Market Data

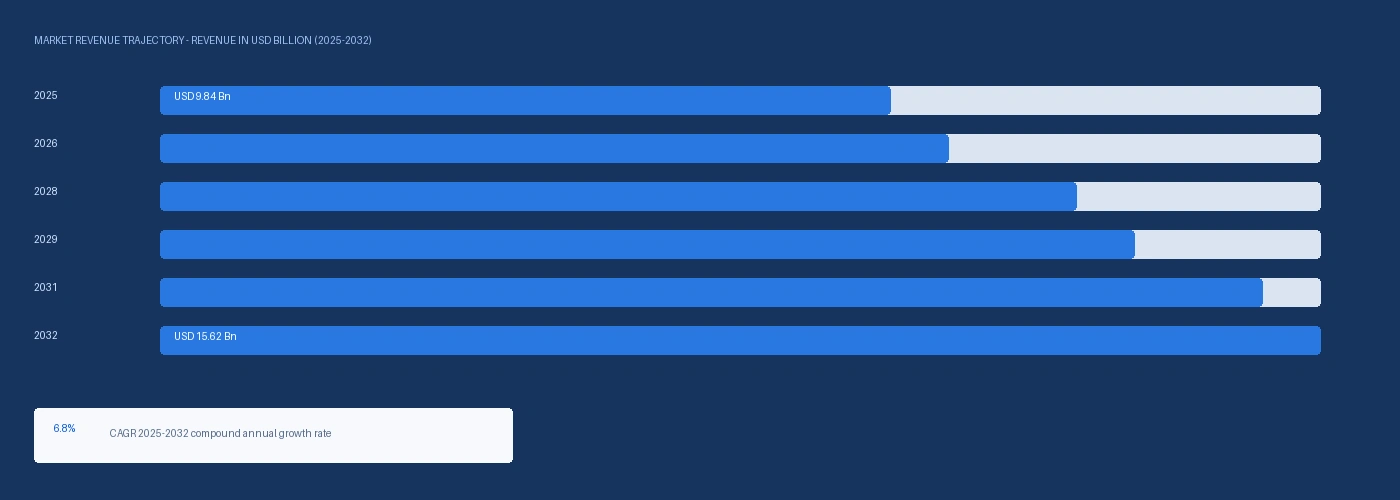

The global automotive refinish coating market size was USD 9.84 Billion in 2025 and is expected to register a revenue CAGR of 6.8% during the forecast period. Market revenue growth is supported by rising vehicle collision rates in emerging Asian markets where vehicle fleet growth outpaces road safety infrastructure investment, regulatory VOC emission limits converting European and North American body shops from solventborne to premium waterborne refinish systems at above-solventborne price points, and the Axalta acquisition of The CoverFlexx Group in 2024 and its announced merger with AkzoNobel restructuring the global refinish distribution landscape. Axalta Coating Systems reported record full year 2024 refinish net sales, with Q4 2024 Refinish net sales at USD 545 Million growing 2% year over year driven by CoverFlexx acquisition contributions and net new body shop wins per Axalta Q4 2024 earnings disclosure. AkzoNobel, in a merger agreement announced in 2025 combining its Sikkens, Lesonal, and Wanda refinish brands with Axalta's Cromax, Standox, Spies Hecker, and Nason brands into a combined platform targeting late 2026 to early 2027 close, creates the world's largest automotive refinish coating supplier with estimated refinish revenues above USD 3.2 Billion. PPG Industries reported mid-single-digit organic sales growth in automotive refinish coatings across global markets in its 2024 annual results, with its Deltron, Envirobase, and Vibrance waterborne refinish systems gaining body shop specification positions in European and North American markets. For instance, in Q2 2024, Axalta Coating Systems, United States, completed its acquisition of The CoverFlexx Group from Transtar Holding Company for initial cash consideration of USD 285 Million, expanding its North American refinish portfolio into the economy body shop customer segment with the Transtar Autobody Technologies, Pro Form, and Aftermkt Armor product brands, adding full primer, basecoat, clearcoat, aerosol, filler, bedliner, and detailing product coverage of the North American economy refinish range. These are some of the key factors driving revenue growth of the market.

