Market Data

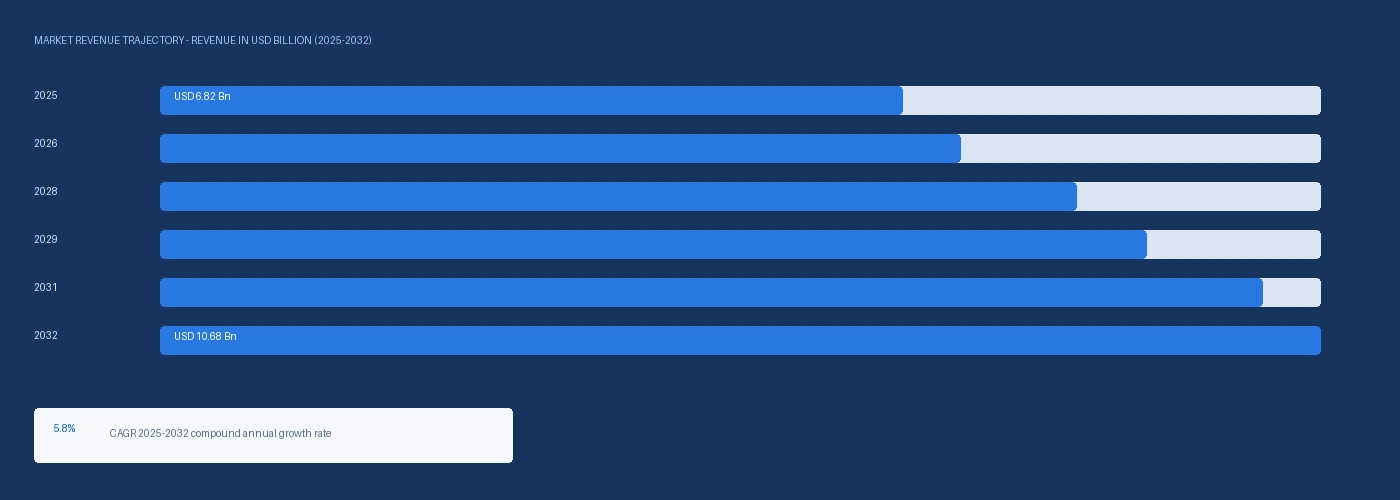

The global adipic acid market size was USD 6.82 Billion in 2025 and is expected to register a revenue CAGR of 5.8% during the forecast period. Market revenue growth is supported by nylon 6,6 demand from automotive airbag system yarn at above-plan vehicle safety system content increases in new car assessment programme-rated vehicles, from engineering plastic nylon 6,6 compound adoption in EV powertrain thermal management components replacing aluminium at BMW, Toyota, and Valeo, and from polyurethane polyol synthesis for flexible foam applications in automotive seating and residential furniture where adipic acid-based polyester polyols compete with polyether polyol systems. Adipic acid is produced almost exclusively through the two-stage cyclohexane oxidation KA oil process, where benzene is hydrogenated to cyclohexane and subsequently air-oxidised to a ketone-alcohol mixture that is further oxidised with nitric acid to yield adipic acid at approximately 92% to 94% selectivity, with nitrous oxide N2O as a co-product requiring catalytic abatement under EU Industrial Emissions Directive due to N2O's global warming potential of approximately 310 times CO2 on a 100-year basis. The 2025 market estimate is grounded in verified company revenues: Invista confirmed in KOCH Industries investor communications that its nylon intermediates business including adipic acid and hexamethylenediamine generated above USD 1.8 billion in annual revenue; BASF SE reported in its Performance Chemicals segment disclosure that its cyclohexane-based adipic acid production at Ludwigshafen contributed approximately EUR 680 million to its 2024 petrochemicals revenue; and Asahi Kasei confirmed in its 2025 annual report that its Performance Products segment including adipic acid and nylon 6,6 polymer generated JPY 186 billion, collectively confirming above USD 3.1 billion in identifiable adipic acid and nylon intermediate revenue at three major producers.

