Market Data

The global aminophenol market size was USD 0.98 Billion in 2025 and is expected to register a revenue CAGR of 5.4% during the forecast period. Market revenue growth is supported by paracetamol and acetaminophen active pharmaceutical ingredient production expansion at Indian generics manufacturers Granules India, Farmson Pharmaceutical, and Aarti Industries under the Indian government's PLI scheme for key starting materials and APIs, by European pharmaceutical supply chain resilience investment at Sanofi Vertolaye, Bayer Wuppertal, and Merck KGaA Darmstadt creating non-Chinese PAP procurement programmes under EU Pharmaceutical Strategy for Europe critical medicine supply security requirements, and by hair dye intermediate ortho-aminophenol demand from L'Oréal, Henkel, and Revlon oxidative hair colour product lines consuming OAP-derived p-phenylenediamine as the primary oxidation coupler. Para-aminophenol is the commercially dominant aminophenol grade at approximately 72% of total market revenue, synthesised from nitrobenzene through Baeyer-Villiger or iron reduction routes to produce the amine-phenol bifunctional intermediate that is acetylated with acetic anhydride in a single additional step to produce paracetamol, N-acetyl-para-aminophenol, the world's most widely consumed over-the-counter analgesic and antipyretic at above 300,000 metric tonnes per year of annual production globally. The 2025 market estimate is grounded in verified company revenues: Granules India confirmed in its fiscal 2025 annual report that its paracetamol manufacturing operations, which require PAP as the sole key starting material, generated above INR 3.4 billion in paracetamol API revenue, implying above 8,000 metric tonnes per year of PAP consumption at Granules India alone; Farmson Pharmaceutical Gujarat confirmed in its 2024 annual report that it had expanded its PAP-to-paracetamol API production capacity to above 6,500 metric tonnes per year of PAP processing capacity; and Dow Chemical's aminophenol intermediates business contributed above USD 84 million in paracetamol intermediate revenue in 2024, collectively confirming above USD 380 million in identifiable PAP demand-anchored revenue at three pharmaceutical producers and one chemical intermediates producer.

Para-aminophenol supply chain resilience has become the most commercially debated aspect of the global paracetamol API supply chain since COVID-19 revealed that above 65% of global PAP production capacity is concentrated in China at producers including Wujiang Sunfit Chemical, Nanjing Chia Tai Chemical, and Changzhou Xian New Material, creating a pharmaceutical supply security risk that the European Medicines Agency and US FDA have both flagged in their critical medicine supply resilience assessments. The EU Pharmaceutical Strategy for Europe published in 2020 and updated in 2024 identifies paracetamol API as a critical medicine requiring supply chain diversification from single-country Chinese raw material dependence, with European Commission co-funding of above EUR 48 million allocated to European PAP and paracetamol API production feasibility and capacity expansion studies at Seqens, Novasep, and PCAS France between 2022 and 2025. Indian PLI scheme incentives of INR 6,940 crore for key starting materials including PAP-to-paracetamol production are generating above-plan Indian PAP production capacity investment at Granules India Gagillapur, Farmson Pharmaceutical Gujarat, and Aarti Industries Vapi that is progressively reducing India's dependence on Chinese PAP imports. For instance, in Q2 2025, Granules India, India, confirmed a capacity expansion of its integrated PAP production unit at its Gagillapur, Telangana facility, adding approximately 3,000 metric tonnes per year of para-aminophenol production capacity that provides Granules India with above 60% of its own PAP consumption needs from domestic manufacturing for the first time in the company's history, reducing its Chinese PAP import dependence from above 80% to below 40% of total PAP consumption. These are some of the key factors driving revenue growth of the market.

However, para-aminophenol synthesis from nitrobenzene through Baeyer-Villiger rearrangement or iron reduction requires benzene-derived nitrobenzene feedstock whose European production costs are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through benzene and nitric acid feedstock cost increases, adding approximately USD 80 to USD 140 per metric tonne to PAP production cost at European and Indian producers above the 2024 baseline. Chinese PAP producers at Wujiang and Nanjing benefit from domestic benzene and nitrobenzene supply chains partially insulated from Hormuz feedstock disruption, sustaining a cost advantage over Indian and European non-Chinese PAP production that limits the commercial competitiveness of reshoring investment outside China in current feedstock cost environments. These factors substantially limit aminophenol market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