Waterborne refinish systems now account for approximately 58% of global automotive refinish coating revenue in 2025, with European regulatory VOC limits under EU Directive 2004/42/CE restricting solventborne clearcoat VOC content below 420 grams per litre, driving mandatory conversion that has pushed waterborne adoption to above 85% of European body shop paint volume. Axalta's Nimbus waterborne mixing system, targeting rollout to over 40,000 body shop locations globally by end 2026 per CFO Carl Anderson's Q2 2025 earnings communication, represents the most ambitious waterborne digital mixing platform expansion in the refinish industry's history, automating formula retrieval and waterborne paint preparation at the body shop level in a way that creates Axalta formula dependency at converted locations. BASF SE's Glasurit waterborne refinish system continues to hold preferred supplier positions at premium vehicle brand authorised body shop networks including Mercedes-Benz approved repairers and BMW Group authorised service centres, where Glasurit 90-Line waterborne clearcoat is specified in OEM body shop approval documentation. PPG Envirobase waterborne system holds preferred repairer agreements with seven of the top ten US insurance companies, making Envirobase system specification a prerequisite for inclusion in those insurers' preferred shop networks at approximately 4,200 PPG-system body shops across North America.

However, automotive body shop consolidation is reducing the number of independent buying decisions in the refinish channel, with Caliber Collision operating approximately 1,800 locations and Service King approximately 340 locations across North America under centralised paint supplier contracts that reduce the ability of coating suppliers to compete for individual body shop specification. Axalta Q2 2025 earnings disclosed Refinish net sales declined 6% year over year predominantly driven by organic decline in North America, confirming US collision industry demand softness from reduced collision claims volumes. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated acrylic resin, polyurethane hardener, and titanium dioxide feedstock costs for waterborne refinish coating manufacturers, adding approximately USD 180 to USD 320 per metric tonne to waterborne clearcoat production cost in Q2 2026. These factors substantially limit automotive refinish coating market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

The announced merger between AkzoNobel N.V. and Axalta Coating Systems, expected to close in late 2026 to early 2027, creates a combined coatings platform with FY2024 revenues of USD 16.9 Billion. The combined Refinish portfolio encompasses Axalta's Cromax, Standox, Spies Hecker, and Nason brands alongside AkzoNobel's Sikkens, Lesonal, and Wanda brands, giving the combined entity an estimated 30% to 35% global refinish market revenue share. Axalta's Nimbus digital waterborne mixing platform targeting 40,000 body shop locations by end 2026, combined with AkzoNobel's Automix digital colour matching system at European body shop networks, creates a combined digital platform presence that independent body shops converting to waterborne systems will encounter as a single supplier alternative post-merger. AkzoNobel reported Refinish as one of its highest-margin performance coatings sub-segments in its 2024 investor day presentation, with Sikkens and Lesonal maintaining premium specification positions at authorised BMW, Audi, and Mercedes-Benz body shop networks. Waterborne Regulatory Conversion and Insurance Preferred Repairer Programmes Driving Premium System Specification EU Directive 2004/42/CE VOC limits and equivalent regulations in the US, Canada, Japan, and South Korea are converting body shops from solventborne to waterborne refinish systems at above-entry-level price points. Waterborne clearcoat at USD 48 to USD 62 per litre represents a 35% to 55% premium above equivalent solventborne products but satisfies VOC compliance requirements that expose non-compliant body shops to operating permit suspension. Insurance company preferred repairer programmes in the US, UK, Germany, and Australia, where insurers negotiate volume-committed paint supplier rates with major body shop chains in exchange for referral volume, are driving system-level waterborne refinish conversion at consolidating body shop operators.

Caliber Collision at approximately 1,800 North American locations and Service King at approximately 340 locations operate centralised paint supplier contracts that concentrate buying power at the DSO corporate procurement level where paint price per litre is negotiated against volume commitments that individual body shops cannot match. Axalta's Q2 2025 Refinish net sales decline of 6% year over year predominantly in North America confirms that the US collision environment has moved to lower collision claim volumes per insured vehicle, driven by advanced driver assistance system adoption reducing accident frequency at newer vehicle vintages. Acrylic resin and polyurethane hardener feedstock cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has added approximately USD 180 to USD 320 per metric tonne to waterborne clearcoat production cost in Q2 2026. These factors substantially limit automotive refinish coating market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Technology | Waterborne, Solventborne, UV-Cure, Powder Coating | Waterborne |

| Product | Primer, Basecoat, Clearcoat, Filler and Sealer | Primer |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles | Passenger Cars |

| End Use | Independent Body Shops, Dealer-Operated Body Shops, Fleet and Commercial Operators | Independent Body Shops |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Waterborne segment is expected to account for a significantly large revenue share in the global automotive refinish coating market during the forecast period.

