Market Data

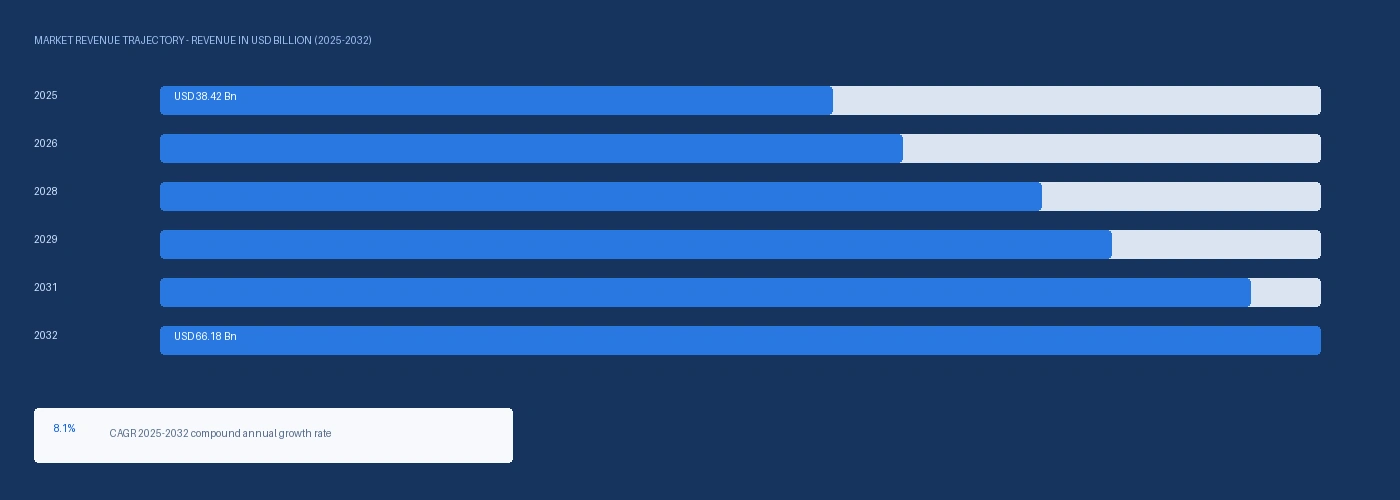

The global automotive aluminum market size was USD 38.42 Billion in 2025 and is expected to register a revenue CAGR of 8.1% during the forecast period. Market revenue growth is supported by EV battery enclosure aluminum demand growing at approximately 18% to 22% per year as each battery electric vehicle requires 40 to 80 kilograms of aluminum in the battery pack tray, side rails, cooling plate, and cross member structures, Novelis Inc. reporting net sales of USD 16.20 Billion for fiscal year 2024 per its SEC 8-K earnings release with strong automotive demand even as total shipments declined from beverage packaging customer inventory reductions, and Alcoa Corporation reporting full-year 2024 revenue of USD 11.90 Billion with annual production records at five aluminum smelters globally. OICA confirmed global EV and plug-in hybrid production of approximately 17 million units in 2024, with each BEV requiring 40 to 80 kilograms of aluminum in the battery enclosure structure in addition to the 150 to 250 kilograms of aluminum content in BIW closures, powertrain castings, and chassis subframes at premium and mid-market EV platforms. Constellium SE supplies aluminum body sheet for the Ford F-150 Lightning battery electric truck, which uses approximately 900 pounds of aluminum body structure per vehicle at a content level that makes it among the most aluminum-intensive volume vehicle programmes globally. Novelis confirmed in its FY2024 SEC 8-K earnings that automotive shipments grew on strong demand even as total Novelis shipments declined 3% from beverage packaging customer inventory reductions, with the company increasing recycled content to 63% of its products in FY2024. For instance, in FY2024 ending March 2024, Novelis Inc., United States, reported net sales of USD 16.20 Billion with automotive shipments growing on strong demand, and the company increased its recycled content to 63% of products, up from 61% in FY2023, per its SEC 8-K earnings release filed with the US Securities and Exchange Commission. These are some of the key factors driving revenue growth of the market.