Nylon 6,6 yarn for automotive airbag fabric is the single most specification-critical adipic acid derivative application, consuming approximately 58% of global adipic acid production and requiring nylon 6,6 polymer grade consistency at relative viscosity above 2.5 and amine end group content within tightly controlled ranges that prevent hydrolytic degradation over the vehicle lifetime. Global Airbag Alliance data confirmed in its 2024 industry report that global airbag unit production exceeded 890 million units in 2024 on above-plan deployment of side-curtain, knee, and centre airbags in five-star Euro NCAP and NHTSA-rated vehicles at Ford, Hyundai, and Toyota, with each airbag cushion consuming approximately 250 to 480 grams of nylon 6,6 fabric yarn from Invista Cordura and Ascend Performance Materials Vydyne supply lines. Engineering plastic nylon 6,6 compounds from LANXESS Durethan, Solvay Technyl, and BASF Ultramid represent the second derivative channel, with EV powertrain thermal management applications at above 150 degrees Celsius operating temperature requiring nylon 6,6 rather than nylon 6 due to the higher melting point of 262 degrees Celsius versus 220 degrees Celsius providing the additional temperature margin for under-hood EV applications. For instance, in Q2 2025, Invista, United States, confirmed a debottlenecking programme at its Victoria, Texas adipic acid production facility targeting an incremental capacity increase of approximately 50,000 metric tonnes per year, responding to above-plan nylon 6,6 airbag yarn demand from Autoliv, Joyson Safety Systems, and ZF TRW airbag cushion fabric procurement programmes. These are some of the key factors driving revenue growth of the market.

However, cyclohexane feedstock for adipic acid KA oil production is derived from benzene hydrogenation, with benzene sourced from catalytic reformate and steam cracker by-product streams at European and Asian refineries whose feedstock costs are elevated approximately 8% to 12% above the 2024 baseline from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through naphtha and crude oil supply restriction, adding approximately USD 60 to USD 110 per metric tonne to European adipic acid production cost. N2O abatement capital expenditure requirements under the EU Industrial Emissions Directive at adipic acid production facilities represent an above-plan capital cost that reduces the returns available for capacity expansion investment, with Invista Victoria and BASF Ludwigshafen both operating catalytic N2O abatement units that require periodic catalyst replacement at costs of USD 8 to USD 18 million per turnaround event. Bio-based adipic acid routes from renewable feedstocks including glucose fermentation at Verdezyne and Genomatica have not yet reached commercial production scale competitive with petroleum-based KA oil routes on cost, limiting the green chemistry alternative's commercial contribution to the overall market. These factors substantially limit adipic acid market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Global airbag unit production exceeding 890 million units in 2024 per Global Airbag Alliance data, driven by above-plan side-curtain and centre airbag deployment in five-star NCAP-rated vehicles, is consuming nylon 6,6 airbag yarn from Invista and Ascend at above-historical-average rates. Each five-star Euro NCAP vehicle rating requires additional airbag positions versus the 2018 NCAP baseline, with the 2026 Euro NCAP protocol requiring driver knee airbag, front-centre airbag, and pedestrian airbag systems on all five-star rated models, adding approximately 200 to 350 grams of additional nylon 6,6 airbag fabric per vehicle above the pre-2026 standard. Ford, Hyundai, and Toyota confirmed in their respective safety system supplier communications that airbag content per vehicle was increasing on all 2026 model year platforms targeting five-star NCAP ratings, confirming the incremental nylon 6,6 yarn demand per vehicle that flows directly to adipic acid and hexamethylenediamine procurement at Invista and Ascend supply chains. At global vehicle production of approximately 94 million units in 2024 per OICA and approximately 9.8 airbags per vehicle average content on five-star rated vehicles, airbag nylon 6,6 fabric consumes approximately 206,000 to 407,000 metric tonnes per year of nylon 6,6 yarn, requiring approximately 140,000 to 280,000 metric tonnes of adipic acid annually from the airbag application alone. EV engineering plastic nylon 6,6 compound adoption at powertrain thermal management, battery cooling system, and electrical connector applications is the fastest-growing end-use channel for nylon 6,6, driven by the 262 degrees Celsius melting point advantage over nylon 6 in continuous-use applications adjacent to EV motor and inverter heat sources. LANXESS Durethan BKV 130 H2.0 nylon 6,6 compound and BASF Ultramid A3WG6 are specified at above-plan rates at Bosch, Valeo, and Aptiv EV connector and thermal management component manufacturing programmes, with each EV platform consuming approximately 2.8 to 4.6 kilograms of nylon 6,6 engineering plastic compound in connectors, cable ties, and cooling circuit components versus approximately 1.2 to 2.4 kilograms on equivalent ICE platforms.

