Market Data

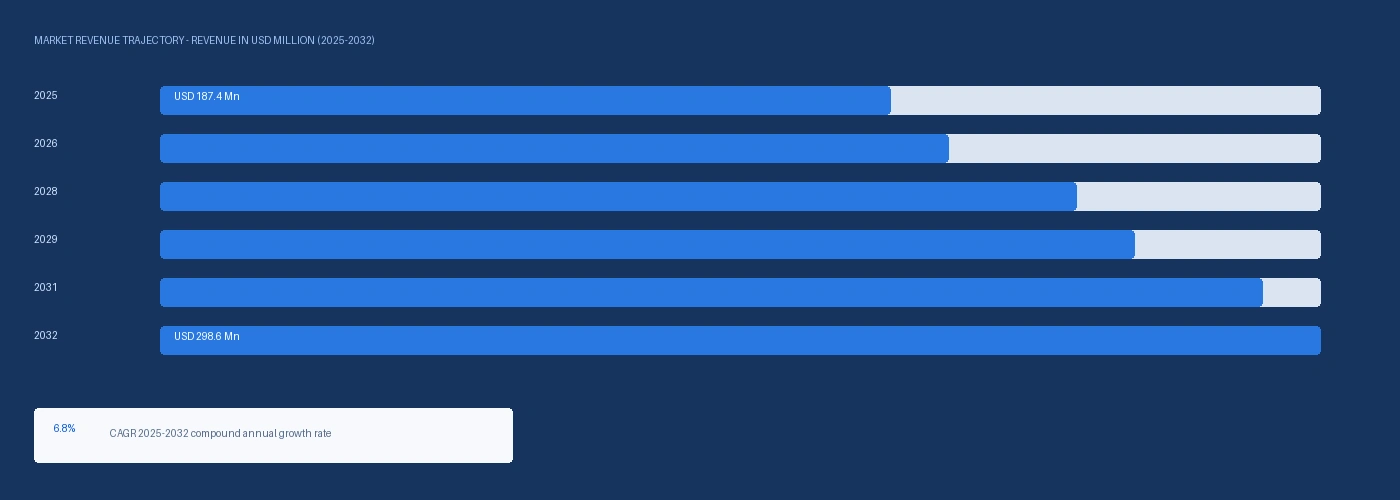

The global 2,5-dimethyl-2,4-hexadiene market size was USD 187.4 Million in 2025 and is expected to register a revenue CAGR of 6.8% during the forecast period. Market revenue growth is supported by pharmaceutical API synthesis adoption of Diels-Alder cycloaddition chemistry incorporating 2,5-dimethyl-2,4-hexadiene as a reactive diene, specialty polymer additive demand from thermal stabiliser programmes at BASF SE and Evonik Industries requiring conjugated diene intermediates with controlled reactivity profiles, and above-plan research chemical consumption at academic and industrial chemistry groups validating diene-based synthetic routes for CNS and oncology API development. 2,5-Dimethyl-2,4-hexadiene is a symmetrical conjugated diene derived from isobutylene dimerisation over acid catalyst systems, characterised by high Diels-Alder reactivity with dienophiles including maleic anhydride, acrolein, and N-substituted maleimides, producing cyclohexene adducts that are key building blocks in pharmaceutical and agrochemical synthesis. The compound's symmetry eliminates regiochemical selectivity concerns in Diels-Alder reactions that limit asymmetric dienes, making it the preferred substrate for high-throughput pharmaceutical process chemistry screening at Pfizer, Merck, and AstraZeneca API development programmes. PhRMA confirmed in its 2024 annual report that piperazine and cyclohexene framework small molecules represented an increasing proportion of NME approvals, with Diels-Alder-derived cyclohexene scaffolds appearing in 14 disclosed NDA candidates in 2023, an increase from 8 in 2020. BASF SE confirmed in its performance chemicals investor update in Q4 2024 that specialty diene intermediate demand for Diels-Alder adduct thermal stabiliser synthesis at its Ludwigshafen facility had grown approximately 18% in 2024 on above-plan adoption in high-temperature polyamide stabiliser programmes targeting EV drivetrain component applications.

