Market Data

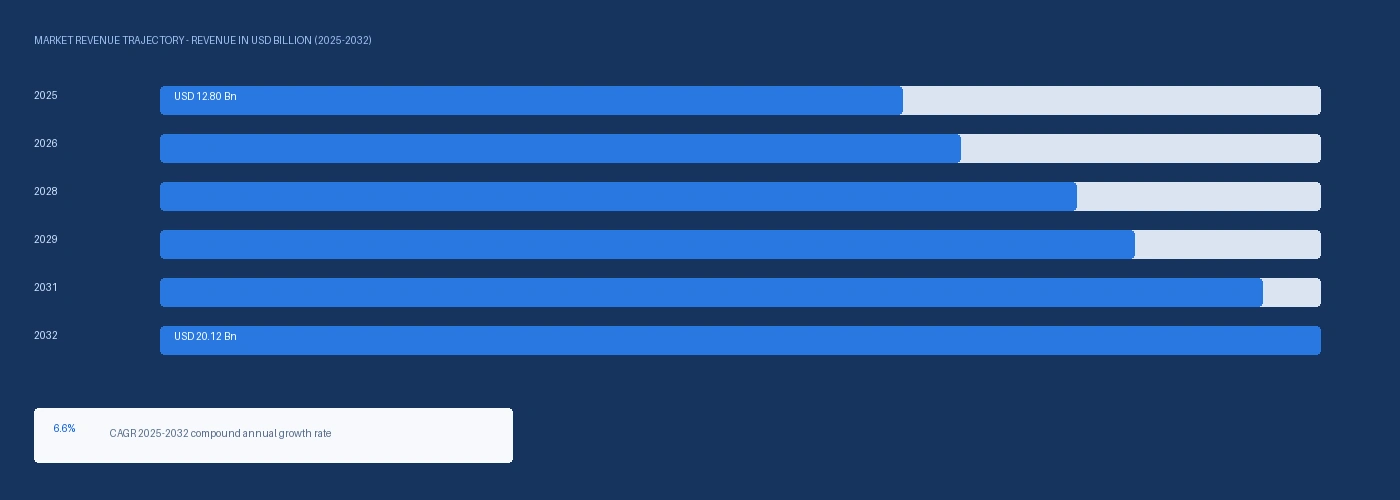

The global automotive adhesives and sealants market size was USD 12.80 Billion in 2025 and is expected to register a revenue CAGR of 6.6% during the forecast period. Market revenue growth is supported by EV platform battery module encapsulation and thermal gap pad bonding consuming three to five kilograms of reactive polyurethane and epoxy adhesive per vehicle above the ICE adhesive load, Henkel Adhesive Technologies generating approximately 20% of its EUR 11 Billion 2024 revenue from automotive applications per Henkel Annual Report 2024, and Sika AG expanding its automotive and industrial adhesive and sealant content per vehicle in China, Japan, and India through 2024 as confirmed in its full-year 2024 results. OICA confirmed global passenger vehicle production of approximately 92 million units in 2024, with each conventional ICE platform consuming approximately 15 to 20 kilograms of adhesives and sealants across body-in-white structural bonding, windshield glazing, powertrain sealing, and interior trim assembly. EV platforms require substantially higher adhesive content than ICE equivalents, with battery module assembly consuming thermally conductive adhesive gap filler at 800 to 1,200 grams per cell module, structural battery pack bonding at 1.5 to 3.0 kilograms per vehicle, and copper bus bar isolation at 200 to 400 grams per vehicle, contributing an incremental 5 to 8 kilograms of reactive adhesive demand per EV above ICE baseline consumption. Dow announced a USD 40 million investment in China in August 2023 to enhance its automotive adhesives and sealants production capacity, increasing Chinese capacity by 20% and targeting EV platform assembly demand from BYD and SAIC. For instance, in Q4 2024, Sika AG, Switzerland, opened a new adhesives and sealants manufacturing facility in Pune, India, targeting the Indian automotive OEM market including Maruti Suzuki, Tata Motors, and Mahindra with localised production of structural bonding and glazing adhesives, reducing import lead times and supporting Sika's strategy to expand content per vehicle in Asian automotive markets. These are some of the key factors driving revenue growth of the market.

Henkel Adhesive Technologies Mobility and Electronics business area, accounting for approximately 36% of the EUR 11 Billion adhesive technologies segment revenue in 2024, includes automotive structural bonding, EV battery thermal management adhesives, powertrain sealing, and body shop hem flange adhesives across its LOCTITE and TEROSON product lines. Sika confirmed in its 2024 annual results that the automotive and industrial adhesive business declined in Europe on lower new vehicle demand while continuing to increase content per vehicle in China and India where EV production growth offset ICE volume softness. H.B. Fuller disclosed automotive adhesive revenue growth driven by structural adhesives for EV battery assembly in its FY2024 earnings, with the company supplying reactive hot melt and two-component epoxy adhesives to North American and Asian EV battery tier-one suppliers. 3M supplies automotive structural adhesive tapes and window bonding adhesives including its VHB tape product family to European body shop assembly lines, with automotive transportation consuming a significant share of its safety and industrial segment revenue.

