Market Data

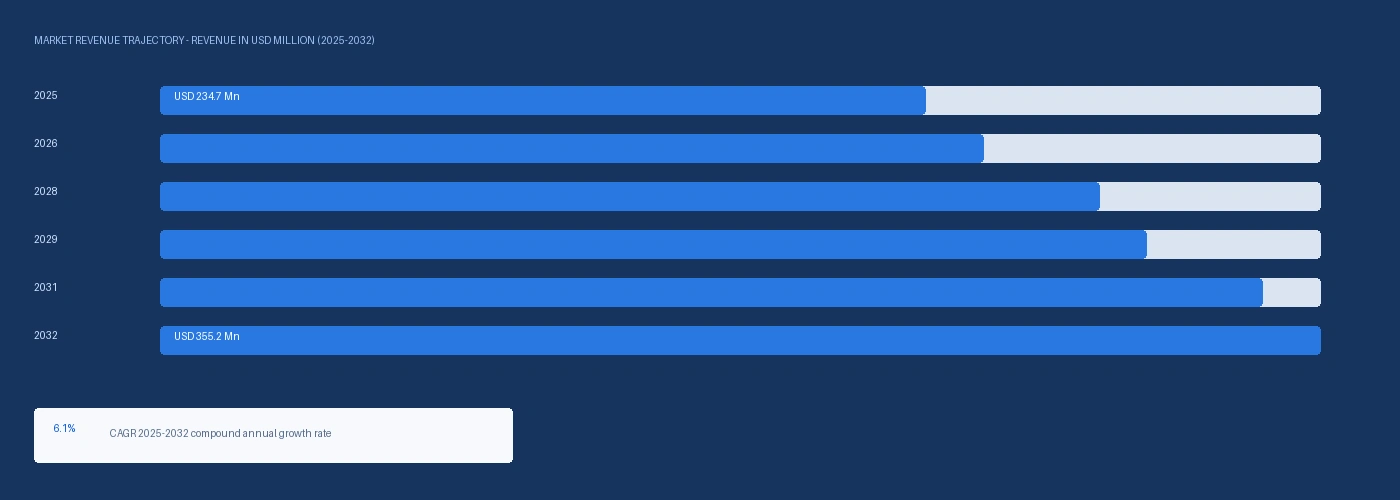

The global 1,5 cyclooctadiene market size was USD 234.7 Million in 2025 and is expected to register a revenue CAGR of 6.1% during the forecast period. Market revenue growth is supported by pharmaceutical API synthesis adoption of nickel(0) and rhodium(I) COD complex precatalysts in cross-coupling and asymmetric hydrogenation reactions, SHOP process industrial catalyst preparation consuming polymer-grade 1,5-COD at Shell Chemicals and Sasol facilities, and growing laboratory and research chemical demand from academic and industrial chemistry groups adopting nickel-catalysed synthesis methodologies validated in pharmaceutical API development pipelines. Pharmaceutical API manufacturers consumed catalyst-grade 1,5-COD at an indicative price of USD 18,400 per metric tonne in Europe in Q2 2026, a 7.6% increase against Q2 2025, reflecting the growing pharmaceutical demand pull from a supply base that has not expanded capacity at equivalent rates. PhRMA disclosed in its 2024 annual report that piperazine-containing small molecules, which frequently require nickel or rhodium catalysed synthesis steps in their API manufacturing routes, represented approximately 34% of NME approvals in 2023, up from approximately 22% in 2018. Evonik Industries confirmed a capacity expansion of 1,5-COD production at its Marl Chemical Park in Q2 2024, the first publicly disclosed European COD capacity expansion since 2018, citing growing pharmaceutical API manufacturer demand for nickel-catalysed cross-coupling precatalysts as the primary rationale. Global 1,5-COD supply is concentrated at approximately three primary commercial producers -- Evonik Industries at Marl, Germany; Sigma-Aldrich (Merck KGaA) through its fine chemicals network; and a small number of Asian specialty producers -- creating a supply structure where any single facility outage can remove a material proportion of global catalyst-grade availability without commercially viable short-term alternatives. For instance, in Q2 2024, Evonik Industries, Germany, confirmed expansion of 1,5-COD production capacity at its Marl Chemical Park facility, adding catalyst-grade COD synthesis capability for pharmaceutical API manufacturers adopting nickel-catalysed cross-coupling routes under FDA and EMA cGMP conditions, the first European COD capacity expansion since 2018. These are some of the key factors driving revenue growth of the market.

