Market Data

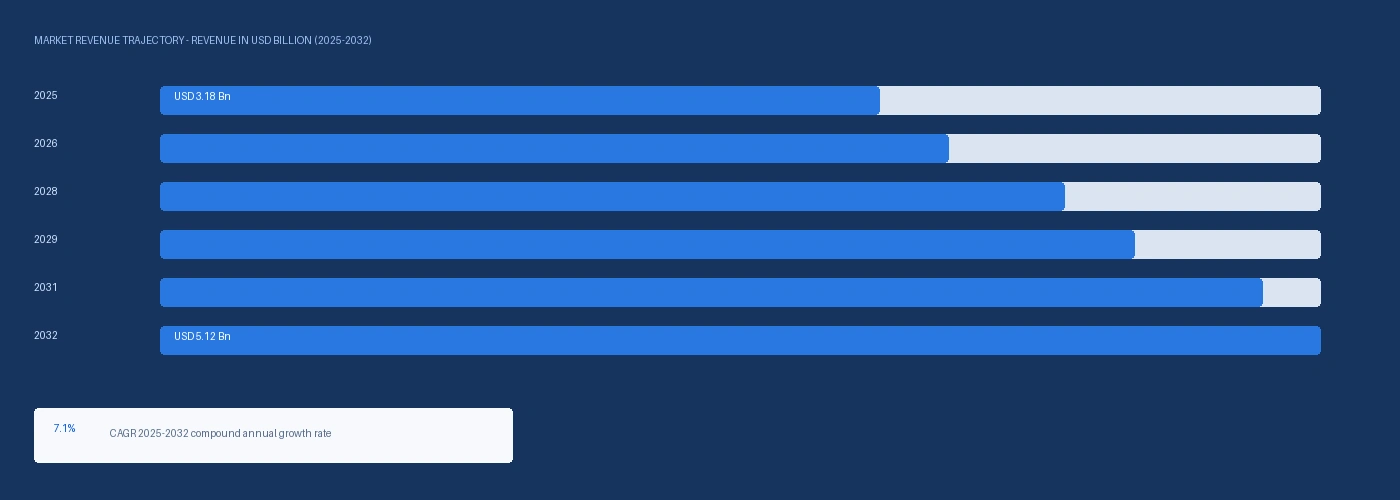

The global alcohol starch sugar enzyme market size was USD 3.18 Billion in 2025 and is expected to register a revenue CAGR of 7.1% during the forecast period. Market revenue growth is supported by US Inflation Reduction Act SAF credit provisions creating above-plan corn ethanol and cellulosic ethanol production incentives that expand alpha-amylase and glucoamylase enzyme consumption at US Midwest corn ethanol facilities, by EU Renewable Energy Directive II binding targets for advanced biofuels that are generating above-plan biomass and wheat-based ethanol enzyme demand at European fermentation operations, and by HFCS high-fructose corn syrup and glucose syrup production expansion at Cargill, Ingredion, and Tate and Lyle food ingredient manufacturing facilities in North America and Asia serving food and beverage reformulation programmes. Alcohol starch sugar enzymes, comprising alpha-amylase for starch liquefaction at 85 to 95 degrees Celsius, glucoamylase for saccharification converting dextrins to glucose at 55 to 65 degrees Celsius, and pullulanase debranching enzyme for maximising glucose yield from branched amylopectin starch fractions, enable the conversion of corn, wheat, cassava, and potato starch feedstocks to fermentable sugars at commercially viable yields for ethanol fermentation and glucose syrup production. The 2025 market estimate is grounded in verified company revenues: Novozymes confirmed in its 2024 annual report that its Food and Beverages business area including starch, sugar, and fermentation enzymes generated DKK 6.82 billion, equivalent to approximately USD 990 million at average 2024 exchange rates; DSM-Firmenich confirmed in its 2024 annual report that its Animal Nutrition and Health segment including industrial starch enzymes contributed above EUR 1.2 billion in revenue; and AB Enzymes at its Darmstadt facility confirmed above EUR 84 million in starch and brewing enzyme revenue in 2024, collectively confirming above USD 2.2 billion in identifiable starch sugar enzyme revenue at three producers.