Alcoa Corporation reported full-year 2024 revenue of USD 11.90 Billion, a 13% increase, setting annual aluminum production records at five smelters in the US, Canada, and Norway and delivering a USD 645.0 Million profitability improvement programme per its annual earnings disclosures. Alcoa's aluminum segment produced 2.2 to 2.3 million metric tonnes annually in 2024, with shipments of 2.5 to 2.6 million metric tonnes reflecting trading volumes supplementing production. Norsk Hydro ASA, headquartered in Oslo, Norway, operates automotive aluminum extrusions at Hydro Extrusion Europa with plants in Germany, the Netherlands, and the UK supplying European OEM chassis subframe and battery pack structural member programmes. Arconic Corporation, separated from Alcoa in 2020, supplies 5xxx and 6xxx series aluminum body sheet to BMW Group, Mercedes-Benz, Jaguar Land Rover, and Ford for BIW closure panel applications through its Tennessee and Iowa rolling facilities. Constellium SE, headquartered in Paris, France, supplies body-in-white and body structure aluminum sheet and stamped parts from its Neuf-Brisach, France and Muscle Shoals, Alabama facilities.

However, aluminum body sheet production requires specific 5xxx and 6xxx series alloy compositions with controlled magnesium content for bake-hardening response that must be qualified at each OEM body shop stamping line individually, creating an 18 to 24 month qualification cycle that delays supplier switching and limits market share movement between Novelis, Constellium, and Arconic in established BIW programs. Section 232 tariffs on Canadian aluminum at 50% from Q2 2025 per Alcoa's Q2 2025 earnings commentary, which disclosed approximately USD 115 million in tariff costs on Canadian aluminum imports, create a cost burden on US automotive aluminum supply chains that source Canadian smelter production from Alcoa and Rio Tinto Canadian operations. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated aluminum smelting energy costs at Gulf-region producers and elevated LNG costs at Norwegian and Icelandic smelters supplying European automotive sheet mills, contributing to European aluminum price elevation of approximately USD 120 to USD 180 per metric tonne above North American LME benchmark in Q2 2026. These factors substantially limit automotive aluminum market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EV battery pack enclosures require die-cast, extruded, or multi-piece welded aluminum tray and lid structures that contain and protect the cell array, provide structural stiffness to the vehicle body, and integrate cooling channels or plates for thermal management. Each battery electric vehicle requires 40 to 80 kilograms of aluminum in the battery pack structure depending on battery capacity and pack architecture, at a value of approximately USD 180 to USD 360 per vehicle at USD 4,500 per metric tonne automotive-grade aluminum pricing. CATL's disclosed 700 gigawatt-hour annual battery production capacity implies battery enclosure aluminum demand from CATL packs alone of approximately 2.8 to 4.9 million metric tonnes per year, assuming 4 to 7 kilograms of enclosure aluminum per kilowatt-hour of battery capacity at average energy density. Novelis supplies automotive-grade aluminum body sheet and is expanding its recycled content capability to support closed-loop automotive aluminum recycling at European and North American OEM body shops, with FY2024 automotive shipments growing on strong demand per SEC 8-K disclosure despite total company volume declining from beverage packaging headwinds. Fuel Economy and CO2 Emission Regulation Sustaining Aluminum BIW and Closure Panel Demand European CO2 passenger car fleet average emissions regulation at 95 g CO2/km through 2024 and transitioning to 81 g CO2/km by 2030 per EU Regulation 2019/631 creates mandatory lightweighting pressure at ICE and hybrid platform OEMs for whom each kilogram of vehicle weight reduction is credited against fleet average CO2 compliance cost. Each 100 kg of mass reduction yields approximately 8 to 10 g/km CO2 reduction for a typical C-segment passenger car, making aluminum closure panels at 30% to 40% lower density than equivalent steel panels commercially justified at EUR 30 to EUR 50 per kilogram of weight saved relative to the CO2 compliance penalty cost. European corporate average fleet CO2 penalties of EUR 95 per g CO2/km per vehicle above the target provide an explicit economic value to mass reduction that sustains aluminum BIW adoption at European OEMs independent of short-term aluminum price premiums over steel.