Pharmaceutical catalyst-grade 1,5-COD commanded USD 18,400 per metric tonne in Europe and USD 16,800 per metric tonne in North America in Q2 2026 against polymer-grade COD for industrial SHOP catalyst preparation at USD 9,200 per metric tonne in Europe, reflecting the ICH Q3D elemental impurity documentation premium that pharmaceutical manufacturing qualification requires. Lonza Group disclosed in Q3 2024 that it had completed qualification of a new nickel(0) COD-based precatalyst supplier for three active API contract manufacturing programmes, the first European CDMO disclosure of COD-based catalyst supplier diversification as a supply chain security measure. Bristol Myers Squibb disclosed in a JACS peer-reviewed publication in March 2025 that its process chemistry team had developed a scalable Ni(cod)2-catalysed cross-coupling synthesis route for a marketed oncology API, the first publicly disclosed scale-up of a nickel-catalysed step for a commercial pharmaceutical product at a major US pharma manufacturer, representing a demand validation event that has influenced procurement decisions at multiple API manufacturers subsequently. Butadiene feedstock costs at Evonik Marl sourced from Ruhr Valley naphtha cracker C4 streams are elevated from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, adding approximately USD 40 to USD 80 per metric tonne to COD production cost at Marl and supporting Q2 2026 European catalyst-grade price increases.

However, the 1,5-COD market is constrained by the concentration of pharmaceutical-grade supply at effectively one commercially established producer per pharmaceutical customer, as ICH Q3D supplier qualification audits are supplier-specific and pharmaceutical companies who have embedded Evonik Marl COD in IND or NDA regulatory filings cannot switch to Sigma-Aldrich COD without a comparability study and regulatory notification that takes three to six months and risks clinical supply timeline delay. Laboratory and research grade COD demand from academic institutions is price-sensitive in a way that limits per-unit pricing power at the lower end of the grade range, creating a volume segment below the pharmaceutical tier that does not contribute proportionally to revenue. These factors substantially limit 1,5 cyclooctadiene market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Piperazine-containing and biaryl framework small molecule APIs, which represent an increasing proportion of oncology, antiviral, and CNS NME approvals, frequently require nickel(0) or rhodium(I) COD complex precatalysts in cross-coupling, carbonylation, and asymmetric hydrogenation steps. PhRMA confirmed piperazine-containing molecular frameworks in approximately 34% of NME approvals in 2023, up from approximately 22% in 2018, reflecting the structural penetration of catalytic synthesis in pharmaceutical API development pipelines. Ni(cod)2, bis(1,5-cyclooctadiene)nickel(0), is consumed as a precatalyst in these steps at the rate of approximately 0.5% to 5% catalyst loading relative to substrate mass, creating a per-batch 1,5-COD demand that scales directly with API batch sizes entering commercial manufacturing. Bristol Myers Squibb's March 2025 JACS disclosure of a scalable Ni(cod)2 cross-coupling synthesis route for a marketed oncology API validated nickel catalysis at commercial pharmaceutical manufacturing scale and has accelerated adoption evaluations at Pfizer, Merck, and AstraZeneca process chemistry teams per Nexchem Intelligence primary research. The FDA ICH Q3D elemental impurity guidance confirmed in January 2025 updates requires quantified catalyst spiking studies for Ni(cod)2 and Rh(cod) precatalysts in drug products, increasing the analytical documentation burden for COD-based catalyst users and reinforcing the preference for Evonik and Sigma-Aldrich qualified-supplier COD over non-certified Chinese alternatives that cannot supply the required ICH Q3D documentation packages. Industrial demand from the Shell Higher Olefin Process for polymer-grade 1,5-COD in nickel catalyst preparation at Shell Chemicals Geismar, Louisiana and Sasol Sasolburg, South Africa provides a baseline industrial consumption of approximately 2,000 to 3,000 metric tonnes per year at polymer-grade pricing, sustaining a volume floor that supports Evonik Marl production economics independent of pharmaceutical demand cycles. SHOP process utilisation above 80% at Shell and Sasol facilities per investor disclosures sustains this demand baseline and provides Evonik with a reliable secondary demand channel that pharmaceuticals supplement. Evonik Marl Capacity Expansion Validating Long-Term Pharmaceutical Demand Trajectory Evonik Industries' Q2 2024 decision to expand 1,5-COD production capacity at Marl, the first such investment since 2018, represents a capital commitment reflecting Evonik's assessment that pharmaceutical demand growth justifies capacity addition before alternative qualified sources enter the market. The expansion adds both COD synthesis capacity and downstream Ni(cod)2 and Rh(cod) complex production capability, extending Evonik's commercial reach from COD monomer into the catalyst-ready precatalyst product form that pharmaceutical process chemistry teams increasingly specify. Sigma-Aldrich expanded its COD-based catalyst precursor product range in the Supelco fine chemicals catalogue in Q4 2024, adding five new Ni(cod)2 and Rh(I) COD complex products, the largest single catalogue expansion for COD derivatives in the Sigma-Aldrich range since 2016, confirming growing pharmaceutical research institution demand for COD-based catalyst precursor product diversity.

