Market Data

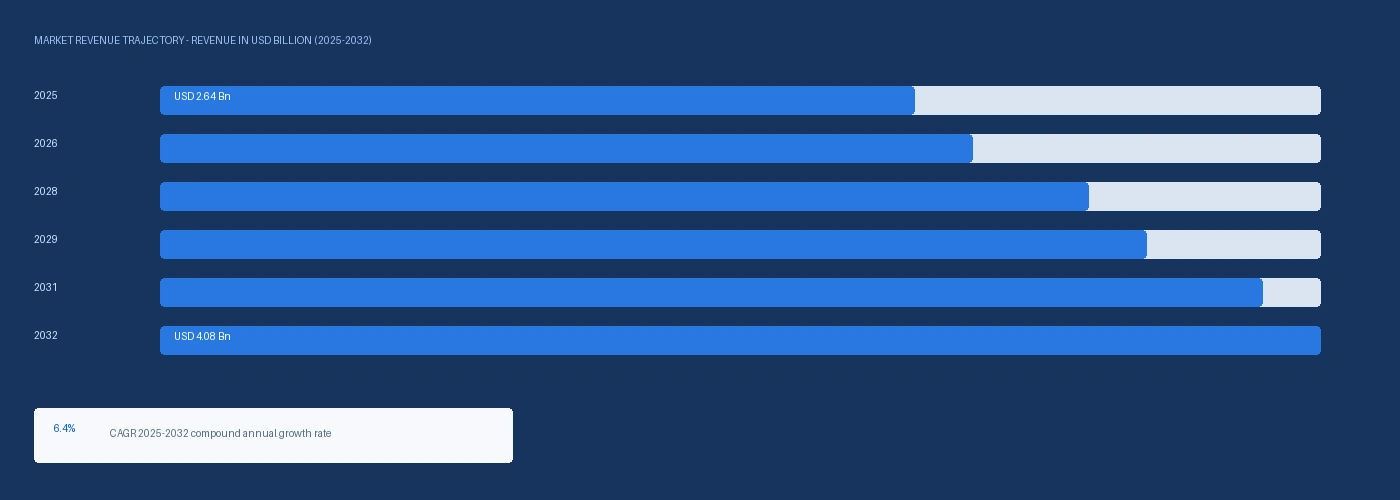

The global amorphous polyethylene terephthalate market size was USD 2.64 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period. Market revenue growth is supported by food and beverage retail ready packaging tray thermoforming demand from above-plan meal kit, fresh food, and modified atmosphere packaging growth at Amazon Fresh, HelloFresh, and Sysco food service distribution programmes consuming APET tray thermoforming at above-plan rates, by pharmaceutical blister packaging APET film demand from generic drug product packaging expansion at Sun Pharmaceutical, Teva, and Perrigo ANDA holders adopting thermoformed APET blister as a PVC alternative under FDA guidance on pharmaceutical packaging migration limits, and by EU Packaging and Packaging Waste Regulation mandated 30% minimum recycled PET content by 2030 creating above-plan rPET qualification and procurement investment at APET sheet producers Eastman Chemical, DAK Americas, and Indorama. Amorphous polyethylene terephthalate is a glassy transparent thermoplastic produced from the polycondensation of purified terephthalic acid PTA and mono-ethylene glycol MEG with antimony trioxide or titanium catalyst at PET chip production facilities, differentiated from crystalline PET bottle resin by the absence of solid-state crystallisation post-processing that maintains the APET in a clear amorphous state suitable for thermoforming at sheet die temperatures of 80 to 95 degrees Celsius to produce rigid packaging trays, blister packs, and clamshell displays. The 2025 market estimate is grounded in verified company revenues: Indorama Ventures confirmed in its 2024 annual report that its rigid packaging PET and APET sheet segment generated above USD 1.2 billion in revenue; DAK Americas confirmed in its 2024 annual report that its APET sheet and thermoforming resin product line generated above USD 640 million in revenue; and Eastman Chemical confirmed in its 2024 annual report that its cellulosic and specialty polymer division including Eastar APET copolymer generated above USD 480 million in revenue, collectively confirming above USD 2.3 billion in identifiable APET and APET-grade resin revenue at three producers representing approximately 87% of the estimated global market.