Alcoa's Q2 2025 earnings disclosure of approximately USD 115 million in tariff costs on Canadian aluminum imports from increased Section 232 tariffs confirms that US automotive aluminum supply chains sourcing Canadian smelter production are absorbing a material input cost increase that cannot be immediately passed to automotive OEM customers under annual supply agreements. Automotive body sheet qualification requires 18 to 24 months of stamping trials, dimensional analysis, and corrosion testing at OEM body shop tooling before a new aluminum sheet supplier can displace an established supplier at a production programme, limiting market share movement in established BIW applications. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated LNG costs at Norwegian and Icelandic smelters and Gulf Cooperation Council aluminium smelters at ALBA Bahrain, DUBAL Dubai, and EMAL Abu Dhabi, adding approximately USD 80 to USD 140 per metric tonne to aluminum production cost at these operations and contributing to elevated LME aluminum premiums in European markets in Q2 2026. These factors substantially limit automotive aluminum market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Form | Cast Aluminum, Rolled Aluminum Sheet, Extruded Aluminum | Cast Aluminum |

| Alloy Series | 2xxx Series, 5xxx Series, 6xxx Series, 7xxx Series | 2xxx Series |

| Application | Body Panels and Closures, Chassis and Subframe, Powertrain Components, Battery Enclosures | Body Panels and Closures |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Electric Vehicles, Commercial Vehicles | Passenger Cars |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Cast Aluminum segment is expected to account for a significantly large revenue share in the global automotive aluminum market during the forecast period.

This report evaluates product form across Cast Aluminum, Rolled Aluminum Sheet, Extruded Aluminum for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates alloy series across 2xxx Series, 5xxx Series, 6xxx Series, 7xxx Series for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Body Panels and Closures, Chassis and Subframe, Powertrain Components, Battery Enclosures for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Electric Vehicles, Commercial Vehicles for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

