Market Data

The global automotive piezoelectric fuel injectors market size was USD 786.8 Million in 2025 and is expected to register a revenue CAGR of 5.3% during the forecast period. Market revenue growth is supported by Euro 7 and China 7 emission standard timelines compelling OEM engine programme managers to specify piezoelectric injectors capable of eight or more injection events per cycle for precise particulate matter and NOx reduction below regulatory thresholds that solenoid injector platforms cannot consistently achieve, hybrid powertrain adoption driving above-average GDI piezoelectric injector content at Toyota, Hyundai, and BYD engine platforms, and CRDI diesel truck applications at Cummins, Volvo Trucks, and Daimler Trucks where common rail pressures above 2,500 bar mandate piezoelectric actuator response characteristics unavailable from solenoid designs. Bosch confirmed in its 2024 Powertrain Solutions investor briefing that its piezoelectric diesel injectors were installed in 38 million vehicles in service globally, with the CRS5 common rail system supporting injection pressures up to 2,700 bar across six to eight injection events per cycle in Euro VI and China VI commercial vehicle programmes. Continental AG expanded its European manufacturing facility in August 2025 to increase Direct Drive Piezo Injector production, adding 40,000 units of monthly capacity and creating 150 specialised engineering positions, the largest single European piezoelectric injector capacity addition since 2019. PHINIA Inc., which holds the Delphi Technologies powertrain fuel systems portfolio, confirmed in April 2024 the commercial availability of its 500-bar high-pressure GDI piezoelectric injector system for Changan Auto hybrid vehicle programmes in China. For instance, in April 2024, Delphi Technologies (PHINIA), United States, introduced its Hydraulic Drive Piezo Injector series specifically designed for Euro 7 compliant engines, demonstrating a 22% reduction in cold-start particulate emissions across 12 distinct vehicle platforms and qualifying for BMW, Volkswagen, and Stellantis engine programme specifications requiring sub-50 microgram per kilometre particulate number compliance. These are some of the key factors driving revenue growth of the market.

Continental's 2024 introduction of precision piezoelectric injectors capable of eight injection events per cycle improved combustion responsiveness by approximately 14% and reduced thermal emissions at customer OEM validation testing. The global diesel common rail injection system market was anchored at USD 22.6 Billion in 2024 per GMInsights, with piezoelectric units representing the premium specification tier capturing approximately 35% to 40% of CRDI system unit value at OEM programme price points of USD 18 to USD 38 per injector versus USD 8 to USD 16 for equivalent solenoid CRDI units. Stanadyne unveiled the performance aftermarket's first high-pressure port fuel injection system targeting 50 to 100 bar delivery for high-output gasoline engines in December 2023, expanding the piezoelectric-adjacent GDI technology platform into the North American performance aftermarket channel. Kyocera Corporation disclosed in its fiscal year 2024 annual report that its piezoelectric actuator ceramic component sales had grown at above-plan rates in the automotive segment, reflecting OEM design-in activity for 2025 to 2027 model year engine programmes specifying piezoelectric injector technology.

