Market Data

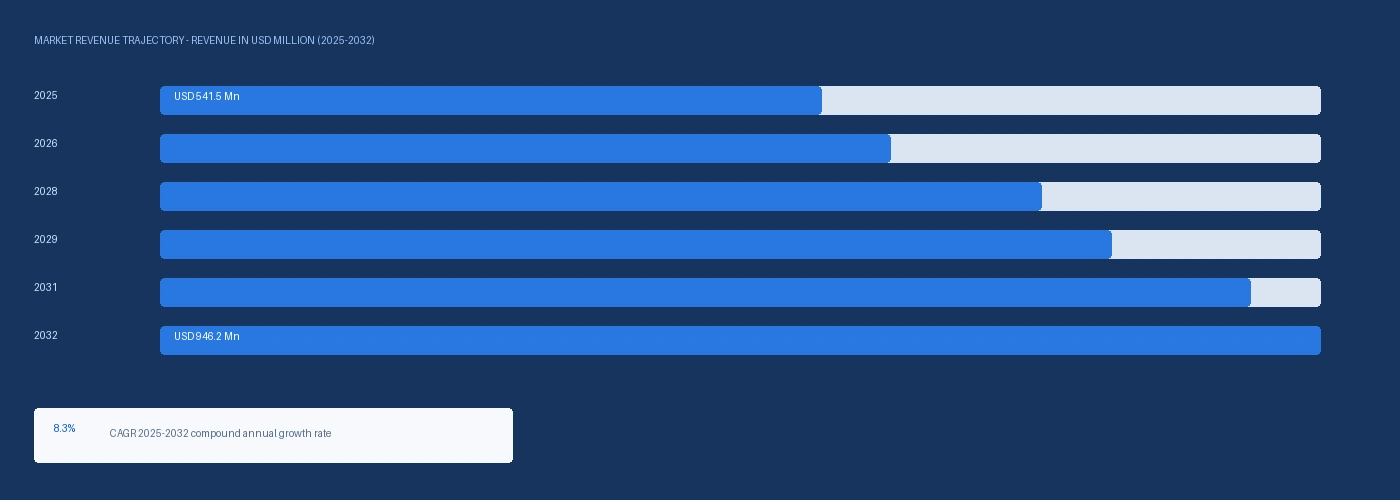

The global 1,3 propanediol market size was USD 541.5 Million in 2025 and is expected to register a revenue CAGR of 8.3% during the forecast period. Market revenue growth is supported by expanding demand for polytrimethylene terephthalate fibre in automotive interior textiles and premium carpet, expanding bio-based PDO adoption in certified natural cosmetics formulations, and growing Ecocert Cosmos and USDA BioPreferred programme requirements that are converting voluntary sustainability preferences into binding procurement specifications across European and North American consumer goods supply chains. DuPont Tate and Lyle Bio Products operates the only commercial-scale bio-based PDO fermentation facility globally at Loudon, Tennessee, producing approximately 65,000 metric tonnes per year under the Zemea personal care and Susterra industrial brands, with the facility reporting a record annual production volume in 2025 driven by above-plan demand from both PTT fibre and personal care applications. PTT fibre spinning capacity expanded in Asia-Pacific through 2024, with the Taiwan Textile Federation confirming approximately 12% growth in PTT capacity at Taiwanese producers including Far Eastern New Century and Shinkong Synthetic Fibre, translating to an incremental PDO demand pull of approximately 7,000 to 9,000 metric tonnes per year from Taiwan alone based on a PTT fibre PDO content of approximately 330 kilograms per metric tonne of polymer. The Carpet and Rug Institute confirmed PTT fibre at approximately 18% of US premium residential carpet fibre volume in 2024, with Shaw Industries and Mohawk Industries each expanding Sorona-incorporating product lines into commercial tile categories. For instance, in October 2024, DuPont, United States, confirmed the completion of an efficiency upgrade at its Sorona PTT fibre production operations in Shenzhen, China, reducing energy consumption per kilogram of PTT produced by approximately 11% and supporting cost competitiveness of bio-based PDO-derived fibre in the automotive interior and premium carpet segments across Asian markets. These are some of the key factors driving revenue growth of the market.