Cyclohexane for adipic acid production is produced by benzene hydrogenation at dedicated units at Invista Victoria, BASF Ludwigshafen, and Asahi Kasei Mizushima using refinery and cracker-derived benzene that is elevated approximately 8% to 12% above the 2024 baseline from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, adding approximately USD 60 to USD 110 per metric tonne to European adipic acid production cost. Nitric acid oxidation of KA oil to adipic acid produces N2O at approximately 0.26 to 0.31 kilograms of N2O per kilogram of adipic acid, with each metric tonne of N2O carrying a CO2 equivalent warming impact of approximately 310 metric tonnes CO2-eq, creating an EU ETS cost burden at adipic acid producers subject to EU emission trading scheme allowances at current carbon prices of approximately USD 60 to USD 70 per metric tonne CO2-eq. The N2O abatement units at BASF and Invista convert N2O to nitrogen and oxygen through catalytic reduction at above 99% efficiency, but catalyst replacement events at every 5 to 8 years represent USD 8 to USD 18 million per event capital expenditure requirements that reduce capacity expansion returns and sustain a structural barrier against greenfield adipic acid investment by new market entrants without existing N2O abatement infrastructure. These factors substantially limit adipic acid market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Application | Nylon 6, 6 Production, Polyurethane Polyol, Plasticisers, Lubricant Additives, Food Acidulant | Nylon 6 |

| End Use | Automotive Airbags and Engineering Plastics, Textiles and Apparel, Flexible PU Foam, Rigid PU Insulation, Food and Beverage | Automotive Airbags and Engineering Plastics |

| Production Route | Cyclohexane Oxidation KA Oil Process, Cyclohexene Oxidation, Bio-Based Routes | Cyclohexane Oxidation KA Oil Process |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Nylon 6,6 Production segment is expected to account for a significantly large revenue share in the global adipic acid market during the forecast period.

This report evaluates application across Nylon 6, 6 Production, Polyurethane Polyol, Plasticisers, Lubricant Additives, Food Acidulant for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive Airbags and Engineering Plastics, Textiles and Apparel, Flexible PU Foam, Rigid PU Insulation, Food and Beverage for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates production route across Cyclohexane Oxidation KA Oil Process, Cyclohexene Oxidation, Bio-Based Routes for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