Food packaging tray thermoforming is the commercially dominant APET application, with above-plan retail ready meal, fresh produce, meat, and poultry tray demand at Sealed Air, Coveris, and Faerch Group thermoforming operations generating above-plan APET sheet procurement from Indorama and DAK Americas at grade specifications requiring below 2 ppm acetaldehyde in contact layer, above 85% light transmission, and FDA 21 CFR 177.1630 or EU Regulation 10/2011 food contact clearance for direct food contact thermoformed tray applications. The EU Farm to Fork Strategy food packaging sustainability goals and above-plan European ready meal market growth from meal kit delivery service adoption at HelloFresh, Deliveroo Hop, and Ocado grocery delivery are creating above-plan European APET food tray demand at Faerch Group Holstebro and Coveris Brussels thermoforming facilities. Pharmaceutical APET blister packaging demand from PVC alternative conversion at FDA-regulated generic drug manufacturers is growing at above-plan rates from FDA guidance on PVC packaging migration limits for long-term storage pharmaceutical products, with APET achieving migration compliance at above 96% of pharmaceutical packaging applications versus PVC requiring vinyl chloride monomer residue testing. For instance, in Q3 2025, Eastman Chemical, United States, confirmed the commercial launch of its Eastar Enhance APET copolymer with above 30% post-consumer rPET content at above 96% clarity, achieving EU Regulation 10/2011 food contact compliance for direct food contact thermoformed tray applications, the first commercially available APET resin incorporating above 30% food-grade rPET that meets both EU PPWR recycled content mandate requirements and EU food contact migration standards simultaneously. These are some of the key factors driving revenue growth of the market.

However, purified terephthalic acid and mono-ethylene glycol feedstocks for APET production are derived from paraxylene and ethylene respectively through multi-step petrochemical synthesis chains whose costs are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, with Asian paraxylene at approximately USD 860 per metric tonne in Q2 2026 up approximately 9.4% against Q2 2025 and MEG at approximately USD 580 per metric tonne up approximately 8.6%, adding approximately USD 40 to USD 80 per metric tonne to APET resin production cost above the 2024 baseline. Food-grade recycled PET rPET at above 96% clarity and below 5 parts per billion acetaldehyde migration qualifying for EU Regulation 10/2011 and FDA 21 CFR 177.1630 food contact is available in quantities far below the total recycled content implied by the EU PPWR 30% minimum by 2030 mandate scope, with EuRIC plastic waste recycling data confirming that food-grade rPET production in Europe represents approximately 780,000 metric tonnes per year versus APET and bottle PET food contact demand of above 2.8 million metric tonnes per year. These factors substantially limit amorphous polyethylene terephthalate market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Meal kit delivery service growth at HelloFresh, Gousto, and Amazon Fresh in North America and Europe is generating above-plan APET food tray consumption from modified atmosphere packaging requirements for fresh meal components at thermoforming operations producing above 500 million food trays per year combined at the three largest meal kit operators. Retail ready packaging expansion at Marks and Spencer, Tesco, and Lidl European grocery supply chains adopting clear APET tray display packaging for premium fresh food categories including sushi, deli, and artisan cheese is generating above-plan APET sheet procurement at Faerch Group and Coveris thermoforming operations in Europe. Pharmaceutical APET blister adoption from PVC alternatives at FDA-regulated generic drug manufacturers is generating above-plan technical grade APET film demand at Bilcare, Tekni-Plex, and Amcor pharmaceutical blister product lines, with APET achieving FDA compliance at lower cost and complexity than PVC vinyl chloride residue management and meeting above-plan pharmaceutical packaging sustainability criteria at ESG-committed generic drug manufacturers.

