Market Data

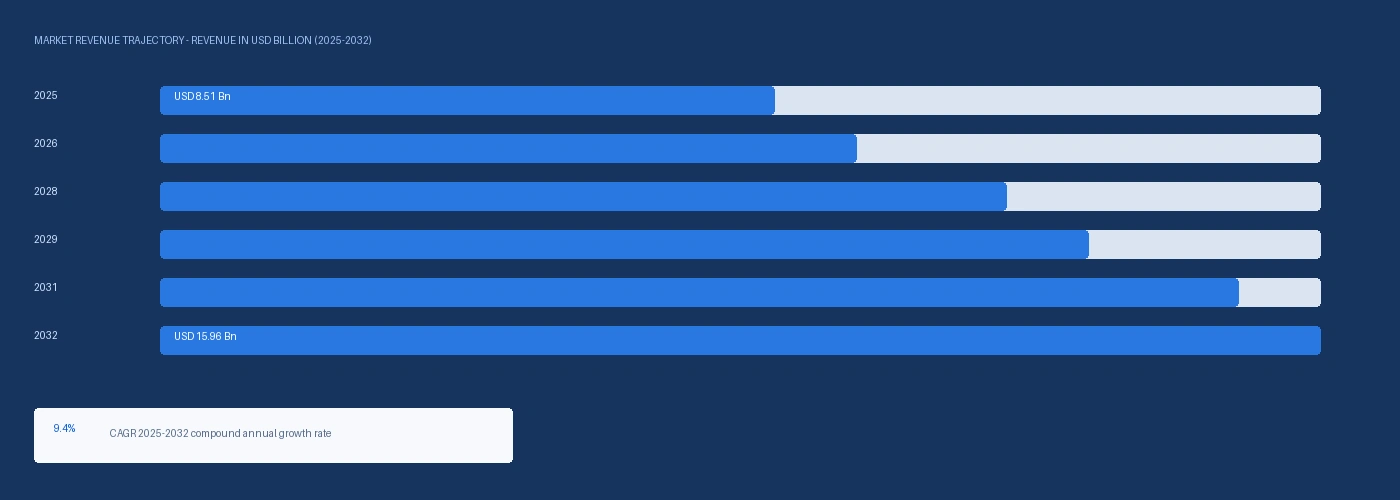

The global 1,4 butanediol market size was USD 8.51 Billion in 2025 and is expected to register a revenue CAGR of 9.4% during the forecast period. Market revenue growth is supported by battery-grade NMP demand from CATL, BYD, and LG Energy Solution battery manufacturing expansion consuming approximately 2 to 4 kilograms of NMP per kilowatt-hour of capacity produced, EV platform PBT resin demand at BASF SE and Lanxess growing at double-digit rates through H1 2025 per investor disclosures, and spandex market recovery pulling PTMEG and THF demand above 2022 to 2023 destocking lows. Global BDO nameplate production capacity reached approximately 4.8 million metric tonnes per year in 2025, with China accounting for approximately 65% of global capacity following a decade of Davy maleic anhydride hydrogenation plant construction at Xinjiang Tianye, Inner Mongolia Pengyuan Chemical, and Shandong Yuhuang Chemical complexes. Chinese domestic BDO consumption was estimated at approximately 2.4 million metric tonnes per year in 2025 per CPCIF data, against nameplate capacity of approximately 3.2 million metric tonnes, creating a structural export surplus of approximately 800,000 metric tonnes per year that has entered Asian spot markets and compressed commodity BDO pricing at or below the cash cost of production at older Western Reppe-route facilities. European producers have responded by redirecting BDO output toward higher-margin NMP, GBL, and engineering-grade THF, with Lanxess confirming in its Q3 2024 earnings that it had fully exited commodity BDO monomer sales from Krefeld-Uerdingen and redirected all output to captive Pocan PBT production. For instance, in Q1 2025, BASF SE, Germany, announced a 12% throughput increase at its Ludwigshafen BDO and gamma-butyrolactone production unit through Davy maleic anhydride hydrogenation catalyst optimisation, responding to growing NMP demand from European battery gigafactory customers including Northvolt and ACC. These are some of the key factors driving revenue growth of the market.

BDO derivative demand is expanding at rates that exceed the headline BDO monomer market pricing signal, because value capture from EV platform demand is occurring at the PBT and NMP derivative product stage rather than at the BDO commodity stage. BASF SE Ultradur PBT automotive segment revenues grew at double-digit rates in H1 2025 while Asian commodity BDO spot prices remained at USD 1,210 per metric tonne in Q2 2025, a divergence that reflects the integrated producer advantage of BASF Verbund internal BDO transfer pricing versus commodity BDO market pricing. NMP battery-grade pricing rose from USD 2,080 per metric tonne in Q2 2025 to USD 2,260 per metric tonne in Q2 2026 as CATL and BYD expanded production at rates outpacing BASF Ludwigshafen NMP debottlenecking output additions. Novamont disclosed an 8% production cost reduction for its Genomatica-licensed bio-based BDO fermentation at its Patrica, Italy facility in its 2024 innovation report, representing progress toward the Novamont cost parity target versus Davy-process BDO by 2028, with ISCC and REDcert2 mass balance certification enabling bio-attributed BDO supply to automotive OEMs with Scope 3 Category 1 reporting requirements.

