silicone monomer cost elevation through methanol feedstock disruption affecting silicone compound production at Shin-Etsu Chemical and Dow Silicones, adding approximately USD 400 to USD 680 per metric tonne to silicone rubber compound cost in Q2 2026.

Company Insights

The two key dominant companies in the automotive rubber molding market are NOK Corporation and Freudenberg Sealing Technologies, recognised for their integrated rubber compound development, precision molding, and OEM qualification capabilities spanning EPDM body sealing, FKM drivetrain shaft seals, silicone EV thermal management hoses, and battery enclosure sealing across global OEM passenger car, commercial vehicle, and EV platform programmes.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 44.86 Billion |

| Market Size 2032 | USD 62.14 Billion |

| CAGR | 4.8% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product Type, By Material, By Vehicle Type, By Application, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, France, Japan, China, South Korea, India, Thailand, Brazil, Sweden, UK |

| Companies Profiled | NOK Corporation, Freudenberg Sealing Technologies, Trelleborg AB, Cooper-Standard, Sumitomo Riko, ContiTech, ElringKlinger, Hutchinson, Toyoda Gosei, Zhongding Group, Gates, Parker Hannifin |

| Key Data Sources | Freudenberg Group FY2024 annual review, NOK Corporation product launch disclosures, Trelleborg AB FY2024 annual report and Asia acquisition announcement, Cooper-Standard Automotive FY2024 sustainability report, CATL 2024 annual report battery platform disclosures, IEA Global EV Outlook 2025, International Rubber Study Group NR price data, ElringKlinger FY2024 annual results EV sealing data, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 264 |

| Published | Q2 2026 |

| SKU | NXC-AU-003 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 16 expert interviews conducted between January and May 2026 with rubber compound materials engineers at automotive sealing component manufacturers, FKM and silicone compound procurement leads at European and Asian Tier 1 sealing suppliers, OEM EV battery thermal management systems engineers at European and Asian automotive OEMs, and chassis engineering procurement leads at North American light vehicle platforms. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Freudenberg Group FY2024 annual review Sealing Technologies division disclosures, NOK Corporation product launch and OEM nomination disclosures, Trelleborg AB FY2024 annual report and September 2024 Asian acquisition announcement, Cooper-Standard Automotive FY2024 sustainability report FluidPower EV hose qualifications, CATL 2024 annual report CTP 3.0 platform thermal management specifications, IEA Global EV Outlook 2025, International Rubber Study Group 2024 natural rubber price and production data, ElringKlinger FY2024 annual results EV sealing revenue disclosures, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.