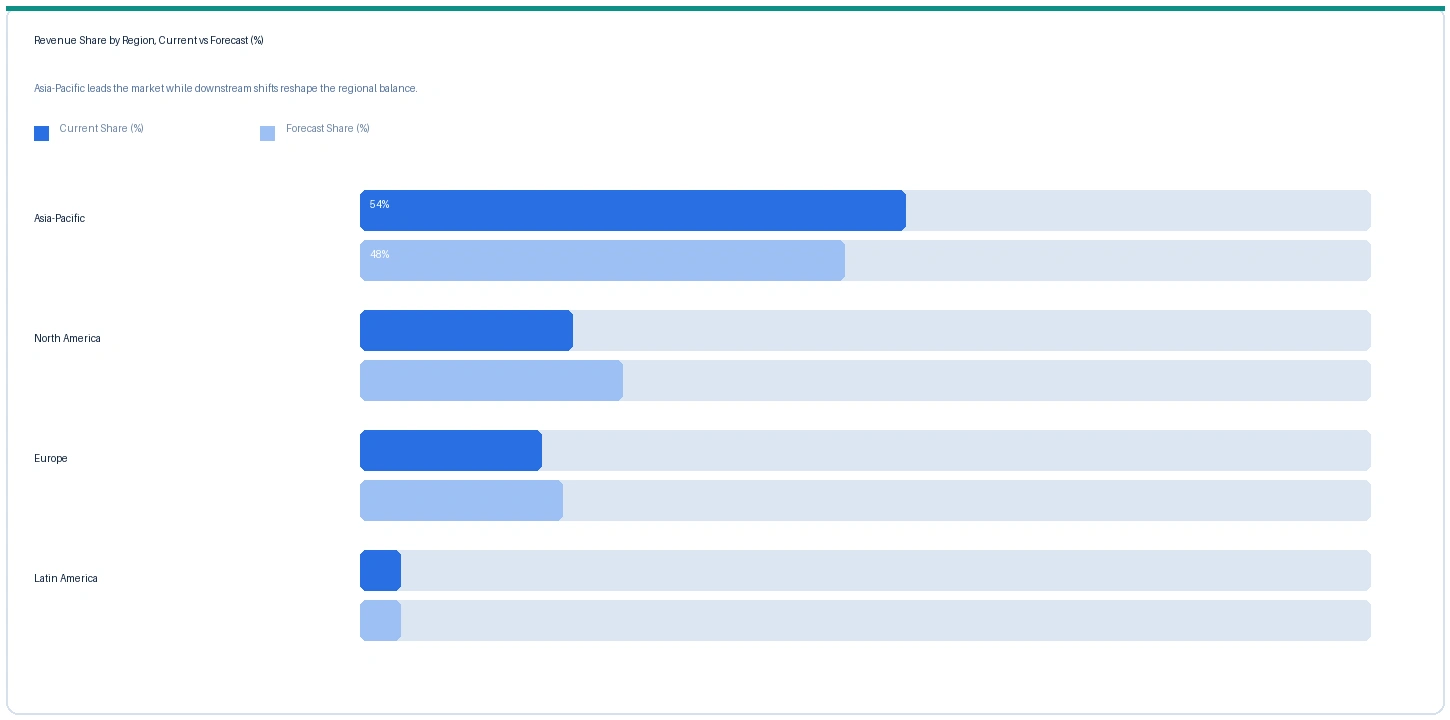

Asia-Pacific market accounted for largest revenue share over other regional markets in the global adipic acid market in 2025. Based on regional analysis, the adipic acid market in Asia-Pacific accounted for largest revenue share in 2025. China is the world's largest adipic acid producer and consumer, with Shenma Group at Pingdingshan, Henan; China Shenghong Petrochemical; and Huafon Chemical at Chongqing collectively operating above 1.8 million metric tonnes per year of domestic adipic acid nameplate capacity using domestic benzene-derived cyclohexane feedstock partially insulated from GCC feedstock disruption. Chinese domestic nylon 6,6 consumption at airbag fabric manufacturers including Huade Textile and Tianlun Nylon, and at engineering plastic compounders including Juhua Group, represents the world's largest single-country adipic acid demand base at above 40% of global consumption. Japan's Asahi Kasei at Mizushima produces adipic acid as an intermediate for its own nylon 6,6 polymer and for Toray Industries nylon 6,6 fibre programmes in an integrated manufacturing complex, with Asahi Kasei Performance Products JPY 186 billion revenue confirming the commercial scale of the Japanese adipic acid production and derivative system.

The market in North America is expected to register the second largest revenue share, anchored in Invista at Victoria, Texas as the world's largest single-site adipic acid producer and in Ascend Performance Materials at Chocolate Bayou, Texas as the second major North American producer, collectively supplying the North American nylon 6,6 airbag yarn, engineering plastic, and polyurethane polyol markets. Invista's Q2 2025 Victoria debottlenecking programme targeting 50,000 metric tonnes per year of incremental capacity confirms that North American airbag and EV engineering plastic nylon 6,6 demand is growing faster than current Victoria capacity can serve at planned utilisation rates. North American airbag system manufacturers Autoliv at Ogden, Utah and Joyson Safety Systems at Auburn Hills, Michigan are the primary North American airbag yarn procurement accounts, consuming Invista and Ascend adipic acid-derived nylon 6,6 yarn under multi-year automotive platform supply commitments.

