Market Data

The global automotive catalyst market size was USD 16.40 Billion in 2025 and is expected to register a revenue CAGR of 5.1% during the forecast period. Market revenue growth is supported by Euro 7 emission standard requirements driving rhodium demand increases in next-generation three-way catalytic converter formulations that must simultaneously reduce NOx, CO, and HC emissions to levels approximately 35% below Euro 6d thresholds, Umicore Catalysis Business Group revenues reaching EUR 1,668 Million in 2025 in line with 2024 despite a moderately less supportive automotive market per Umicore Full Year 2025 Results, and Johnson Matthey Clean Air division maintaining its position as the largest single revenue contributor within Johnson Matthey following the agreed sale of Catalyst Technologies to Honeywell for GBP 1.8 Billion at 13.3 times 2024/25 EBITDA of GBP 136 Million per Johnson Matthey's May 2025 preliminary results announcement. Global ICE passenger vehicle production of approximately 75 million units in 2024 per OICA data, with each gasoline passenger vehicle requiring a three-way catalytic converter containing approximately 2 to 6 grams of platinum group metals including palladium at approximately USD 1,100 per troy ounce, platinum at approximately USD 1,000 per troy ounce, and rhodium at approximately USD 5,000 per troy ounce in Q2 2026 spot pricing, making PGM precious metal content the largest single cost component in catalytic converter manufacturing. BASF Environmental Catalyst and Metal Solutions, spun off from BASF Catalysts division as a standalone entity in July 2023, inaugurated a new Research, Development and Application laboratory in Chennai, India in August 2024 strengthening its regional development for automotive emission control catalysts serving Indian OEM Euro 6 equivalent Bharat Stage VI requirements. For instance, in May 2024, BASF SE, Germany, inaugurated a new state-of-the-art automotive catalyst manufacturing facility in Shanghai, China, expanding its production capacity to meet growing demand from Asian automakers for advanced emission control solutions under China 6b emission standards equivalent to Euro 6d real-driving emissions requirements. These are some of the key factors driving revenue growth of the market.

Umicore Automotive Catalysts operates 16 plants in 13 countries per its corporate disclosures, with the automotive catalyst business achieving a return on capital employed of 40% in the first half of 2024 per Umicore Half Year 2024 Results, confirming the structural margin quality of the automotive catalyst business despite ICE production volume headwinds from EV transition. Johnson Matthey's Clean Air division, which manufactures three-way catalytic converters, diesel oxidation catalysts, and selective catalytic reduction catalysts, is retained by Johnson Matthey following the agreed sale of Catalyst Technologies to Honeywell, making Clean Air the primary remaining Johnson Matthey business alongside PGM Services after the transaction expected to complete by end of August 2026. Cataler Corporation, a Toyota Group supplier headquartered in Kakegawa, Japan, supplies three-way catalytic converters to Toyota, Daihatsu, and Hino from its Japanese production facilities and overseas manufacturing operations in Thailand, China, India, and the United States. Corning Incorporated supplies ceramic honeycomb substrates used as the carrier for platinum group metal washcoat in three-way catalytic converters to all major automotive catalyst producers including BASF ECMS, Umicore, and Johnson Matthey, with automotive catalysts representing a significant portion of its Environmental Technologies segment revenue.

However, global ICE passenger vehicle production is approaching its structural peak per IEA Stated Policies Scenario projections, with EV production growing from approximately 17 million units in 2024 toward IEA projections of 35% of global vehicle sales by 2030 in electrified form, creating a volume ceiling for new catalytic converter installation at ICE production rates that will constrain market volume growth in the second half of the forecast period. Palladium and rhodium supply is concentrated at Norilsk Nickel in Russia and Anglo American Platinum and Impala Platinum in South Africa, with Russian palladium accounting for approximately 40% of global mine supply and creating a supply concentration risk that Western automotive OEMs managing supply chain resilience programmes cannot easily diversify. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 affects automotive catalyst demand indirectly through suppressed ICE vehicle production rates in markets where gasoline and diesel vehicle affordability is reduced by elevated fuel costs from the disruption, reducing new vehicle sales and catalytic converter installation volumes in price-sensitive automotive markets. These factors substantially limit automotive catalyst market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