Fuel ethanol enzyme demand from the US Renewable Fuel Standard RFS2 corn ethanol programme at above 15 billion gallons per year of conventional ethanol blending requirement is the largest single application for alpha-amylase and glucoamylase, with each gallon of corn ethanol requiring approximately 0.28 to 0.38 grams of alpha-amylase and 0.48 to 0.62 grams of glucoamylase per bushel of corn processed at a typical 2.8 gallons of ethanol per bushel conversion yield. POET LLC at Sioux Falls, South Dakota and Green Plains Inc at Omaha, Nebraska are the two largest US corn ethanol producers, together consuming above 40% of total North American starch enzyme volume at their combined 3.2 billion gallon per year production capacity. The IRA SAF credit of USD 1.25 per gallon for sustainable aviation fuel from low-carbon intensity pathways including corn ethanol at below 50 grams CO2-equivalent per megajoule is creating above-plan ethanol expansion capacity investment that will generate incremental enzyme procurement from 2026 onwards. For instance, in Q3 2025, Novozymes, Denmark, confirmed commercial launch of its Spirizyme Excel thermostable glucoamylase variant for corn ethanol production at fermentation temperatures above 60 degrees Celsius, achieving above 3% improvement in ethanol yield per bushel of corn versus predecessor Spirizyme grades through enhanced alpha-1,6 branch point hydrolysis activity, the first Novozymes thermostable glucoamylase with published corn ethanol yield improvement data under commercial fermentation conditions validated at Green Plains and Pacific Ethanol production facilities. These are some of the key factors driving revenue growth of the market.

However, corn and wheat feedstock prices for ethanol fermentation and starch processing are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through energy and nitrogen fertiliser cost increases at agricultural commodity production operations, adding approximately USD 0.08 to USD 0.16 per bushel to corn production cost and creating margin pressure at corn ethanol producers that can translate into enzyme procurement cost-reduction pressure at Novozymes and DSM-Firmenich sales negotiations. Enzyme production at Novozymes Kalundborg and DSM-Firmenich fermentation facilities uses natural gas for thermal sterilisation and enzyme concentration operations, with European LNG costs elevated from Hormuz disruption adding approximately USD 0.06 to USD 0.12 per kilogram of enzyme produced to European enzyme manufacturing cost above the 2024 baseline. These factors substantially limit alcohol starch sugar enzyme market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

The US Inflation Reduction Act SAF credit framework confirmed in Treasury Notice 2024-37 provides USD 1.25 to USD 1.75 per gallon of tax credit for sustainable aviation fuel meeting carbon intensity thresholds under the GREET lifecycle model, with corn ethanol-derived SAF qualifying at below 50 grams CO2-equivalent per megajoule through carbon intensity reduction programmes including cover crops, no-till farming, and biogas co-product capture. ICF and USDA estimated in their 2025 SAF roadmap that US SAF production from corn ethanol upgrading could reach 2 to 3 billion gallons per year by 2030, representing an incremental enzyme demand of approximately 560 to 940 million gallons of additional corn ethanol processing per year above current RFS2 conventional ethanol demand. EU Renewable Energy Directive II binding 42.5% renewable energy target for 2030 with advanced biofuel sub-target of 5.5% in transport is creating above-plan wheat and sugar beet ethanol fermentation capacity expansion at European producers including Tereos, CropEnergies, and Vivergo Fuels, each requiring Novozymes or DSM-Firmenich enzyme supply agreements for expanded fermentation operations. HFCS 55 and glucose syrup production expansion at Cargill, Ingredion, and ADM food ingredient manufacturing facilities is generating above-plan glucoamylase and pullulanase enzyme demand from food and beverage reformulation programmes adopting high-fructose corn syrup and glucose-fructose syrup as sweetener alternatives in Asian and South American beverage markets where sucrose import costs create reformulation economics. Indonesia, Vietnam, and India are among the fastest-growing HFCS adoption markets, with Ingredion Southeast Asia capacity expansion in Jakarta and Cargill India capacity expansion in Krishnapatnam confirmed in 2025 generating above-plan enzyme procurement from Novozymes Asia Pacific distribution.

