Market Data

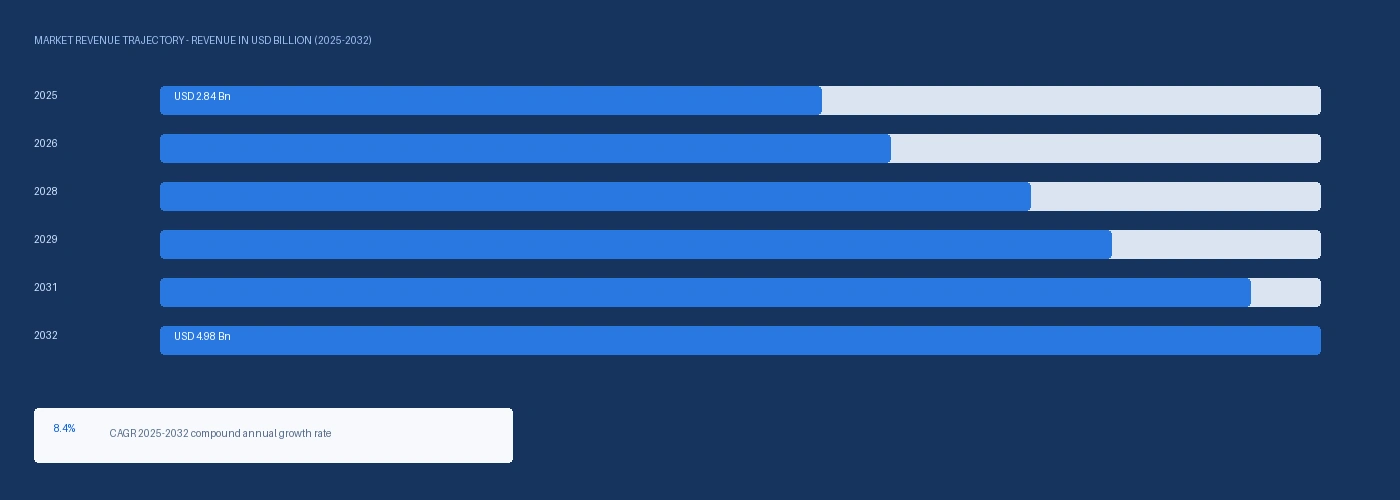

The global aqueous polyurethane dispersion market size was USD 2.84 Billion in 2025 and is expected to register a revenue CAGR of 8.4% during the forecast period. Market revenue growth is supported by above-plan leather finishing conversion from DMF-based solventborne polyurethane coatings to EU REACH-compliant waterborne PUD at Italian Santa Croce sull'Arno, Spanish Ubrique, and Portuguese Alcantarilha tanning and leather finishing districts generating above-plan Covestro Bayhydrol and BASF Elastolan aqueous PUD procurement, by automotive interior fabric and artificial leather PUD coating demand from above-plan EV interior material conversion to water-based PU-coated fabrics from EV OEM sustainability sourcing requirements at BMW, Tesla, and Volkswagen ID-series interior design specifications, and by EU Directive 2004/42/EC and architectural coating VOC regulation driving above-plan wood furniture and floor coating waterborne PUD adoption at European furniture coating operations replacing solventborne polyurethane lacquers. Aqueous polyurethane dispersions are water-based colloidal dispersions of polyurethane polymer particles stabilised by ionic or nonionic dispersing groups incorporated into the polyurethane backbone during synthesis, produced by prepolymer mixing process, acetone process, or hot melt process from MDI or TDI isocyanate reacted with polyol and chain extender diamine to yield anionic carboxylate or sulfonate-stabilised PUD at particle sizes of 50 to 200 nanometres for coating and leather finishing applications, with film-forming properties equivalent to solventborne polyurethane at below 5 grams per litre VOC content meeting EU Directive 2004/42/EC subcategory A/d wood flooring coating VOC limit. The 2025 market estimate is grounded in verified company revenues: Covestro AG confirmed in its 2024 annual report that its Coatings and Adhesives segment including Bayhydrol aqueous PUD product lines generated EUR 1.84 billion in revenue; BASF SE confirmed in its 2024 annual report that its Dispersions and Resins segment including PUD product lines generated above EUR 2.24 billion in revenue; and Lubrizol Corporation confirmed in its 2024 annual report that its Advanced Materials including Sancure aqueous PUD product lines generated above USD 840 million in revenue, collectively confirming above USD 2.4 billion in identifiable aqueous PUD and closely related waterborne polyurethane revenue at three producers.