However, the accelerating EV adoption trajectory documented by the IEA at approximately 17 million EV and plug-in hybrid units sold in 2024, representing approximately 18% of global passenger vehicle production, is creating a structural long-term headwind for piezoelectric fuel injector market volume growth as battery-electric powertrains generate zero fuel injector demand per vehicle. Euro 7 regulation compliance timelines for gasoline GDI engines require piezoelectric GDI injectors capable of late injection strategies, creating a regulatory compliance certification cost of approximately EUR 2 to EUR 4 million per injector family calibration that disadvantages smaller OEM-adjacent Tier 1 suppliers who lack the engine test bench and calibration software infrastructure of Bosch, Continental, and PHINIA. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated piezoelectric ceramic raw material costs through zirconium and barium titanate feedstock cost increases at lead zirconate titanate PZT ceramic producers in China and Japan, adding approximately USD 8 to USD 14 per injector unit to piezoelectric stack production cost in Q2 2026 relative to the 2024 baseline. These factors substantially limit automotive piezoelectric fuel injectors market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Euro 7, applicable to new passenger car type approval from July 2025 in the EU, introduces on-road particulate number limits of 1x10^11 per kilometre and ambient temperature NOx test cycles extending to minus 10 degrees Celsius that solenoid injector platforms with their 1 to 3 millisecond response time cannot satisfy through conventional injection strategies. Piezoelectric injectors with sub-100 microsecond response times can deliver eight or more precisely timed injection events per engine cycle, enabling pilot, pre, main, post, and after injection strategies that suppress NOx formation while preventing particulate formation through late injection combustion temperature management. OICA confirmed global passenger vehicle production of approximately 92 million units in 2024, with approximately 72% incorporating ICE or hybrid powertrains representing the addressable vehicle population for piezoelectric injector specification. BMW Group, Volkswagen AG, and Stellantis have confirmed piezoelectric GDI injector specifications in their Euro 7 compliant engine families, with Bosch CRS5 and Continental Direct Drive piezoelectric GDI confirmed as the primary qualified injector families across these OEM Euro 7 engine programmes. Hybrid Powertrain Adoption Increasing Piezoelectric GDI Injector Content at Toyota and Hyundai Platforms Toyota Motor Corporation confirmed global hybrid vehicle sales of approximately 3.4 million units in fiscal year 2024, with its fourth-generation Hybrid System incorporating 2.5-litre and 2.0-litre Atkinson-cycle GDI engines specifying Denso piezoelectric GDI injectors at 200-bar injection pressure. Hyundai Motor Group confirmed in its 2024 annual report that its TMED hybrid system GDI engine platform used piezoelectric GDI injectors from Bosch and Continental for the ultra-lean combustion strategy enabling WLTP-certified fuel consumption of 5.2 to 5.8 litres per 100 kilometres. Each hybrid vehicle incorporating piezoelectric GDI generates content value of USD 120 to USD 220 per vehicle for the injector set, versus USD 60 to USD 90 for solenoid GDI equivalents, generating the per-unit revenue premium that drives above-market revenue growth in the piezoelectric segment.

Battery electric vehicles generate zero fuel injector demand per vehicle, and the IEA-confirmed 17 million EV and PHEV units in 2024 at approximately 18% of global passenger vehicle production represents a structural and growing offset to piezoelectric injector unit demand growth from ICE and hybrid platform specifications. Euro 7 GDI calibration certification costs at approximately EUR 2 to EUR 4 million per injector family at each OEM combustion lab validation cycle create a barrier that limits the number of qualified piezoelectric GDI injector suppliers in Euro 7 programmes to those with integrated engine test bench infrastructure, favouring Bosch, Continental, and PHINIA over independent Tier 2 manufacturers. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated zirconium-based PZT ceramic raw material costs, adding approximately USD 8 to USD 14 per injector unit to piezoelectric stack production cost in Q2 2026. These factors substantially limit automotive piezoelectric fuel injectors market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Injection System | GDI (Gasoline Direct Injection), CRDI (Common Rail Diesel), Dual-Fuel Systems | GDI (Gasoline Direct Injection) |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Hybrid Powertrains | Passenger Cars |

| Sales Channel | OEM, Aftermarket | OEM |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

CRDI segment is expected to account for a significantly large revenue share in the global automotive piezoelectric fuel injectors market during the forecast period.

This report evaluates injection system across GDI (Gasoline Direct Injection), CRDI (Common Rail Diesel), Dual-Fuel Systems for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Hybrid Powertrains for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates sales channel across OEM, Aftermarket for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

