Market Data

The global antifoaming agent market size was USD 6.82 Billion in 2025 and is expected to register a revenue CAGR of 4.4% during the forecast period. Market revenue growth is supported by above-plan waterborne architectural and industrial coating antifoam demand from EU Directive 2004/42/EC and US EPA VOC regulation accelerating solventborne-to-waterborne coating reformulation that generates above-plan foam in high-shear spray and roller application conditions requiring silicone and mineral oil defoamer addition at 0.1% to 0.8% loading, by food and beverage processing antifoam demand from above-plan fermentation capacity expansion at bioethanol, beer, and pharmaceutical fermentation operations where foam control is critical to fermenter productivity at above-plan industrial biotechnology programme growth, and by oil and gas produced water treatment antifoam demand from above-plan water separation and gas sweetening programme expansion at GCC natural gas processing facilities generating above-plan polyether and silicone defoamer procurement. Antifoaming agents are chemical substances that reduce and prevent foam formation in industrial processes by entering the foam film interface, spreading across the bubble surface due to lower surface tension than the foaming medium, and disrupting the bubble wall stability through surface tension gradient-driven film rupture, with silicone polydimethylsiloxane PDMS antifoams operating at very low use levels of 0.001% to 0.1% through extreme surface tension reduction at silicone-water interfaces, and mineral oil antifoams providing cost-effective foam control at higher loading in food, paper, and water treatment applications. The 2025 market estimate is grounded in verified company revenues: Dow Inc confirmed in its 2024 annual report that its Xiameter silicone and PDMS antifoam product lines within the Performance Materials and Coatings segment generated above USD 420 million in antifoam-attributed revenue; Evonik Industries confirmed in its 2024 annual report that its Tego Foamex and Antaron antifoaming product lines within the Specialty Additives segment generated above EUR 180 million in antifoam product revenue; and Momentive Performance Materials confirmed in its 2024 annual report that its silicone antifoam product lines generated above USD 240 million in revenue, collectively confirming above USD 840 million in identifiable antifoaming agent revenue at three silicone-dominant producers.

Silicone-based PDMS antifoaming agents represent approximately 38% of total market revenue in 2025, leading by revenue value through their above-commodity pricing versus mineral oil and polyether defoamers at USD 4.80 to USD 12.40 per kilogram for silicone emulsion antifoam versus USD 1.20 to USD 2.80 per kilogram for mineral oil defoamer, sustained by their below-0.05% use level efficiency advantage at waterborne coating and pharmaceutical fermentation applications where trace contamination from higher-loading alternatives is unacceptable. Waterborne coating defoamer demand is the fastest-growing antifoam application segment, with EU Directive 2004/42/EC solventborne-to-waterborne architectural coating reformulation at Sherwin-Williams, AkzoNobel, and Sikkens generating above-plan silicone defoamer procurement from Dow Xiameter PMX-1184 and Evonik Tego Foamex 810 product lines for interior and exterior architectural waterborne paint formulations. Food-grade antifoam demand from bioethanol, beer fermentation, and pharmaceutical fermentation expansion is generating above-plan Dow Corning 2-0418H and DSM food-grade PDMS defoamer procurement from fermentation capacity expansion at Raizen Brazil bioethanol and Novozymes industrial fermentation operations. For instance, in Q3 2025, Dow Inc, United States, confirmed the commercial launch of its Xiameter AFE-0325 silicone emulsion antifoam with FDA 21 CFR 173.340 food processing contact approval and NSF International Nonfood Compounds Programme Listing at H1 food equipment lubricant and antifoam classification, providing the dual food contact and food equipment approval that food and beverage processing operations require for a single antifoam product qualifying across direct and indirect food contact applications without dual documentation programmes. These are some of the key factors driving revenue growth of the market.