Bio-based PDO supply at the Loudon, Tennessee facility operated at above-95% utilisation through 2025 per DuPont investor communications, with allocation between Zemea personal care and Susterra industrial grades managed to capture the higher-margin personal care premium. Zemea PDO was indicatively priced at USD 2,840 per metric tonne in North America and USD 3,140 per metric tonne in Europe in Q2 2026, commanding a premium of approximately 2.4 times the propylene glycol USP reference price on a per kilogram basis in European certified natural cosmetics markets. Petroleum-based PDO from SK Chemicals at its Ulsan, South Korea facility and from Shell Chemicals supplies Asian PTT fibre producers who do not require bio-certification, with SK Chemicals disclosing full capacity utilisation at Ulsan through 2024 on supply agreements with Far Eastern New Century and Huvis. WELEDA AG confirmed in its January 2025 ingredient transparency report that bio-based PDO had replaced propylene glycol as the primary humectant across its full COSMOS-certified skin care range, marking the first major European natural cosmetics brand to achieve 100% bio-based PDO conversion across all certified formulations.

However, the supply base for bio-certified PDO is concentrated at a single production facility with no publicly committed backup, creating an allocation risk that intensifies as automotive PTT fibre demand and personal care adoption grow simultaneously. Glucose feedstock cost at the Loudon facility swung between approximately USD 120 and USD 190 per metric tonne of PDO impact across the 2022 to 2025 corn price cycle per USDA Economic Research Service data, creating production cost variability that is difficult to fully hedge in long-term fixed-price Zemea supply contracts. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated US corn production and logistics costs through diesel and agricultural energy price pass-through, maintaining glucose feedstock costs above the 2023 baseline and sustaining upward pressure on Zemea and Susterra pricing into Q2 2026. These factors substantially limit 1,3 propanediol market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

PTT fibre spinning capacity across Taiwan, South Korea, and China expanded through 2024 in response to sportswear brand sourcing commitments targeting reduced elastane content and automotive OEM interior textile specifications favouring bio-attributed materials with documented Scope 3 carbon footprint credentials. Far Eastern New Century commissioned approximately 8,000 metric tonnes per year of new PTT spinning capacity at its Taoyuan facility in Q2 2024 under a Susterra PDO supply agreement with DuPont Tate and Lyle Bio Products, with the fibre targeted at European and North American sportswear brands specifying bio-based content. Each tonne of PTT polymer produced at these new lines consumes approximately 330 kilograms of PDO, translating the capacity expansion directly into a sustained PDO feedstock demand increment. Hyosung TNC in South Korea and Huvis Corporation have each disclosed PTT programme evaluations for 2026 to 2027 capacity additions that would further increase Asian PDO demand if committed. Shaw Industries in the United States expanded its Sorona-incorporating commercial carpet tile product range to cover four additional product families targeting LEED-certified building interiors in March 2025, citing PTT fibre bio-based carbon content as a documented LEED Materials and Resources credit contribution. Automotive OEM interior textile specifications are creating a durable demand anchor for PTT fibre incorporating bio-based PDO. Ford, Toyota, BMW Group, and Honda have each incorporated Sorona PTT in interior textile specifications for select model programmes, with the bio-based carbon content of the fibre documented in Scope 3 Category 1 supplier emissions reporting. BASF SE and Evonik Industries have evaluated PDO as a building block for bio-based polyurethane polyol synthesis for coatings and adhesives, with Evonik Care Solutions confirming interest in PDO-incorporating bio-based polyol programmes for European automotive and construction applications in its 2024 specialty chemicals strategy update. Certified Natural Cosmetics Demand Driving Zemea PDO Volume Growth The personal care application for bio-based PDO is the fastest-expanding end-use segment by revenue value per kilogram, with Zemea commanding USD 2,840 per metric tonne in North America versus propylene glycol USP at USD 1,180 per metric tonne on an equivalent basis. Cosmetics Europe confirmed that bio-derived polyols and humectants were the fastest-expanding ingredient category by volume in certified natural cosmetics across EU markets in its 2024 annual report, with PDO among the top five bio-derived humectants in new product launches. Pai Skincare confirmed in February 2026 that Zemea PDO was specified in 14 of its 18 product formulations, completing a full certified natural range transition driven by consumer demand for transparently sourced bio-derived ingredients. The USDA BioPreferred programme database listed 142 PDO-incorporating consumer product formulations as of Q1 2026, an increase of approximately 38 products from the Q1 2024 listing, confirming the programme-driven demand pull for Loudon facility output across US institutional and consumer markets.

