Market Data

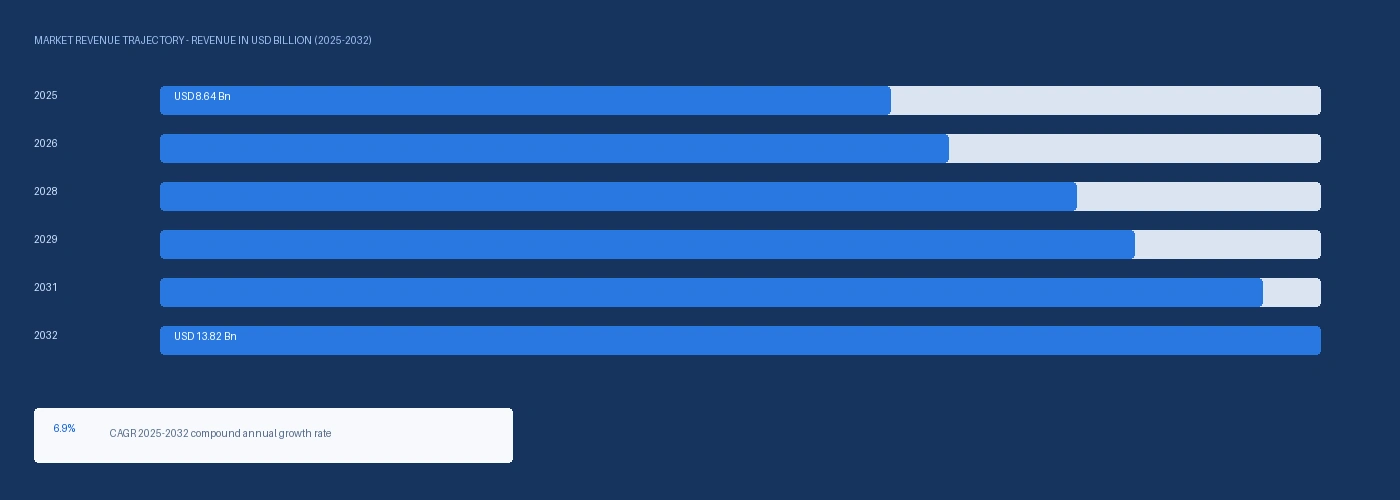

The global automotive adhesives market size was USD 8.64 Billion in 2025 and is expected to register a revenue CAGR of 6.9% during the forecast period. Market revenue growth is supported by EV battery module structural potting adhesive demand growing at approximately 20% to 25% per year as CATL, BYD, and LG Energy Solution expand cell-to-pack and module-to-pack battery architectures requiring 1.5 to 3.0 kilograms of structural epoxy or polyurethane adhesive per battery pack, Henkel Adhesive Technologies Mobility and Electronics business area generating approximately EUR 3.96 Billion in revenue in 2024 at 36% of EUR 11 Billion Adhesive Technologies per Henkel Annual Report 2024 with automotive as the largest downstream application, and multi-material body-in-white structural bonding demand from premium European OEMs growing as aluminium-intensive and CFRP-aluminium-steel hybrid body structures replace conventional all-steel monocoque designs. OICA confirmed global passenger vehicle production of approximately 92 million units in 2024, with each premium platform incorporating 8 to 12 kilograms of structural adhesive per vehicle in hem flange, structural reinforcement, and anti-flutter applications versus 3 to 5 kilograms in standard steel body designs. ArcelorMittal S-in motion and ThyssenKrupp automotive steel technical studies confirm that multi-material vehicle bodies with aluminium closures and AHSS BIW require continuous structural adhesive beads at dissimilar material joints that cannot be resistance spot welded without galvanic corrosion risk. For instance, in Q1 2025, Henkel AG, Germany, announced a strategic partnership with a leading Chinese electric vehicle manufacturer to co-develop advanced structural adhesives for EV battery module assembly and lightweight body applications, marking Henkel's first publicly disclosed Chinese domestic OEM co-development partnership for EV-specific adhesive systems. These are some of the key factors driving revenue growth of the market.

Two-component epoxy structural adhesive was indicatively priced at USD 6,240 per metric tonne in Europe in Q2 2026, representing an 8.9% increase against Q2 2025 driven by bisphenol A and epichlorohydrin epoxy resin feedstock cost elevation from Hormuz-related naphtha disruption at European cracker feedstock supply chains. Dow's BETAFORCE two-component polyurethane structural adhesive for aluminium-to-steel BIW bonding and BASF's structural crash adhesive systems for European premium OEMs are both increasing in per-unit price alongside rising MDI isocyanate feedstock costs. Silane modified polymer adhesives, confirmed as the fastest-growing resin type by multiple automotive adhesive technical publications, are gaining share in exterior panel bonding and glass-to-metal applications at European and Asian OEMs because they require no primers, generate zero volatile organic compounds during cure, and provide elastic bonding characteristics compatible with mixed aluminium and steel panel thermal expansion coefficients. H.B. Fuller confirmed automotive adhesive revenue growth in its FY2024 earnings, with reactive hot melt and two-component epoxy adhesives for North American EV battery tier-one assembly suppliers representing the growth drivers within its engineering adhesives division.

