Market Data

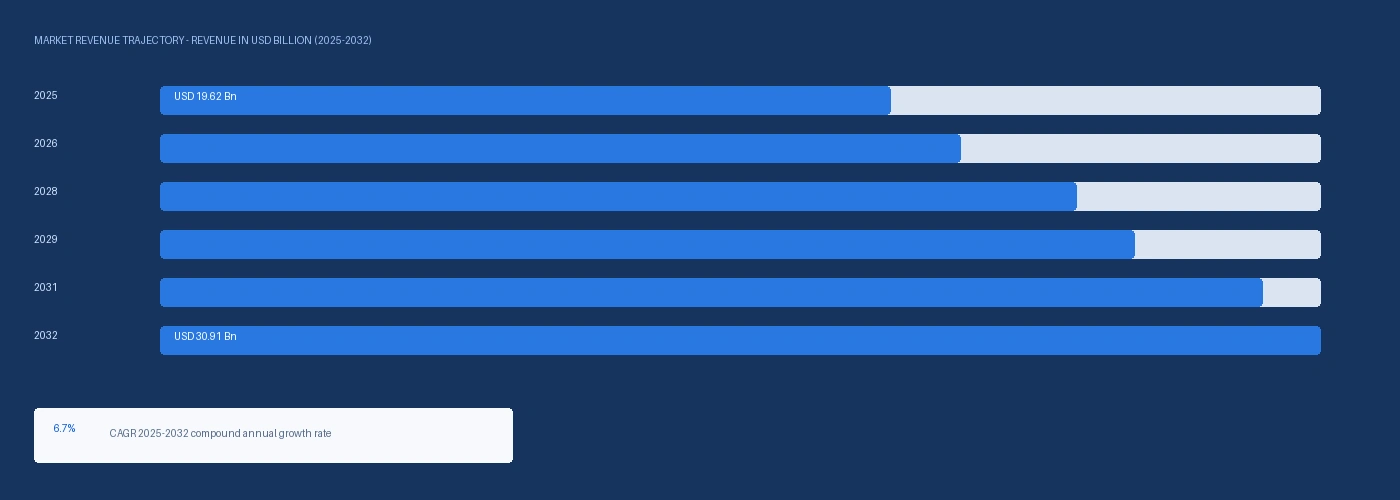

The global automotive advanced high strength steel market size was USD 19.62 Billion in 2025 and is expected to register a revenue CAGR of 6.7% during the forecast period. Market revenue growth is supported by press hardened steel PHS grade adoption in EV battery protection underbody frames and B-pillar inner sections growing at above-trend rates as OEMs prioritise passenger protection against battery intrusion in side-impact and under-vehicle impact scenarios, ArcelorMittal confirming full-year 2024 results indicating sustained advanced automotive steel demand above pre-pandemic production levels, and AM/NS India (ArcelorMittal Nippon Steel India) launching advanced automotive steel production lines in January 2025 targeting Indian passenger vehicle manufacturers with AHSS supply as India's domestic automotive production continues growing toward 6 million units per year. Global passenger vehicle production of approximately 92 million units in 2024 per OICA data, with AHSS content per vehicle growing from approximately 200 to 250 kilograms in standard passenger cars in 2019 to approximately 260 to 320 kilograms in 2024 as dual-phase and press-hardened steel penetration of BIW structural and crash management components increased. ArcelorMittal disclosed its Fortiform 1500 ultra-high strength steel grade launch in 2023 for automotive structural components, with the 1500 MPa tensile strength grade providing body structure designers with a material option achieving equivalent crash performance to conventional HSS at 20% to 30% weight reduction. In June 2025, ArcelorMittal finalised full ownership of AM/NS Calvert following acquisition of Nippon Steel's 50% stake, expanding its production of ultra-high-strength and advanced steel grades for automotive and industrial applications in North America. For instance, in January 2025, ArcelorMittal Nippon Steel India, India, launched advanced automotive steel production lines at its integrated steel plant, delivering customised AHSS solutions for Indian passenger vehicle manufacturers and reinforcing the Atmanirbhar Bharat domestic steel ecosystem, becoming the first commercially operating advanced automotive steel production capability in India at scale. These are some of the key factors driving revenue growth of the market.