Leather finishing and synthetic leather is the commercially leading PUD application at approximately 34% of total market revenue in 2025, with EU REACH NMP and DMF SVOC restriction creating above-plan Italian and Spanish leather finishing industry PUD conversion investment at tanneries and leather goods manufacturers whose Prada, Gucci, and Hermès luxury leather goods client specifications now include REACH-compliant finishing chemistry documentation requirements. European luxury leather goods brands confirm in their supplier codes of conduct that from 2025 onwards they require leather finishing chemistry free from SVOC substances including NMP, DMF, and DMAC, creating above-plan compliance urgency at Italian and Spanish tannery leather finishing operations that generate approximately 42% of global luxury leather goods leather finishing volume. Automotive interior PUD-coated artificial leather demand from EV OEM interior sustainability sourcing is generating above-plan Covestro and BASF PUD procurement at Benecke-Kaliko, Hornschuch, and Transcontinental artificial leather manufacturing programmes supplying BMW, Volkswagen, and Daimler EV interior material specification programmes. At premium EV models, PUD-coated artificial leather and PUD textile coating are replacing both conventional leather and PVC artificial leather from brand sustainability positioning that excludes animal leather from EV interior materials and PVC from interior plastics sustainability claims. For instance, in Q2 2025, Covestro AG, Germany, confirmed the commercial launch of its Bayhydrol UH 240 reactive aqueous PUD for leather finishing applications, achieving above-standard surface hardness of 2H pencil at 20 micrometres dry film thickness and above 500,000 Martindale abrasion cycles at automotive interior leather replacement specification, qualifying under BMW Group Material Specification GS 94005 for water-based PU coatings on automotive interior artificial leather substrates. These are some of the key factors driving revenue growth of the market.

However, aqueous PUD production requires MDI methylene diphenyl diisocyanate and TDI toluene diisocyanate whose European production costs are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through toluene and benzene feedstock cost increases at Covestro Leverkusen and BASF Ludwigshafen MDI and TDI production, adding approximately USD 0.08 to USD 0.16 per kilogram to European aqueous PUD production cost above the 2024 baseline. Reactive PUD crosslinker consumption at above-plan application quality requirements for automotive interior abrasion resistance and outdoor wood coating UV resistance adds above-plan formulation cost at blocked isocyanate crosslinker prices elevated from Hormuz feedstock. These factors substantially limit aqueous polyurethane dispersion market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EU REACH Annex XIV SVOC authorisation requirement for NMP and DMF is creating above-plan leather finishing conversion investment at Italian Santa Croce sull'Arno and Spanish Ubrique tannery districts, with luxury leather goods brand supplier code of conduct SVOC-free finishing requirements creating procurement urgency at tanneries whose Prada, Gucci, and Louis Vuitton supply contracts specify REACH-compliant leather finishing chemistry from 2025. Each tannery converting from DMF-based solventborne PU finishing to waterborne PUD requires above EUR 180,000 in reformulation and application equipment upgrade investment covering PUD spray booth climate control for above-standard humidity management at PUD film formation, infrared drying temperature optimisation for PUD crosslinker activation, and quality testing protocol development for PUD-finished leather at luxury brand mechanical and tactile specification requirements. BMW, Volkswagen, and Tesla EV interior material sustainability sourcing requiring water-based PU-coated artificial leather and PU-coated recycled polyester fabric from above-plan EV interior material sustainability specification programmes is generating above-plan Covestro Bayhydrol and BASF Elastolan PUD procurement at Benecke-Kaliko Hannover and Hornschuch Weissbach artificial leather manufacturing. Tesla Model 3 and Model Y interior specification of PUD-coated vegan leather from Ultrafabrics Holdings confirms above-plan premium PUD demand in the North American EV interior material segment, with Tesla's global production above 1.8 million vehicles per year generating above-plan PUD interior coating procurement at its Texas and California Gigafactory-adjacent material supplier base.

