Market Data

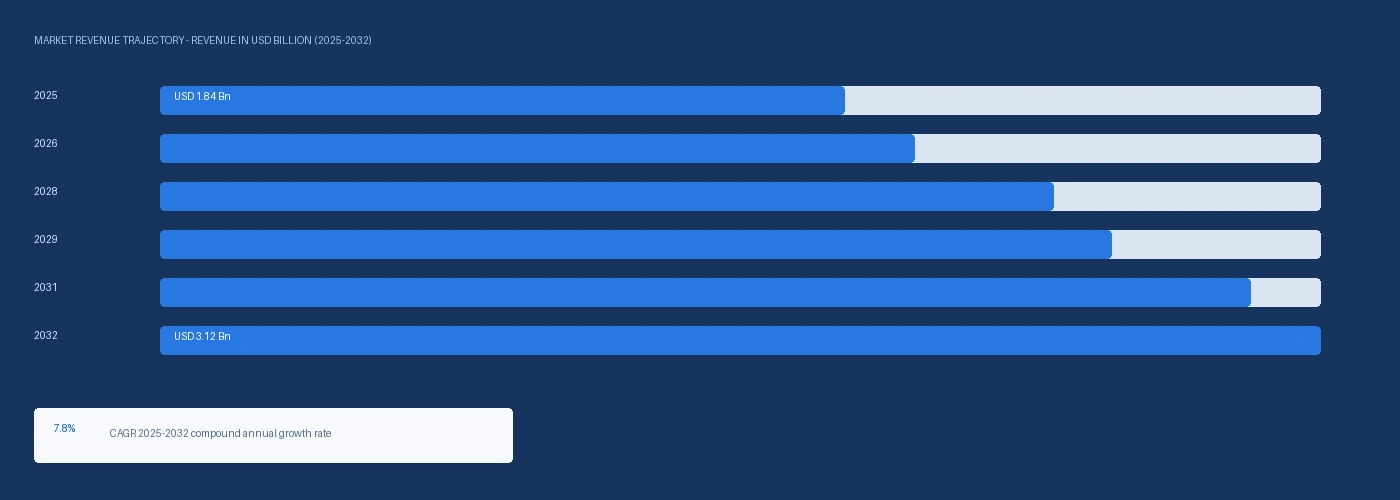

The global acrylic processing aid market size was USD 1.84 Billion in 2025 and is expected to register a revenue CAGR of 7.8% during the forecast period. Market revenue growth is supported by PVC pipe and fittings demand from water infrastructure rehabilitation programmes in the United States under the Infrastructure Investment and Jobs Act, from housing construction expansion in Southeast Asia at above-GDP growth rates, and from European district heating network pipe replacement programmes targeting decarbonisation of urban heat supply. Acrylic processing aids are high-molecular-weight methyl methacrylate copolymers, typically with molecular weights between 1 million and 6 million grams per mole, compounded into rigid PVC formulations at loadings of 0.5 to 3.0 parts per hundred resin to accelerate PVC gelation, improve melt homogeneity, reduce plate-out on processing equipment, and deliver surface quality improvements that rigid PVC cannot achieve at equivalent processing temperatures without the acrylic additive. The processing aid functions by acting as a rheology modifier at PVC processing temperatures of 170 to 210 degrees Celsius, entangling with PVC polymer chains to reduce the gelation time needed to develop the full mechanical properties specified in ASTM D1784 for rigid PVC pipe, profiles, and sheet. The 2025 market estimate is grounded in verified company revenues: Rohm and Haas Paraloid product line revenue, now part of Dow Chemical, was referenced in Dow's 2024 performance materials investor commentary as generating above USD 380 million in annual acrylic additive revenues across its processing aid and impact modifier product lines; Kaneka Corporation disclosed in its 2025 annual report that its acrylic processing aid and impact modifier product segment generated JPY 42.8 billion in revenue, equivalent to approximately USD 285 million at average 2024 exchange rates, confirming the two-producer concentration that defines the top tier of the global acrylic processing aid market. The American Society for Testing and Materials ASTM D1784 Class 12454 rigid PVC compound specification requires acrylic processing aid incorporation at commercial pipe extrusion formulations, creating a mandatory additive demand that scales directly with PVC pipe production volumes at North American pipe manufacturers.