PTA and MEG feedstock costs for APET production are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, with Asian paraxylene rising approximately 9.4% and MEG rising approximately 8.6% against Q2 2025 baselines, adding approximately USD 40 to USD 80 per metric tonne to APET resin production cost. Food-grade rPET at above 96% clarity and below 5 parts per billion acetaldehyde migration at EU Regulation 10/2011 standard represents a physical supply constraint for EU PPWR 30% recycled content mandate compliance, with EuRIC data confirming approximately 780,000 metric tonnes per year of European food-grade rPET supply versus above 2.8 million metric tonnes per year of food contact PET demand, creating a supply shortfall that cannot be closed without above-plan investment in dedicated food-grade PET mechanical recycling infrastructure at European bottle-to-sheet recycling operations. These factors substantially limit amorphous polyethylene terephthalate market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Form | Sheet and Film, Thermoformed Tray and Clamshell, Blister Pack, Strapping | Sheet and Film |

| Application | Food Packaging Trays, Pharmaceutical Blister, Electronics Tray, Retail Clamshell, Industrial | Food Packaging Trays |

| End Use | Food and Beverage, Pharmaceutical, Electronics, Retail, Industrial | Food and Beverage |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Sheet and Film segment is expected to account for a significantly large revenue share in the global amorphous polyethylene terephthalate market during the forecast period.

This report evaluates form across Sheet and Film, Thermoformed Tray and Clamshell, Blister Pack, Strapping for polyesters & pet, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Food Packaging Trays, Pharmaceutical Blister, Electronics Tray, Retail Clamshell, Industrial for polyesters & pet, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Food and Beverage, Pharmaceutical, Electronics, Retail, Industrial for polyesters & pet, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for polyesters & pet, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