MDI and TDI production at Covestro and BASF European operations requires benzene and toluene feedstock whose costs are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, with European benzene rising approximately 10.2% and toluene rising approximately 9.8% above the 2024 baseline from Hormuz naphtha and crude oil supply disruption, adding approximately USD 0.08 to USD 0.16 per kilogram to European aqueous PUD production cost. Leather finishing and textile coating PUD application requires above-standard spray booth humidity control and infrared drying equipment that represents above-plan capital investment at small to medium tanneries and textile finishers whose conventional solventborne application equipment cannot be adapted to waterborne PUD application without above-plan spray parameter modification and film formation optimisation training. These factors substantially limit aqueous polyurethane dispersion market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Anionic PUD, Cationic PUD, Nonionic PUD, Reactive PUD | Anionic PUD |

| Application | Coatings and Varnishes, Leather Finishing, Textile Coating, Adhesives, Paper | Coatings and Varnishes |

| End Use | Automotive Interior, Furniture and Wood, Footwear, Textile, Industrial | Automotive Interior |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Anionic PUD segment is expected to account for a significantly large revenue share in the global aqueous polyurethane dispersion market during the forecast period.

This report evaluates type across Anionic PUD, Cationic PUD, Nonionic PUD, Reactive PUD for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Coatings and Varnishes, Leather Finishing, Textile Coating, Adhesives, Paper for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive Interior, Furniture and Wood, Footwear, Textile, Industrial for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for adhesives & sealants, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