However, two-component epoxy and polyurethane structural adhesives require automated dispensing and mixing equipment at OEM assembly plants that represent fixed capital investment preventing rapid supplier switching at production lines where adhesive is specified as part of process validation. The cure time requirement of two-component epoxy structural adhesives at room temperature or elevated cure processes creates throughput constraints at high-volume body shop assembly lines relative to resistance spot welding cycle times, limiting per-joint adhesive bonding replacement of spot welds to hem flanges and specific multi-material joints rather than wholesale substitution. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated both MDI isocyanate and bisphenol A feedstock costs at European automotive structural adhesive producers, compressing margins on existing OEM annual supply agreements priced before the disruption. These factors substantially limit automotive adhesives market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Cell-to-pack and module-to-pack EV battery architectures require structural potting adhesive to encapsulate cell arrays in aluminium or composite module housings, providing both mechanical load-bearing at 1.5 to 3.0 kilograms per battery pack and thermal isolation between cells that prevents thermal runaway propagation. CATL's cell-to-pack architecture, which eliminates the module layer and bonds prismatic cells directly to pack structure using continuous structural adhesive, consumes approximately 2.0 to 2.5 kilograms of two-component epoxy adhesive per pack with a tensile strength specification above 15 MPa to maintain pack integrity through vehicle lifetime thermal cycling. Henkel's LOCTITE EA 9466 and EA 9480 series structural epoxy adhesives are qualified at multiple European and Asian EV battery pack assembly programmes, with Henkel's Q2 2024 battery testing centre at Dusseldorf enabling accelerated qualification testing that reduces the typical 12 to 18 month adhesive qualification timeline for new EV battery programmes. Silane Modified Polymer Adhesives Gaining Share from Isocyanate and Epoxy Systems in Exterior Bonding Silane modified polymer structural adhesives have captured approximately 18% to 22% of the exterior panel bonding and trim attachment adhesive market in Europe by 2025, driven by their zero VOC emission profile, isocyanate-free chemistry that avoids REACH diisocyanate professional use regulation compliance burden, and primer-free adhesion to aluminium, galvanised steel, painted surfaces, and glass simultaneously. Sika's Sikaflex SMP range and Henkel's TEROSON MS 935 and MS 939 SMP adhesives represent the primary commercial products in this segment, with European Tier 1 body shop operators including Magna Steyr and Karmann specifying SMP adhesive at aluminium closure-to-steel hinge mounting joints on SUV programmes where thermal expansion differential between aluminium door and steel hinge requires elastic bonding rather than rigid epoxy. The European Chemicals Agency REACH restriction on diisocyanates in professional use effective from 2023 has accelerated evaluation of SMP as an alternative to one-component polyurethane in some exterior adhesion applications.

Two-component structural adhesive application requires automated metering, mixing, and dispensing equipment at OEM body shop assembly lines that represents a capital investment of EUR 200,000 to EUR 400,000 per application station, with the mix ratio and dispensing programme validated as part of the body shop process qualification. This equipment investment creates incumbent supplier lock-in that limits re-sourcing at validated OEM production lines within annual contract cycles. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated both MDI isocyanate for polyurethane adhesive and bisphenol A diglycidyl ether for epoxy adhesive feedstock costs at European structural adhesive producers, adding approximately USD 60 to USD 90 per metric tonne to European reactive adhesive production cost in Q2 2026 and compressing margins on pre-negotiated OEM annual supply contracts. These factors substantially limit automotive adhesives market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Resin Type | Epoxy, Polyurethane, Acrylic, Methyl Methacrylate, Silane Modified Polymer | Epoxy |

| Application | Structural Bonding, Hem Flange, Anti-Flutter and NVH, EV Battery Assembly, Powertrain | Structural Bonding |

| Technology | Two-Component, One-Component, Reactive Hot Melt | Two-Component |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Electric Vehicles | Passenger Cars |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Epoxy Resin segment is expected to account for a significantly large revenue share in the global automotive adhesives market during the forecast period.