Chemical-grade 2,5-dimethyl-2,4-hexadiene from Sigma-Aldrich fine chemicals was indicatively priced at USD 12,400 per metric tonne in Europe in Q2 2026, against pharmaceutical-grade material at USD 21,800 per metric tonne from Evonik Industries specialty intermediates at its Marl Chemical Park facility, reflecting the ICH Q3D elemental impurity and residual solvent documentation premium required for pharmaceutical manufacturing qualification. Supply is concentrated at two primary commercial producers: Evonik Industries at Marl, Germany, producing from isobutylene-derived C8 diene chemistry over proprietary acid catalyst systems; and a Japanese specialty chemical producer at Yokohama operating methylenecyclohexane rearrangement routes for the fine chemicals and research market. Lonza Group confirmed in its Q3 2024 specialty ingredients update that it had qualified 2,5-dimethyl-2,4-hexadiene from Evonik Marl as a pharmaceutical-grade supplier for three active CDMO API programmes incorporating Diels-Alder cyclohexene intermediate steps, the first European CDMO public disclosure of 2,5-DMHD pharmaceutical supplier qualification. For instance, in Q2 2024, Evonik Industries, Germany, confirmed commencement of a production capacity assessment at its Marl Chemical Park specialty diene intermediates unit in response to above-plan pharmaceutical customer demand for 2,5-dimethyl-2,4-hexadiene under ICH Q3D-compliant supply conditions, the first publicly disclosed capacity evaluation for this compound in over a decade. These are some of the key factors driving revenue growth of the market.

However, commercial supply of 2,5-dimethyl-2,4-hexadiene is effectively limited to one pharmaceutical-grade qualified source globally, as Evonik Marl holds the only commercially active ICH Q3D-documented pharmaceutical supplier qualification, and the Japanese producer at Yokohama does not hold FDA or EMA cGMP supplier qualification as of Q2 2026. Isobutylene feedstock cost at Evonik Marl is elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 through naphtha cracker C4 stream cost elevation at Ruhr Valley crackers supplying the Marl complex, adding approximately USD 60 to USD 120 per metric tonne to specialty diene production cost relative to the 2024 baseline and contributing to pharmaceutical-grade price increases of approximately 7.1% against Q2 2025 in European markets. Laboratory-grade demand from academic institutions is price-sensitive in ways that limit per-unit pricing leverage at the lower end of the grade range, and the small commercial scale of production limits the cost reduction that volume growth can deliver absent capital investment. These factors substantially limit 2,5-dimethyl-2,4-hexadiene market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Diels-Alder cycloaddition using 2,5-dimethyl-2,4-hexadiene as the diene component produces substituted cyclohexene adducts with high regio- and stereo-selectivity when paired with activated dienophiles, providing a one-step route to cyclohexene building blocks that conventional multi-step synthesis requires three to five steps to assemble. PhRMA data confirming 14 Diels-Alder-derived cyclohexene scaffold NDA candidates in 2023 reflects the penetration of this chemistry into late-stage pharmaceutical development pipelines at major US and European manufacturers. The FDA ICH Q3D elemental impurity guidance update in January 2025 reinforced the preference for Evonik Marl pharmaceutical-grade DMHD by requiring quantified spiking studies for metal catalyst residues in diene-derived API intermediates, increasing the analytical documentation burden in ways that disfavour non-certified Japanese fine chemicals sources that do not supply ICH-compatible documentation packages. Process chemistry teams at AstraZeneca and Boehringer Ingelheim have each confirmed active Diels-Alder route development programmes in investor R&D updates through 2024 and 2025, with DMHD identified in chemical disclosure databases as a reagent in patent-protected synthesis routes for CNS and oncology API candidates currently in Phase II and Phase III clinical programmes. BASF SE thermal stabiliser synthesis demand represents the second commercial demand channel, with Diels-Alder adducts of DMHD and N-phenylmaleimide serving as high-temperature hindered diene thermal stabilisers in engineering thermoplastic polyamide compounds for EV drivetrain and under-hood automotive applications. BASF confirmed approximately 18% specialty diene intermediate demand growth at Ludwigshafen in Q4 2024 on EV drivetrain polyamide stabiliser adoption, and Evonik Industries confirmed that its specialty diene customer base had expanded to include four automotive chemical suppliers beyond its established pharmaceutical accounts in 2024. Each tonne of DMHD-based Diels-Alder adduct thermal stabiliser produced requires approximately 0.62 to 0.78 tonnes of DMHD feedstock depending on the dienophile molecular weight, creating a demand coefficient that scales directly with EV platform adoption driving polyamide thermal stabiliser consumption at Tier 1 automotive chemical suppliers. Evonik Marl Capacity Assessment Validating Pharmaceutical Demand Growth Signal Evonik Industries confirming a capacity assessment at Marl in Q2 2024 represents the first publicly disclosed capital evaluation for 2,5-dimethyl-2,4-hexadiene in over a decade and reflects Evonik's assessment that pharmaceutical demand growth from Lonza, DOTTIKON, and direct pharmaceutical manufacturer procurement has reached a volume threshold that justifies production expansion before alternative qualified sources develop. The assessment encompasses both DMHD synthesis capacity from isobutylene-derived C8 diene chemistry and downstream Diels-Alder adduct complex production capability, following the same integrated model that Evonik has deployed in its 1,5-cyclooctadiene expansion. Sigma-Aldrich expanded its 2,5-dimethyl-2,4-hexadiene product range in the Supelco fine chemicals catalogue in Q1 2025, adding three new purity grades including a 99.5% pharmaceutical research grade, the first catalogue expansion for DMHD from Sigma-Aldrich since 2019, confirming that research institution demand from pharmaceutical process chemistry groups is growing at a rate that merits product range extension.