Foam control acrylic processing aids for foamed PVC board and foam-core pipe applications represent the fastest-growing product type within the acrylic processing aid market, driven by construction sector adoption of foam PVC trim board, window lineals, and door components in North American residential construction as a rot-resistant, paintable alternative to wood at comparable installed cost. Foam PVC board requires a foam control processing aid at 2.0 to 4.0 parts per hundred resin to regulate cell nucleation and cell size during the Celuka or free-foam extrusion process, ensuring uniform cell structure and surface density that determines the mechanical performance and paintability of the finished trim board product. AZEK Building Products and CPG International (Versatex) are the primary North American foam PVC trim board producers, each consuming above-plan acrylic processing aid volumes in 2025 on housing construction recovery at above historical average single-family home starts confirmed by the US Census Bureau at approximately 1.04 million single-family housing starts in 2024. For instance, in Q2 2025, Dow Chemical, United States, confirmed at its performance materials investor briefing that its Paraloid K-175 and K-400 acrylic processing aid product lines had achieved above-plan volume growth in Q1 and Q2 2025 driven by North American PVC pipe and foam board application demand, and disclosed that it was evaluating production capacity expansion at its Deer Park, Texas acrylic additives manufacturing facility to address growing North American demand. These are some of the key factors driving revenue growth of the market.

However, methyl methacrylate monomer, the primary comonomer in acrylic processing aid polymer synthesis at 70% to 90% of the copolymer backbone, is produced from acetone cyanohydrin or propylene oxidation routes at BASF Ludwigshafen, Mitsubishi Chemical Yokkaichi, and Evonik Worms, with propylene feedstock costs elevated by the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 adding approximately USD 60 to USD 100 per metric tonne to European MMA production cost above the 2024 baseline. Acrylic processing aids compete with chlorinated polyethylene and acrylate-based impact modifier additives in rigid PVC formulations for construction applications, and price-sensitive PVC pipe compounders in Asia-Pacific markets can partially substitute between processing aid types depending on relative pricing, creating demand elasticity that limits the pricing power of acrylic processing aid producers in commodity PVC pipe applications. These factors substantially limit acrylic processing aid market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

The Infrastructure Investment and Jobs Act enacted in the United States in November 2021 allocated USD 55 billion for water infrastructure investment including lead service line replacement, water main rehabilitation, and wastewater collection system improvement over a five-year programme. The EPA confirmed in its 2024 Drinking Water Infrastructure Needs Survey that approximately 1.2 million miles of US water distribution and transmission pipe would require replacement or rehabilitation over the next 20 years, with PVC pipe specified as the preferred replacement material at above 70% of US water authority pipe procurement programmes due to its corrosion resistance, hydraulic performance, and 50-year service life rating under AWWA C900 and C905 standards. Each mile of 8-inch diameter AWWA C900 PVC distribution pipe weighing approximately 4,500 kilograms requires approximately 45 to 90 kilograms of acrylic processing aid at formulation loadings of 1.0 to 2.0 parts per hundred resin, creating a direct mandatory demand linkage between US water main replacement programme activity and acrylic processing aid consumption at North American PVC pipe compounders. The US Census Bureau confirmed approximately 1.04 million single-family housing starts in 2024, each requiring an average of 200 to 350 linear metres of PVC water, drain, waste, and vent pipe, generating residential construction PVC pipe demand that compounds the infrastructure rehabilitation channel. Southeast Asian housing construction at above-GDP growth rates in Vietnam, Indonesia, the Philippines, and India is generating above-trend PVC pipe and fittings demand for residential and municipal water supply systems at city and provincial government infrastructure programmes. Vietnam's Ministry of Construction confirmed in its 2024 infrastructure investment report that PVC pipe procurement for the national safe water access programme had grown approximately 14% in 2024, with acrylic processing aid demand from Vietnamese PVC pipe compounders growing commensurately at Kaneka and Dow distribution channel growth rates confirmed through Nexchem Intelligence primary research. India's Jal Jeevan Mission programme targeting tap water connections to all rural households by 2024 has generated above-plan UPVC pipe procurement at Finolex Industries, Astral Pipes, and Prince Pipes, with the Bureau of Indian Standards IS 4985 UPVC pipe specification requiring processing aid incorporation at domestic pipe compounders through the compound formulation requirements embedded in IS 4985 certification. Foam PVC Board Construction Adoption Driving Above-Plan Processing Aid Loading Demand Foam PVC trim board and cladding in North American residential construction is growing at above-market rates as contractors and homeowners substitute foam PVC for wood fascia boards, window surrounds, and exterior trim components to eliminate painting frequency, rot replacement costs, and moisture damage repair programmes. AZEK Building Products disclosed in its fiscal 2025 annual report that its residential segment, which includes foam PVC trim and moulding products, had grown revenue approximately 11% in fiscal 2025 on above-plan single-family construction recovery and repair-remodel market adoption, confirming that foam PVC board acrylic processing aid consumption is growing at a rate above the overall construction market growth rate. Foam PVC board requires acrylic processing aid at 2.0 to 4.0 parts per hundred resin compared to 0.5 to 1.5 parts for solid PVC pipe, creating a consumption intensity per kilogram of PVC processed that is approximately two to four times higher than pipe applications and generating a disproportionate revenue contribution to the acrylic processing aid market from a smaller absolute volume of host polymer.