This report evaluates resin type across Epoxy, Polyurethane, Acrylic, Methyl Methacrylate, Silane Modified Polymer for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Structural Bonding, Hem Flange, Anti-Flutter and NVH, EV Battery Assembly, Powertrain for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates technology across Two-Component, One-Component, Reactive Hot Melt for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Electric Vehicles for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

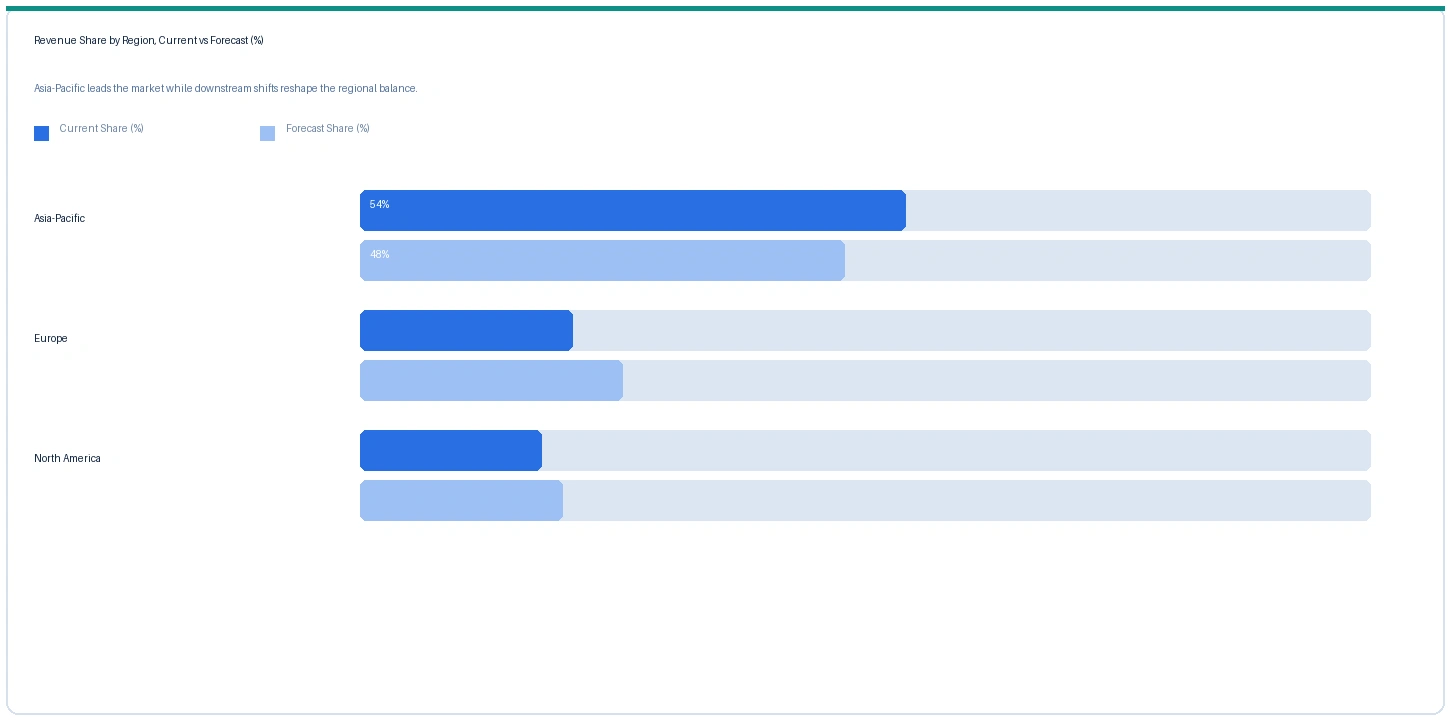

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive adhesives market in 2025. Based on regional analysis, the automotive adhesives market in Asia-Pacific accounted for largest revenue share in 2025. China, South Korea, Japan, and India collectively account for approximately 55% to 60% of global automotive adhesive consumption by volume, driven by the region's dominance in global vehicle production and rapidly expanding EV production at CATL-supplied battery assembly operations. Henkel's partnership with a leading Chinese EV OEM confirmed in Q1 2025 and Sika's content expansion at Chinese domestic manufacturers confirmed in its 2024 full-year results demonstrate that both leading European adhesive producers are executing Asia-Pacific EV content capture strategies.

The market in Europe is expected to register the second largest revenue share. European automotive structural adhesive demand benefits from the highest per-vehicle structural adhesive content globally, with premium OEM programmes at BMW Group, Volkswagen Group, Mercedes-Benz, and Audi incorporating 8 to 12 kilograms of crash-durable epoxy structural adhesive per vehicle at body shop prices of USD 5,000 to USD 7,000 per metric tonne. ACEA confirmed European car production of approximately 11.1 million units in 2024, below 2019 levels, creating volume headwinds that are partially offset by increasing adhesive content per vehicle from lightweighting programmes.