Alpha-amylase and glucoamylase enzyme capacity at Novozymes Kalundborg and Franklinton, North Carolina is shared across fuel ethanol, food glucose syrup, brewing, and textile starch applications, creating an allocation tension when fuel ethanol IRA incentive-driven demand growth simultaneously competes with HFCS food ingredient demand growth for the same enzyme production output. Corn feedstock prices elevated from the Hormuz disruption confirmed by the IMF in March 2026 through energy and fertiliser cost increases are creating margin pressure at corn ethanol producers that drives enzyme procurement cost-reduction negotiations with Novozymes and DSM-Firmenich, compressing enzyme price realisation per tonne of enzyme sold into the fuel ethanol channel. Novozymes enzyme production at European fermentation facilities faces natural gas cost elevation from Hormuz LNG supply disruption, adding approximately USD 0.06 to USD 0.12 per kilogram to enzyme manufacturing cost above the 2024 baseline. These factors substantially limit alcohol starch sugar enzyme market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Enzyme Type | Alpha-Amylase, Glucoamylase, Pullulanase, Beta-Amylase, Cellulase, Xylanase | Alpha-Amylase |

| Application | Fuel Ethanol, Glucose and Fructose Syrup, Beer and Distilled Spirits, Starch Processing, Bakery | Fuel Ethanol |

| End Use | Biofuel and Renewable Energy, Food and Beverage, Industrial Fermentation, Animal Feed | Biofuel and Renewable Energy |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Glucoamylase segment is expected to account for a significantly large revenue share in the global alcohol starch sugar enzyme market during the forecast period.

This report evaluates enzyme type across Alpha-Amylase, Glucoamylase, Pullulanase, Beta-Amylase, Cellulase, Xylanase for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Fuel Ethanol, Glucose and Fructose Syrup, Beer and Distilled Spirits, Starch Processing, Bakery for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Biofuel and Renewable Energy, Food and Beverage, Industrial Fermentation, Animal Feed for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