Press hardened steel was indicatively priced at USD 1,240 per metric tonne in Europe and USD 1,180 per metric tonne in Asia-Pacific in Q2 2026, representing premiums of approximately USD 340 per metric tonne and USD 280 per metric tonne respectively above standard automotive dual-phase steel, reflecting the additional processing cost of hot stamping, quenching, and die trimming at temperature that PHS production requires versus cold-stamped DP steel. ThyssenKrupp, voestalpine, SSAB, and Tata Steel Europe compete with ArcelorMittal and POSCO in European advanced automotive steel supply, with European hot-stamping AHSS prices elevated approximately USD 80 to USD 120 per metric tonne above Asian levels in Q2 2026 reflecting European energy cost elevation from the Strait of Hormuz supply disruption. SSAB announced in April 2025 a major expansion at its Alabama plant including a new tempering furnace to boost high-strength steel production capacity, expanding its Hardox and Strenx product availability for North American and global automotive and industrial markets. Nippon Steel's June 2025 completion of the US Steel acquisition integrates advanced high-strength steel technologies and enhances global production capabilities for automotive and construction sector supply.

However, aluminium sheet content in automotive BIW outer panels is increasing at European premium OEMs including BMW, Audi, and Mercedes-Benz as lightweighting programme requirements push outer panel materials toward aluminium alloys that AHSS cannot match on a density basis regardless of strength, reducing AHSS volume in skin panel applications that had historically been supplied in dual-phase grades. The structural shift of EV platforms toward aluminium-intensive BIW in premium segments and toward AHSS-dominant BIW in mass-market EV platforms creates a product mix uncertainty for AHSS producers who must supply both AHSS-dominant and AHSS-reduced body structures depending on OEM segment strategy. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated European steel production energy costs through LNG and natural gas price elevation at blast furnace and electric arc furnace operations, adding approximately USD 30 to USD 60 per metric tonne to European AHSS production cost in Q2 2026. These factors substantially limit automotive advanced high strength steel market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EV battery protection requirements have created a new structural application for press hardened steel in underbody frame members and battery pack cross members that must absorb impact energy in both side-impact FMVSS 214 and under-vehicle pole impact scenarios without allowing intrusion into the battery cell array. NCAP and Euro NCAP side-impact battery protection test protocols introduced in 2022 and expanded in 2024 require OEM body structures to prevent battery intrusion in standardised side-impact scenarios at 50 to 60 km/h, creating a functional requirement for ultra-high strength material at battery sill and rocker panel positions that conventional dual-phase or high-strength low-alloy steel cannot satisfy at commercially viable gauge. ArcelorMittal's press hardened steel Usibor 1500 and Ductibor 1000 grades are qualified at BMW, Volkswagen Group, Stellantis, and Hyundai Motor for EV battery frame applications, with EV platform content per vehicle in PHS grades growing approximately 40% above ICE equivalent designs at the same OEM platforms as the battery protection frame replaces conventional rocker panel and underbody cross member designs. SSAB confirmed in its April 2025 Alabama expansion announcement that demand for its high-strength steel products in North American automotive and industrial markets was growing at rates justifying incremental capacity investment. AM/NS India and Asian AHSS Capacity Expansion Supporting Indian and South-East Asian Vehicle Production Growth AM/NS India's January 2025 advanced automotive steel production line launch at its integrated plant provides Indian vehicle manufacturers including Maruti Suzuki, Tata Motors, Mahindra, and Hyundai India with domestic AHSS supply for the first time, reducing import dependency on Japanese and Korean AHSS at a premium that had historically made Indian vehicle lightweighting programmes less economically viable than at equivalent-volume European or North American OEM plants. The Society of Indian Automobile Manufacturers SIAM confirmed Indian passenger vehicle production exceeded 5.5 million units in fiscal year 2025, with OEMs targeting above-5-star Bharat NCAP safety ratings creating mandatory demand for advanced high-strength steel in A and B pillars, door intrusion beams, and bumper beams. POSCO's automotive steel division at Pohang and Gwangyang in South Korea, and NSSMC's automotive steel at Nagoya and Kimitsu in Japan, continue to supply the highest-grade press hardened steel for the most demanding EV battery protection applications in the region.