The effective supplier count for pharmaceutical-grade 1,5-COD is one per customer programme, not three, because ICH Q3D supplier qualification audits are supplier-site-specific and regulatory filings embedding Evonik Marl COD in IND and NDA documentation cannot switch to Sigma-Aldrich COD without a comparability study, regulatory notification, and three to six month delay risk to clinical supply timelines. Lonza Q3 2024 disclosure of completing a new COD precatalyst supplier qualification for three API programmes represents procurement best practice that the majority of pharmaceutical buyers have not yet implemented, leaving most pharma COD buyers on single-source supply with no commercially activated alternative. The South Korean specialty chemical producer that announced pilot-scale 1,5-COD production in Q2 2025 represents a potential future third pharmaceutical-grade source but faces an estimated 18 to 24 month supplier qualification timeline before any pharmaceutical customer can use the material in a regulated manufacturing context. Butadiene feedstock cost at Evonik Marl, sourced from Ruhr Valley naphtha cracker C4 streams, is elevated by approximately USD 40 to USD 80 per metric tonne in Q2 2026 relative to 2024 baseline from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026, which has elevated naphtha costs at European crackers supplying the Marl C4 stream and is flowing through to 1,5-COD production cost. This feedstock cost elevation supports Q2 2026 European catalyst-grade COD price increases but is non-hedgeable in long-term fixed-price pharmaceutical supply contracts, creating production margin uncertainty at Evonik Marl when naphtha costs normalise relative to contracted pharmaceutical COD pricing. These factors substantially limit 1,5 cyclooctadiene market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Grade | Polymer Grade, Catalyst Grade, Laboratory Grade | Polymer Grade |

| Application | Ni and Rh Catalyst Synthesis, COD-Based Polymers, Specialty Chemical Intermediate, Pharmaceutical Synthesis | Ni and Rh Catalyst Synthesis |

| End Use | Specialty Catalysis, Fine Chemicals, Polymer Research, Pharmaceutical APIs | Specialty Catalysis |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Catalyst Grade segment is expected to account for a significantly large revenue share in the global 1,5 cyclooctadiene market during the forecast period.

This report evaluates grade across Polymer Grade, Catalyst Grade, Laboratory Grade for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Ni and Rh Catalyst Synthesis, COD-Based Polymers, Specialty Chemical Intermediate, Pharmaceutical Synthesis for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Specialty Catalysis, Fine Chemicals, Polymer Research, Pharmaceutical APIs for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for olefins & glycols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