This report evaluates technology across Waterborne, Solventborne, UV-Cure, Powder Coating for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates product across Primer, Basecoat, Clearcoat, Filler and Sealer for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Independent Body Shops, Dealer-Operated Body Shops, Fleet and Commercial Operators for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for coatings & resins, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

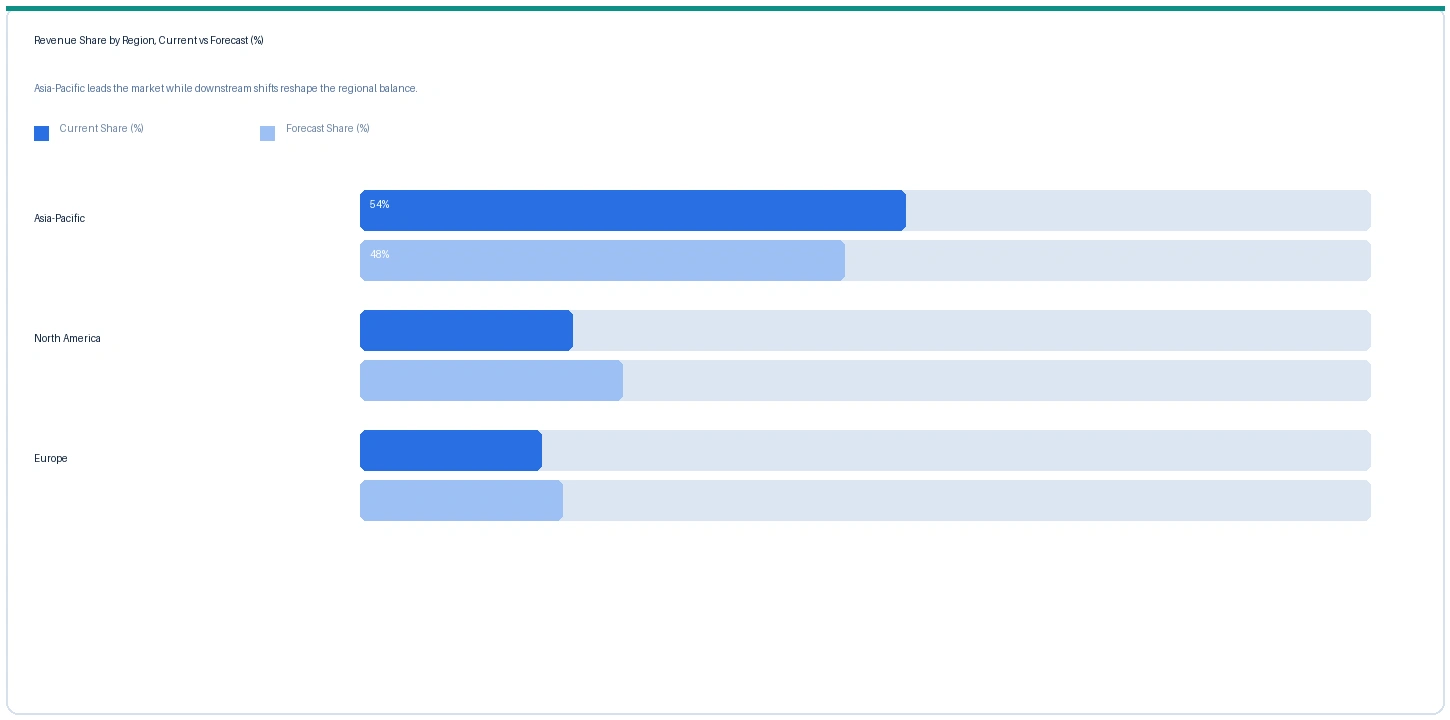

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive refinish coating market in 2025. Based on regional analysis, the automotive refinish coating market in Asia-Pacific accounted for largest revenue share in 2025. China's vehicle fleet of approximately 340 million registered vehicles in 2024 generates the world's largest collision repair volume by absolute unit count, with Nippon Paint Holdings, Kansai Paint, and Chinese local brands holding significant body shop specification positions alongside Axalta and PPG Western brand systems at premium tier repair operators. Japan's vehicle refinish market is served by Nippon Paint, Kansai Paint, and BASF Glasurit through domestic distribution at Toyota and Honda authorised body shops.

North America market accounted for second largest revenue share in the global automotive refinish coating market in 2025. The market in North America is expected to register the second largest revenue share. Axalta Performance Coatings Refinish at approximately USD 2.1 Billion annual North American revenue anchors the market, with PPG Refinish at approximately USD 1.4 Billion and BASF Glasurit at approximately USD 480 Million North American revenue providing the primary competition at premium body shop specification level. Axalta's Nimbus digital mixing platform targeting 40,000 global locations by end 2026 and the CoverFlexx Group acquisition expanding its economy segment coverage are the primary North American competitive dynamics in the 2024 to 2026 period.

