Market Data

The global ammonia market size was USD 68.4 Billion in 2025 and is expected to register a revenue CAGR of 4.1% during the forecast period. Market revenue growth is supported by global nitrogen fertiliser demand from the United Nations Food and Agriculture Organization-projected food production requirement for above 9.7 billion global population by 2050 requiring above-plan urea and ammonium nitrate fertiliser production from CF Industries, Yara International, and OCI NV, by green ammonia production investment from renewable hydrogen electrolysis at NEOM Helios Project in Saudi Arabia targeting 1.2 million metric tonnes per year of green ammonia production by 2026 and Yara International at Herøya Norway targeting 500,000 metric tonnes per year of green ammonia from offshore wind hydrogen by 2030, and by ammonia-to-power generation demand from Japan's JERA co-firing programme at Hekinan coal power station targeting 20% ammonia co-firing reducing CO2 emissions at above-plan adoption rates. Ammonia is produced predominantly by the Haber-Bosch process combining nitrogen from air separation with hydrogen from steam methane reforming of natural gas or coal gasification at temperatures of 400 to 500 degrees Celsius and pressures of 150 to 300 atmospheres over iron catalyst, consuming approximately 28 to 33 gigajoules of natural gas per metric tonne of ammonia produced and representing one of the world's most energy-intensive large-scale chemical processes at approximately 1.8% of global total energy consumption. The 2025 market estimate is grounded in verified company revenues: Yara International confirmed in its 2024 annual report that it generated USD 12.9 billion in revenue from ammonia, urea, and derivative fertiliser products; CF Industries confirmed in its 2024 annual report that it generated USD 4.46 billion in revenue from ammonia, urea ammonium nitrate, and diesel exhaust fluid products; and SABIC confirmed in its 2024 annual report that its fertiliser and ammonia derivatives segment generated SAR 8.4 billion, equivalent to approximately USD 2.24 billion, collectively confirming above USD 19.6 billion in identifiable ammonia and primary derivative revenue at three major producers representing approximately 29% of the global market.

Fertiliser nitrogen demand for global food production anchors approximately 73% of total ammonia market revenue in 2025, with urea produced from ammonia and CO2 representing the largest single nitrogen fertiliser at above 180 million metric tonnes per year of global production and ammonium nitrate and urea ammonium nitrate solution representing the second largest nitrogen application fertiliser at above 50 million metric tonnes per year. The IFA International Fertilizer Association confirmed in its 2025 global fertiliser supply and demand report that global nitrogen fertiliser demand was expected to reach 115 to 120 million metric tonnes of nitrogen in 2025 to 2026, requiring approximately 200 to 210 million metric tonnes of ammonia equivalent production from existing Haber-Bosch capacity. CF Industries at Donaldsonville, Louisiana operates the world's largest single-site ammonia production complex at above 3.2 million metric tonnes per year of ammonia capacity, using US Gulf Coast natural gas at Henry Hub pricing that has remained below USD 3 per million British thermal units in 2024 and 2025, providing CF Industries with the lowest-cost Haber-Bosch production economics of any major Western ammonia producer. For instance, in Q3 2025, JERA, Japan, confirmed that its Hekinan coal power station Unit 4 had successfully co-fired at 20% ammonia volumetric blend on a 30-day continuous operation basis, achieving the 20% ammonia co-firing milestone that Japan's Green Innovation Fund programme had targeted as the demonstration threshold for commercial-scale ammonia power generation adoption, validating the power generation application channel for above-plan ammonia demand growth beyond the fertiliser and industrial chemical incumbent markets. These are some of the key factors driving revenue growth of the market.