BMW Group, Audi, and Mercedes-Benz continue increasing aluminium sheet content in outer body panels including hood, door skins, and trunk lids at their premium models, reducing the total AHSS volume available per vehicle even as press hardened steel content in structural applications grows. At BMW Group 2024 model portfolio, aluminium accounted for approximately 60% of outer body panel weight at its high-end models versus approximately 40% at its mass-market models, creating a product mix effect at ArcelorMittal and ThyssenKrupp automotive steel supply chains. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated European steel mill energy costs through LNG and natural gas price elevation of approximately EUR 8 to EUR 14 per MWh above the 2024 baseline for blast furnace and EAF steelmaking operations in Germany, France, and Italy, adding approximately USD 30 to USD 60 per metric tonne to European AHSS production cost and sustaining the European premium above Asian AHSS pricing. These factors substantially limit automotive advanced high strength steel market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product Type | Dual Phase Steel, TRIP Steel, Complex Phase Steel, Martensitic Steel, Press Hardened Steel | Dual Phase Steel |

| Application | Body-in-White, Chassis and Suspension, Bumpers and Crash Management, Door Intrusion Beams, Pillars | Body-in-White |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles | Passenger Cars |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Dual Phase Steel segment is expected to account for a significantly large revenue share in the global automotive advanced high strength steel market during the forecast period.

This report evaluates product type across Dual Phase Steel, TRIP Steel, Complex Phase Steel, Martensitic Steel, Press Hardened Steel for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Body-in-White, Chassis and Suspension, Bumpers and Crash Management, Door Intrusion Beams, Pillars for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for steel, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