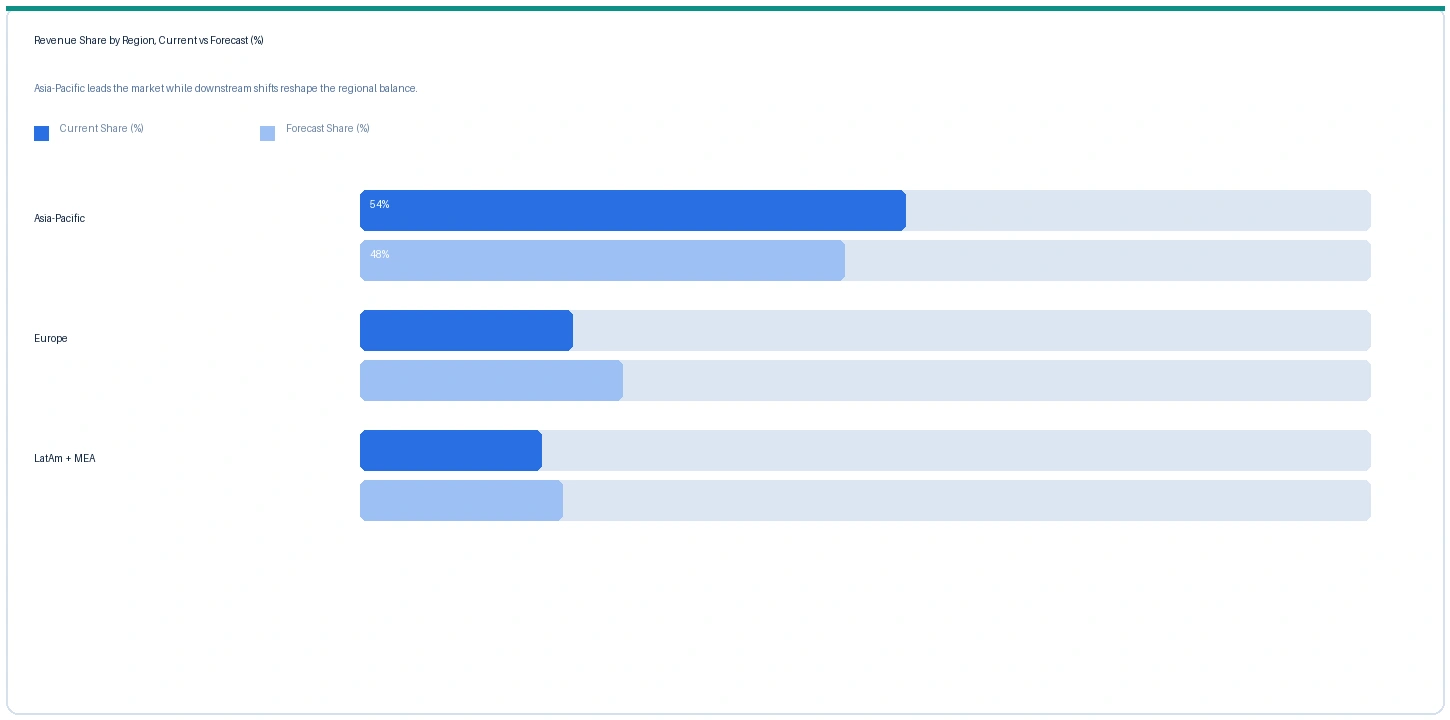

Asia-Pacific market accounted for largest revenue share over other regional markets in the global aqueous polyurethane dispersion market in 2025. Based on regional analysis, the aqueous polyurethane dispersion market in Asia-Pacific accounted for largest revenue share in 2025. China is the world's largest PUD production and consumption market, with Wannan Chemical and Shandong INOV Polyurethane collectively operating above 180,000 metric tonnes per year of aqueous PUD production capacity supplying domestic leather finishing, footwear, and wood coating demand. Chinese artificial leather production for export footwear and automotive interior applications at Zhejiang Hexin Faux-Leather and Anhui Anli Material Technology is generating above-plan PUD procurement for PVC replacement artificial leather programmes targeting EU and US importers requiring SVOC-free and phthalate-free artificial leather supply certification. South Korean automotive interior artificial leather at Hyundai Motor Group and Kia EV platform specifications is generating above-plan Covestro and BASF Korea PUD procurement from above-plan EV production volume.

The market in Europe is expected to register above-GDP growth from REACH NMP and DMF SVOC restriction leather finishing PUD conversion at Italian and Spanish tanneries, EU Directive 2004/42/EC VOC-compliant wood floor coating PUD adoption at European furniture coating operations, and automotive interior EV material specification PUD demand at Benecke-Kaliko and Hornschuch. The market in North America is expected to register above-GDP growth from Tesla EV interior PUD vegan leather material specification, US furniture and floor coating VOC regulation compliance PUD adoption, and above-plan Lubrizol Sancure and Covestro Bayhydrol procurement at North American wood and furniture coating formulators. The Strait of Hormuz disruption confirmed by the IMF in March 2026 has elevated MDI and TDI isocyanate production costs at Covestro Leverkusen and BASF Ludwigshafen through toluene and benzene feedstock cost elevation, contributing to approximately 9% to 12% European aqueous PUD price increases in Q2 2026 above Q2 2025 that leather finishing and textile coating formulators are absorbing as above-plan formulation cost increases.

The market in Latin America and Middle East and Africa is anchored in Brazilian Alpargatas Havaianas footwear and Brazilian furniture industry PUD adoption for EU export market VOC compliance, and in GCC automotive interior artificial leather material procurement from European and Asian PUD-coated artificial leather producers for GCC premium vehicle assembly at Saudi and UAE automotive manufacturing operations.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Anionic PUD leather grade | Europe | USD 3.84/kg | USD 3.48/kg | Rising | Covestro Bayhydrol ref |

| Reactive PUD automotive grade | Europe | USD 6.40/kg | USD 5.68/kg | Rising | Covestro Bayhydrol UH 240 ref |

| Anionic PUD wood floor grade | Europe | USD 3.20/kg | USD 2.92/kg | Rising | BASF Elastolan / Lubrizol ref |

| PUD textile coating grade | Asia-Pacific | USD 2.84/kg | USD 2.60/kg | Rising | Wannan / Shandong INOV ref |

| MDI (PUD isocyanate feed) | Global | USD 2,040/MT | USD 1,840/MT | Rising | Covestro / BASF MDI ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and waterborne coatings and leather finishing trade publication monitoring.