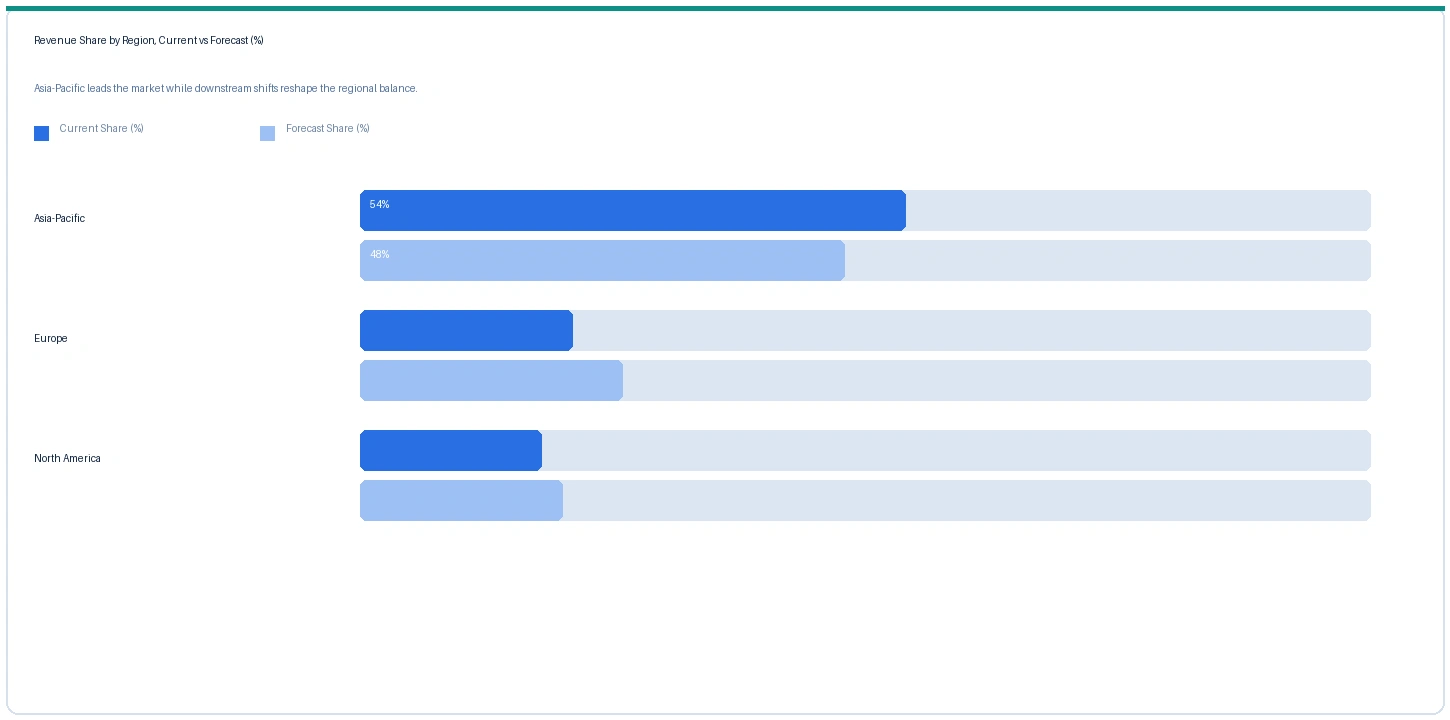

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive aluminum market in 2025. Based on regional analysis, the automotive aluminum market in Asia-Pacific accounted for largest revenue share in 2025. China accounts for approximately 55% to 60% of global automotive aluminum consumption, driven by its position as the world's largest automotive production market at above 30 million vehicles per year and the fastest-growing EV market with BYD, NIO, SAIC, and CATL-supplied EV platforms incorporating battery enclosure aluminum at above-global-average rates. Japanese aluminium producers UACJ Corporation and Sumitomo Light Metal Industries supply automotive sheet to Toyota, Honda, and Nissan domestic production, while South Korea's POSCO subsidiary Poschampf supplies aluminum sheet to Hyundai Motor Group.

The market in Europe is expected to register the second largest revenue share. Novelis at Nachterstedt Germany and Lutten Germany, Constellium at Neuf-Brisach France, and Arconic at Koblenz Germany supply the primary European automotive aluminum sheet to BMW, Volkswagen Group, Mercedes-Benz, Stellantis, and Renault body shop programmes. Norsk Hydro supplies extrusions for EV battery structural members and chassis subframes at European OEM programmes. European aluminum prices were elevated approximately USD 120 to USD 180 per metric tonne above LME North American levels in Q2 2026 from Hormuz-related LNG energy cost elevation at Norwegian smelters.

North America market is expected to register steady revenue growth in the global automotive aluminum market during the forecast period. The market in North America is anchored in Novelis at Oswego New York and Berea Kentucky, Arconic at Tennessee and Iowa, and Constellium at Muscle Shoals Alabama supplying automotive body sheet to Ford, General Motors, Stellantis, and Toyota North American assembly. Alcoa's USD 11.90 Billion 2024 revenue with smelter production records at five facilities confirms North American aluminum primary production growth, though Section 232 tariffs on Canadian aluminum at 50% per Alcoa's Q2 2025 disclosure are adding approximately USD 115 million in quarterly tariff cost to US automotive aluminum supply chains importing from Canadian smelter sources.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| 6xxx Series Auto Body Sheet (5182/6016) | Europe | USD 3,840/MT | USD 3,560/MT | Rising | Novelis / Constellium ref |

| 6xxx Series Auto Body Sheet (5182/6016) | North America | USD 3,620/MT | USD 3,380/MT | Rising | Novelis / Arconic ref |

| 5xxx Series Battery Enclosure Sheet | Asia-Pacific | USD 3,280/MT | USD 3,020/MT | Rising | UACJ / Sumitomo ref |

| Extruded Structural Profiles (6xxx) | Europe | USD 3,420/MT | USD 3,160/MT | Rising | Hydro Extrusion ref |

| High-Pressure Die Cast Alloy | Global | USD 2,840/MT | USD 2,620/MT | Rising | LME + alloy premium |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and LME and Midwest premium monitoring. Automotive aluminum prices include LME ingot plus regional delivery premium plus alloy surcharge plus conversion premium for automotive specification sheet or extrusion.