North America market is expected to register steady revenue growth in the global automotive adhesives market during the forecast period. The market in North America is supported by H.B. Fuller, 3M, Dow Inc., and Illinois Tool Works supplying structural adhesives to North American OEM body shops and EV battery assembly programmes. Inflation Reduction Act-supported gigafactory construction at Panasonic Kansas, Toyota Battery Manufacturing North Carolina, and Stellantis-Samsung SDI Indiana is generating battery pack structural adhesive demand that is being sourced locally to meet domestic content requirements where available.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Two-Component Epoxy Structural (crash-durable) | Europe | USD 6,240/MT | USD 5,720/MT | Rising | Henkel TEROSON EP ref |

| Two-Component PU Structural Adhesive | Europe | USD 5,480/MT | USD 5,020/MT | Rising | Dow BETAFORCE ref |

| Silane Modified Polymer (SMP) Adhesive | Europe | USD 4,180/MT | USD 3,840/MT | Rising | Sika/Henkel SMP ref |

| Reactive Hot Melt PU Adhesive | Asia-Pacific | USD 3,680/MT | USD 3,360/MT | Rising | Interior trim ref |

| One-Component Anaerobic / Threadlocker | North America | USD 12,400/MT | USD 11,600/MT | Rising | Henkel LOCTITE ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and automotive OEM supply chain monitoring. Prices vary by chemistry, cure system, tensile strength specification, and OEM qualification status.

Two-component epoxy structural crash-durable adhesive prices in Europe rose approximately 9.1% in Q2 2026 against Q2 2025, driven by bisphenol A and epichlorohydrin epoxy resin feedstock cost increases from Hormuz-related naphtha disruption and Hexion and Olin Corporation epoxy resin price increases passed through the adhesive formulation supply chain. Two-component polyurethane structural adhesive rose approximately 9.2% in Europe on MDI diisocyanate feedstock cost elevation. Silane modified polymer adhesive rose approximately 8.9% as dimethoxy and trimethoxy silane raw material costs increased in line with methanol and silicon metal input prices.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive adhesives market, the Hormuz disruption elevates feedstock costs for both dominant adhesive chemistries simultaneously. Epoxy resin producers including Hexion, Olin Corporation, and KUKDO Chemical source bisphenol A from phenol-acetone plants and epichlorohydrin from propylene-based allyl chloride synthesis, both affected by Hormuz-driven naphtha and propylene cost elevation at European and Asian integrated chemical facilities. MDI isocyanate for polyurethane structural adhesives is produced from benzene and aniline intermediates affected by the same naphtha cost disruption. Combined feedstock cost increases are adding approximately USD 60 to USD 90 per metric tonne to European structural adhesive production cost in Q2 2026, flowing into the above-plan price increases documented in the price tracker.

Company Insights

The two key dominant companies in the automotive adhesives market are Henkel AG and Dow Inc., recognised for their structural adhesive technology leadership in crash-durable epoxy and polyurethane systems for European premium OEM multi-material body structures, their established engineering qualification relationships with BMW, Volkswagen Group, and Mercedes-Benz body shop programmes, and their expanding EV battery assembly structural potting adhesive portfolios.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 8.64 Billion |

| Market Size 2032 | USD 13.82 Billion |

| CAGR | 6.9% |

| Units | Revenue in USD Billion |

| Segments Covered | By Resin Type, By Application, By Technology, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, China, Japan, South Korea, India, Brazil |

| Companies Profiled | Henkel AG, Dow Inc., Sika AG, 3M, H.B. Fuller, BASF SE, Bostik, Illinois Tool Works, Huntsman, Permabond, Delo, Technicoll |

| Key Data Sources | Henkel Annual Report 2024, Dow Inc. China adhesive investment press release August 2023, Sika AG 2024 full-year results, ArcelorMittal S-in motion technical documentation, OICA 2024 vehicle production statistics, IEA Global EV Outlook 2025, ACEA European vehicle production 2024, EU REACH diisocyanate restriction regulation, IMF March 2026 Strait of Hormuz statement, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 258 |

| Published | Q2 2026 |

| SKU | NXC-AT-002 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 16 expert interviews conducted between January and May 2026, structured across a 2x2 supply-side and demand-side grid. Supply-side contacts included automotive structural adhesive product managers and commercial leads at European and Asian producers, dispensing equipment engineers at body shop automation system integrators, and EV battery pack structural adhesive technical leads. Demand-side contacts included BIW structural adhesive specification engineers at European premium OEMs, EV battery pack assembly procurement managers at Chinese and Korean battery tier-ones, and body shop materials procurement leads at North American OEM assembly plants. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Henkel AG Annual Report 2024, Dow Inc. China capacity expansion announcement August 2023, Sika AG Full Year 2024 Results, ArcelorMittal S-in motion multi-material body structure technical documentation, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, ACEA 2024 European production data, EU Commission REACH diisocyanate restriction regulation, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.