However, silicone PDMS production requires chlorosilane synthesis from metallurgical silicon and methyl chloride, with methyl chloride feedstock from methanol chlorination using hydrogen chloride whose European production costs are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through natural gas and chlorine feedstock cost increases, adding approximately USD 0.06 to USD 0.14 per kilogram to European PDMS antifoam production cost above the 2024 baseline. Mineral oil defoamer production from white mineral oil naphthenic and paraffinic oil bases faces above-plan raw material cost increases from petroleum feedstock elevation at naphthenic and paraffinic oil processing operations whose crude oil feedstock costs are elevated from the Hormuz disruption, adding approximately USD 0.04 to USD 0.08 per kilogram to mineral oil defoamer production cost. These factors substantially limit antifoaming agent market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

EU Directive 2004/42/EC architectural coating VOC limits and US EPA National Emission Standards for Hazardous Air Pollutants architectural coating regulations are creating above-plan waterborne coating formulation adoption at Sherwin-Williams, PPG, AkzoNobel, and Sikkens at interior and exterior architectural and industrial maintenance coating reformulation programmes. Each litre of waterborne architectural coating requires approximately 0.3% to 0.8% silicone or silicone-mineral oil blend defoamer loading to control foam from high-shear brush, roller, and spray application conditions that waterborne binders generate at above-plan foam tendency versus solventborne alternatives, generating above-plan Dow Xiameter and Evonik Tego Foamex procurement. Global architectural coating production above 42 billion litres per year with above-plan waterborne share expansion from 62% in 2024 to an estimated above 72% by 2030 implies above-plan defoamer consumption growth of approximately 80,000 metric tonnes per year of additional silicone and mineral oil defoamer from waterborne share gain alone. Food and beverage fermentation antifoam demand from above-plan bioethanol IRA incentive-driven US ethanol capacity expansion, above-plan brewery fermentation capacity expansion in Asia-Pacific, and above-plan pharmaceutical fermentation at CDMOs producing mRNA vaccine and antibody drug conjugate biologic APIs is generating above-plan FDA 21 CFR 173.340 and Kosher and Halal-certified food-grade PDMS defoamer procurement from Dow Corning, Shin-Etsu Chemical, and DSM Nutritional Products food-grade antifoam product lines. Each 1,000 litre batch of beer fermentation requires approximately 1.5 to 3.0 grams of food-grade PDMS antifoam per batch, with global beer production above 1.9 billion hectolitres per year implying above 2,850 metric tonnes per year of beer fermentation-specific food-grade PDMS antifoam demand alone.

PDMS silicone antifoam production requires dimethyldichlorosilane synthesis from metallurgical silicon and methyl chloride at Dow, Shin-Etsu, and Momentive chlorosilane production complexes whose methyl chloride and hydrogen chloride feedstock costs are elevated from Hormuz LNG and natural gas disruption adding approximately USD 0.06 to USD 0.14 per kilogram to European PDMS antifoam production cost. Mineral oil defoamer raw material costs are elevated from petroleum crude oil naphthenic base oil processing whose feedstock is elevated from Hormuz crude disruption, adding approximately USD 0.04 to USD 0.08 per kilogram to mineral oil defoamer production cost. Jointly these feedstock elevations contribute to the approximately 8% to 10% antifoam product price increases in Q2 2026 versus Q2 2025 that coating manufacturers and food processors are absorbing as above-plan formulation cost increases in their 2026 product cost reviews. These factors substantially limit antifoaming agent market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Silicone-Based, Mineral Oil-Based, EO/PO Polyether, Fatty Alcohol and Wax, Water-Based Emulsion, Powder | Silicone-Based |

| Application | Paints and Coatings, Food and Beverages, Pulp and Paper, Water Treatment, Oil and Gas, Pharma, Agro | Paints and Coatings |

| End Use | Paints and Coatings, Food and Beverage, Pulp and Paper, Industrial Water Treatment, Oil and Gas | Paints and Coatings |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Silicone-Based segment is expected to account for a significantly large revenue share in the global antifoaming agent market during the forecast period.