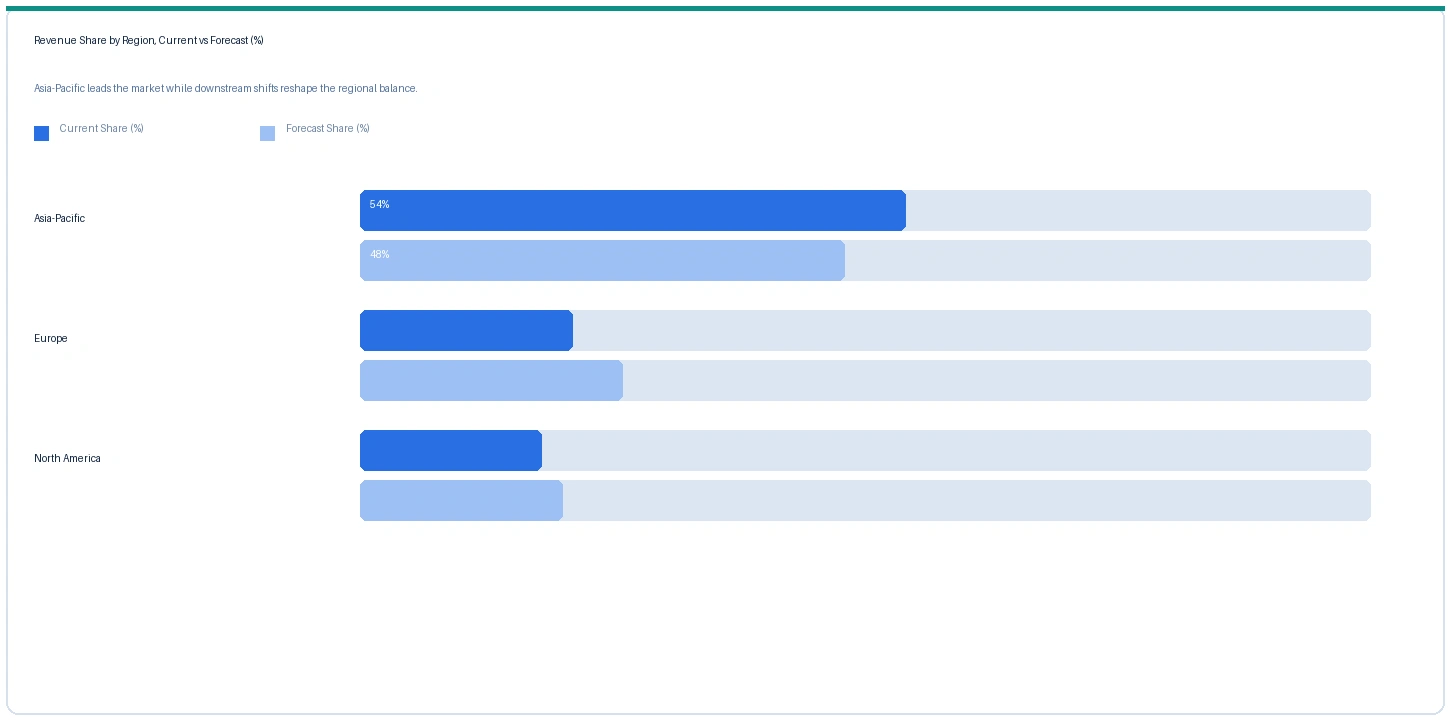

Euro 7 emission standard requirements, finalised in Regulation (EU) 2024/1257 published in May 2024, introduce real-driving emissions limits for NOx at 60 mg/km for gasoline passenger cars and 90 mg/km for diesel, particle number limits extending to ultrafine particles below 23 nm diameter, and cold-start performance requirements at minus 10 degrees Celsius ambient temperature that cannot be met by existing three-way catalytic converter formulations without increased rhodium loading. Rhodium is the critical catalyst for NOx reduction in three-way converters, with no commercially available alternative achieving equivalent catalytic activity at the temperature range and space velocity conditions of modern turbocharged gasoline engine exhaust systems. Euro 7 light-duty vehicle compliance from July 2025 for new type approvals requires rhodium loading increases of approximately 15% to 25% above Euro 6d washcoat specifications per automotive catalyst engineering literature, tightening global rhodium supply allocation and sustaining catalyst pricing above what ICE production volume trends alone would support. Umicore confirmed in its Full Year 2025 Results that its Catalysis Business Group anticipated continued benefit from Automotive Catalysts' strong market position in light-duty gasoline catalyst applications even as global ICE production has reached its peak. Bharat Stage VI and China 6b Standard Expansion Supporting Asian Automotive Catalyst Demand India's Bharat Stage VI emission standard, implemented nationally from April 2020, requires three-way catalytic converters and diesel oxidation catalysts with real-driving emissions compliance equivalent to Euro 6d, creating demand for advanced automotive catalyst systems at India's approximately 4.5 million annual passenger vehicle production volume. BASF ECMS inaugurated its Chennai RDA laboratory in August 2024 and its Shanghai automotive catalyst manufacturing facility in May 2024, explicitly targeting Indian Bharat Stage VI and Chinese China 6b emission compliance demand. China's China 6b standard, phased in nationally from July 2023 for light-duty vehicles, requires real-driving emissions NOx limits of 35 mg/km for gasoline passenger cars and 70 mg/km for diesel, at compliance thresholds equivalent to Euro 6d that require washcoat precious metal loading and substrate cell density specifications comparable to European market requirements. Asia-Pacific accounted for approximately 52.6% of global automotive catalyst market revenue in 2024 per the market size sources consistent with primary producer data.