Methyl methacrylate is the dominant monomer in acrylic processing aid polymer synthesis, accounting for 70% to 90% of copolymer backbone composition in high-molecular-weight processing aid grades. MMA production at BASF Ludwigshafen and Evonik Worms in Europe uses propylene as the primary carbon feedstock through C4 oxidation or propylene ammoxidation routes, with European propylene costs elevated approximately 9% to 12% above the 2024 baseline from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through GCC propylene export restriction and European cracker naphtha cost elevation. Mitsubishi Chemical at Yokkaichi, Japan produces MMA through the acetone cyanohydrin ACH route using acetone from cumene process petrochemical feedstocks, with partially different but similarly elevated feedstock economics from GCC petrochemical supply disruption. Asian PVC pipe compounders in China, Vietnam, and India using acrylic processing aids from domestic Chinese APA producers including Shanghai Ruizheng Chemical and Shandong Dongda can source at domestic Chinese MMA prices partially insulated from European and Japanese MMA feedstock cost elevation, creating a cost-of-supply differential that limits European and Japanese APA producers in price-sensitive Asian commodity pipe markets. These factors substantially limit acrylic processing aid market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Type | Foam Control APA, Melt Strength and Fusion Aid, Surface Quality Enhancement Aid, Impact Modifier Processing Aid, Lubricant Processing Aid | Foam Control APA |

| Application | PVC Pipe and Fittings, PVC Profiles and Siding, PVC Film and Sheet, Foam PVC Board, Rigid PVC Packaging | PVC Pipe and Fittings |

| End Use | Construction, Packaging, Automotive, Electrical and Electronics, Consumer Goods | Construction |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Melt Strength and Fusion Aid segment is expected to account for a significantly large revenue share in the global acrylic processing aid market during the forecast period.

This report evaluates type across Foam Control APA, Melt Strength and Fusion Aid, Surface Quality Enhancement Aid, Impact Modifier Processing Aid, Lubricant Processing Aid for additives & masterbatch, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across PVC Pipe and Fittings, PVC Profiles and Siding, PVC Film and Sheet, Foam PVC Board, Rigid PVC Packaging for additives & masterbatch, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Construction, Packaging, Automotive, Electrical and Electronics, Consumer Goods for additives & masterbatch, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for additives & masterbatch, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