The market in Europe is expected to register steady above-GDP growth driven by automotive airbag content increase at European five-star Euro NCAP 2026 protocol vehicle platforms at Volkswagen, BMW, and Stellantis, engineering plastic nylon 6,6 adoption at Bosch and Valeo EV connector and thermal management programmes, and polyurethane insulation rigid foam demand from EU Renovation Wave building envelope improvement programmes requiring adipic acid-based polyester polyol rigid foam at above-plan rates. BASF at Ludwigshafen and Invista European distribution supply European nylon 6,6 polymerisation at LANXESS Dormagen, DSM Engineering Materials, and Solvay Engineering Polymers for compound production. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated benzene and cyclohexane feedstock costs at BASF Ludwigshafen adipic acid production, contributing to European adipic acid price increases of approximately 9.6% against Q2 2025.

The market in Latin America is anchored in Brazil, where Braskem produces adipic acid at its Triunfo, Rio Grande do Sul integrated petrochemical complex for domestic nylon 6,6 polyurethane polyol and plasticiser consumption, and in Mexico, where automotive-grade nylon 6,6 engineering plastic compounds are consumed at Tier 1 automotive component manufacturers in the Bajio region. The market in Middle East and Africa is at early commercial adipic acid production, with SABIC at Jubail processing domestically produced cyclohexane for limited domestic nylon intermediate consumption, and the broader GCC market dependent on US and European adipic acid imports for polyurethane and nylon applications.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Adipic Acid (nylon grade) | Europe | USD 1,640/MT | USD 1,496/MT | Rising | BASF / Invista ref |

| Adipic Acid (nylon grade) | Asia-Pacific | USD 1,280/MT | USD 1,200/MT | Rising | Shenma / Huafon ref |

| Adipic Acid (PU polyol grade) | North America | USD 1,480/MT | USD 1,360/MT | Rising | Invista Victoria ref |

| Nylon 6,6 Polymer (airbag grade) | Global | USD 3,840/MT | USD 3,480/MT | Rising | Invista / Ascend ref |

| Cyclohexane (feedstock) | Europe | USD 980/MT | USD 880/MT | Rising | BASF cracker ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and petrochemical and nylon intermediates trade publication monitoring. Adipic acid is traded on a contract and spot basis; prices vary by grade, purity specification, and supply agreement structure.