However, the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 is the most direct and commercially consequential geopolitical risk event the ammonia market has encountered in a generation, because SABIC Saudi Arabia, Qatar Industries, and ADNOC UAE collectively operate above 18% of global traded ammonia export capacity at GCC natural gas feedstock costs of approximately USD 0.50 to USD 0.75 per million BTU that are the lowest commercially viable Haber-Bosch economics globally, and a sustained Hormuz disruption constrains these low-cost production capacities from reaching European, Asian, and Latin American fertiliser and industrial ammonia customers at import-dependent volumes that domestic production cannot rapidly replace. Green ammonia production costs from water electrolysis with renewable electricity of approximately USD 450 to USD 900 per metric tonne remain 2 to 4 times above conventional Haber-Bosch grey ammonia at USD 180 to USD 260 per metric tonne, limiting green ammonia commercial adoption to policy-supported and premium-priced applications before further cost reduction occurs. These factors substantially limit ammonia market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

The NEOM Helios Project in Tabuk, Saudi Arabia, operated by ACWA Power and Air Products and Chemicals, targets 1.2 million metric tonnes per year of green ammonia production from 4 gigawatts of solar and wind power through proton exchange membrane electrolysis hydrogen production and Haber-Bosch synthesis, representing the world's largest single green ammonia project commitment with US Air Products confirmed as the offtake partner for US hydrogen hub distribution. NEOM Helios reached financial close in late 2023 and is targeting commissioning by 2026 to 2027, with green ammonia priced at a premium above conventional Haber-Bosch grey ammonia to reflect renewable energy input cost, serving early-adopter industrial decarbonisation applications in Japan, South Korea, and European industrial clusters. Japan's JERA 20% ammonia co-firing milestone at Hekinan confirmed in Q3 2025 validates the power generation ammonia demand channel that Japan's Agency for Natural Resources and Energy projects could reach 3 million metric tonnes per year of ammonia co-firing demand by 2030 at 20% co-firing across Japan's 50-gigawatt coal fleet, representing a new above-plan demand channel above the fertiliser and industrial ammonia incumbent market. CF Industries Donaldsonville low-cost US Gulf Coast Haber-Bosch at below USD 3 per million BTU Henry Hub gas pricing is generating above-plan urea and UAN solution export volumes to European and Asian nitrogen fertiliser markets where domestic Haber-Bosch production at elevated European natural gas costs from Hormuz LNG disruption has created above-plan CF Industries export revenue growth. Yara International at Sluiskil, Netherlands and Ferrara, Italy reduced ammonia production by approximately 12% to 18% in Q4 2025 and Q1 2026 due to European natural gas costs elevated above their variable cost breakeven threshold from Hormuz disruption, creating above-plan CF Industries and SABIC export market opportunities at European nitrogen fertiliser importers.

The Strait of Hormuz disruption confirmed by the IMF in March 2026 constrains above 18% of global traded ammonia export capacity from SABIC, Qatar Industries, and ADNOC at GCC production sites that are physically adjacent to the disrupted shipping lane, creating a direct supply chain impact on European, South Asian, and Latin American nitrogen fertiliser import programmes that depend on GCC ammonia and urea supply for pre-planting season procurement. IFA estimated that GCC ammonia and urea export shortfalls from Hormuz disruption of 4 to 6 weeks could create nitrogen fertiliser supply deficits for the South Asian kharif planting season of 2 to 4 million metric tonnes of urea equivalent, representing 3% to 5% of annual global nitrogen application, with food production yield impact estimates from IFPRI ranging from 1% to 2.5% reduction in South Asian cereal production per season of below-normal nitrogen application. Green ammonia from electrolysis at USD 450 to USD 900 per metric tonne represents a 2 to 4 times cost premium above conventional grey ammonia at USD 180 to USD 260 per metric tonne in normal feedstock cost conditions, limiting green ammonia commercial adoption to decarbonisation-mandated or policy-supported applications before renewable energy cost reduction closes the gap toward 2030. These factors substantially limit ammonia market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Production Route | Haber-Bosch Natural Gas SMR, Haber-Bosch Coal Gasification, Blue Ammonia CCS, Green Ammonia | Haber-Bosch Natural Gas SMR |

| Application | Nitrogen Fertilisers, Industrial Chemicals, Refrigerants, Mining Explosives ANFO, Power Generation | Nitrogen Fertilisers |

| End Use | Agriculture, Chemical Intermediates, Refrigeration, Mining, Energy | Agriculture |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Haber-Bosch Natural Gas SMR segment is expected to account for a significantly large revenue share in the global ammonia market during the forecast period.