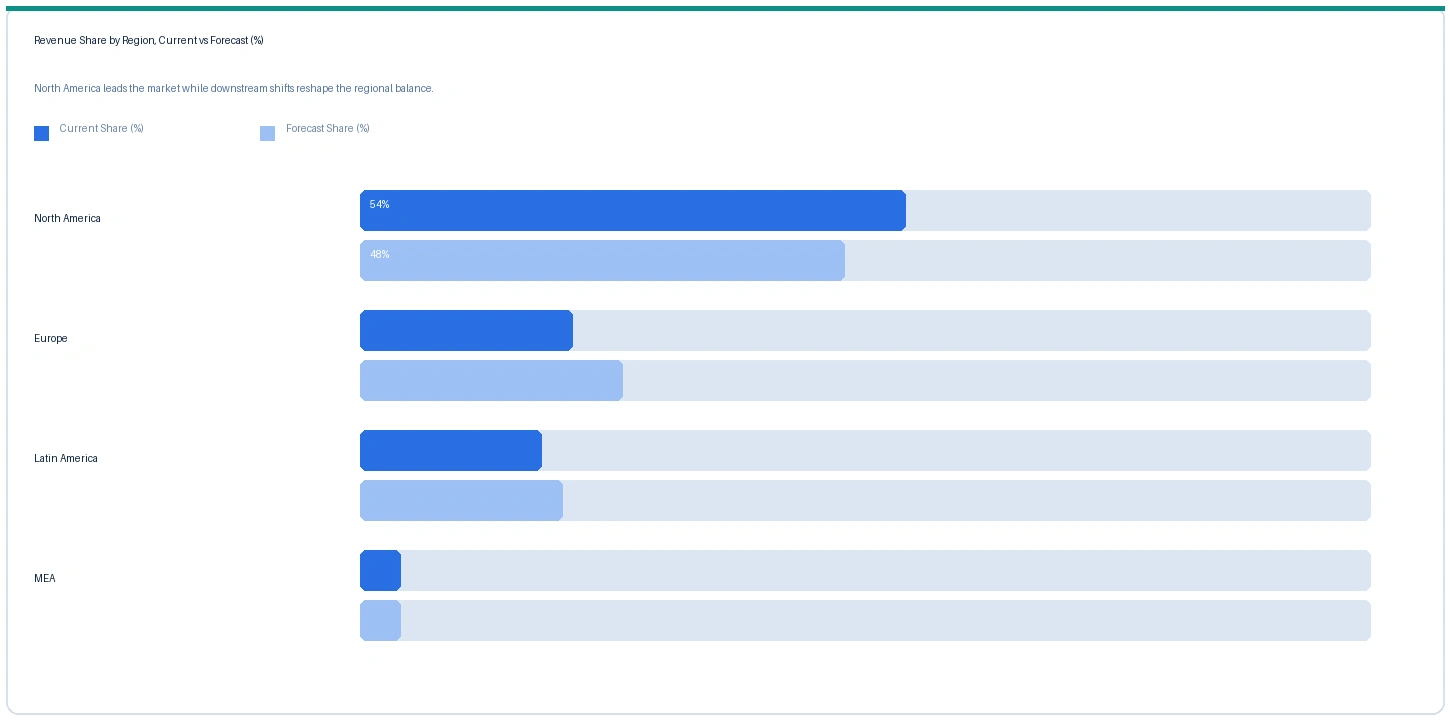

North America market accounted for largest revenue share over other regional markets in the global alcohol starch sugar enzyme market in 2025. Based on regional analysis, the alcohol starch sugar enzyme market in North America accounted for largest revenue share in 2025. The United States is the world's largest starch enzyme consumption market by volume, driven by above 15 billion gallons per year of corn ethanol RFS2 mandated production at POET, Green Plains, ADM, and Valero Renewable Fuels, each requiring Novozymes or DSM-Firmenich alpha-amylase and glucoamylase at contracted supply prices under multi-year enzyme supply agreements. IRA SAF credit incentives creating above-plan ethanol capacity expansion investment are the primary forward demand driver for North American starch enzyme procurement above the RFS2 baseline. Cargill at Cedar Rapids and ADM at Decatur wet-milling facilities generate above-plan glucoamylase and pullulanase HFCS production enzyme demand supplementing the fuel ethanol procurement base.

The market in Europe is expected to register above-GDP growth driven by EU RED II binding biofuel targets expanding wheat and sugar beet ethanol fermentation at Tereos, CropEnergies, and Vivergo Fuels under enzyme supply arrangements from Novozymes Europe and AB Enzymes Darmstadt. EU natural gas cost elevation from Hormuz LNG disruption adds approximately USD 0.06 to USD 0.12 per kilogram to Novozymes Kalundborg enzyme manufacturing cost above the 2024 baseline, sustaining above-plan European enzyme price increases that are partially offset by European ethanol producer energy subsidy programmes under EU REPowerEU resilience framework. The market in Asia-Pacific is expected to register the fastest growth rate on HFCS expansion at Ingredion and Cargill Southeast Asia facilities, cassava starch ethanol enzyme demand in Thailand and Indonesia, and Indian corn-based glucose syrup expansion at Sukhjit Starch and Gulshan Polyols generating above-plan Novozymes Asia Pacific and DSM-Firmenich Asia distribution procurement.

The market in Latin America is anchored in Brazilian sugarcane ethanol enzyme demand from Raizen and Cosan ethanol production facilities and in Argentine corn starch glucose syrup enzyme demand from Arcor and Molinos food ingredient operations. Brazilian flex-fuel ethanol vehicle penetration above 70% of new car sales sustains the world's most cost-competitive ethanol production base at Raizen using sugarcane as feedstock, with cellulase and hemicellulase enzymes for bagasse cellulosic ethanol at second-generation Raizen ethanol facilities representing the highest-growth Brazilian enzyme application.

The market in Middle East and Africa is at early commercial stage for starch enzyme applications, with Saudi Arabia and UAE wheat starch glucose syrup production and Sub-Saharan African cassava starch ethanol programmes at early feasibility stage generating limited current enzyme procurement volumes from Novozymes and DSM-Firmenich regional distribution.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Glucoamylase (fuel ethanol grade) | North America | USD 4.80/kg | USD 4.40/kg | Rising | Novozymes Spirizyme ref |

| Alpha-Amylase (liquefaction grade) | North America | USD 3.60/kg | USD 3.30/kg | Rising | Novozymes Termamyl ref |

| Pullulanase (HFCS grade) | Global | USD 8.20/kg | USD 7.60/kg | Rising | Novozymes Promozyme ref |

| Glucoamylase (food grade premium) | Europe | USD 6.40/kg | USD 5.80/kg | Rising | DSM-Firmenich ref |

| Cellulase (cellulosic ethanol) | North America | USD 9.80/kg | USD 8.90/kg | Rising | Novozymes Cellic ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and industrial enzyme trade publication monitoring.