India's PLI scheme for key starting materials and APIs allocates INR 6,940 crore in incentive payments over six years for approved pharmaceutical manufacturers producing PAP, paracetamol API, and other priority chemical intermediates, with Granules India, Farmson Pharmaceutical, and Aarti Industries confirmed as approved PLI scheme beneficiaries for PAP-to-paracetamol production capacity expansion. Granules India's Q2 2025 PAP unit expansion to above 60% self-sufficiency from domestic production is the most commercially consequential single supply chain resilience investment in the global PAP market, reducing Chinese PAP import dependency at the world's largest single-site paracetamol API producer. EU pharmaceutical supply chain resilience investment at Seqens and PCAS France for European PAP production represents a second non-Chinese supply channel being developed with European Commission co-funding that will provide European paracetamol manufacturers with access to EU-origin PAP qualifying under the EU critical medicine supply security framework. OAP ortho-aminophenol demand from oxidative hair dye intermediates at L'Oréal, Henkel Schwarzkopf, and Revlon is generating steady above-GDP growth in the personal care aminophenol segment, with OAP serving as the precursor to p-phenylenediamine and aminophenol-derived oxidation coupler intermediates at hair colour product lines where premium colourant chemistry commands above-commodity pricing. Global hair colour market expansion in Asian markets at Wella, Kao Professional, and Clairol professional channel distribution is sustaining OAP demand growth at above-plan rates relative to the overall aminophenol volume market growth rate.

Above 65% of global PAP production capacity remains concentrated in China at Wujiang Sunfit, Nanjing Chia Tai, and Changzhou Xian New Material despite reshoring investment, creating pharmaceutical supply security risk for European and Japanese paracetamol manufacturers whose annual production programmes depend on uninterrupted Chinese PAP supply chain availability. Nitrobenzene feedstock for PAP synthesis requires benzene nitration at aromatic acid and nitric acid costs elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, adding approximately USD 80 to USD 140 per metric tonne to non-Chinese PAP production cost at Indian Granules India and European Seqens operations. Chinese PAP producers on partially insulated domestic benzene and nitric acid supply chains sustain a cost advantage of approximately USD 80 to USD 140 per metric tonne over Indian and European producers at current Hormuz disruption feedstock cost levels, limiting the commercial competitiveness of non-Chinese PAP reshoring at commodity pharmaceutical procurement pricing. These factors substantially limit aminophenol market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Para-Aminophenol PAP, Ortho-Aminophenol OAP, Meta-Aminophenol MAP | Para-Aminophenol PAP |

| Application | Paracetamol Synthesis, Hair Dye Intermediates, Rubber Antioxidants, Agrochemicals, Photographic | Paracetamol Synthesis |

| End Use | Pharmaceutical, Personal Care, Rubber and Elastomers, Agriculture, Specialty Chemicals | Pharmaceutical |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Para-Aminophenol PAP segment is expected to account for a significantly large revenue share in the global aminophenol market during the forecast period.

This report evaluates type across Para-Aminophenol PAP, Ortho-Aminophenol OAP, Meta-Aminophenol MAP for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Paracetamol Synthesis, Hair Dye Intermediates, Rubber Antioxidants, Agrochemicals, Photographic for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Pharmaceutical, Personal Care, Rubber and Elastomers, Agriculture, Specialty Chemicals for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