This report evaluates production route across Haber-Bosch Natural Gas SMR, Haber-Bosch Coal Gasification, Blue Ammonia CCS, Green Ammonia for hydrogen, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Nitrogen Fertilisers, Industrial Chemicals, Refrigerants, Mining Explosives ANFO, Power Generation for hydrogen, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Agriculture, Chemical Intermediates, Refrigeration, Mining, Energy for hydrogen, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for hydrogen, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

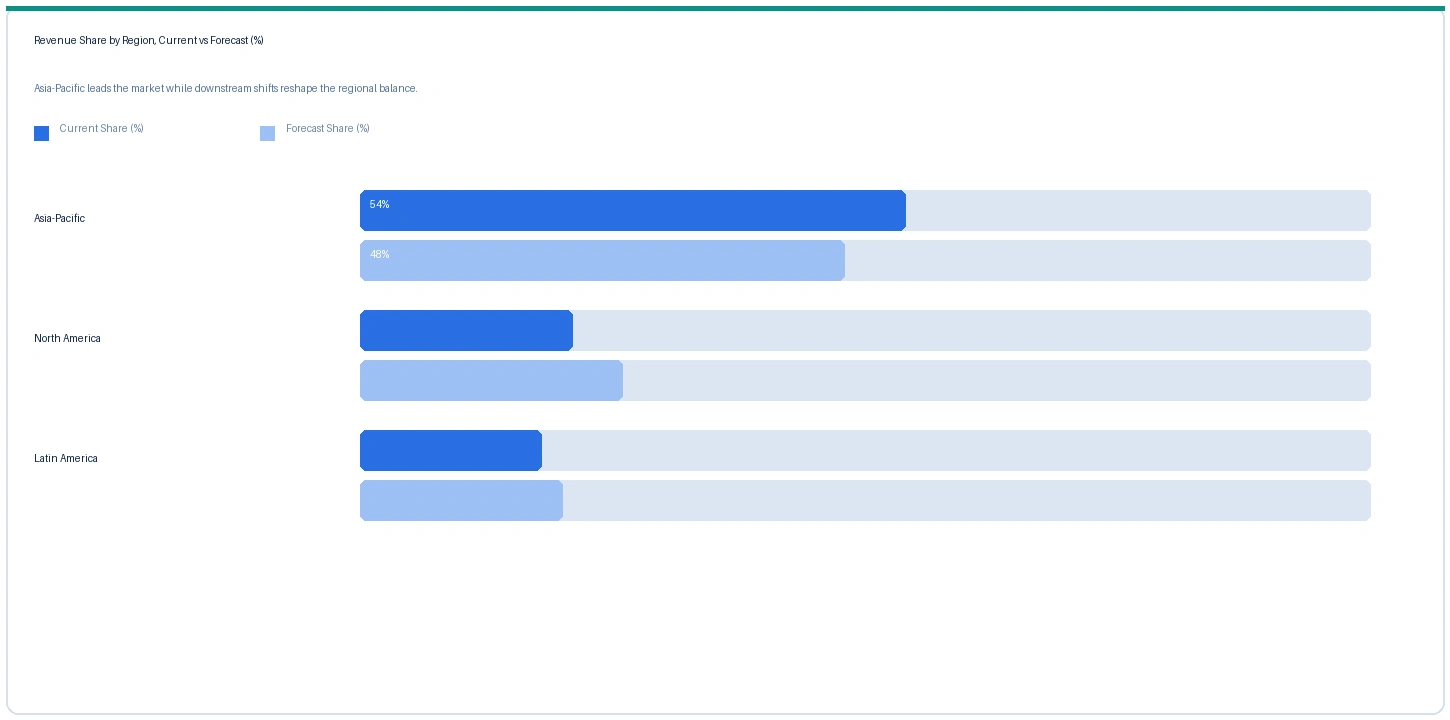

Asia-Pacific market accounted for largest revenue share over other regional markets in the global ammonia market in 2025. Based on regional analysis, the ammonia market in Asia-Pacific accounted for largest revenue share in 2025. China is the world's largest ammonia producer and consumer at above 55 million metric tonnes per year of production from coal gasification and natural gas Haber-Bosch routes, supplying domestic urea, ammonium bicarbonate, and ammonium phosphate fertiliser production and industrial chemical applications at captive integrated chemical complex consumption. India is the world's second largest ammonia import market, consuming above 9 million metric tonnes per year of urea equivalent nitrogen from domestic production at GSFC, Chambal Fertilisers, and Coromandel International and from GCC and Russian ammonia and urea imports, with Hormuz disruption creating above-plan Indian urea import procurement from CF Industries US and Yara Trinidad and Tobago as alternative GCC supply replacement channels.

The market in North America is expected to register above-GDP growth on CF Industries' low-cost US Gulf Coast production capturing European and Asian market share from Hormuz-disrupted GCC exports, and on above-plan ammonia demand from US corn belt nitrogen fertiliser consumption at Midwest spring planting season procurement programmes. The