Europe market is expected to register the third largest revenue share in the global automotive refinish coating market during the forecast period. The market in Europe is the technology origin and regulatory driver for waterborne refinish conversion, with EU Directive 2004/42/CE compliance at European body shops confirmed above 85% waterborne adoption. Axalta Standox and Spies Hecker, AkzoNobel Sikkens and Lesonal, and BASF Glasurit hold the primary European premium body shop specifications, with the pending AkzoNobel-Axalta merger set to consolidate the European premium specification market into a single entity with estimated 38% to 42% European refinish revenue share post-close.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Waterborne Clearcoat (2K premium) | Europe | USD 58/litre | USD 54/litre | Rising | BASF Glasurit / Axalta ref |

| Waterborne Clearcoat (2K premium) | North America | USD 52/litre | USD 48/litre | Rising | PPG Envirobase ref |

| Solventborne Clearcoat (2K) | North America | USD 38/litre | USD 35/litre | Stable | Economy segment ref |

| Waterborne Basecoat (mixing) | Europe | USD 44/litre | USD 41/litre | Rising | Axalta Cromax ref |

| UV-Cure Clearcoat | North America | USD 68/litre | USD 63/litre | Rising | Fast-cure premium ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, body shop procurement interviews, and coating manufacturer commercial disclosures. Automotive refinish coatings are traded under body shop supply agreements and preferred repairer contracts. Prices vary by technology, brand specification tier, volume commitment, and region.

Premium waterborne clearcoat prices rose approximately 7.4% in Europe and 8.3% in North America in Q2 2026 against Q2 2025, driven by acrylic resin and polyurethane hardener feedstock cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which has restricted GCC isocyanate and acrylate monomer exports and elevated waterborne clearcoat raw material costs by approximately USD 180 to USD 320 per metric tonne. The waterborne-to-solventborne clearcoat price premium of approximately USD 20 per litre in North American markets in Q2 2026 reflects the regulatory compliance value, scratch resistance performance advantage, and Axalta and PPG brand premium at insurance preferred repairer body shops where waterborne system specification is a programme participation requirement. UV-cure clearcoat rose approximately 7.9% to USD 68 per litre in North America on demand pull from DSO body shop chain throughput optimisation programmes.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive refinish coating market, the Hormuz disruption affects production economics through acrylic resin, polyurethane isocyanate hardener, and titanium dioxide feedstock cost elevation. GCC petrochemical producers export acrylate monomers and isocyanate precursors through Hormuz transit routes to European and Asian waterborne refinish coating manufacturers, and the Hormuz closure has partially disrupted these export flows, adding approximately USD 180 to USD 320 per metric tonne to waterborne clearcoat production cost in Q2 2026 and contributing to Q2 2026 waterborne clearcoat price increases of approximately 7% to 8% in European and North American body shop markets against Q2 2025 levels.

Company Insights

The two key dominant companies in the automotive refinish coating market are Axalta Coating Systems and PPG Industries, recognised for their integrated waterborne refinish system platforms spanning colour databases, digital mixing technology, OEM authorised body shop programmes, and preferred repairer insurance company contracts, with combined global refinish revenue representing approximately 35% to 40% of total market revenue.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 9.84 Billion |

| Market Size 2032 | USD 15.62 Billion |

| CAGR | 6.8% |

| Units | Revenue in USD Billion |

| Segments Covered | By Technology, By Product, By Vehicle Type, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Netherlands, Japan, China, South Korea, India, Brazil, Mexico, UAE, Saudi Arabia |

| Companies Profiled | Axalta, PPG Industries, BASF Glasurit, AkzoNobel, Sherwin-Williams, Nippon Paint, Kansai Paint, 3M, Henkel, Mipa Paints |

| Key Data Sources | Axalta Q4 2024 and Q2 2025 earnings disclosures, Axalta-AkzoNobel merger announcement 2025, PPG Industries FY2024 annual report, BASF SE Glasurit product communications, American Coatings Association waterborne adoption data, EU Directive 2004/42/CE VOC limit regulatory framework, European Automobile Manufacturers Association 2024 production data, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 268 |

| Published | Q2 2026 |

| SKU | NXC-AU-002 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 16 expert interviews conducted between January and May 2026 with body shop owners and paint procurement managers at European and North American independent and DSO collision repair operators, insurance company preferred repairer programme administrators, refinish coating product managers and commercial directors at coating manufacturers, and distribution and mixing system technology leads at Axalta and PPG. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Axalta Coating Systems Q4 2024 and Q2 2025 earnings releases, Axalta-AkzoNobel merger announcement and Form 425 filings 2025, Axalta CoverFlexx acquisition announcement 2024, PPG Industries FY2024 annual report and quarterly earnings releases, BASF SE Glasurit product and sustainability communications, American Coatings Association waterborne coating adoption data, EU Directive 2004/42/CE VOC emission limits for vehicle refinishing activities, European Automobile Manufacturers Association 2024 vehicle production and registration data, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.