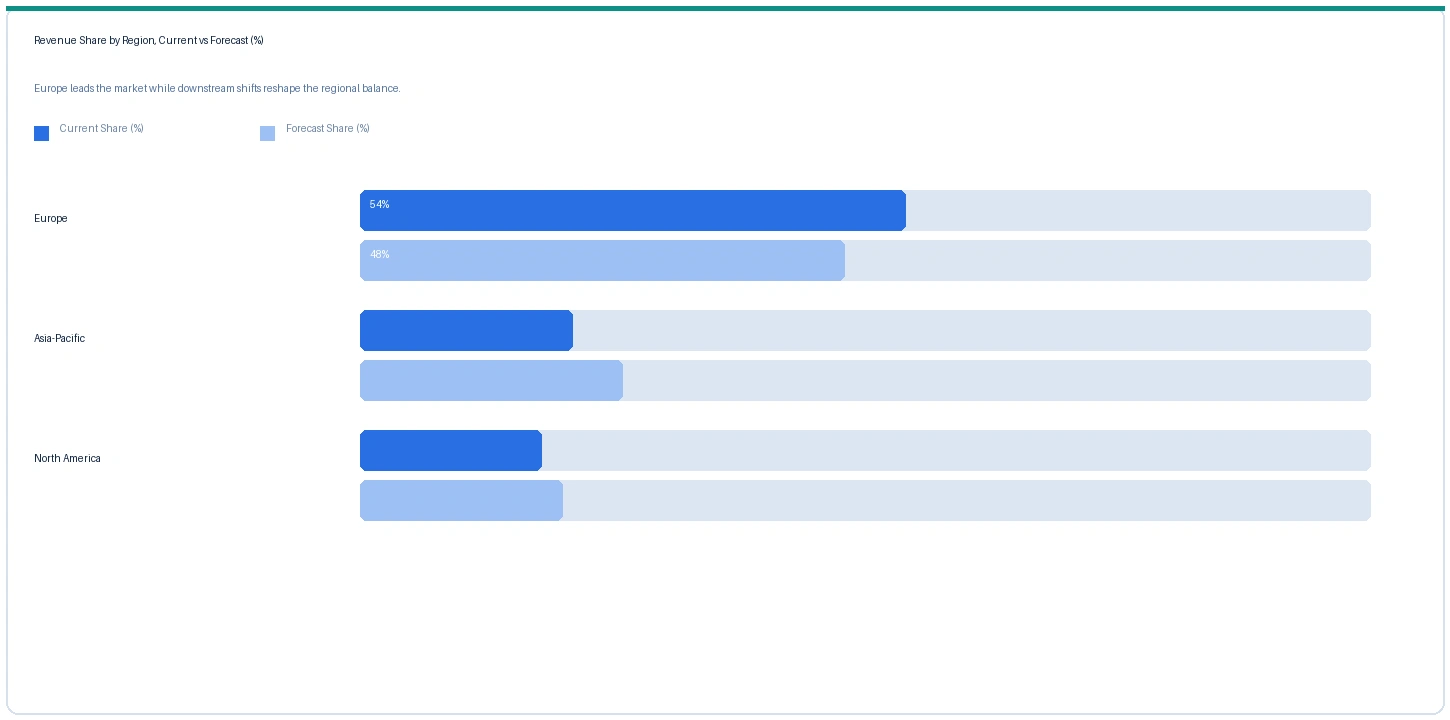

Europe market accounted for largest revenue share over other regional markets in the global automotive piezoelectric fuel injectors market in 2025. Based on regional analysis, the automotive piezoelectric fuel injectors market in Europe accounted for largest revenue share in 2025. Bosch at Stuttgart, Continental AG at Regensburg, and PHINIA Delphi Technologies at Luxembourg and Sudbury are the primary European piezoelectric injector design and manufacturing operations, with combined European market share estimated at approximately 68% to 72% of global piezoelectric automotive injector revenue. Continental's August 2025 European manufacturing expansion adding 40,000 units per month of Direct Drive Piezo Injector capacity confirms that European piezoelectric injector demand is exceeding existing production allocation at the current manufacturing run rate.

Asia-Pacific market accounted for second largest revenue share in the global automotive piezoelectric fuel injectors market in 2025. The market in Asia-Pacific is expected to register the second largest revenue share. China VI emission standards drove piezoelectric CRDI adoption at Chinese commercial vehicle manufacturers including Weichai Power, Yuchai, and Cummins China joint ventures. Japan contributes precision piezoelectric ceramic component manufacturing at Kyocera, Murata Manufacturing, and NGK Spark Plug facilities that supply PZT actuator stacks to Bosch, Continental, and Denso injector assembly operations globally. India's Bharat Stage VI standards from April 2020 drove piezoelectric CRDI adoption at Mahindra, Tata Motors, and Ashok Leyland commercial vehicle diesel programmes served by Bosch India and Delphi India.

North America market is expected to register steady revenue growth in the global automotive piezoelectric fuel injectors market during the forecast period. The market in North America is anchored in heavy commercial vehicle piezoelectric CRDI applications at Cummins and Detroit Diesel, and in GDI piezoelectric applications at Ford F-Series and Chevrolet Silverado high-output gasoline engine families. The 2024 Ford Super Duty and Chevrolet Silverado HD incorporated Bosch and Denso piezoelectric injectors in their updated diesel and gasoline engine families to meet EPA and CARB 2024 emission requirements. Stanadyne's December 2023 launch of the aftermarket's first high-pressure port fuel injection system expands the piezoelectric-compatible aftermarket channel in North American performance applications.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Piezo CRDI Injector (2,500 bar) | Europe | USD 38/unit | USD 35/unit | Rising | Bosch CRS5 ref |

| Piezo GDI Injector (200 bar) | North America | USD 22/unit | USD 20/unit | Rising | Continental ref |

| Piezo GDI Injector (200 bar) | Asia-Pacific | USD 18/unit | USD 16/unit | Rising | PHINIA / Denso ref |

| PZT Ceramic Stack (per injector) | Global | USD 9.40/unit | USD 8.20/unit | Rising | Kyocera / Murata ref |

| Solenoid CRDI (comparator) | Europe | USD 14/unit | USD 13/unit | Stable | Benchmark ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, OEM procurement disclosures, and automotive supplier trade publication monitoring. Piezoelectric fuel injectors are traded under OEM long-term supply agreements. Prices vary by injection system type, pressure rating, injection event capability, and vehicle platform programme volume.