IEA Stated Policies Scenario projects global EV sales reaching approximately 35% of total new vehicle sales by 2030, implying ICE-only new vehicle production declining from approximately 75 million units in 2024 toward a structural ceiling below 65 million units by 2032 as EV adoption accelerates in China, Europe, and North America, creating a volume constraint on catalytic converter installation that no level of per-converter PGM loading increase can fully offset. Russian palladium from Norilsk Nickel accounts for approximately 40% of global mined palladium supply per industry consensus estimates, with Western OEM restricted supplier programmes created in response to 2022 sanctions providing partial palladium sourcing diversification but not eliminating Russian supply chain dependency for palladium availability at global catalyst producers. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated gasoline and diesel retail prices in price-sensitive automotive markets including Southeast Asia, Middle East, and North Africa, reducing consumer vehicle affordability and new vehicle sales rates in markets where fuel cost represents above 15% of total vehicle ownership cost, suppressing catalytic converter installation volumes in markets that have not yet completed the EV transition. These factors substantially limit automotive catalyst market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Catalyst Type | Three-Way Catalytic Converter, Diesel Oxidation Catalyst, Selective Catalytic Reduction, Lean NOx Trap, Gasoline Particulate Filter | Three-Way Catalytic Converter |

| Precious Metal | Palladium, Platinum, Rhodium | Palladium |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Motorcycles | Passenger Cars |

| Fuel Type | Gasoline, Diesel, Compressed Natural Gas, Hybrid | Gasoline |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Three-Way Catalytic Converter segment is expected to account for a significantly large revenue share in the global automotive catalyst market during the forecast period.