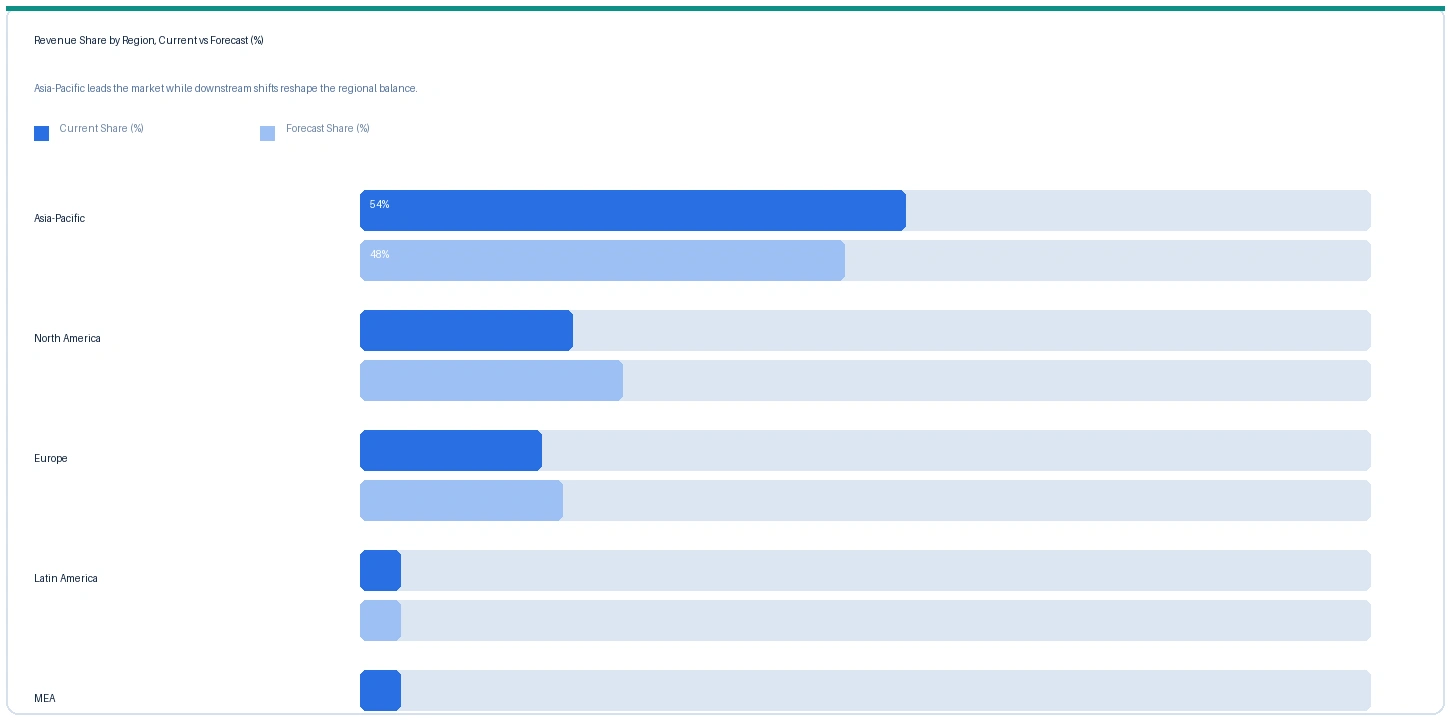

Asia-Pacific market accounted for largest revenue share over other regional markets in the global acrylic processing aid market in 2025. Based on regional analysis, the acrylic processing aid market in Asia-Pacific accounted for largest revenue share in 2025. China is the world's largest PVC consumer and the dominant acrylic processing aid demand market, with PVC pipe and fittings production at Lesso Group, China Lesso Holdings, and Rifeng Enterprise generating acrylic processing aid procurement from Kaneka Japan distribution, Dow Paraloid Asia, and domestic Chinese APA producers including Shanghai Ruizheng Chemical and Shandong Dongda New Materials at combined volumes above 65,000 metric tonnes per year per Nexchem Intelligence primary research. China National Building Material Group confirmed in its 2024 annual report that PVC construction materials procurement had grown approximately 8% in 2024 on infrastructure and residential construction programme activity, confirming the upstream APA demand signal. India's Jal Jeevan Mission rural water access programme and urban piped water expansion at Finolex Industries, Astral Pipes, and Supreme Industries are generating above-plan UPVC pipe demand that translates directly to acrylic processing aid procurement growth at Indian pipe compounders sourcing from Kaneka and Dow regional distribution networks. Vietnam, Indonesia, and the Philippines are generating incremental APA demand from housing construction and municipal water infrastructure investment at government programme spending above 4% of GDP in each country.

The market in North America is expected to register the second largest revenue share, anchored in the Infrastructure Investment and Jobs Act USD 55 billion water infrastructure programme driving above-plan PVC pipe demand at JM Eagle, National Pipe and Plastics, and Georg Fischer Piping Systems North American production facilities. The US Census Bureau-confirmed 1.04 million single-family housing starts in 2024 and above-plan AZEK foam PVC board revenue growth of 11% in fiscal 2025 confirm that both infrastructure and construction application channels are drawing APA demand growth simultaneously. Dow Chemical Deer Park, Texas supplies the majority of North American commercial acrylic processing aid demand through its Paraloid K-series product line, with the Q2 2025 capacity expansion evaluation confirming that North American demand growth is absorbing existing Deer Park output at above-plan rates. Kaneka North American distribution supplements Dow supply for specialty processing aid grades at foam board and rigid profile extrusion applications.