However, automotive adhesive and sealant formulations using isocyanate-based polyurethane chemistry face REACH Annex XVII restriction requirements for diisocyanate professional use training from February 2023, adding compliance cost to one-component and two-component polyurethane adhesive production at European body shop applications where PU adhesives dominate window bonding and hem flange applications. European automotive production remained below 2019 peak levels in 2024 per OICA data, with German vehicle production declining materially in a challenging demand environment that Henkel identified in its 2024 annual report as weighing on the Adhesive Technologies Mobility segment despite above-market organic growth. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated MDI isocyanate feedstock costs at European polyurethane adhesive producers through methylene diphenyl diisocyanate upstream naphtha cost elevation, adding approximately USD 60 to USD 90 per metric tonne to reactive PU adhesive production cost in Q2 2026. These factors substantially limit automotive adhesives and sealants market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Battery electric vehicle architectures require thermally conductive gap filler adhesive between battery cells and cooling plates, structural potting adhesive to encapsulate cell arrays within module housings, and sealing adhesive at battery pack perimeter joints where ingress protection ratings of IP67 or IP68 require continuous bead-applied silicone or polyurethane sealant. Henkel confirmed in its 2024 Annual Report that the e-mobility segment represented 20% of its automotive adhesive and sealant sales and that it opened a battery testing centre at its Dusseldorf headquarters in 2024, directly connected to its global innovation centre, to expand EV adhesive development capabilities. CATL disclosed approximately 700 gigawatt-hours of annual battery production capacity in its 2024 annual report, and at 500 to 800 kilograms of thermally conductive adhesive per gigawatt-hour of module assembly, CATL alone is consuming an estimated 350,000 to 560,000 metric tonnes per year of battery assembly adhesive across its global network. Sika's investment in EV-specific structural adhesive and thermal management material product lines positions it to capture content-per-vehicle increases at Chinese domestic OEMs including BYD and NIO that are rapidly expanding EV production. Lightweighting Multi-Material Body Structure Bonding Driving Structural Adhesive Demand Multi-material automotive body structures combining advanced high-strength steel, aluminium sheet, carbon fibre reinforced plastic, and glass fibre reinforced thermoplastic panels require structural adhesive to join dissimilar materials that cannot be spot welded without galvanic corrosion risk or thermal distortion. Dow's BETAFORCE structural adhesive range, BASF's structural adhesive systems for CFRP-steel hybrid bonding, and Henkel's TEROSON structural adhesive for aluminium-intensive vehicle body structures each address the multi-material BIW requirement. The European Automobile Manufacturers Association ACEA confirmed European car production of approximately 11.1 million units in 2024, with premium segment vehicles at BMW Group, Mercedes-Benz, and Stellantis Premium Brands incorporating multi-material BIW structures that require 8 to 12 kilograms of structural adhesive per vehicle.

EU Commission Regulation on diisocyanates under REACH Article 68 requires industrial and professional users of isocyanate-containing adhesives and sealants to complete formal training programmes from 24 February 2023, with non-compliance potentially restricting supply in the European market for one-component PU body seam sealers and two-component PU structural bonding adhesives that dominate European BIW and glazing applications. European automotive OEM production softness in 2024, specifically in Germany where Henkel identified market challenges in its 2024 Annual Report, constrained adhesive volume growth in the region with the highest per-vehicle structural bonding adhesive content globally. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 elevated MDI feedstock costs at European polyurethane adhesive producers, with naphtha cost increases from Hormuz-restricted GCC exports adding approximately USD 60 to USD 90 per metric tonne to European reactive PU adhesive production cost in Q2 2026. These factors substantially limit automotive adhesives and sealants market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Technology | Solvent-Based, Water-Based, Hot Melt, Reactive | Solvent-Based |

| Resin Type | Epoxy, Polyurethane, Silicone, Acrylic, Silane Modified Polymer | Epoxy |

| Application | Body-in-White, Glazing, Powertrain, Paint Shop, Interior and Upholstery | Body-in-White |

| Vehicle Type | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles | Passenger Cars |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Reactive Technology segment is expected to account for a significantly large revenue share in the global automotive adhesives and sealants market during the forecast period.