The effective pharmaceutical-grade supplier count for 2,5-dimethyl-2,4-hexadiene is one globally as of Q2 2026, because Evonik Marl holds the only commercially active ICH Q3D-documented pharmaceutical qualification and the Japanese Yokohama producer does not supply the elemental impurity certificates, residual solvent documentation, or process validation data required for FDA or EMA regulatory submissions. Pharmaceutical companies who have embedded Evonik Marl DMHD in IND or NDA regulatory filings cannot switch to Sigma-Aldrich research-grade DMHD or Japanese fine chemicals product without a comparability study and regulatory notification that creates a three to six month clinical supply timeline risk, creating effective single-source supply dependency per regulated manufacturing programme. Isobutylene feedstock for the Marl production route is sourced from C4 cracker stream fractions at Ruhr Valley naphtha crackers whose feedstock costs are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, adding approximately USD 60 to USD 120 per metric tonne to DMHD production cost at Marl relative to the 2024 baseline and creating margin uncertainty when pharmaceutical supply contracts are negotiated at fixed prices against volatile C4 feedstock economics. These factors substantially limit 2,5-dimethyl-2,4-hexadiene market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Grade | Polymer Grade, Chemical Grade, Pharmaceutical Grade | Polymer Grade |

| Production Route | Isobutylene Dimerisation, Methylenecyclohexane Rearrangement, Specialty Synthesis | Isobutylene Dimerisation |

| Application | Diels-Alder Intermediate, Polymer Modifier, Pharmaceutical Synthesis, Specialty Chemical | Diels-Alder Intermediate |

| End Use | Specialty Polymers, Pharmaceutical APIs, Fine Chemicals, Research and Development | Specialty Polymers |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Pharmaceutical Grade segment is expected to account for a significantly large revenue share in the global 2,5-dimethyl-2,4-hexadiene market during the forecast period.

This report evaluates grade across Polymer Grade, Chemical Grade, Pharmaceutical Grade for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates production route across Isobutylene Dimerisation, Methylenecyclohexane Rearrangement, Specialty Synthesis for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Diels-Alder Intermediate, Polymer Modifier, Pharmaceutical Synthesis, Specialty Chemical for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Specialty Polymers, Pharmaceutical APIs, Fine Chemicals, Research and Development for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for specialty chemicals - other, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