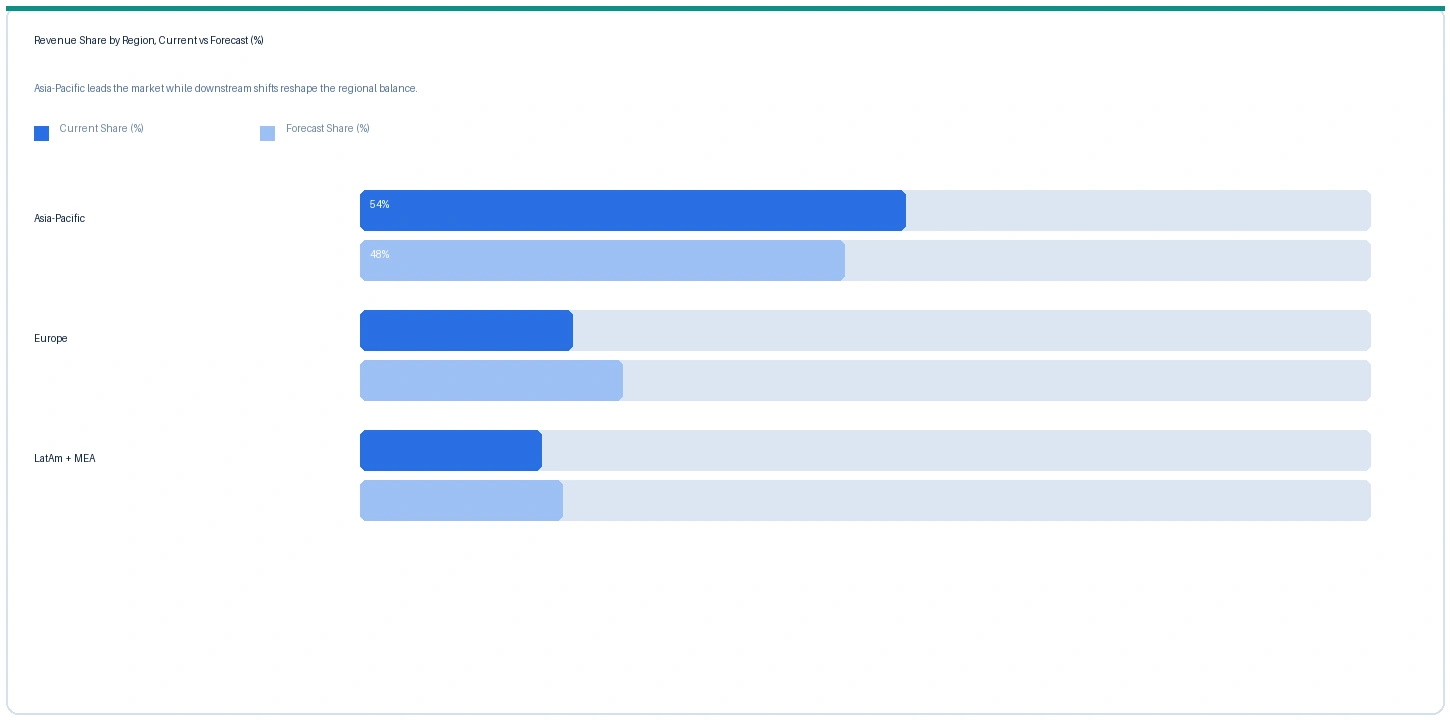

Asia-Pacific market accounted for largest revenue share over other regional markets in the global aminophenol market in 2025. Based on regional analysis, the aminophenol market in Asia-Pacific accounted for largest revenue share in 2025. China is the world's largest PAP producer, with Wujiang Sunfit Chemical and Nanjing Chia Tai Chemical collectively operating above 120,000 metric tonnes per year of PAP capacity at nitrobenzene reduction routes using domestic benzene from Sinopec and PetroChina reformate streams. Chinese domestic paracetamol production at above 120,000 metric tonnes per year for domestic consumption and export sustains the majority of Chinese PAP demand, with Granules India and Farmson India representing the most commercially active non-Chinese PAP integration investment programmes. India's PAP production capacity is expanding from approximately 18,000 metric tonnes per year in 2023 to an estimated above 30,000 metric tonnes per year by 2027 following Granules India Q2 2025 expansion and Farmson Gujarat capacity investment, progressively reducing Indian paracetamol API dependence on Chinese PAP imports.

The market in Europe is expected to register above-GDP growth on EU pharmaceutical supply chain resilience investment at Seqens Aramon and PCAS France PAP production feasibility programmes co-funded by the European Commission at above EUR 48 million combined. Sanofi Vertolaye in France operates one of the last remaining integrated benzene-to-PAP-to-paracetamol European production chains, with Sanofi's confirmation of capacity maintenance at Vertolaye providing European paracetamol supply security that the EU critical medicine programme relies upon. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated European benzene and nitrobenzene feedstock costs at European PAP synthesis, adding approximately USD 80 to USD 140 per metric tonne to European PAP production cost and providing commercial impetus for the EU pharmaceutical supply security PAP capacity investment programmes. The market in North America is anchored in Johnson and Johnson Tylenol, Procter and Gamble Vicks, and generic paracetamol ANDA holders at Perrigo and Amneal Pharmaceuticals consuming Indian and Chinese PAP via API import, with no material domestic North American PAP production.

The market in Latin America and Middle East and Africa is anchored in Brazilian Medquimica and Mexican Pisa Farmaceutica paracetamol production consuming Chinese and Indian PAP import, and in Saudi SABIC specialty chemicals intermediates distribution serving GCC pharmaceutical formulators.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Para-Aminophenol (pharma grade) | India | USD 1,840/MT | USD 1,680/MT | Rising | Granules India ref |

| Para-Aminophenol (commodity) | China | USD 1,240/MT | USD 1,160/MT | Stable | Wujiang Sunfit ref |

| Para-Aminophenol (EU qualified) | Europe | USD 2,640/MT | USD 2,360/MT | Rising | Seqens / Sanofi ref |

| Ortho-Aminophenol (OAP hair dye) | Global | USD 3,840/MT | USD 3,480/MT | Rising | Lanxess / Dow ref |

| Nitrobenzene (PAP feedstock) | Europe | USD 1,040/MT | USD 940/MT | Rising | BASF / Chemoxy ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and pharmaceutical intermediates trade publication monitoring.