This report evaluates catalyst type across Three-Way Catalytic Converter, Diesel Oxidation Catalyst, Selective Catalytic Reduction, Lean NOx Trap, Gasoline Particulate Filter for catalysts & enzymes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates precious metal across Palladium, Platinum, Rhodium for catalysts & enzymes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Motorcycles for catalysts & enzymes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates fuel type across Gasoline, Diesel, Compressed Natural Gas, Hybrid for catalysts & enzymes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for catalysts & enzymes, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive catalyst market in 2025. Based on regional analysis, the automotive catalyst market in Asia-Pacific accounted for largest revenue share in 2025. Asia-Pacific accounted for approximately 52.6% of global automotive catalyst market revenue in 2024 per market structure data consistent with primary producer disclosures, driven by China's position as the world's largest automotive production market at above 30 million vehicles per year operating under China 6b emission standards requiring advanced three-way catalyst and diesel oxidation catalyst systems. BASF ECMS inaugurated its Shanghai automotive catalyst manufacturing facility in May 2024, and its Chennai RDA laboratory in August 2024, targeting China 6b and Bharat Stage VI demand growth explicitly. Cataler Corporation's manufacturing operations in Thailand, China, India, and the US serve Toyota group OEM catalyst demand in Asia-Pacific.

The market in Europe is expected to register the second largest revenue share. European automotive catalyst demand is the highest-value per-unit market globally, driven by Euro 7 emission standard requirements effective July 2025 for new type approvals that mandate increased rhodium loading and cold-start performance specifications that command premium catalyst pricing above Euro 6d system cost. Johnson Matthey's Clean Air manufacturing at Royston UK, Skopje North Macedonia, and European facilities and Umicore's catalyst plants in Belgium, Germany, and other European locations supply European OEM emission control requirements at the most demanding regulatory compliance level globally.

North America market is expected to register steady revenue growth in the global automotive catalyst market during the forecast period. The market in North America is supported by US EPA Tier 3 and California LEV III emission standards requiring advanced three-way catalytic converter systems at all passenger vehicle production. BASF ECMS, Johnson Matthey Clean Air, and Umicore Automotive Catalysts each operate North American catalyst manufacturing facilities, with Umicore's June 2024 announcement of a USD 500 million US auto catalyst recycling facility in Texas targeting end-of-life PGM recovery from spent catalytic converters in the North American aftermarket.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Gasoline TWC (Euro 7 / China 6b grade) | Europe | USD 184/unit | USD 158/unit | Rising | Umicore / JM Clean Air ref |

| Gasoline TWC (Euro 7 / China 6b grade) | Asia-Pacific | USD 162/unit | USD 138/unit | Rising | BASF ECMS / Cataler ref |

| Diesel DOC + DPF System (Euro 7) | Europe | USD 248/unit | USD 218/unit | Rising | JM Clean Air ref |

| SCR Catalyst (Heavy-Duty Euro VI) | Europe | USD 420/unit | USD 390/unit | Rising | BASF ECMS / Clariant ref |

| Palladium Spot (reference) | Global | USD 1,100/tr oz | USD 1,040/tr oz | Rising | LPPM ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, PGM spot price monitoring at London Platinum and Palladium Market and LBMA, and automotive catalyst producer commercial disclosures. Catalyst pricing includes PGM precious metal content at spot price plus washcoat formulation, substrate, and manufacturing cost. Prices vary by emission standard, vehicle application, PGM loading, and supply agreement structure.