market in Europe is expected to register revenue growth but at compressed Haber-Bosch production economics from Hormuz LNG-elevated natural gas costs at Yara Sluiskil and Ferrara and BASF Antwerp and Ludwigshafen, with European producers reducing ammonia output and importing from CF Industries and SABIC at above-normal import volumes to serve European urea and ammonium nitrate production requirements. The market in Middle East and Africa is structurally affected by the Hormuz disruption, with SABIC Saudi Jubail, Qatar Industries Mesaieed, and ADNOC UAE Ruwais operating at below-capacity utilisation due to shipping logistics constraints from the Hormuz closure, creating above-plan pricing at ammonia spot markets from supply tightness despite GCC production capacity availability at site.

The market in Latin America is anchored in Brazilian ammonia and urea import demand from Petrobras Nitrogenados and Heringer fertiliser distribution operations, with above 65% of Brazilian nitrogen fertiliser requirements met by imports from GCC, Russia, and North America, making Brazil the world's single largest nitrogen fertiliser import-dependent agricultural economy and the primary commercial beneficiary of CF Industries export volume growth when GCC supply is constrained.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Ammonia (CFR South East Asia) | Asia-Pacific | USD 480/MT | USD 380/MT | Rising | Argus Media ref |

| Ammonia (US Gulf export) | North America | USD 380/MT | USD 320/MT | Rising | CF Industries ref |

| Urea (FOB Black Sea) | Global | USD 380/MT | USD 310/MT | Rising | ICIS / Argus ref |

| Green Ammonia (NEOM offtake) | Global | USD 720/MT | USD 780/MT | Stable | Air Products ref |

| European Natural Gas (EUR/MWh) | Europe | EUR 58/MWh | EUR 42/MWh | Rising | TTF Hormuz ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and fertiliser and ammonia market publication monitoring including Argus Media and ICIS ammonia assessments.