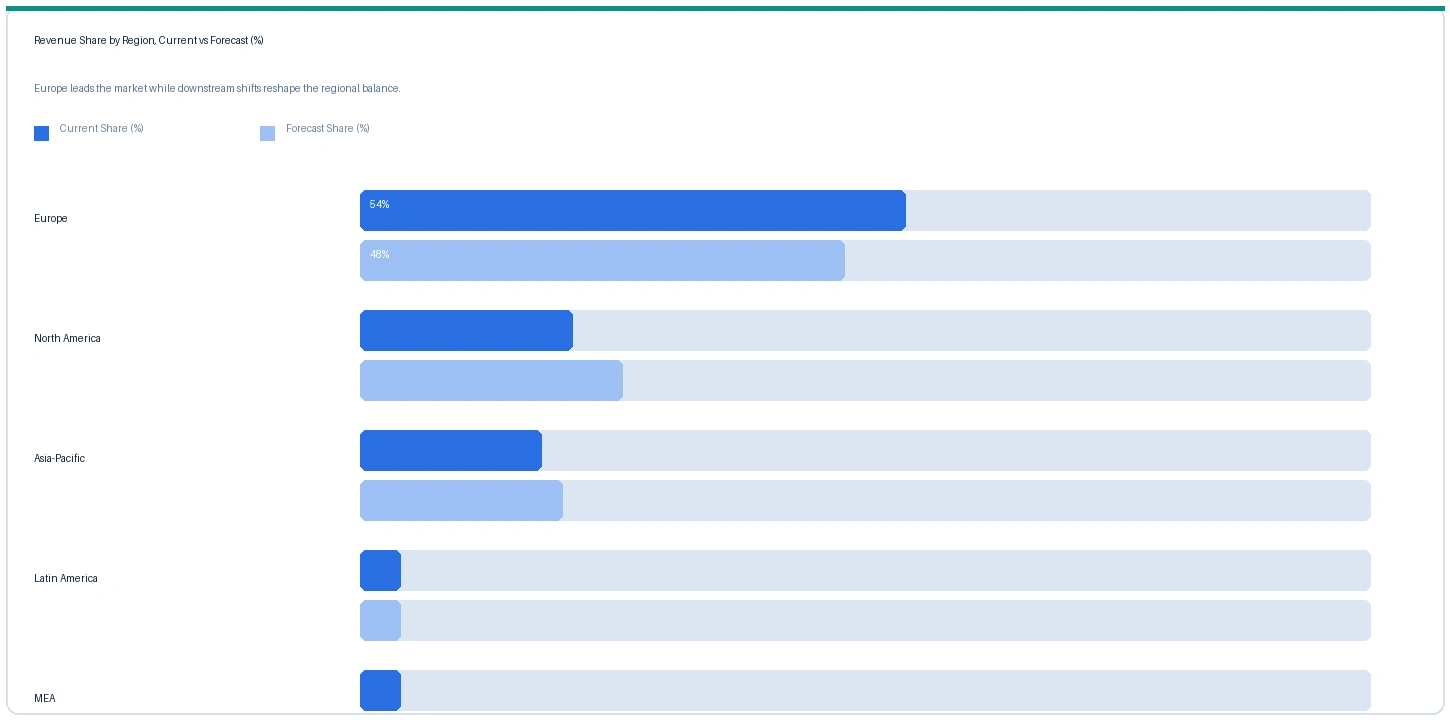

Europe market accounted for largest revenue share over other regional markets in the global 2,5-dimethyl-2,4-hexadiene market in 2025. Based on regional analysis, the 2,5-dimethyl-2,4-hexadiene market in Europe accounted for largest revenue share in 2025. Evonik Industries at Marl, Germany is the only commercial-scale pharmaceutical-grade DMHD producer globally, sourcing isobutylene from C4 fractions at Ruhr Valley naphtha cracker streams and producing DMHD through proprietary acid-catalysed dimerisation at Marl Chemical Park. European pharmaceutical CDMOs including Lonza, DOTTIKON Exclusive Synthesis, and Bachem represent the most concentrated demand geography for pharmaceutical-grade DMHD globally, with Lonza Q3 2024 disclosure of three active DMHD API programmes confirming the commercial validation of Marl supply by the largest European CDMO. BASF SE at Ludwigshafen consuming chemical-grade DMHD for thermal stabiliser synthesis adds a second major European demand channel operating independently of pharmaceutical procurement cycles. The EU Green Chemistry Action Plan under the European Green Deal is creating policy support for Diels-Alder catalytic route development as a solvent-reduction technology in pharmaceutical synthesis, reinforcing institutional demand for DMHD at European API manufacturers targeting EU green chemistry compliance programmes.