The Loudon, Tennessee facility produces approximately 65,000 metric tonnes per year of bio-based PDO across Zemea and Susterra grades at above-95% utilisation, with no second commercial-scale bio-certified PDO source available globally as of Q2 2026. Any unplanned outage at Loudon creates an immediate allocation situation where DuPont Tate and Lyle Bio Products prioritises longest-term and highest-volume customers, leaving spot and short-term contract buyers without certified supply for the duration of the outage. Pharmaceutical-equivalent ICH Q7 documentation is not required for PDO but Ecocert and USDA BioPreferred qualification audits are supplier-specific, meaning that petroleum-based PDO from SK Chemicals or Shell cannot substitute for Zemea in certified natural cosmetics formulations that have completed a supplier qualification against the Loudon facility. SK Chemicals disclosed in Q3 2024 that it was evaluating bio-based PDO fermentation technology licensing, which would represent the first potential second bio-certified source, but commercialisation timelines of five to seven years from pilot to qualified production mean no relief within the current forecast period. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated corn production, transport, and storage costs in the US Midwest through diesel and agricultural energy cost pass-through, sustaining glucose feedstock costs at the Loudon facility above the 2023 baseline. USDA Economic Research Service data shows US corn prices ranged from USD 4.20 to USD 6.80 per bushel across the 2022 to 2025 period, creating a USD 120 to USD 190 per metric tonne swing in PDO production cost from glucose input alone. Petroleum-based PDO pricing from acrolein hydration is linked to propylene costs, which are also elevated from the Hormuz crude oil supply disruption, meaning both PDO source routes are rising simultaneously without the relative cost gap narrowing to attract new entrants. These factors substantially limit 1,3 propanediol market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Source | Bio-Based PDO, Petroleum-Based PDO | Bio-Based PDO |

| Application | PTT Fibre, Polyurethanes, Cosmetics and Personal Care, Engine Coolants, Unsaturated Polyester Resins | PTT Fibre |

| End Use | Textiles and Apparel, Automotive, Consumer Goods, Industrial | Textiles and Apparel |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Bio-Based PDO segment is expected to account for a significantly large revenue share in the global 1,3 propanediol market during the forecast period.

This report evaluates source across Bio-Based PDO, Petroleum-Based PDO for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across PTT Fibre, Polyurethanes, Cosmetics and Personal Care, Engine Coolants, Unsaturated Polyester Resins for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Textiles and Apparel, Automotive, Consumer Goods, Industrial for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