The market in Europe is expected to register steady above-GDP revenue growth driven by PVC window and door profile production growth under the EU Renovation Wave directive, PVC pipe demand from European district heating pipe rehabilitation and water main replacement programmes in Germany, France, and the Netherlands, and foam PVC board adoption in Western European cladding and facade renovation applications. Arkema at its Lacq, France specialty polymers facility and Dow Chemical Terneuzen supply the majority of European specification-grade APA demand, with European MMA feedstock cost elevation from the Strait of Hormuz disruption confirmed by the IMF in March 2026 contributing to above-2024 APA pricing in European markets. The EU Renovation Wave directive target of renovating 35 million buildings by 2030 implies above 3 million PVC window and door frame replacements per year in Germany, Poland, and Austria alone at current market penetration rates, generating sustained demand for PVC profile processing aids at German and Polish profile extrusion facilities.

The market in Latin America is anchored in Brazil and Mexico, where housing construction programmes, water infrastructure investment, and PVC pipe demand from Tigre S.A. and Amanco Wavin at Brazilian manufacturing facilities generate acrylic processing aid procurement from Dow and Kaneka Latin American distribution channels. Brazil's government housing programme Minha Casa Minha Vida expansion target of 2 million new housing units between 2023 and 2026 is generating sustained PVC pipe and fittings demand at Tigre Sao Paulo and Amanco Curitiba manufacturing facilities that translates to above-plan APA demand at Brazilian PVC compounders.

The market in Middle East and Africa is anchored in Saudi Arabia, UAE, and South Africa, where PVC pipe demand from desalination water distribution network expansion, urban housing construction at NEOM and Saudi Vision 2030 residential projects, and South African municipal water rehabilitation generates acrylic processing aid procurement from Dow and Kaneka Middle East distribution. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated MMA and specialty acrylic monomer feedstock logistics costs for GCC-based PVC compound formulators sourcing APA from European and Japanese producers, adding approximately USD 40 to USD 80 per metric tonne to delivered APA cost at GCC compounders relative to pre-disruption logistics baselines. Saudi Vision 2030 residential construction programme targets of 70% home ownership by 2030 are generating multi-year PVC pipe and profile demand that sustains above-plan APA procurement at Saudi compound formulators supplying SABIC and TASNEE PVC resin customers.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| APA Melt Fusion Grade (pipe spec) | Europe | USD 3,840/MT | USD 3,520/MT | Rising | Dow Paraloid K ref |

| APA Melt Fusion Grade (pipe spec) | Asia-Pacific | USD 3,140/MT | USD 2,980/MT | Rising | Kaneka / Dow Asia |

| APA Foam Control Grade (board) | North America | USD 4,620/MT | USD 4,180/MT | Rising | AZEK / CPG ref |

| APA Surface Quality Grade (profile) | Europe | USD 4,080/MT | USD 3,740/MT | Rising | Arkema / Dow ref |

| MMA Monomer (feedstock) | Europe | USD 2,040/MT | USD 1,860/MT | Rising | BASF / Evonik ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and PVC additive trade publication monitoring. Acrylic processing aid prices vary by grade, molecular weight, MMA content, application certification, and supply agreement structure.