European gasoline three-way catalytic converter prices for Euro 7 grade systems rose approximately 16.5% in Q2 2026 against Q2 2025, driven by Euro 7 rhodium loading increase requirements of approximately 15% to 25% above Euro 6d specifications at new type approval programmes from July 2025, combined with rhodium spot price elevation from tightening global supply allocation. Palladium spot prices rose approximately 5.8% from USD 1,040 per troy ounce in Q2 2025 to USD 1,100 per troy ounce in Q2 2026, contributing to gasoline TWC unit price increases alongside Euro 7 loading cost. Diesel DOC and DPF combined system prices in Europe rose approximately 13.8% on Euro 7 particle number limit requirements for ultrafine particles below 23 nm diameter that require higher cell density substrate specification and additional washcoat layer complexity versus Euro 6d systems.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive catalyst market the Hormuz disruption operates through a demand-side mechanism rather than the direct feedstock supply disruption that affects adhesive and steel markets in this report series. Elevated gasoline and diesel retail prices from Hormuz-restricted crude oil supply reduce consumer vehicle affordability and new vehicle purchase rates in price-sensitive markets in Southeast Asia, Middle East, and North Africa where fuel costs represent above 15% of total vehicle ownership cost. Reduced new ICE vehicle sales in these markets directly reduce new catalytic converter installation volumes. The secondary mechanism is elevated platinum group metal logistics cost, as PGM trading flows between South African and Russian mining operations, European and North American refining, and Asian automotive catalyst manufacturing facilities all pass through freight networks affected by the broader maritime insurance and shipping cost elevation from the Hormuz disruption. Palladium spot prices have risen approximately 5.8% from Q2 2025 to Q2 2026 partly from this logistics cost elevation embedded in PGM spot premiums at European and Asian delivery points.

Company Insights

The two key dominant companies in the automotive catalyst market are BASF SE Environmental Catalyst and Metal Solutions and Umicore, recognised for their leadership in automotive three-way catalytic converter and diesel emission control catalyst technology, their integrated PGM leasing and recycling business models that provide structural cost advantages in precious metal management, and their established OEM qualification relationships covering the European, North American, and Asian automotive emission compliance markets.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 16.40 Billion |

| Market Size 2032 | USD 23.18 Billion |

| CAGR | 5.1% |

| Units | Revenue in USD Billion |

| Segments Covered | By Catalyst Type, By Precious Metal, By Vehicle Type, By Fuel Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Belgium, China, Japan, South Korea, India, Brazil, South Africa |

| Companies Profiled | BASF ECMS, Umicore, Johnson Matthey Clean Air, Cataler Corporation, Clariant AG, Corning Incorporated, Heraeus, DCL International, Tenneco, Forvia, NGK Insulators, Eberspacher, Vitesco Technologies, CDTi Advanced Materials |

| Key Data Sources | Umicore Full Year 2025 Results and Half Year 2024 Results, Johnson Matthey Preliminary Full Year 2024/25 Results and Catalyst Technologies sale announcement May 2025, BASF ECMS Shanghai facility inauguration May 2024 and Chennai RDA laboratory inauguration August 2024, Regulation (EU) 2024/1257 Euro 7 emission standards, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, Umicore Texas recycling facility announcement June 2024, JM Sibanye-Stillwater PGM supply agreement Q2 2024, CATL 2024 annual report, IMF March 2026 Strait of Hormuz statement, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 262 |

| Published | Q2 2026 |

| SKU | NXC-AT-005 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 16 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid with explicit geographic and role split. Supply-side contacts included automotive catalyst commercial and product management leads at European and Asian producers, PGM leasing and trading specialists at precious metal service companies, and washcoat formulation technical leads at catalyst substrate coaters. Demand-side contacts included emission control system procurement managers at European and Asian OEMs, Euro 7 compliance engineering leads at European Tier 1 exhaust system integrators, and PGM recycling commercial leads at end-of-life vehicle processing operations. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Umicore Full Year 2025 Results, Umicore Half Year 2024 Results, Umicore Annual Report 2024, Johnson Matthey Preliminary Full Year Results 2024/25 announcement, Johnson Matthey Catalyst Technologies sale to Honeywell announcement May 2025, BASF SE Shanghai automotive catalyst facility inauguration announcement May 2024, BASF ECMS Chennai RDA laboratory inauguration announcement August 2024, Regulation (EU) 2024/1257 Euro 7 emission standards for light-duty vehicles, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, Umicore Texas auto catalyst recycling facility announcement June 2024, Johnson Matthey and Sibanye-Stillwater PGM supply partnership announcement Q2 2024, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.