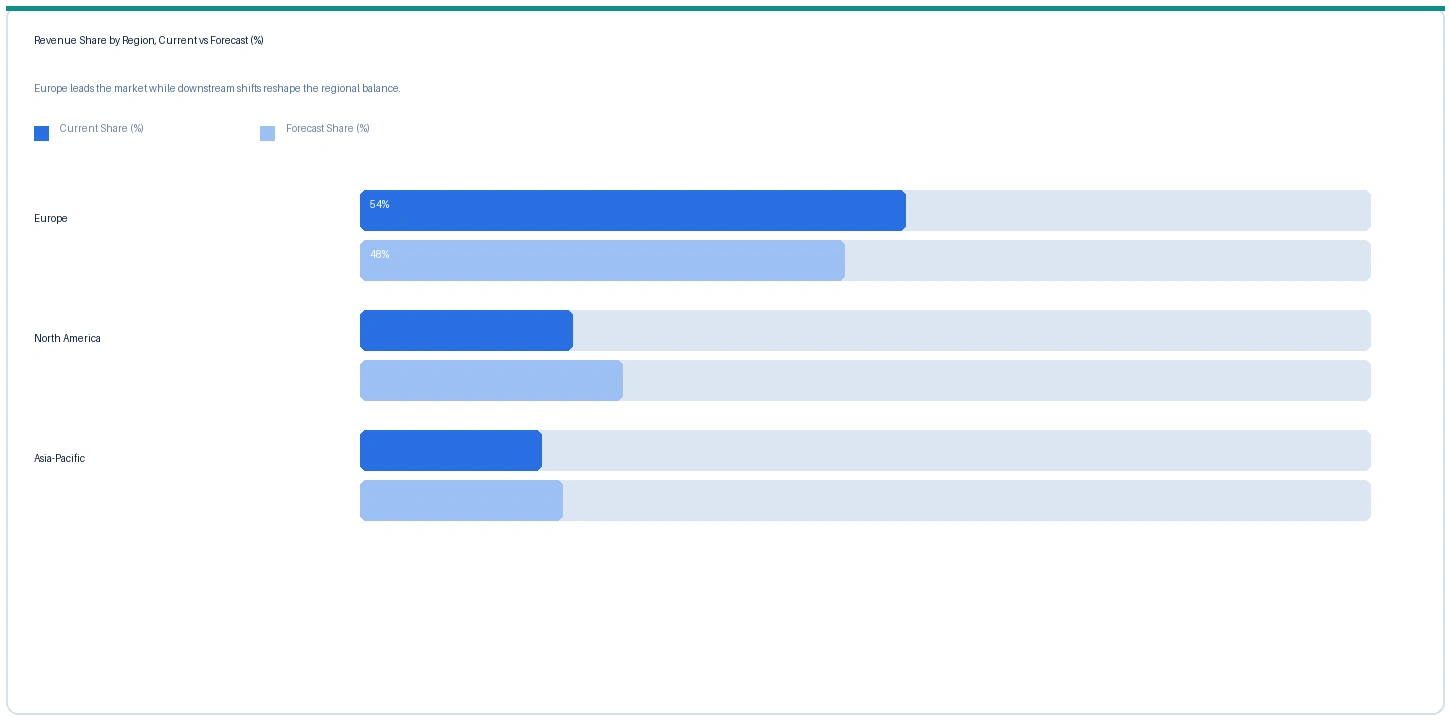

Europe market accounted for largest revenue share over other regional markets in the global 1,5 cyclooctadiene market in 2025. Based on regional analysis, the 1,5 cyclooctadiene market in Europe accounted for largest revenue share in 2025. Evonik Industries at Marl, Germany is the primary commercial-scale producer of catalyst-grade 1,5-COD globally, sourcing butadiene from Ruhr Valley naphtha cracker C4 streams at Marl Chemical Park. European pharmaceutical API manufacturers and CDMOs including Lonza, DOTTIKON Exclusive Synthesis, Siegfried Group, and Bachem represent the most concentrated demand geography for pharmaceutical-grade COD globally, with each CDMO operating multiple active API programmes requiring Ni(cod)2 and Rh(cod) precatalysts. Lonza Q3 2024 disclosure of completing a new COD precatalyst supplier qualification for three API programmes, DOTTIKON Q1 2025 multi-year supply agreement for GMP-compliant piperazine derivative synthesis with a major US pharmaceutical company, and Evonik Q2 2024 COD capacity expansion collectively confirm that European COD supply and demand are both growing, with the capacity expansion responding to demand growth that had already tightened Marl allocation toward existing pharmaceutical accounts.

North America market accounted for second largest revenue share in the global 1,5 cyclooctadiene market in 2025. The market in North America is expected to register the second largest revenue share. North American pharmaceutical API manufacturers including Pfizer, Merck, Bristol Myers Squibb, and AstraZeneca US operations are adopting nickel-catalysed cross-coupling routes confirmed by the BMS JACS March 2025 publication, with Sigma-Aldrich Supelco and Evonik North America distribution as the primary COD supply channels. Shell Chemicals SHOP facility at Geismar, Louisiana consumes polymer-grade COD for industrial nickel catalyst preparation, providing an estimated 800 to 1,200 metric tonnes per year of stable industrial demand. Evonik Q1 2026 disclosed that pharmaceutical-grade COD volumes shipped in 2025 had exceeded the 2024 record, with North American CDMO customers growing faster than European accounts for the first time, reflecting the acceleration of nickel-catalysed API synthesis adoption in US pharmaceutical manufacturing following the BMS disclosure.

Asia-Pacific market is expected to register the fastest revenue growth rate in the global 1,5 cyclooctadiene market during the forecast period. The market in Asia-Pacific is expected to register the fastest revenue growth rate over the forecast period. Japanese pharmaceutical API manufacturers including Takeda, Daiichi Sankyo, and Eisai are integrating transition metal catalysis into API synthesis programmes, sourcing COD-based precatalysts through TCI Chemicals and Nacalai Tesque domestic distribution and from Evonik and Sigma-Aldrich import channels. Chinese pharmaceutical contract manufacturers supplying FDA and EMA cGMP-qualified API volumes are adopting nickel-catalysed synthesis routes and sourcing COD through European-qualified supply channels. The South Korean specialty chemical producer that announced pilot-scale 1,5-COD production in Q2 2025 represents the first potential Asian commercial-scale COD source, with its supplier qualification timeline of 18 to 24 months targeting pharmaceutical customer approval in 2027 to 2028 at the earliest.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| 1,5-COD Catalyst Grade | Europe | USD 18,400/MT | USD 17,100/MT | Rising | Evonik Marl ref |