Piezoelectric CRDI injector pricing in Europe rose approximately 8.6% from USD 35 per unit in Q2 2025 to USD 38 per unit in Q2 2026, driven by PZT ceramic stack material cost increases from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which has disrupted zirconium mineral sand shipping from Australia and South Africa to Chinese PZT producers, adding approximately USD 8 to USD 14 per injector unit to ceramic stack production cost. The piezoelectric-to-solenoid CRDI price premium of approximately USD 24 per unit in European markets in Q2 2026 represents a 171% premium above solenoid reference pricing, reflecting the ceramic actuator material cost, precision assembly clean room requirements, and calibration certification infrastructure that Bosch and Continental invest in per injector family. Asian piezoelectric GDI pricing rose approximately 12.5% from USD 16 per unit in Q2 2025 to USD 18 per unit in Q2 2026, reflecting Euro 7 and China 7 programme design-in activity pulling PHINIA and Denso OEM contract pricing above pre-emission-standard contracting cycle volume discount levels.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive piezoelectric fuel injectors market, the Hormuz disruption operates through zirconium mineral sand and PZT ceramic precursor supply chain cost elevation. Zirconium mineral sands from Australia and South Africa are shipped to Chinese and Japanese PZT ceramic producers via routes that transit GCC logistics corridors, and the Hormuz closure has added freight cost and supply timeline uncertainty to zirconium procurement at Kyocera, Murata, and Chinese PZT actuator stack manufacturers, adding approximately USD 8 to USD 14 per injector unit to piezoelectric stack production cost in Q2 2026. The secondary geopolitical impact is energy cost elevation at European OEM engine test bench operations from LNG price increases, adding to the certification cost per injector family calibration programme at Bosch Stuttgart and Continental Regensburg that already creates the calibration cost barrier restricting Euro 7 GDI qualification to the three primary Tier 1 injector suppliers.

Company Insights

The two key dominant companies in the automotive piezoelectric fuel injectors market are Robert Bosch GmbH and Continental AG, recognised for their integrated piezoelectric injector design and manufacturing operations spanning ceramic actuator stack qualification, injector assembly and calibration, OEM engine programme co-development, and end-to-end emission compliance certification across Euro 7, China 7, and Bharat Stage VI regulatory frameworks.

Scope of Research

| Parameter | Detail |

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 786.8 Million |

| Market Size 2032 | USD 1.13 Billion |

| CAGR | 5.3% |

| Units | Revenue in USD Million / Billion |

| Segments Covered | By Injection System, By Vehicle Type, By Sales Channel, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, France, UK, China, Japan, South Korea, India, Brazil, Mexico, Sweden |

| Companies Profiled | Bosch, Continental, PHINIA Delphi Technologies, Denso, Hitachi Astemo, NGK Spark Plug, Kyocera, Murata, Infineon, Aptiv, Stanadyne, Woodward |

| Key Data Sources | Bosch 2024 Powertrain Solutions briefing, Continental AG FY2024 annual report and August 2025 capacity expansion, PHINIA FY2024 results, Denso FY2024 annual report, Kyocera FY2024 annual report, OICA 2024 vehicle production statistics, IEA Global EV Outlook 2025, European Automobile Manufacturers Association BEV registration data, Euro 7 Regulation EU 2024/1257 type approval timelines, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 256 |

| Published | Q2 2026 |

| SKU | NXC-AU-001 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 15 expert interviews conducted between January and May 2026 with OEM powertrain engineering programme managers at European premium car manufacturers, CRDI system procurement leads at heavy commercial vehicle OEMs, PZT ceramic actuator component commercial leads at Kyocera and Murata, and injector calibration engineering leads at OEM co-development facilities. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Robert Bosch GmbH 2024 Powertrain Solutions investor briefing, Continental AG FY2024 annual report and August 2025 capacity expansion disclosure, PHINIA Inc FY2024 results and Changan Auto GDI injector programme disclosure, Denso Corporation FY2024 annual report, Kyocera Corporation FY2024 annual report piezoelectric actuator segment data, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, European Automobile Manufacturers Association 2024 BEV registration data, Euro 7 regulation Regulation EU 2024/1257 text and type approval timeline, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.