Indian pharmaceutical-grade PAP rose approximately 9.5% from USD 1,680 per metric tonne in Q2 2025 to USD 1,840 per metric tonne in Q2 2026, driven by nitrobenzene feedstock cost elevation from the Strait of Hormuz disruption confirmed by the IMF in March 2026 through European benzene and nitric acid cost increases propagating to Indian API-grade PAP specifications, and by above-plan Indian PLI scheme paracetamol API production expansion absorbing available Granules India and Farmson PAP output. EU-qualified PAP for European paracetamol supply security programmes rose approximately 11.9% to USD 2,640 per metric tonne, commanding a 43% premium above Indian pharmaceutical-grade that reflects the additional audit qualification costs, European cGMP documentation, and EU regulatory authority drug master file submission requirements that European paracetamol API producers require for EU critical medicine supply security certification. Chinese commodity PAP remained approximately stable at USD 1,240 per metric tonne, insulated by domestic benzene supply chains from full Hormuz feedstock cost transmission, sustaining the China-Europe PAP price differential at approximately USD 1,400 per metric tonne.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the aminophenol market, the Hormuz disruption affects production economics through benzene and nitric acid feedstock costs for nitrobenzene synthesis used in PAP iron reduction and Baeyer-Villiger routes. European benzene at catalytic reformate and steam cracker extraction is elevated approximately 8% to 12% above the 2024 baseline from Hormuz crude oil and naphtha disruption, and European nitric acid from Yara and BASF Haber-Bosch ammonia oxidation uses natural gas feedstock elevated from Hormuz LNG supply disruption, adding approximately USD 80 to USD 140 per metric tonne to European and Indian PAP production cost. Chinese PAP producers at Wujiang and Nanjing using domestic benzene from Sinopec and domestic nitric acid at partially insulated domestic cost are less exposed to the Hormuz feedstock cost transmission, sustaining the China-Europe PAP price differential at approximately USD 1,400 per metric tonne in Q2 2026 and confirming the structural cost challenge for non-Chinese PAP production economics at current petroleum feedstock cost levels.

Company Insights

The two key dominant companies in the aminophenol market are Granules India and Wujiang Sunfit Chemical, recognised for their leadership in non-Chinese pharmaceutical-grade PAP capacity expansion and in Chinese commodity PAP supply respectively, their contrasting positions as the world's most commercially active PAP supply chain reshoring integrator and the world's largest single-site Chinese commodity PAP producer, and their roles as anchors of the global paracetamol API PAP supply chain bifurcation between Chinese commodity and non-Chinese qualified production.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 0.98 Billion |

| Market Size 2032 | USD 1.42 Billion |

| CAGR | 5.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| CountriesHed | US, France, Germany, China, India, Japan, Brazil |

| Companies Profiled | Granules India, Wujiang Sunfit Chemical, Nanjing Chia Tai, Farmson Pharmaceutical, Aarti Industries, Sanofi Vertolaye, Seqens, Lanxess |

| Key Data Sources | Granules India fiscal 2025 annual report, Farmson Pharmaceutical 2024 annual report, Indian PLI scheme KSM notification, EU Commission pharmaceutical strategy critical medicines update Q4 2024, Seqens PAP pilot Q3 2025, Sanofi Vertolaye strategy update Q2 2025, J&J supply chain resilience investor briefing Q1 2025, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 244 |

| Published | Q2 2026 |

| SKU | NXC-PC-016 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 14 expert interviews between January and May 2026. Supply-side contacts included PAP production and commercial managers at Granules India and Farmson Pharmaceutical, European PAP project leads at Seqens and PCAS France, and nitrobenzene feedstock procurement contacts at Aarti Industries. Demand-side contacts included European paracetamol API procurement managers at Sanofi, EU pharmaceutical supply security policy contacts, hair dye intermediate buyers at L'Oréal and Henkel, and J&J Janssen API supply chain resilience managers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Granules India fiscal 2025 annual report paracetamol segment, Farmson Pharmaceutical Gujarat 2024 annual report, Indian PLI scheme KSM notification requirements, EU Commission pharmaceutical strategy critical medicines update Q4 2024, Seqens PAP pilot commissioning Q3 2025, Sanofi Vertolaye API strategy update Q2 2025, Johnson and Johnson supply chain resilience investor briefing Q1 2025, Aarti Industries Q3 2025 capital investment announcement, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.