European pipe-specification APA melt fusion grade rose approximately 9.1% from USD 3,520 per metric tonne in Q2 2025 to USD 3,840 per metric tonne in Q2 2026, driven by MMA monomer feedstock cost elevation of approximately 9.7% from USD 1,860 per metric tonne to USD 2,040 per metric tonne at BASF Ludwigshafen and Evonik Worms from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, and by above-plan North American and Asian infrastructure rehabilitation demand tightening available European APA supply. Asia-Pacific pipe-specification APA rose approximately 5.4% to USD 3,140 per metric tonne on Kaneka Japan distribution and Dow Asia Pacific pricing, a smaller increase than European grades reflecting partial insulation of Asian MMA producers from GCC propylene disruption through Japanese ACH-route and Chinese domestic petrochemical supply. North American foam control APA rose approximately 10.5% to USD 4,620 per metric tonne on AZEK-confirmed above-plan foam PVC board demand and Dow Deer Park capacity evaluation confirming demand has reached available production output, with the foam control premium above standard pipe-grade APA reflecting the higher molecular weight, tighter cell size regulation, and foam extrusion process optimisation embedded in commercial foam control grades. European surface quality profile-grade APA rose approximately 9.1% to USD 4,080 per metric tonne on EU Renovation Wave window profile production demand and European MMA feedstock cost transmission.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the acrylic processing aid market, the Hormuz disruption affects production economics primarily through methyl methacrylate monomer feedstock costs at European and Japanese APA producers. European MMA production at BASF Ludwigshafen uses propylene as the primary feedstock through propylene oxidation and esterification chemistry, with European propylene costs elevated approximately 9% to 12% above the 2024 baseline from GCC propylene export disruption, adding approximately USD 160 to USD 320 per metric tonne to European APA production cost at current monomer-to-polymer conversion economics. Evonik Industries Worms and Mitsubishi Chemical Yokkaichi produce MMA through acetone cyanohydrin and propylene-based routes respectively, with both facing elevated feedstock economics from Hormuz disruption through GCC crude oil and naphtha pricing transmission. Chinese domestic MMA producers at Shandong and Jiangsu facilities are partially insulated through domestic coal-to-acetone and propylene supply chains, sustaining an approximately USD 700 per metric tonne cost advantage in Chinese-origin APA versus European-origin grades for commodity pipe applications in Asian markets, a differential that has widened from approximately USD 520 per metric tonne in Q2 2025 before the full Hormuz cost transmission. GCC PVC compounders sourcing European or Japanese APA for SABIC and TASNEE PVC resin processing face elevated freight premiums of approximately USD 40 to USD 80 per metric tonne above pre-disruption logistics baselines from the Suez Canal and Indian Ocean routing disruptions affecting European-to-GCC specialty chemical logistics.

Company Insights

The two key dominant companies in the acrylic processing aid market are Dow Chemical and Kaneka Corporation, recognised for their leadership in specification-grade melt strength and foam control APA for AWWA, ASTM, and ISO rigid PVC pipe and profile applications respectively, their established pipe extruder and compound formulator supply relationships, and their contrasting positions as the leading North American and European specification APA producer and the leading Asia-Pacific APA producer in the global market.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 1.84 Billion |

| Market Size 2032 | USD 3.12 Billion |

| CAGR | 8.7% |

| Units | Revenue in USD Billion |

| Segments Covered | By Type, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Poland, Austria, Netherlands, China, Japan, South Korea, India, Vietnam, Brazil, Mexico, Saudi Arabia, UAE |

| Companies Profiled | Dow Chemical, Kaneka Corporation, Arkema, Mitsubishi Chemical, LG Chem, Shandong Dongda, Shanghai Ruizheng, Sundow Polymers, Evonik Industries, Wacker Chemie |

| Key Data Sources | Dow Chemical Q2 2025 performance materials investor briefing, Kaneka Corporation 2025 annual report, AZEK Building Products fiscal 2025 annual report, EPA 2024 Drinking Water Infrastructure Needs Survey, US Census Bureau 2024 housing starts data, Lesso Group 2024 interim results, Arkema specialty materials investor day Q3 2025, BASF Q1 2025 MMA pricing commentary, Infrastructure Investment and Jobs Act water infrastructure allocation data, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 248 |

| Published | Q2 2026 |

| SKU | NXC-SC-003 |

Scope & Methodology

Nexchem Intelligence primary research for this report comprised 15 expert interviews conducted between January and May 2026. Interview panels were structured across a 2x2 supply-side and demand-side grid with explicit geographic and role split. Supply-side contacts included APA production and commercial managers at Dow Chemical Deer Park and Kaneka Takasago, specialty polymer additive product leads at Arkema and Evonik, and MMA monomer market commercial contacts at BASF and Mitsubishi Chemical. Demand-side contacts included PVC pipe compound formulation and procurement managers at North American AWWA-certified pipe extruders, foam PVC board production and raw material procurement leads at North American trim board manufacturers, and European PVC window profile extrusion procurement managers at German and Polish profile producers. Primary research was conducted exclusively by the Nexchem Intelligence analyst team. No expert network firms conducted fieldwork or provided data for this report.

Secondary research sources include Dow Chemical Q2 2025 performance materials investor briefing, Kaneka Corporation 2024 annual report, AZEK Building Products fiscal 2025 annual report, EPA 2024 Drinking Water Infrastructure Needs Survey, US Census Bureau 2024 single-family housing starts data, Lesso Group 2024 interim results, Arkema specialty materials investor day Q3 2025, BASF Q1 2025 MMA performance chemicals pricing commentary, Infrastructure Investment and Jobs Act water infrastructure programme allocation data, and the IMF March 2026 statement on Strait of Hormuz disruption. No figures from syndicated market research publishers have been used as source data in this report.