European nylon-grade adipic acid rose approximately 9.6% from USD 1,496 per metric tonne in Q2 2025 to USD 1,640 per metric tonne in Q2 2026, driven by cyclohexane feedstock cost elevation of approximately 11.4% from USD 880 per metric tonne to USD 980 per metric tonne at BASF Ludwigshafen from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through benzene and naphtha feedstock cost increases at Ruhr Valley crackers, and by above-plan airbag yarn and EV engineering plastic nylon 6,6 demand drawing on available European adipic acid production. Asian nylon-grade adipic acid rose approximately 6.7% to USD 1,280 per metric tonne, with the Europe-Asia price differential widening from approximately USD 296 to approximately USD 360 per metric tonne reflecting greater European feedstock exposure to Hormuz-driven cyclohexane cost. North American polyurethane polyol-grade adipic acid rose approximately 8.8% to USD 1,480 per metric tonne on Invista Victoria capacity operating above plan ahead of the debottlenecking programme completion. Nylon 6,6 airbag-grade polymer rose approximately 10.3% to USD 3,840 per metric tonne globally on airbag content increase per vehicle from Euro NCAP 2026 protocol and above-plan EV engineering plastic nylon 6,6 demand at LANXESS and BASF compound production.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the adipic acid market, the Hormuz disruption affects production economics through two connected feedstock chains. Benzene for cyclohexane production is sourced from catalytic reformate and steam cracker by-product streams at European refineries whose crude oil throughput costs are elevated from Hormuz crude supply disruption, adding approximately USD 60 to USD 100 per metric tonne to European benzene prices above the 2024 baseline and consequently to European cyclohexane costs at benzene hydrogenation units at BASF Ludwigshafen and Invista European operations. Nitric acid for the second-stage oxidation of KA oil to adipic acid is produced from ammonia through the Ostwald process, with European ammonia production at Yara and BASF Haber-Bosch units using natural gas whose European cost is elevated from Hormuz LNG supply disruption, creating a secondary feedstock cost vector analogous to the dual propylene-ammonia cost impact in the acrylonitrile market. The combined benzene-derived cyclohexane and natural gas-derived nitric acid feedstock elevation adds approximately USD 60 to USD 110 per metric tonne to European adipic acid production cost relative to the 2024 baseline, explaining the approximately 9.6% European adipic acid price increase in Q2 2026 against Q2 2025 and the widening Europe-Asia price differential. Chinese adipic acid producers are partially insulated through domestic benzene supply chains and coal-based ammonia production that are less exposed to GCC feedstock disruption, sustaining the Chinese cost advantage and widening the Europe-Asia adipic acid price differential from approximately USD 296 to approximately USD 360 per metric tonne in Q2 2026.

Company Insights

The two key dominant companies in the adipic acid market are Invista and BASF SE, recognised for their leadership in airbag-grade nylon 6,6 adipic acid supply and in European adipic acid production and engineering plastic nylon compound supply respectively, their established airbag system manufacturer and engineering plastic compounder supply relationships, and their contrasting positions as the world's largest integrated nylon 6,6 and adipic acid producer and the leading European integrated petrochemical adipic acid producer.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 6.82 Billion |

| Market Size 2032 | USD 10.68 Billion |

| CAGR | 5.8% |

| Units | Revenue in USD Billion |

| Segments Covered | By Application, By End Use, By Production Route, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, France, UK, Japan, China, South Korea, India, Brazil, Saudi Arabia |

| Companies Profiled | Invista, BASF SE, Ascend Performance Materials, Asahi Kasei, Shenma Group, Huafon Chemical, China Shenghong, LANXESS, Radici Group, Rhodia Solvay |

| Key Data Sources | Invista Q2 2025 Victoria debottlenecking disclosure, BASF 2024 performance chemicals segment, Ascend Q4 2024 supplier day disclosure, Asahi Kasei 2025 annual report, Global Airbag Alliance 2024 industry report, Euro NCAP 2026 protocol publication, LANXESS Q3 2025 High Performance Materials investor update, OICA 2024 vehicle production statistics, IEA Global EV Outlook 2025, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 254 |

| Published | Q2 2026 |

| SKU | NXC-PC-014 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 14 expert interviews conducted between January and May 2026. Interview panels were structured across a 2x2 supply-side and demand-side grid with explicit geographic and role split. Supply-side contacts included adipic acid production and commercial managers at Invista and Ascend Performance Materials, nylon 6,6 engineering plastic compounding product leads at LANXESS and BASF, and cyclohexane and benzene feedstock procurement contacts at European adipic acid producers. Demand-side contacts included airbag system design and raw material procurement engineers at Autoliv and Joyson Safety Systems, EV connector and thermal management component nylon 6,6 procurement managers at European Tier 1 automotive suppliers, and polyurethane polyol formulation leads at European and North American foam producers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Invista Q2 2025 Victoria debottlenecking programme disclosure, BASF SE 2024 performance chemicals segment commentary, Ascend Performance Materials Q4 2024 Chocolate Bayou supplier day, Asahi Kasei 2025 annual report Performance Products segment, Global Airbag Alliance 2024 industry report, Euro NCAP 2026 testing protocol publication, LANXESS Q3 2025 High Performance Materials investor update, Shenma Group 2024 annual report, OICA 2024 global vehicle production statistics, IEA Global EV Outlook 2025, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.