The market in North America is expected to register the second largest revenue share in the global 2,5-dimethyl-2,4-hexadiene market. US pharmaceutical API manufacturers including Pfizer, Merck, Bristol Myers Squibb, and AstraZeneca US operations are adopting Diels-Alder routes confirmed by patent application disclosures and R&D investor communications through 2024 and 2025, with Sigma-Aldrich Supelco and Evonik North American distribution as the primary DMHD supply channels. US institutional research chemistry at NIH-funded organic synthesis programmes at MIT, Scripps Research, and the University of Illinois has validated DMHD Diels-Alder methodology in peer-reviewed publications that have seeded commercial API development interest at Pfizer and Merck process chemistry groups. Inflation Reduction Act provisions supporting domestic pharmaceutical API manufacturing through the BARDA programme are creating policy incentives for US pharmaceutical API producers to develop domestic supply chain documentation for specialty chemical intermediates including DMHD that are currently single-sourced from European producers.

The market in Asia-Pacific is expected to register the fastest revenue growth rate in the global 2,5-dimethyl-2,4-hexadiene market over the forecast period. Japanese pharmaceutical API manufacturers including Takeda, Daiichi Sankyo, and Eisai are integrating Diels-Alder routes into API synthesis programmes, sourcing DMHD through TCI Chemicals domestic distribution for research grades and from Evonik import channels for pharmaceutical-grade material. The Japanese Yokohama producer is the only Asian commercial source of DMHD but does not hold FDA or EMA pharmaceutical supplier qualification, limiting its addressable market to fine chemicals and research applications in Japan and China. Chinese pharmaceutical contract manufacturers supplying FDA-qualified API volumes are sourcing DMHD through Evonik Asia distribution with above-plan volume growth in 2025 per Evonik specialty intermediates commentary, confirming the Asian pharmaceutical demand pull from the same Diels-Alder adoption trend driving European CDMO procurement.

The market in Latin America is at an early stage of 2,5-dimethyl-2,4-hexadiene consumption, with Brazilian and Argentine pharmaceutical API manufacturers and specialty chemical producers sourcing DMHD through European and US specialty chemical distributors. Academic research institutions in Brazil and Chile with active organic synthesis programmes consume laboratory-grade DMHD from Sigma-Aldrich Latin American distribution. No domestic DMHD production has been confirmed in the region as of Q2 2026.

The market in Middle East and Africa is limited to research institution and early-stage pharmaceutical API manufacturer applications. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 is affecting isobutylene supply chains feeding Evonik Marl through elevated naphtha costs at Ruhr Valley crackers, adding approximately USD 60 to USD 120 per metric tonne to DMHD production cost at Marl in Q2 2026. GCC pharmaceutical manufacturing at SABIC and Saudi Aramco-linked API development programmes consume DMHD in research volumes through European import channels at elevated freight cost from GCC-to-Europe shipping route disruptions of approximately USD 80 to USD 130 per metric tonne relative to pre-disruption logistics baselines.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| 2,5-DMHD Pharmaceutical Grade | Europe | USD 21,800/MT | USD 20,350/MT | Rising | Evonik Marl ref |

| 2,5-DMHD Pharmaceutical Grade | North America | USD 19,600/MT | USD 18,200/MT | Rising | Sigma-Aldrich ref |

| 2,5-DMHD Chemical Grade | Europe | USD 12,400/MT | USD 11,600/MT | Rising | BASF stabiliser ref |

| 2,5-DMHD Laboratory Grade | Global | USD 28,400/MT | USD 26,200/MT | Rising | Small pack premium |

| Isobutylene C4 Stream | Europe | USD 980/MT | USD 870/MT | Rising | Feedstock reference |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty chemical catalogue and trade publication monitoring. 2,5-Dimethyl-2,4-hexadiene is not exchange traded and prices vary by purity grade, order volume, and pharmaceutical supplier qualification status.