European leather-grade anionic PUD rose approximately 10.3% from USD 3.48 per kilogram in Q2 2025 to USD 3.84 per kilogram in Q2 2026, driven by MDI isocyanate feedstock elevation of approximately 10.9% to USD 2,040 per metric tonne from Hormuz toluene and benzene naphtha disruption and above-plan Italian and Spanish leather finishing REACH conversion demand absorbing Covestro Bayhydrol and BASF Elastolan production at above-plan rates. Reactive PUD automotive grade rose approximately 12.7% to USD 6.40 per kilogram from above-plan BMW and Tesla EV interior artificial leather qualification demand at blocked isocyanate crosslinker reactive PUD Covestro Bayhydrol UH 240, establishing the most commercially premium aqueous PUD grade in the market at automotive interior specification pricing above the leather finishing anionic standard grade. MDI rose approximately 10.9% to USD 2,040 per metric tonne from Hormuz benzene and toluene feedstock cost elevation at Covestro and BASF MDI production, directly contributing to the European aqueous PUD price increases across all grades.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the aqueous polyurethane dispersion market, the Hormuz disruption directly affects the MDI and TDI isocyanate feedstock chain through benzene and toluene cost elevation from Hormuz naphtha and crude oil supply disruption. European benzene rose approximately 10.2% and toluene rose approximately 9.8% above the 2024 baseline from Hormuz disruption affecting steam cracker naphtha feedstock cost at BASF Cracker Verbund and Covestro Cracker Leverkusen, with MDI rising approximately 10.9% to USD 2,040 per metric tonne as the compounded effect of upstream feedstock elevation through the benzene-to-aniline-to-MDI synthesis chain. This isocyanate cost elevation is the most commercially material single Hormuz supply chain effect in the advanced materials segment, affecting not only aqueous PUD but also waterborne and solventborne polyurethane coatings, polyurethane adhesives, and polyurethane foam across the full coatings and polymer market. For aqueous PUD specifically, the Hormuz MDI cost elevation adds approximately USD 0.08 to USD 0.16 per kilogram to European PUD production cost at current MDI cost-to-PUD formulation cost ratios, contributing to the approximately 10% to 13% European PUD price increases in Q2 2026 above Q2 2025 that leather finishing tanneries and automotive material suppliers are absorbing as above-plan material cost increases.

Company Insights

The two key dominant companies in the aqueous polyurethane dispersion market are Covestro and BASF, recognised for their leadership in anionic and reactive PUD production for leather finishing, automotive interior, and wood coating applications globally, their established tannery, automotive material, and furniture coating customer supply relationships, and their contrasting positions as the MDI-integrated reactive PUD innovator with the most commercially advanced automotive interior qualification and the world's largest PUD production capacity with the broadest geographic distribution network.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 2.84 Billion |

| Market Size 2032 | USD 4.98 Billion |

| CAGR | 8.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, Netherlands, Italy, Spain, South Korea, China, Japan, India, Brazil |

| Companies Profiled | Covestro, BASF, Lubrizol, Stahl, DIC Corporation, Mitsui Chemicals, Wannan Chemical, Shandong INOV |

| Key Data Sources | Covestro 2024 Coatings and Adhesives annual report, BASF 2024 Dispersions and Resins, Lubrizol 2024 Advanced Materials, Covestro Bayhydrol UH 240 Q2 2025 launch, BASF Lemfoerde PUD expansion Q3 2025, Stahl EvoTechnika Q4 2025, Confindustria Moda REACH roadmap Q1 2026, Ultrafabrics Tesla supply agreement Q3 2025, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 248 |

| Published | Q2 2026 |

| SKU | NXC-AM-008 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 14 expert interviews between January and May 2026. Supply-side contacts included aqueous PUD product and commercial managers at Covestro and BASF, specialty PUD application contacts at Lubrizol and Stahl, and reactive PUD crosslinker development leads at Covestro. Demand-side contacts included Italian Santa Croce sull'Arno and Arzignano tannery leather finishing REACH compliance programme managers, BMW and Tesla EV interior material programme engineers, automotive artificial leather material procurement leads at Benecke-Kaliko, and European wood floor coating formulators implementing EU Directive 2004/42/EC VOC compliance PUD programmes. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Covestro AG 2024 Coatings and Adhesives annual report, BASF SE 2024 Dispersions and Resins segment, Lubrizol 2024 Advanced Materials PUD revenue, Covestro Bayhydrol UH 240 automotive launch Q2 2025, BASF Lemfoerde PUD capacity expansion Q3 2025, Stahl EvoTechnika waterborne leather finishing launch Q4 2025, Confindustria Moda REACH SVOC compliance roadmap Q1 2026, Ultrafabrics Tesla vegan leather supply agreement Q3 2025, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.