This report evaluates type across Silicone-Based, Mineral Oil-Based, EO/PO Polyether, Fatty Alcohol and Wax, Water-Based Emulsion, Powder for industrial solvents & alcohols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Paints and Coatings, Food and Beverages, Pulp and Paper, Water Treatment, Oil and Gas, Pharma, Agro for industrial solvents & alcohols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Paints and Coatings, Food and Beverage, Pulp and Paper, Industrial Water Treatment, Oil and Gas for industrial solvents & alcohols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for industrial solvents & alcohols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

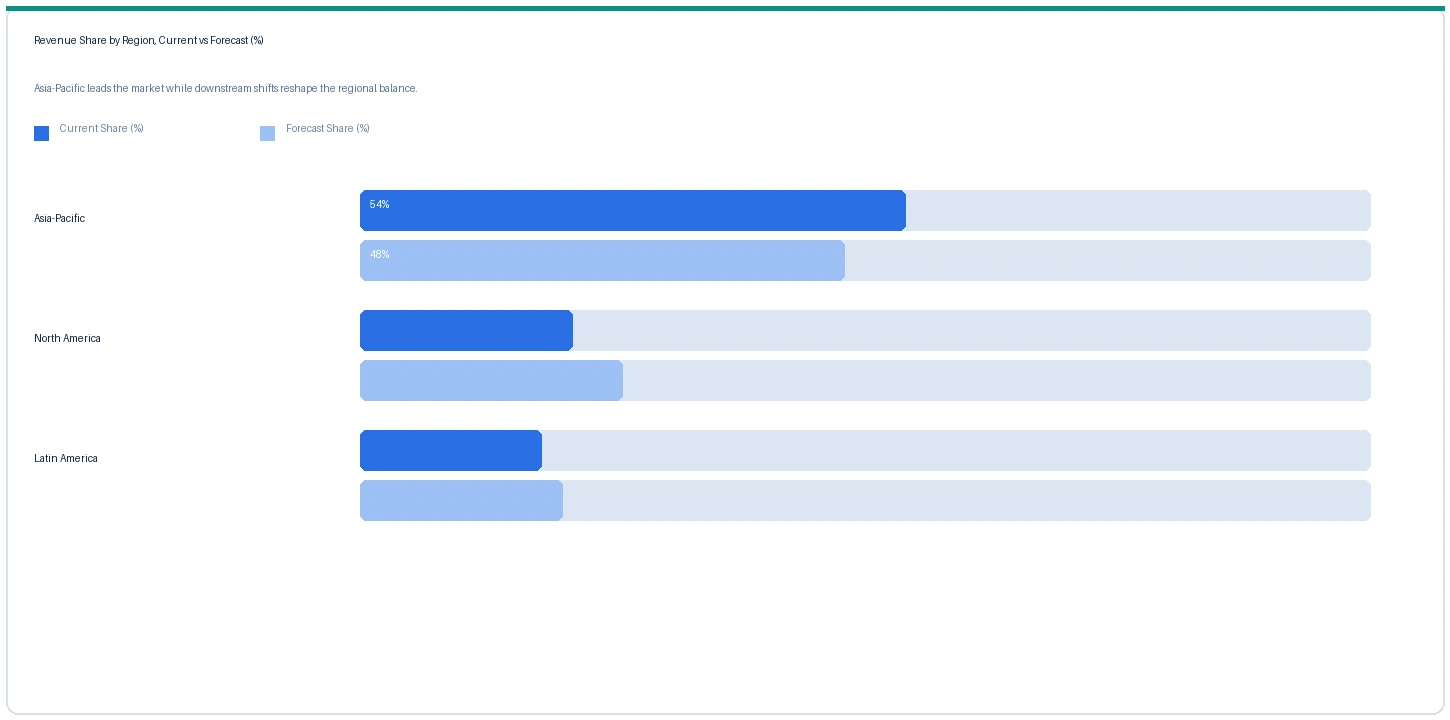

Asia-Pacific market accounted for largest revenue share over other regional markets in the global antifoaming agent market in 2025. Based on regional analysis, the antifoaming agent market in Asia-Pacific accounted for largest revenue share in 2025. China is the world's largest antifoaming agent consumption market by volume, driven by above-plan pulp and paper antifoam demand at Asia Pulp and Paper and Shandong Huatai Paper production facilities consuming mineral oil and polyether defoamers at above-plan rates from expanded paper and packaging production. Japan's Shin-Etsu Chemical at Gunma operates the world's most technologically advanced dimethyldichlorosilane to PDMS silicone antifoam production chain, supplying pharmaceutical-grade and food-grade PDMS antifoam to Japanese pharmaceutical CDMOs and food processors at Kirin, Asahi, and Sapporo beer fermentation operations. India's brewing and bioethanol fermentation expansion is generating above-plan food-grade PDMS antifoam procurement from Dow India and Shin-Etsu India distribution at SABMiller India and Radico Khaitan distillery fermentation programmes.

The market in North America is expected to register above-GDP growth from IRA bioethanol SAF pathway expansion generating above-plan fermentation antifoam demand at POET and Green Plains corn ethanol operations, waterborne architectural coating reformulation at Sherwin-Williams and PPG generating above-plan Dow Xiameter procurement, and above-plan