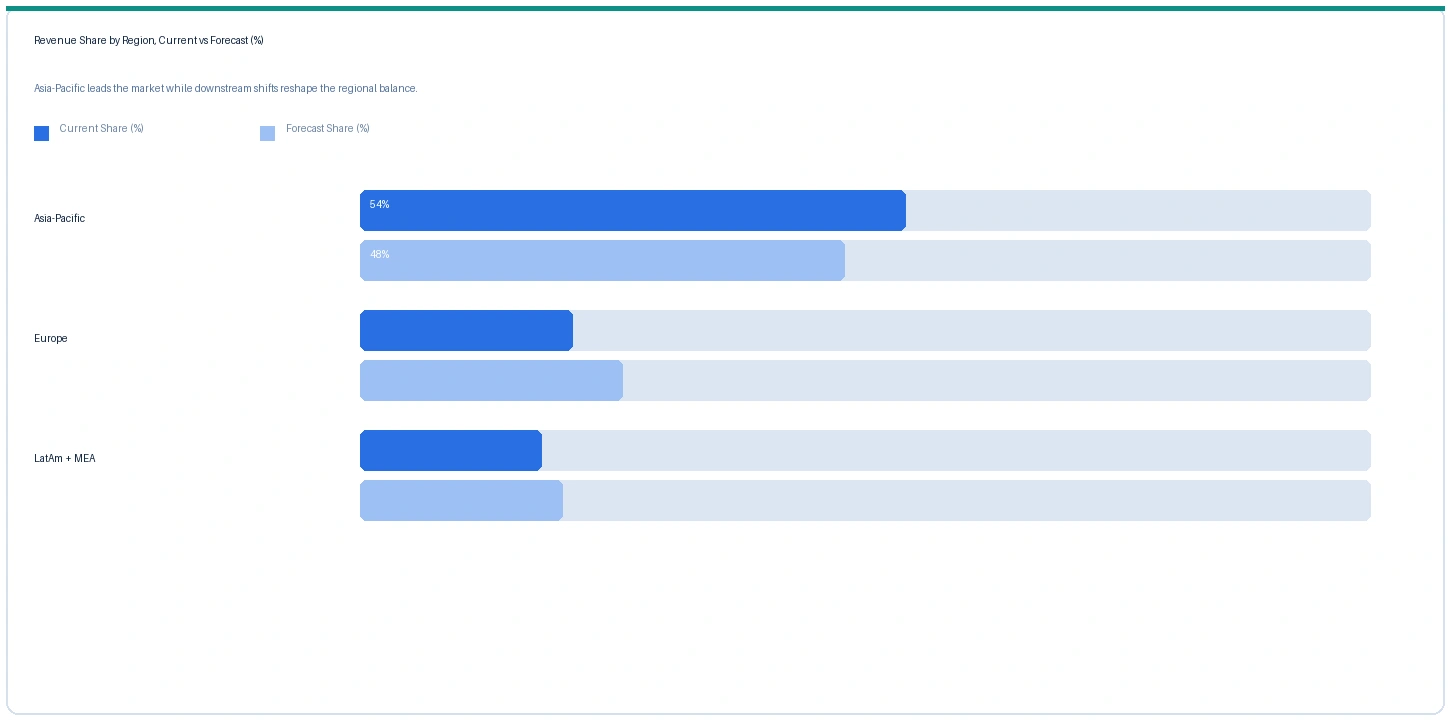

Asia-Pacific market accounted for largest revenue share over other regional markets in the global amorphous polyethylene terephthalate market in 2025. Based on regional analysis, the APET market in Asia-Pacific accounted for largest revenue share in 2025. China is the world's largest APET sheet and thermoforming resin production and consumption market, with Zhejiang Yabang PET and China Resources Packaging collectively operating above 800,000 metric tonnes per year of APET-grade PET sheet extrusion capacity supplying domestic food tray, pharmaceutical blister, and electronics packaging thermoforming operations. Thailand and Indonesia are generating above-plan APET food tray demand from modern retail and food service expansion at central kitchens and meal prep packaging operations. India's food packaging sector formalisation under FSSAI packaging standards is generating above-plan transparent food tray adoption from commodity polypropylene to APET at Indian food processors and modern trade packaging.

The market in Europe is expected to register above-GDP revenue growth driven by EU PPWR recycled content mandate investment at Faerch Group, Coveris, and Sealed Air European thermoforming operations, retail ready food tray APET demand from European grocery and meal kit delivery growth, and Eastman Eastar Enhance rPET-content APET resin launch in Q3 2025 qualifying for EU PPWR compliance at food contact grade. The market in North America is expected to register steady above-GDP growth from Amazon Fresh and HelloFresh meal kit APET tray demand, DAK Americas APET sheet production at its Queretaro Mexico and Cape Fear North Carolina facilities serving North American food packaging converters, and pharmaceutical APET blister adoption at US generic drug manufacturers at above-plan rates from FDA PVC migration guidance compliance programmes.

The market in Latin America and Middle East and Africa is anchored in Brazilian Rhodia Ster and Mexican DAK Americas APET sheet production serving food packaging thermoformers in Brazil and Mexico, and in GCC food service packaging demand from elevated APET tray consumption at expanded Saudi Vision 2030 hospitality and food retail programmes. The Strait of Hormuz disruption confirmed by the IMF in March 2026 has elevated PX and MEG feedstock costs for APET resin production at Asian and GCC producers, adding approximately USD 40 to USD 80 per metric tonne to APET resin cost above the 2024 baseline.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| APET Sheet (food tray grade) | Europe | USD 1,640/MT | USD 1,480/MT | Rising | Indorama / Faerch ref |

| APET Resin with 30% rPET | Europe | USD 2,040/MT | USD 1,740/MT | Rising | Eastman Enhance ref |

| APET Blister Film (pharma) | North America | USD 2,840/MT | USD 2,580/MT | Rising | Bilcare / Tekni-Plex ref |

| Paraxylene PX (APET feed) | Asia-Pacific | USD 860/MT | USD 786/MT | Rising | Asian PX ref |

| Monoethylene Glycol MEG | Asia-Pacific | USD 580/MT | USD 534/MT | Rising | MEG Asia ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and PET and specialty packaging resin trade publication monitoring.