This report evaluates technology across Solvent-Based, Water-Based, Hot Melt, Reactive for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates resin type across Epoxy, Polyurethane, Silicone, Acrylic, Silane Modified Polymer for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Body-in-White, Glazing, Powertrain, Paint Shop, Interior and Upholstery for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates vehicle type across Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

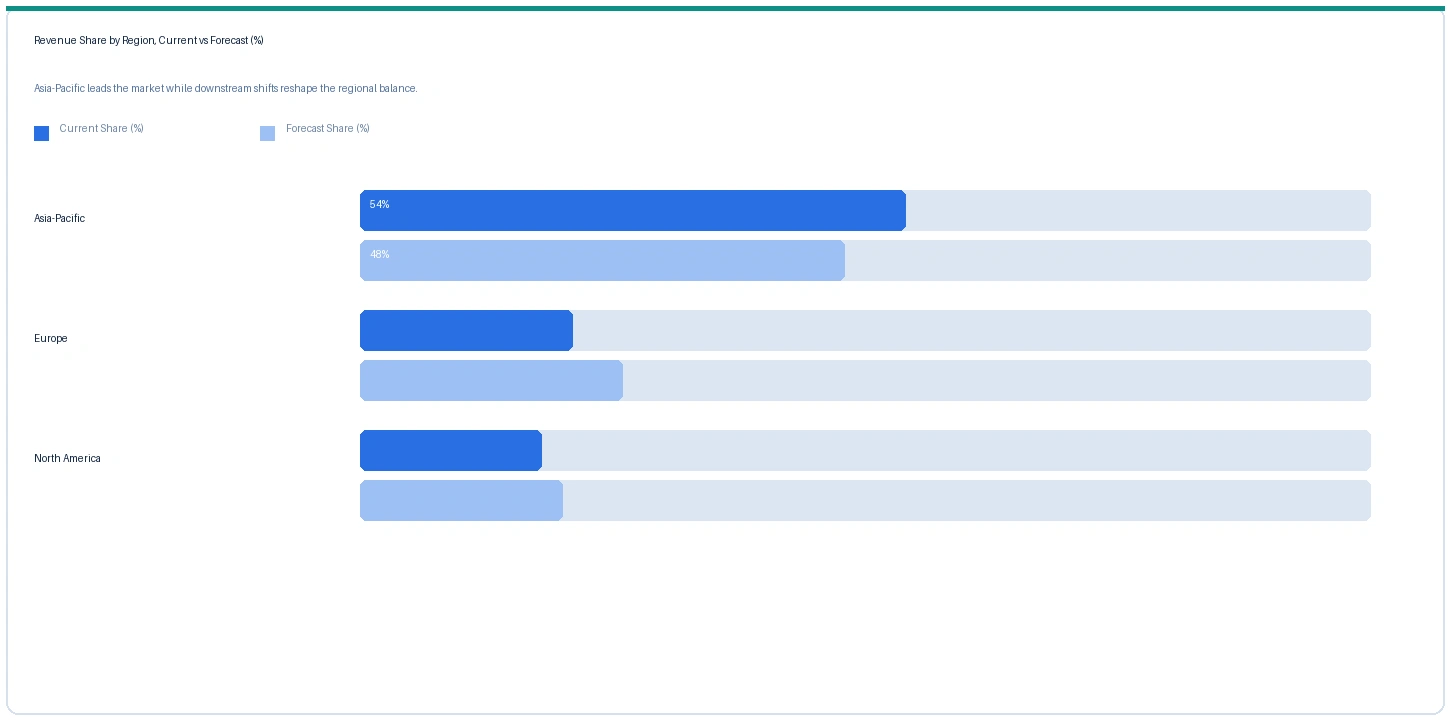

Asia-Pacific market accounted for largest revenue share over other regional markets in the global automotive adhesives and sealants market in 2025. Based on regional analysis, the automotive adhesives and sealants market in Asia-Pacific accounted for largest revenue share in 2025. China accounted for approximately 21% of global automotive adhesive and sealant market revenue in 2025, driven by the world's largest single-country automotive production base at approximately 30 million units per year and the fastest-growing EV production volume globally. Sika confirmed in its 2024 full-year results that it continued to increase the share of its technologies in vehicles of local and international manufacturers in China, Japan, and India in its automotive and industrial business segment, with Chinese EV OEM content growth partially offsetting ICE segment softness.

Europe market accounted for second largest revenue share in the global automotive adhesives and sealants market in 2025. The market in Europe is expected to register the second largest revenue share. Henkel's Adhesive Technologies business confirmed that the automotive market in Germany faced particular challenges in 2024 in its Annual Report while the company outperformed overall market growth. BASF and Dow supply structural adhesive systems for body shop hem flange and BIW bonding at German premium OEMs BMW, Volkswagen Group, and Mercedes-Benz, with premium platforms incorporating multi-material bonding that commands above-average adhesive value per vehicle.