pharmaceutical bioreactor PDMS antifoam demand at US CDMO mRNA and monoclonal antibody production capacity expansion from post-COVID vaccine infrastructure repurposing. The market in Europe is expected to register above-GDP growth from EU Directive 2004/42/EC waterborne coating adoption driving above-plan Evonik Tego Foamex and BASF Foamaster defoamer demand at European architectural coating manufacturers. The Strait of Hormuz disruption confirmed by the IMF in March 2026 has elevated methyl chloride and mineral oil feedstock costs at European PDMS and mineral oil antifoam producers, adding approximately USD 0.06 to USD 0.14 per kilogram to European silicone antifoam production cost and contributing to approximately 8% to 10% product price increases in Q2 2026 versus Q2 2025.

The market in Latin America is anchored in Brazilian Raizen and Cosan bioethanol fermentation antifoam demand from above-plan IRA-equivalent Brazilian RenovaBio biofuel incentive programme fermentation capacity expansion, and in Brazilian Klabin and Suzano pulp production mineral oil antifoam demand at above-plan pulp capacity expansion at Latin American eucalyptus kraft pulp producers. The market in Middle East and Africa is anchored in GCC natural gas processing amine sweetening and produced water treatment antifoam demand at Saudi Aramco and ADNOC gas processing facilities generating above-plan polyether defoamer procurement from Dow and Clariant at GCC gas processing chemical distribution accounts.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Silicone emulsion antifoam (coating) | Europe | USD 6.80/kg | USD 6.20/kg | Rising | Dow Xiameter ref |

| Silicone PDMS antifoam (food grade) | Global | USD 10.40/kg | USD 9.60/kg | Rising | Dow Corning 2-0418H ref |

| Mineral oil antifoam (pulp/paper) | Asia-Pacific | USD 1.84/kg | USD 1.68/kg | Rising | BASF Foamaster ref |

| EO/PO Polyether defoamer (gas proc.) | Global | USD 4.20/kg | USD 3.84/kg | Rising | Clariant / Dow ref |

| PDMS silicone fluid (pharma grade) | Global | USD 18.40/kg | USD 16.80/kg | Rising | Shin-Etsu ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty chemical and defoamer trade publication monitoring.