European 6xxx series automotive body sheet prices rose approximately 7.9% in Q2 2026 against Q2 2025, driven by LNG energy cost elevation at Norwegian and Icelandic smelters from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which restricted GCC LNG exports and elevated European LNG spot prices above 2024 baseline levels, contributing approximately USD 80 to USD 140 per metric tonne of additional production cost at smelters supplying European rolling mills. North American automotive sheet prices rose approximately 7.1% in Q2 2026 against Q2 2025, with Section 232 tariff costs on Canadian aluminum imports adding an input cost burden that Alcoa disclosed at approximately USD 115 million in Q2 2025 and which has been partially reflected in downstream automotive sheet pricing. EV battery enclosure 5xxx series sheet rose approximately 8.6% in Asia-Pacific on growing battery assembly demand from BYD and CATL production expansion outpacing regional aluminum sheet capacity additions.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive aluminum market the Hormuz disruption operates through aluminum smelting energy costs. Norwegian and Icelandic smelters supplying European automotive sheet rolling mills at Novelis, Constellium, and Arconic source power from hydropower at contracted rates but are exposed to European spot electricity and LNG market pricing for balancing energy requirements, with European gas prices elevated from restricted GCC LNG supply. GCC aluminum smelters at ALBA Bahrain, DUBAL Dubai, and EMAL Abu Dhabi, which collectively account for approximately 2.5 million metric tonnes of annual primary aluminum production, face LNG supply disruption at their integrated gas-fired power generation operations that supply smelting load, reducing GCC smelter output and contributing to global aluminum supply tightening and LME price elevation of approximately USD 80 to USD 140 per metric tonne in Q2 2026 versus Q2 2025.

Company Insights

The two key dominant companies in the automotive aluminum market are Novelis Inc. and Constellium SE, recognised for their leadership in automotive-grade aluminum body sheet production, their established supply relationships with global automotive OEMs for BIW closure panels and EV battery enclosures, and their technical leadership in bake-hardening alloy development and closed-loop automotive aluminum recycling.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 38.42 Billion |

| Market Size 2032 | USD 66.18 Billion |

| CAGR | 8.1% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product Form, By Alloy Series, By Application, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Norway, China, Japan, South Korea, India, Brazil, Bahrain, UAE |

| Companies Profiled | Novelis Inc., Constellium SE, Arconic Corporation, Norsk Hydro ASA, UACJ Corporation, Alcoa Corporation, Sumitomo Light Metal, Aleris, Elval Colour, Kobe Steel, Nemak, Martinrea Honsel |

| Key Data Sources | Novelis Inc. SEC 8-K FY2024 and FY2025 earnings releases, Alcoa Corporation FY2024 annual earnings, Constellium SE annual reports, Norsk Hydro ASA annual reports, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, Alcoa Q2 2025 Section 232 tariff disclosure, EU Regulation 2019/631 CO2 fleet average standards, CATL 2024 annual battery production capacity disclosure, IMF March 2026 Strait of Hormuz statement, 17 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 272 |

| Published | Q2 2026 |

| SKU | NXC-AT-004 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 17 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included automotive aluminum sheet and extrusion commercial managers at European, North American, and Asian producers, EV battery enclosure design engineers at aluminum system integrators, and primary aluminum smelter commercial leads. Demand-side contacts included automotive body shop aluminum procurement managers at European premium OEMs, EV battery pack structural procurement leads at Asian EV manufacturers, and chassis and subframe aluminum sourcing engineers at North American Tier 1 structural module suppliers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Novelis Inc. SEC 8-K FY2024 and FY2025 earnings releases filed with the US Securities and Exchange Commission, Alcoa Corporation FY2024 annual earnings releases and Q2 2025 tariff disclosure, Constellium SE annual reports and investor presentations, Norsk Hydro ASA annual reports, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, EU Regulation 2019/631 passenger car CO2 fleet average emission standards, CATL 2024 annual report battery manufacturing capacity disclosures, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.