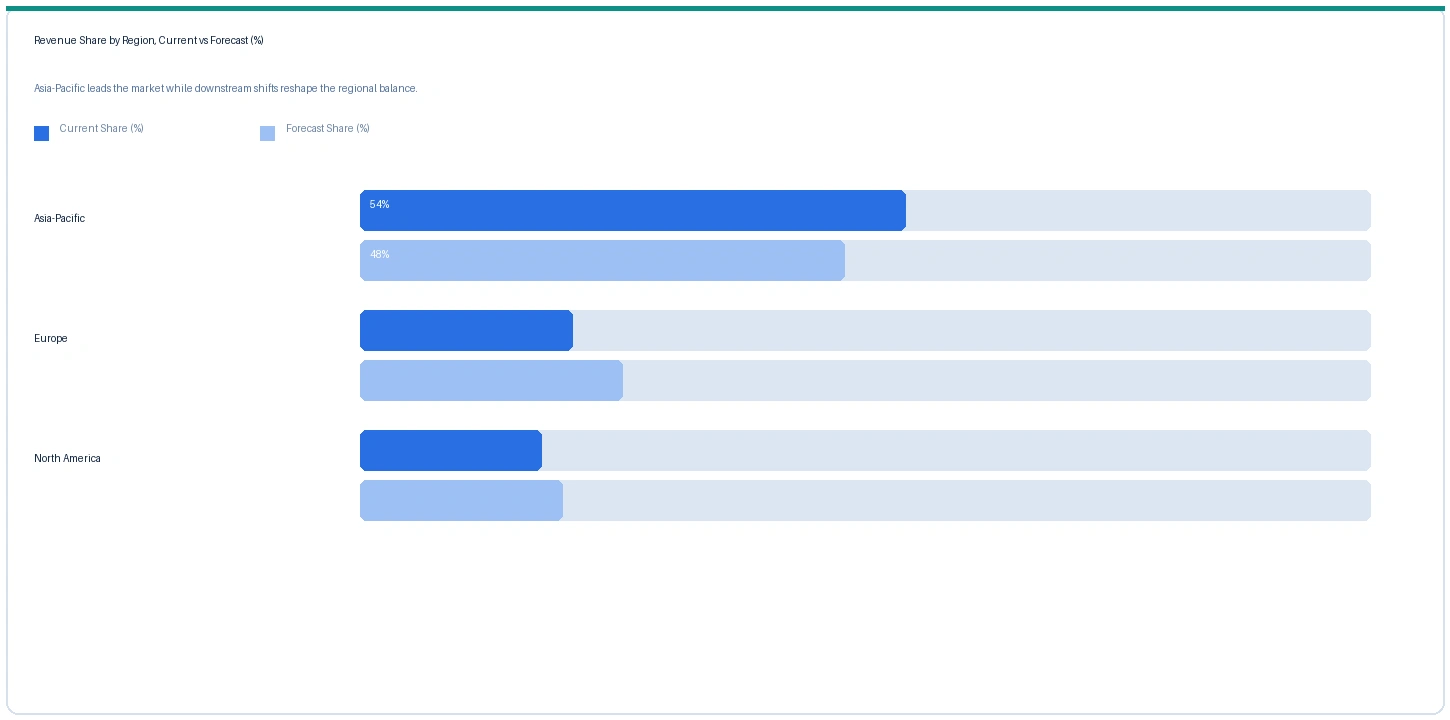

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive advanced high strength steel market in 2025. Based on regional analysis, the automotive advanced high strength steel market in Asia-Pacific accounted for largest revenue share in 2025. China alone accounted for approximately 45% to 50% of global automotive AHSS consumption, driven by above-30-million-unit annual passenger vehicle production at Baowu Group, POSCO Zhangjiagang, and ArcelorMittal's Chinese joint ventures supplying domestic OEMs and international brands. South Korea's POSCO at Pohang and Gwangyang and Japan's Nippon Steel at Nagoya and Kimitsu are the primary export sources of highest-grade press hardened steel for global EV battery protection applications.

Europe market accounted for second largest revenue share in the global automotive advanced high strength steel market in 2025. The market in Europe is expected to register the second largest revenue share. ArcelorMittal's European Flat Products division, ThyssenKrupp Steel Europe, voestalpine Automotive Components, and Tata Steel's Ijmuiden, Netherlands facility supply European OEM body shops with dual phase, TRIP, and press hardened steel grades. European AHSS pricing at USD 1,240 per metric tonne for press hardened steel in Q2 2026 carries a USD 60 per metric tonne premium above Asian pricing, reflecting energy cost elevation from Hormuz-related LNG disruption at European steelmaking operations.

North America market is expected to register steady revenue growth in the global automotive advanced high strength steel market during the forecast period. The market in North America is anchored in ArcelorMittal's AM/NS Calvert Alabama facility following its June 2025 acquisition of full ownership, Nucor Corporation, United States Steel (now integrated with Nippon Steel following June 2025 acquisition), and Cleveland-Cliffs supplying advanced automotive steel to Ford, General Motors, Stellantis, BMW Group Plant Spartanburg, and Mercedes-Benz Vance assembly operations. SSAB's April 2025 Alabama plant tempering furnace expansion increases North American Hardox and Strenx high-strength steel capacity serving automotive and industrial markets.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Press Hardened Steel (PHS Usibor 1500) | Europe | USD 1,240/MT | USD 1,140/MT | Rising | ArcelorMittal ref |

| Press Hardened Steel (PHS Usibor 1500) | Asia-Pacific | USD 1,180/MT | USD 1,080/MT | Rising | POSCO / NSSMC ref |

| Dual Phase Steel DP 780 | Europe | USD 900/MT | USD 840/MT | Rising | ThyssenKrupp ref |

| Dual Phase Steel DP 780 | Asia-Pacific | USD 860/MT | USD 800/MT | Stable | Baowu / POSCO ref |

| TRIP Steel 590 | Europe | USD 940/MT | USD 880/MT | Rising | voestalpine ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, steel producer commercial disclosures, and automotive procurement market intelligence. Prices vary by grade, tensile strength, processing route, and supply agreement structure.