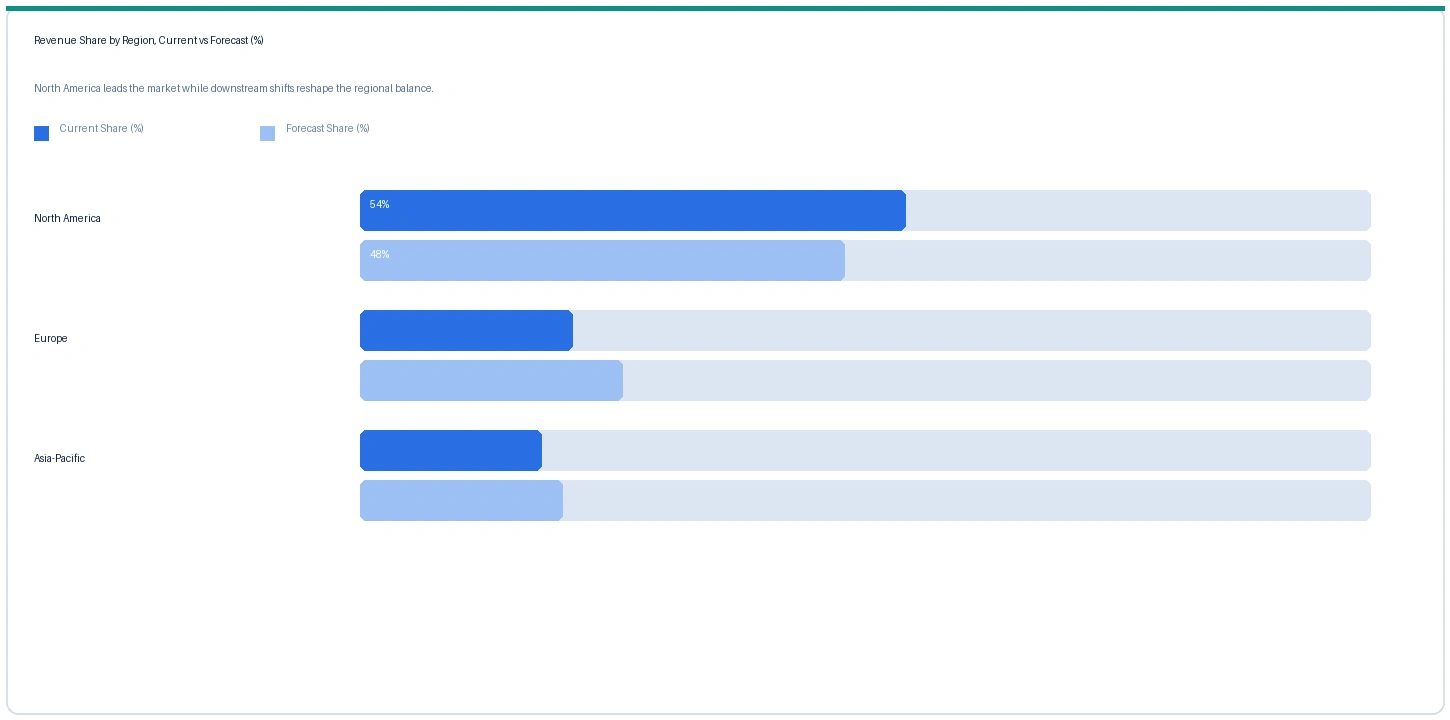

North America market accounted for largest revenue share over other regional markets in the global 1,3 propanediol market in 2025. Based on regional analysis, the 1,3 propanediol market in North America accounted for largest revenue share in 2025. The Loudon, Tennessee production facility is the geographic origin of all commercially available bio-certified PDO globally, making North America the revenue-dominant region by production origin and by a large proportion of end-use consumption through the US carpet industry and US personal care manufacturing. Shaw Industries and Mohawk Industries combined consume an estimated 18,000 to 24,000 metric tonnes per year of PDO through PTT fibre incorporation in premium carpet at US production facilities. The USDA BioPreferred programme listed 142 PDO-incorporating consumer products in its database as of Q1 2026, with federal government procurement preference requirements creating a recurring institutional demand channel that grows with each new product addition.

The market in Europe is expected to register the second largest revenue share in the global 1,3 propanediol market. Ecocert Cosmos certification for Zemea PDO has driven adoption among European certified natural brands including WELEDA, Korres, Pai Skincare, and approximately 340 additional Cosmos-certified personal care brands across Germany, France, and the UK that specify PDO as a primary humectant. The European personal care market consumed an estimated 4,200 to 5,800 metric tonnes per year of Zemea PDO in certified natural formulations in 2024. Automotive interior textile applications in Germany, where Continental, Adient, and Faurecia supply seat fabrics to European OEMs, represent a second demand channel for PTT fibre incorporating bio-based PDO at estimated annual consumption of 2,000 to 3,000 metric tonnes.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global 1,3 propanediol market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period. PTT spinning capacity additions at Far Eastern New Century, Shinkong Synthetic Fibre, and Nan Ya Plastics in Taiwan added an estimated 7,000 to 9,000 metric tonnes per year of incremental PDO demand in 2024 alone, with further capacity expansions at South Korean and Chinese producers under evaluation for 2026 to 2027 commissioning. Chinese personal care contract manufacturers supplying European and North American brands under Ecocert-certified formulation contracts are sourcing Zemea PDO through DuPont Asia distribution, with Chinese Zemea volumes growing at an estimated 15% to 20% per year through 2024 on contract manufacturing expansion.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| Bio-Based PDO (Zemea) | North America | USD 2,840/MT | USD 2,620/MT | Rising | Personal care ref |