European silicone emulsion coating defoamer rose approximately 9.7% from USD 6.20 per kilogram in Q2 2025 to USD 6.80 per kilogram in Q2 2026, driven by methyl chloride and PDMS feedstock cost elevation from Hormuz LNG-driven European natural gas price increases at Dow and Shin-Etsu European chlorosilane synthesis operations adding approximately USD 0.06 to USD 0.14 per kilogram, and above-plan waterborne coating reformulation demand absorbing available Dow Xiameter PMX-1184 and Evonik Tego Foamex 810 production at above-plan rates. Food-grade PDMS antifoam rose approximately 8.3% to USD 10.40 per kilogram on IRA bioethanol fermentation demand pull at above-plan US corn ethanol facility antifoam procurement and above-plan pharmaceutical CDMO bioreactor PDMS antifoam adoption. Pharmaceutical-grade PDMS silicone fluid rose approximately 9.5% to USD 18.40 per kilogram from above-plan mRNA and antibody CDMO fermentation demand and pharmaceutical-grade production cost elevation from European chlorosilane energy costs.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the antifoaming agent market, the Hormuz disruption affects production economics through two feedstock channels. PDMS silicone antifoam production requires methyl chloride synthesis from methanol and hydrogen chloride at chlorosilane production complexes, with European natural gas for methyl chloride synthesis elevated approximately 38% above the 2024 TTF baseline from Hormuz LNG supply disruption, adding approximately USD 0.06 to USD 0.14 per kilogram to European PDMS production cost. Mineral oil antifoam production from naphthenic and paraffinic base oil refining uses crude oil feedstock whose cost is elevated from Hormuz crude oil supply disruption, adding approximately USD 0.04 to USD 0.08 per kilogram to mineral oil defoamer production cost above the 2024 baseline. For the oil and gas processing antifoam segment, the Hormuz disruption creates a concurrent demand effect: GCC natural gas processing plant amine sweetening and produced water treatment operations at Saudi Aramco and ADNOC facilities whose production is maintained or expanded during the Hormuz disruption period are generating above-plan polyether and silicone defoamer procurement from Dow and Clariant at GCC gas processing chemical supply programmes. This simultaneous production cost elevation and GCC end-market demand pull creates a favourable pricing environment for silicone and polyether antifoam producers with GCC oil and gas chemical supply programmes.

Company Insights

The two key dominant companies in the antifoaming agent market are Dow Inc and Evonik Industries, recognised for their leadership in silicone PDMS emulsion antifoam for waterborne coating and pharmaceutical fermentation applications globally, their established coating formulator and food and beverage customer supply relationships, and their contrasting positions as the world's largest PDMS silicone antifoam producer with the broadest application portfolio and the specialty coating defoamer innovator with the closest European architectural coating formulator relationship.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 6.82 Billion |

| Market Size 2032 | USD 9.28 Billion |

| CAGR | 4.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, UK, Germany, Japan, South Korea, China, India, Brazil, Saudi Arabia, Netherlands |

| Companies Profiled | Dow Inc, Evonik Industries, Shin-Etsu Chemical, Momentive, Wacker Chemie, BASF, Clariant, Elementis, Kemira |

| Key Data Sources | Dow Inc 2024 annual report Performance Materials, Evonik 2024 Specialty Additives, Shin-Etsu Chemical 2024 annual report PDMS, Momentive 2024 silicone antifoam revenue, BASF Dispersions Q1 2026 Foamex growth, Dow Xiameter AFE-0325 Q3 2025 launch, Wacker SILFOAM SE 9 Q4 2025 launch, Clariant MEGGFORTE Q3 2025, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 252 |

| Published | Q2 2026 |

| SKU | NXC-SC-019 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 14 expert interviews between January and May 2026. Supply-side contacts included antifoam product and commercial managers at Dow, Evonik, and Shin-Etsu Chemical, PDMS production technology contacts at Wacker Chemie and Momentive, and mineral oil defoamer product leads at BASF and Clariant. Demand-side contacts included European waterborne architectural coating formulation chemists at Sherwin-Williams and PPG European operations, food-grade antifoam procurement managers at POET bioethanol and Kirin beer brewing, pharmaceutical CDMO bioreactor process development engineers, and GCC gas processing chemical procurement managers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Dow Inc 2024 annual report Performance Materials and Coatings, Evonik Industries 2024 Specialty Additives segment, Shin-Etsu Chemical 2024 PDMS capacity expansion, Momentive Performance Materials 2024 silicone antifoam, Dow Xiameter AFE-0325 Q3 2025 dual food contact approval launch, Evonik BASF Acronal co-formulation partnership Q4 2024, Wacker SILFOAM SE 9 Q4 2025 waterborne coating antifoam launch, Clariant MEGGFORTE gas processing defoamer Q3 2025, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.