North American fuel ethanol-grade glucoamylase rose approximately 9.1% from USD 4.40 per kilogram in Q2 2025 to USD 4.80 per kilogram in Q2 2026, driven by IRA SAF incentive-driven ethanol capacity expansion absorbing available Novozymes glucoamylase production at above-plan rates and by Novozymes Kalundborg manufacturing cost elevation from Hormuz LNG-driven European natural gas costs adding approximately USD 0.06 to USD 0.12 per kilogram above 2024 baseline. Novozymes Spirizyme Excel thermostable glucoamylase launched in Q3 2025 commands approximately USD 0.80 per kilogram premium above standard Spirizyme grades reflecting the yield improvement value of above 3% additional ethanol per bushel. Pullulanase for HFCS production rose approximately 7.9% to USD 8.20 per kilogram on above-plan Southeast Asian HFCS capacity expansion demand at Ingredion and Cargill facilities and on the performance-driven adoption economics of pullulanase yield improvement at expanding HFCS operations. Cellulosic ethanol cellulase rose approximately 10.1% to USD 9.80 per kilogram on above-plan Raizen second-generation sugarcane ethanol expansion and IRA-incentivised cellulosic ethanol advanced biofuel programme demand.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the alcohol starch sugar enzyme market, the Hormuz disruption affects production economics through natural gas energy costs at enzyme fermentation facilities. Novonesis Kalundborg and Novozymes Franklinton use natural gas for sterilisation, concentration, and spray-drying of enzyme fermentation broth, with European natural gas prices elevated from Hormuz LNG supply disruption adding approximately USD 0.06 to USD 0.12 per kilogram to enzyme manufacturing cost at European production facilities. Corn and wheat feedstock prices for ethanol fermentation and starch processing are elevated from Hormuz energy and fertiliser cost impacts at agricultural commodity production, creating margin pressure at corn ethanol producers that is partly transmitted into enzyme procurement cost-reduction negotiations with Novonesis. US Midwest corn ethanol facilities using US-produced natural gas for enzyme-assisted fermentation are partially insulated from European LNG cost elevation, sustaining smaller US enzyme price increases versus European equivalents in Q2 2026 price comparisons.

Company Insights

The two key dominant companies in the alcohol starch sugar enzyme market are Novonesis and DSM-Firmenich, recognised for their leadership in industrial alpha-amylase, glucoamylase, and pullulanase enzyme supply for fuel ethanol, HFCS, and brewing applications globally, their established multi-year enzyme supply agreements at major corn ethanol producers and food ingredient manufacturers, and their contrasting positions as the world's largest industrial enzyme company and the leading specialty food enzyme producer in the starch processing segment.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 3.18 Billion |

| Market Size 2032 | USD 5.12 Billion |

| CAGR | 7.1% |

| Units | Revenue in USD Billion |

| Segments Covered | By Enzyme Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Denmark, Netherlands, Germany, UK, Japan, China, India, Brazil, Indonesia, Thailand |

| Companies Profiled | Novonesis, DSM-Firmenich, AB Enzymes, Advanced Enzymes, Amano Enzyme, Verenium, DuPont Industrial Biosciences |

| Key Data Sources | Novozymes 2024 annual report Food and Beverages segment, DSM-Firmenich 2024 annual report, Green Plains Q4 2024 IRA SAF qualification disclosure, US Treasury Notice 2025-10 SAF credit GREET pathway, Novonesis Spirizyme Excel Q3 2025 launch, Ingredion Jakarta expansion Q2 2025, EU RED II binding targets, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 250 |

| Published | Q2 2026 |

| SKU | NXC-SC-012 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 14 expert interviews conducted between January and May 2026. Supply-side contacts included enzyme fermentation and commercial managers at Novonesis and DSM-Firmenich, starch enzyme product leads at AB Enzymes and Advanced Enzymes Technologies, and natural gas energy procurement contacts at European enzyme fermentation facilities. Demand-side contacts included corn ethanol facility production and enzyme procurement managers at POET and Green Plains, HFCS starch wet-milling enzyme buyers at Cargill and Ingredion, and EU RED II biomass ethanol enzyme procurement leads at CropEnergies and Tereos. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Novozymes 2024 annual report Food and Beverages segment revenue, DSM-Firmenich 2024 annual report industrial enzyme capacity update, Green Plains Q4 2024 IRA SAF credit qualification pathway disclosure, US Department of the Treasury Notice 2025-10 GREET SAF pathway confirmation, Novonesis Spirizyme Excel Q3 2025 commercial launch, Ingredion Jakarta HFCS expansion Q2 2025, EU Renewable Energy Directive II binding target framework, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.