| Bio-Based PDO (Susterra) | North America | USD 2,280/MT | USD 2,100/MT | Rising | PTT / industrial |

| Bio-Based PDO (Zemea) | Europe | USD 3,140/MT | USD 2,890/MT | Rising | Ecocert certified |

| Petroleum-Based PDO | Asia-Pacific | USD 1,640/MT | USD 1,520/MT | Rising | SK Chemicals ref |

| Propylene Glycol USP | Global | USD 1,180/MT | USD 1,090/MT | Stable | Conventional benchmark |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and trade publication monitoring. 1,3-Propanediol is not exchange traded. Prices vary by source certification, grade, volume, and contract structure. The propylene glycol row is included as a conventional reference benchmark only.

Zemea and Susterra prices are rising across North America and Europe in Q2 2026, with Zemea personal care grade up approximately 8.4% against Q2 2025 in North America and approximately 8.7% in Europe. The RSPO-equivalent certification premium for bio-based PDO relative to propylene glycol USP has widened from approximately 2.3 times propylene glycol in Q2 2025 to approximately 2.4 times in Q2 2026 in European markets. Glucose feedstock cost elevation from the US-Iran conflict and Strait of Hormuz disruption confirmed by the IMF in March 2026 is sustaining the upward trajectory, with US Midwest corn production and logistics costs approximately 6% to 9% above the 2024 baseline on diesel and agricultural energy cost pass-through. Petroleum-based PDO from SK Chemicals and Shell is rising in parallel on propylene and crude oil cost pressure, narrowing the absolute percentage premium of bio-based over petroleum-based PDO on a per kilogram basis while the absolute per-tonne differential remains above USD 1,000 per metric tonne in North American markets.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 1,3 propanediol market the Hormuz disruption affects production economics through US corn production costs: elevated diesel and agricultural energy costs in the US Midwest from the crude oil supply disruption are increasing corn production, transport, and storage costs at the Loudon, Tennessee glucose feedstock sourcing region, adding an estimated USD 15 to USD 30 per metric tonne to bio-based PDO production cost relative to the 2024 baseline and sustaining the Q2 2026 upward pricing trajectory for Zemea and Susterra. Petroleum-based PDO pricing is rising in parallel on propylene and crude oil input cost pressure from the same Hormuz disruption, meaning both PDO source routes are absorbing feedstock cost increases simultaneously. The conflict environment is reinforcing US domestic bio-manufacturing investment rationale within the USDA BioPreferred programme, providing medium-term policy support for the Loudon facility as a strategically important domestic production asset.

Company Insights

The two key dominant companies in the 1,3 propanediol market are DuPont Tate and Lyle Bio Products and SK Chemicals, recognised for their leadership in bio-based and petroleum-based PDO production respectively, their established supply relationships with PTT fibre producers and personal care manufacturers, and their contrasting market positions as the sole bio-certified global source and the primary Asian petroleum-based alternative.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 541.5 Million |

| Market Size 2032 | USD 946.2 Million |

| CAGR | 8.3% |

| Units | Revenue in USD Million |

| Segments Covered | By Source, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, France, UK, Switzerland, China, Japan, South Korea, Taiwan, India, Brazil |

| Companies Profiled | DuPont Tate and Lyle Bio Products, SK Chemicals, Shell Chemicals, Evonik Industries, Far Eastern New Century, Shinkong Synthetic Fibre, Huvis, Mohawk Industries, Shaw Industries, WELEDA AG |

| Key Data Sources | DuPont investor presentations, USDA BioPreferred programme database, Cosmetics Europe annual report, Taiwan Textile Federation capacity data, Carpet and Rug Institute fibre data, USDA Economic Research Service corn price series, 15 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 264 |

| Published | Q2 2026 |

| SKU | NXC-PC-002 |

Scope & Methodology

Primary Research

Secondary Research