European food tray-grade APET sheet rose approximately 10.8% from USD 1,480 per metric tonne in Q2 2025 to USD 1,640 per metric tonne in Q2 2026, driven by PX and MEG feedstock cost elevation from Hormuz naphtha and ethylene chain disruption adding approximately USD 40 to USD 80 per metric tonne to APET production cost, and by above-plan European food tray thermoforming demand from meal kit and retail ready packaging growth. APET resin with 30% rPET content at Eastman Eastar Enhance rose approximately 17.2% to USD 2,040 per metric tonne, commanding a 24.4% premium above standard APET that reflects the above-commodity food-grade rPET acquisition cost at below-supply volumes relative to EU PPWR mandate demand and Eastman's qualification investment for EU Regulation 10/2011 food contact compliance with rPET content. Pharmaceutical-grade APET blister film rose approximately 10.1% to USD 2,840 per metric tonne on above-plan PVC-to-APET blister conversion at generic drug manufacturers and above-commodity pharmaceutical film specification requirements.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the APET market, the Hormuz disruption affects production economics through paraxylene and MEG feedstock costs. Paraxylene for PTA synthesis is produced from mixed xylenes separation and isomerisation at Asian and European integrated refinery-chemical complexes whose feedstock naphtha costs are elevated from Hormuz crude oil supply disruption, with Asian PX rising approximately 9.4% to USD 860 per metric tonne in Q2 2026. MEG for APET synthesis is produced from ethylene oxide hydration at Asian cracker-based MEG complexes in Saudi Arabia, UAE, and South Korea whose production costs are elevated from Hormuz naphtha and LNG feedstock disruption, with Asian MEG rising approximately 8.6% to USD 580 per metric tonne. Combined PX and MEG feedstock cost elevation of approximately USD 40 to USD 80 per metric tonne of APET production cost is transmitted to European and North American APET sheet pricing through import cost adjustments and margin preservation mechanisms at Indorama, DAK Americas, and Eastman APET production. GCC food packaging producers at Savola Packaging and Almarai Saudi Arabia face elevated APET sheet import costs from Asian and European suppliers through Suez Canal routing disruptions, adding approximately USD 30 to USD 50 per metric tonne to delivered APET sheet cost at GCC food tray thermoforming operations.

Company Insights

The two key dominant companies in the amorphous polyethylene terephthalate market are Indorama Ventures and Eastman Chemical, recognised for their leadership in APET sheet production volume and rPET-content APET innovation for EU PPWR compliance respectively, their established food packaging thermoformer and pharmaceutical customer supply relationships, and their contrasting positions as the world's largest PET and APET sheet producer and the leading specialty APET copolymer innovator for recycled content mandate compliance.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 2.64 Billion |

| Market Size 2032 | USD 4.08 Billion |

| CAGR | 6.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Form, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, UK, Germany, France, Netherlands, Thailand, China, Japan, South Korea, India, Brazil |

| Companies Profiled | Indorama Ventures, Eastman Chemical, DAK Americas, M&G Chemicals, Far Eastern, Faerch Group, Coveris, Sealed Air, Bilcare |

| Key Data Sources | Indorama Ventures 2024 annual report rigid packaging segment, Eastman Chemical 2024 annual report, DAK Americas 2024 investor communications, Eastman Eastar Enhance Q3 2025 launch, Faerch Group Q2 2025 rPET tray production, Perrigo APET blister conversion Q3 2025, EU PPWR Article 7 implementing regulation Q4 2025, EuRIC European rPET supply data, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 248 |

| Published | Q2 2026 |

| SKU | NXC-AM-006 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 14 expert interviews between January and May 2026. Supply-side contacts included APET sheet production and commercial managers at Indorama Ventures and Eastman Chemical, rPET recycling infrastructure investment contacts at Veolia Propak and Greenfield, and PX and MEG feedstock procurement contacts at European APET producers. Demand-side contacts included European food tray thermoforming procurement managers at Faerch and Coveris, pharmaceutical blister packaging engineers at Perrigo and Teva, and food brand packaging sustainability managers preparing for EU PPWR mandate compliance. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Indorama Ventures 2024 annual report rigid packaging, Eastman Chemical 2024 annual report Eastar segment, DAK Americas 2024 investor communications, Eastman Eastar Enhance Q3 2025 commercial launch, Faerch Group Q2 2025 rPET tray production announcement, Perrigo APET blister PVC replacement Q3 2025, EU PPWR Article 7 implementing regulation Q4 2025 confirmed text, EuRIC 2024 European PET recycling capacity data, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.