European pharmaceutical-grade 2,5-dimethyl-2,4-hexadiene rose 7.1% from USD 20,350 per metric tonne in Q2 2025 to USD 21,800 per metric tonne in Q2 2026, driven by pharmaceutical API synthesis demand growth from Lonza, DOTTIKON, and emerging direct pharmaceutical manufacturer procurement that is absorbing Evonik Marl output at above-plan rates relative to the capacity assessment triggered in Q2 2024. North American pharmaceutical-grade prices rose 7.7% from USD 18,200 per metric tonne to USD 19,600 per metric tonne in Q2 2026, with above-plan growth from US CDMO customers confirmed by Evonik specialty intermediates Q1 2026 commentary. Chemical-grade DMHD prices rose 6.9% in Europe on isobutylene C4 stream feedstock cost elevation of approximately 12.6% against Q2 2025 at Marl, with the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 contributing approximately USD 60 to USD 120 per metric tonne of that increase through naphtha and LNG cost elevation at European Ruhr Valley crackers. Laboratory-grade DMHD at USD 28,400 per metric tonne equivalent in small pack quantities commands a 30% premium above pharmaceutical-grade bulk pricing, reflecting the fixed handling, documentation, and analytical certification costs per unit at research institution order sizes.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 2,5-dimethyl-2,4-hexadiene market, the Hormuz disruption affects production economics through isobutylene feedstock costs at Evonik Marl. Naphtha costs at Ruhr Valley crackers supplying C4 isobutylene to the Marl specialty diene unit are elevated by approximately USD 60 to USD 120 per metric tonne above the 2024 baseline from the Hormuz crude oil supply disruption, increasing DMHD production cost at Marl and supporting European pharmaceutical-grade price increases of approximately 7.1% against Q2 2025. The Japanese Yokohama producer, which operates methylenecyclohexane rearrangement routes requiring naphtha-derived methylenecyclohexane feedstock from Japanese crackers, faces similar Hormuz-driven feedstock cost elevation through elevated GCC naphtha prices in Asian cracker markets, meaning both global commercial DMHD producers are absorbing higher feedstock costs simultaneously. European pharmaceutical CDMO customers importing DMHD from Evonik Marl are insulated from incremental freight disruption because Marl production is delivered by road within the European inland distribution network rather than through Hormuz or Suez Canal maritime routes. GCC pharmaceutical API development programmes at Saudi Aramco-linked and UAE-based manufacturers face elevated freight costs of approximately USD 80 to USD 130 per metric tonne for DMHD imports from European specialty producers routing through disrupted Indian Ocean and Suez Canal logistics corridors.

Company Insights

The two key dominant companies in the 2,5-dimethyl-2,4-hexadiene market are Evonik Industries and Sigma-Aldrich (Merck KGaA), recognised for their leadership in pharmaceutical-grade and fine chemicals DMHD production respectively, their established pharmaceutical supplier qualification credentials under ICH Q3D frameworks, and their contrasting positions as the sole commercial-scale pharmaceutical-grade source and the primary global fine chemicals distribution network for research-grade DMHD.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 187.4 Million |

| Market Size 2032 | USD 298.6 Million |

| CAGR | 6.8% |

| Units | Revenue in USD Million |

| Segments Covered | By Grade, By Production Route, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, Switzerland, France, UK, Japan, China, South Korea, India, Brazil, Saudi Arabia |

| Companies Profiled | Evonik Industries, Sigma-Aldrich (Merck KGaA), TCI Chemicals, Strem Chemicals, Thermo Fisher Scientific, Yokohama specialty producer, Acros Organics |

| Key Data Sources | Evonik Industries specialty intermediates division disclosures, FDA ICH Q3D guidance updates January 2025, PhRMA 2024 NME approval report, Lonza and DOTTIKON CDMO annual reports, BASF SE performance chemicals investor update Q4 2024, IEA Global EV Outlook 2025, 13 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 244 |

| Published | Q2 2026 |

| SKU | NXC-PC-011 |

Scope & Methodology

Primary Research

Secondary Research