| 1,5-COD Catalyst Grade | North America | USD 16,800/MT | USD 15,600/MT | Rising | Sigma-Aldrich ref |

| 1,5-COD Polymer Grade | Europe | USD 9,200/MT | USD 8,600/MT | Rising | SHOP process ref |

| 1,5-COD Laboratory Grade | Global | USD 24,600/MT | USD 22,800/MT | Rising | Small pack premium |

| Butadiene (Davy) | Europe | USD 1,440/MT | USD 1,310/MT | Rising | Feedstock reference |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and specialty chemical catalogue and trade publication monitoring. 1,5-COD is not exchange traded and prices vary by purity grade, order volume, and pharmaceutical supplier qualification status.

European catalyst-grade 1,5-COD rose 7.6% from USD 17,100 per metric tonne in Q2 2025 to USD 18,400 per metric tonne in Q2 2026, driven by pharmaceutical API synthesis demand growth from a supply base where the Evonik Marl Q2 2024 capacity expansion is being absorbed by existing qualified pharmaceutical accounts rather than opening price competition from new entrants. North American catalyst-grade prices rose 7.7% from USD 15,600 per metric tonne to USD 16,800 per metric tonne, with above-plan CDMO demand growth confirmed by Evonik Q1 2026 in its specialty intermediates update. Polymer-grade COD prices rose 7.0% in Europe on butadiene feedstock cost elevation of approximately USD 130 per metric tonne against Q2 2025 at Ruhr Valley cracker sourcing levels, with the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 contributing approximately USD 40 to USD 80 per metric tonne of that increase through naphtha and LNG cost elevation at European crackers. Laboratory-grade COD at USD 24,600 per metric tonne equivalent in small pack quantities commands a 33% premium above catalyst-grade bulk pricing, reflecting the fixed handling, documentation, and analytical certification costs per unit that are independent of pack size.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 1,5 cyclooctadiene market, the Hormuz disruption affects production economics through butadiene feedstock cost at Evonik Marl. Naphtha costs at Ruhr Valley crackers supplying C4 butadiene to Marl are elevated by approximately USD 40 to USD 80 per metric tonne above the 2024 baseline from the Hormuz crude oil supply disruption, increasing COD production cost at Marl and supporting the European catalyst-grade COD price increase of approximately 7.6% against Q2 2025. The South Korean pilot-scale COD producer at Ulsan, using a proprietary butadiene cyclooligomerisation process, has access to butadiene from South Korean crackers that are also exposed to GCC naphtha cost elevation from the Hormuz disruption, meaning the Korean entrant faces similar feedstock cost headwinds to Evonik during the Hormuz closure period. Japanese pharmaceutical COD demand routing through TCI Chemicals and Nacalai Tesque domestic distribution is sourced from Evonik Europe imports at elevated freight costs from Gulf of Oman and Suez Canal shipping routes, adding approximately USD 80 to USD 140 per metric tonne to delivered COD cost in Japan relative to pre-Hormuz disruption logistics costs.

Company Insights

The two key dominant companies in the 1,5 cyclooctadiene market are Evonik Industries and Sigma-Aldrich (Merck KGaA), recognised for their leadership in catalyst-grade COD production at industrial and fine chemicals scale respectively, their established pharmaceutical supplier qualification credentials under ICH Q3D frameworks, and their integrated COD-to-catalyst-precursor product offerings extending from COD monomer into downstream Ni(cod)2 and Rh(cod) complex products.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 234.7 Million |

| Market Size 2032 | USD 355.2 Million |

| CAGR | 6.1% |

| Units | Revenue in USD Million |

| Segments Covered | By Grade, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, Switzerland, Ireland, Italy, Japan, South Korea, China, India, Brazil |

| Companies Profiled | Evonik Industries, Sigma-Aldrich (Merck KGaA), TCI Chemicals, Strem Chemicals, Thermo Fisher Scientific, Nippon Zeon, South Korean specialty producer (pilot stage) |

| Key Data Sources | Evonik Industries specialty intermediates division disclosures, FDA ICH Q3D guidance updates January 2025, PhRMA 2024 annual industry NME approval report, Lonza and DOTTIKON CDMO annual reports, BMS JACS March 2025 publication, Shell SHOP process investor disclosures, 14 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 248 |

| Published | Q2 2026 |

| SKU | NXC-PC-006 |

Scope & Methodology

Primary Research

Secondary Research