Asian-delivered ammonia CFR South East Asia rose approximately 26.3% from USD 380 per metric tonne in Q2 2025 to USD 480 per metric tonne in Q2 2026, driven by GCC export supply constraint from Hormuz shipping disruption confirmed by the IMF in March 2026 removing above 18% of global traded ammonia from normal export channels, with European and Asian importers competing for available CF Industries and Trinidad and Tobago ammonia export volumes at above-commodity spot pricing. US Gulf Coast ammonia export pricing rose approximately 18.8% to USD 380 per metric tonne as CF Industries and Koch Fertilizer captured above-plan export volume from Hormuz-disrupted GCC supply replacement, reaching above 2.8 million metric tonnes per year of US ammonia export volume at Q1 and Q2 2026 run rate above the 2024 baseline. Urea FOB Black Sea rose approximately 22.6% to USD 380 per metric tonne on the same GCC nitrogen supply disruption logic, with Indian government tender procurement from OCI NV and Yara at above-spot prices confirming the kharif season procurement urgency. European natural gas at TTF rose approximately 38.1% from EUR 42 per megawatt-hour in Q2 2025 to EUR 58 per megawatt-hour in Q2 2026 from Hormuz LNG supply disruption, above the Yara Sluiskil and Ferrara variable cost breakeven threshold and sustaining Yara European ammonia production curtailment at 12% to 18% of normal European output.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the ammonia market, the Hormuz disruption is the primary market-defining event of the current period rather than a secondary feedstock cost driver. SABIC Saudi Jubail, Qatar Industries Mesaieed, and ADNOC Ruwais collectively operate above 18% of global traded ammonia export capacity at GCC natural gas feedstock costs of USD 0.50 to USD 0.75 per million BTU, representing the world's most cost-competitive Haber-Bosch production. The Hormuz disruption constrains these exports from reaching European and Asian nitrogen fertiliser and industrial ammonia customers, creating above-plan spot market price premiums of approximately 26% at CFR South East Asia ammonia benchmarks in Q2 2026 against Q2 2025. European natural gas at TTF rose approximately 38.1% to EUR 58 per megawatt-hour from Hormuz LNG supply disruption, triggering Yara production curtailments at Sluiskil and Ferrara that further tighten European nitrogen fertiliser supply beyond the direct GCC export constraint. CF Industries at Donaldsonville, Koch Fertilizer at Dodge City, and OCI NV at Beaumont benefit commercially from the Hormuz disruption through above-plan export volume capture at above-spot pricing, with CF Industries confirming above 2.4 million metric tonnes per year of US ammonia export volume in 2024 growing further in 2025 and 2026 as GCC supply constraint opens market share for US Gulf Coast supply. The kharif 2026 South Asian planting season represents the most acute near-term food security risk from the Hormuz-driven ammonia supply constraint, with Indian government emergency urea procurement tenders and Bangladesh and Pakistan fertiliser import programmes competing for available non-GCC ammonia and urea supply at above-plan procurement cost.

Company Insights

The two key dominant companies in the ammonia market are CF Industries and Yara International, recognised for their leadership in low-cost US Gulf Coast Haber-Bosch production and in European and global nitrogen fertiliser and green ammonia production respectively, their contrasting positions as the primary commercial beneficiary of Hormuz-driven GCC supply disruption and the world's largest nitrogen fertiliser company facing European production curtailment from the same event.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 68.4 Billion |

| Market Size 2032 | USD 92.8 Billion |

| CAGR | 4.1% |

| Units | Revenue in USD Billion |

| Segments Covered | By Production Route, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Netherlands, Germany, Norway, Saudi Arabia, Qatar, UAE, China, India, Japan, Brazil, Australia |

| Companies Profiled | CF Industries, Yara International, SABIC, ADNOC, Qatar Industries, OCI NV, Koch Fertilizer, EuroChem, Nutrien, ACWA Power |

| Key Data Sources | Yara International 2024 annual report, CF Industries 2024 annual report, SABIC 2024 annual report fertiliser segment, IFA 2025 global fertiliser supply and demand report, JERA Q3 2025 Hekinan co-firing milestone, NEOM Helios Q2 2025 construction progress, OCI NV Fertiglobe blue ammonia commissioning Q3 2025, IMF March 2026 Hormuz disruption confirmation, 16 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 262 |

| Published | Q2 2026 |

| SKU | NXC-PC-017 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 16 expert interviews between January and May 2026. Supply-side contacts included ammonia production and commercial managers at CF Industries and Yara International, GCC fertiliser export commercial leads at SABIC and ADNOC, and green ammonia project development contacts at ACWA Power and Yara Herøya programme teams. Demand-side contacts included European nitrogen fertiliser importer procurement managers, Indian government emergency urea procurement programme contacts, Japanese JERA co-firing programme procurement leads, and green ammonia industrial offtake programme contacts. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Yara International 2024 annual report, CF Industries 2024 annual report, SABIC 2024 annual report fertiliser segment, IFA 2025 global fertiliser supply and demand report, JERA Q3 2025 Hekinan ammonia co-firing milestone disclosure, NEOM Helios Q2 2025 construction progress update, OCI NV Fertiglobe blue ammonia commissioning Q3 2025, Yara Q1 2026 European production curtailment announcement, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.