European press hardened steel prices rose approximately 8.8% in Q2 2026 against Q2 2025, driven by energy cost elevation at European blast furnace and EAF steelmaking operations from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which restricted GCC LNG exports and elevated European natural gas and electricity costs at integrated steel mills in Germany, France, Belgium, and the Netherlands by approximately EUR 8 to EUR 14 per MWh above 2024 baseline levels. Asian press hardened steel prices rose approximately 9.3% at POSCO and Nippon Steel on coking coal and iron ore supply chain cost increases from the broader global commodity disruption from Hormuz. European dual-phase DP 780 prices rose approximately 7.1% in Q2 2026 against Q2 2025, with the Europe-Asia DP 780 differential at approximately USD 40 per metric tonne in Q2 2026.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive advanced high strength steel market, the Hormuz disruption operates through two primary cost channels. European steelmaking operations at ArcelorMittal Dunkirk, ThyssenKrupp Duisburg, and voestalpine Linz use LNG and natural gas for furnace heating and heat treatment processes that are directly exposed to European LNG cost elevation from disrupted GCC LNG exports, adding approximately EUR 8 to EUR 14 per MWh to European steelmaking energy cost above 2024 baseline and contributing approximately USD 30 to USD 60 per metric tonne to European AHSS production cost in Q2 2026. The secondary impact is coking coal and iron ore logistics cost elevation from disrupted GCC crude oil tanker traffic, which affects freight rates on all bulk commodity shipping including dry bulk vessels carrying iron ore from Brazil and Australia to European and Asian steel mills.

Company Insights

The two key dominant companies in the automotive advanced high strength steel market are ArcelorMittal and POSCO, recognised for their leadership in press hardened steel technology development and production, their established OEM qualification relationships across European, North American, and Asian automotive programmes, and their integrated production models spanning mining, steelmaking, and automotive-grade cold-rolling and coating operations.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 19.62 Billion |

| Market Size 2032 | USD 30.91 Billion |

| CAGR | 6.7% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product Type, By Application, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Sweden, Austria, China, Japan, South Korea, India, Brazil, South Africa |

| Companies Profiled | ArcelorMittal, POSCO, Nippon Steel, ThyssenKrupp Steel Europe, Tata Steel, SSAB, voestalpine, US Steel, Nucor, Cleveland-Cliffs, Baowu Group, Hyundai Steel |

| Key Data Sources | ArcelorMittal annual results and investor presentations, POSCO annual report, SSAB Alabama expansion announcement April 2025, AM/NS India automotive steel line launch January 2025, ArcelorMittal AM/NS Calvert acquisition completion June 2025, Nippon Steel US Steel acquisition completion June 2025, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, SIAM Indian vehicle production statistics FY2025, Euro NCAP and NHTSA side-impact battery protection test protocol documentation, IMF March 2026 Strait of Hormuz statement, 18 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 274 |

| Published | Q2 2026 |

| SKU | NXC-AT-003 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 18 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included automotive AHSS commercial managers at European, Asian, and North American integrated steel producers, press hardening process engineers at hot stamping Tier 1 suppliers, and automotive steel technical application specialists. Demand-side contacts included BIW and body structure material procurement engineers at European premium OEMs, EV platform battery protection frame structural engineers at Asian EV manufacturers, and automotive AHSS specification engineers at Indian and Southeast Asian vehicle producers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include ArcelorMittal annual results, Fortiform 1500 product launch communications, AM/NS Calvert acquisition completion announcement June 2025, AM/NS India automotive steel line launch announcement January 2025, POSCO GIGA STEEL product communications, SSAB Alabama expansion announcement April 2025, Nippon Steel US Steel acquisition completion announcement June 2025, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, SIAM FY2025 Indian vehicle production data, Euro NCAP side-impact battery protection test protocol updates, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.