North America market is expected to register steady revenue growth in the global automotive adhesives and sealants market during the forecast period. The market in North America is supported by Inflation Reduction Act electric vehicle manufacturing incentives generating new battery plant assembly lines at Panasonic Kansas, Toyota Battery Manufacturing North Carolina, and Stellantis-Samsung SDI Indiana, each requiring thermally conductive adhesive and structural battery pack bonding systems.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| One-Component PU Glazing Adhesive | Europe | USD 4,840/MT | USD 4,420/MT | Rising | Sika Sikaflex ref |

| Two-Component Epoxy Structural | Europe | USD 6,240/MT | USD 5,680/MT | Rising | Henkel TEROSON ref |

| Thermally Conductive Gap Filler | Global | USD 18,400/MT | USD 16,800/MT | Rising | EV battery grade |

| Reactive Hot Melt PU Adhesive | Asia-Pacific | USD 3,680/MT | USD 3,360/MT | Rising | Interior trim ref |

| Body Seam Sealer (PVC-Based) | North America | USD 2,140/MT | USD 1,980/MT | Stable | Body shop ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and automotive supply chain monitoring. Prices vary by chemistry, application, volume, and OEM qualification status.

One-component polyurethane glazing adhesive prices in Europe rose approximately 9.5% in Q2 2026 against Q2 2025, driven by MDI isocyanate feedstock cost elevation from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which restricted GCC naphtha exports and maintained European benzene costs above the 2024 baseline. Two-component epoxy structural adhesive rose approximately 9.9% in Europe on MDI and bisphenol A diglycidyl ether feedstock cost increases. Thermally conductive gap filler adhesive rose approximately 9.5% globally as EV battery assembly demand from CATL, BYD, and Panasonic production expansion outpaced thermally conductive filler compound and silicone base polymer supply additions.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the automotive adhesives and sealants market, the Hormuz disruption affects production economics through two feedstock chains. MDI and TDI diisocyanates for polyurethane adhesives are produced from benzene and toluene derived from naphtha at European and Asian crackers exposed to GCC naphtha cost elevation from the Hormuz closure, adding approximately USD 60 to USD 90 per metric tonne to European reactive PU adhesive production cost. Epoxy resin BADGE is produced from bisphenol A and epichlorohydrin, both derived from propylene and benzene also affected by GCC naphtha supply disruption, contributing to two-component epoxy structural adhesive price increases of approximately 9.9% against Q2 2025 in European markets.

Company Insights

The two key dominant companies in the automotive adhesives and sealants market are Henkel AG and Sika AG, recognised for their comprehensive product portfolios covering structural bonding, glazing, powertrain sealing, and EV battery assembly applications, their established OEM supply agreements across European, North American, and Asian automotive manufacturers, and their technical leadership in reactive adhesive formulation for multi-material and electric vehicle body structures.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 12.80 Billion |

| Market Size 2032 | USD 20.12 Billion |

| CAGR | 6.6% |

| Units | Revenue in USD Billion |

| Segments Covered | By Technology, By Resin Type, By Application, By Vehicle Type, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, China, Japan, South Korea, India, Brazil, South Africa |

| Companies Profiled | Henkel AG, Sika AG, H.B. Fuller, 3M, Dow Inc., BASF SE, Bostik, PPG Industries, Illinois Tool Works, Huntsman, Wacker Chemie, Jowat SE |

| Key Data Sources | Henkel Annual Report 2024, Sika AG Full Year 2024 Results, Dow Inc. China adhesive expansion press release August 2023, OICA 2024 vehicle production statistics, CATL 2024 annual battery capacity disclosures, ACEA European vehicle production data, IEA Global EV Outlook 2025, IMF March 2026 Strait of Hormuz statement, 17 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 268 |

| Published | Q2 2026 |

| SKU | NXC-AT-001 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 17 expert interviews conducted between January and May 2026. Interview panels were structured across a 2x2 supply-side and demand-side grid with explicit geographic and role split. Supply-side contacts included automotive adhesive and sealant commercial leads at European and Asian producers, EV battery thermal adhesive technical specialists, and regional distribution managers serving Asian automotive OEM markets. Demand-side contacts included body shop materials procurement managers at European and North American OEMs, EV battery assembly adhesive technical leads at tier-one battery system integrators, and glazing adhesive specification engineers at Asian automotive assembly plants. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Henkel AG Annual Report 2024, Sika AG Full Year 2024 Results and Financial Report 2024, Dow Inc. China adhesive capacity expansion announcement August 2023, OICA 2024 global vehicle production statistics, CATL 2024 annual report battery capacity disclosures, ACEA European Automobile Manufacturers Association production statistics 2024, IEA Global EV Outlook 2025, EU Commission REACH diisocyanate restriction regulation, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.