However, Chinese Davy-process BDO nameplate capacity at approximately 3.2 million metric tonnes per year against domestic consumption of approximately 2.4 million metric tonnes creates approximately 800,000 metric tonnes of structural annual export surplus that is unlikely to be absorbed by domestic demand growth within the forecast period, maintaining downward pricing pressure on commodity BDO monomer that constrains the margin available to Western producers in non-integrated commodity applications. The Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has added approximately USD 40 to USD 70 per metric tonne to European Davy-process BDO production cost through GCC maleic anhydride export disruption, partially offsetting the downward commodity BDO pricing pressure from Chinese export surplus but not reversing it. Scale-up of bio-based BDO from Novamont at approximately USD 2,140 per metric tonne in Europe in Q2 2026 remains at a premium of approximately 25% to 30% above Davy-process BDO that limits adoption outside certified bio-content applications. These factors substantially limit 1,4 butanediol market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

NMP consumption per gigawatt-hour of battery capacity is approximately 2 to 4 kilograms per kilowatt-hour produced, and the IEA confirmed in its Global EV Outlook 2025 that global EV battery manufacturing capacity was on a trajectory to exceed 4,000 gigawatt-hours per year by 2030. CATL disclosed approximately 700 gigawatt-hours of annual battery production capacity in its 2024 annual report, implying NMP consumption of 1.4 to 2.8 million metric tonnes per year from CATL alone at midpoint solvent recovery rates. BASF SE confirmed NMP production capacity debottlenecking at Ludwigshafen adding approximately 15% throughput in Q1 2026 to serve Northvolt, ACC, and Panasonic Kansas gigafactory customers, and simultaneously disclosed in its Q4 2025 earnings that the NMP expansion was drawing additional BDO from internal Verbund supply that would otherwise have routed to THF and PTMEG production, confirming the battery NMP versus PTMEG allocation trade-off at scale. PBT resin demand from EV platform connector and sensor housing applications is growing independently of total automotive production volume, with BASF SE Ultradur double-digit automotive segment revenue growth in H1 2025 and Lanxess Pocan achieving its highest quarterly revenue since 2021 in Q3 2024 on EV platform qualification wins at BMW, Volkswagen Group, and Hyundai Motor. PTMEG demand for spandex and high-performance polyurethane elastomers recovered strongly in 2024 following the 2022 to 2023 destocking cycle, with Dairen Chemical at Ta-lin reporting above-88% PTMEG utilisation in Q4 2024 and commissioning an additional 50,000 metric tonne per year line in Q2 2024. Huafon Group commissioned its Chongqing spandex and PTMEG integrated expansion in November 2024, adding 100,000 metric tonnes per year of spandex capacity consuming an incremental 33,000 to 35,000 metric tonnes per year of PTMEG feedstock. Nike and Adidas both confirmed inventory normalisation in Q4 2024 earnings, signalling that the activewear restocking cycle is pulling spandex and PTMEG volumes above the 2022 to 2023 trough and sustaining above-trend BDO demand through THF and PTMEG derivative channels. Bio-Based BDO Demand Pull from Automotive OEM Scope 3 Reporting Requirements Automotive OEMs with committed Scope 3 Category 1 emissions reduction targets are willing to pay a 20% to 30% premium for bio-attributed BDO enabling them to report reduced embodied carbon in PBT connector components. Novamont at its Patrica, Italy facility produces bio-based BDO from glucose fermentation under Genomatica-licensed technology with ISCC and REDcert2 mass balance certification, enabling bio-attributed BDO supply with the regulatory documentation required for OEM Scope 3 Category 1 accounting. BASF SE commercially qualified a partially bio-attributed Ultradur PBT grade at Schwarzheide in March 2025 incorporating Novamont bio-based BDO content, the first publicly disclosed commercially qualified bio-attributed PBT product for automotive OEM Scope 3 reporting. Chevron Phillips Chemical announced a selective C10 technology development agreement in Q1 2026 targeting on-purpose bio-based monomer routes, and Genomatica confirmed an expanded technology licensing agreement with an Asian chemical producer for bio-based BDO fermentation in March 2025, the first Genomatica licence in Asia.

Chinese BDO nameplate production capacity reached approximately 3.2 million metric tonnes per year in 2025 per CPCIF data, against domestic consumption of approximately 2.4 million metric tonnes, generating a structural export surplus of approximately 800,000 metric tonnes per year at full utilisation. Xinjiang Tianye, operating one of the world's largest single-site BDO complexes with captive coal-based maleic anhydride integration at Shihezi, Xinjiang, produces BDO at a cost floor that remains cashflow positive at Asian spot prices of USD 1,340 per metric tonne in Q2 2026, below the cash cost of production at older European and North American Reppe-route facilities. INEOS disclosed in Q1 2026 that it was evaluating conversion of a portion of its Gladbeck, Germany BDO Reppe-process capacity to Davy maleic anhydride hydrogenation configuration, the first publicly disclosed European Reppe-to-Davy conversion evaluation, as the persistent cost disadvantage of acetylene-based production accelerates Western capacity rationalisation. The US-Iran conflict and the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 has elevated maleic anhydride feedstock costs for European Davy-process BDO plants, adding approximately USD 40 to USD 70 per metric tonne to European BDO production cost and compressing margins at non-integrated European producers caught between elevated feedstock costs and Chinese export price competition. These factors substantially limit 1,4 butanediol market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Production Route | Reppe Process, Davy Process, Mitsubishi Process, Propylene Oxide Route, Bio-Based | Reppe Process |

| Application | PBT, PTMEG and Spandex, GBL, THF, NMP | PBT |

| End Use | Automotive, Electronics and Battery, Textiles, Pharmaceuticals, Industrial Solvents | Automotive |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Davy Process segment is expected to account for a significantly large revenue share in the global 1,4 butanediol market during the forecast period.

This report evaluates production route across Reppe Process, Davy Process, Mitsubishi Process, Propylene Oxide Route, Bio-Based for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across PBT, PTMEG and Spandex, GBL, THF, NMP for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Automotive, Electronics and Battery, Textiles, Pharmaceuticals, Industrial Solvents for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

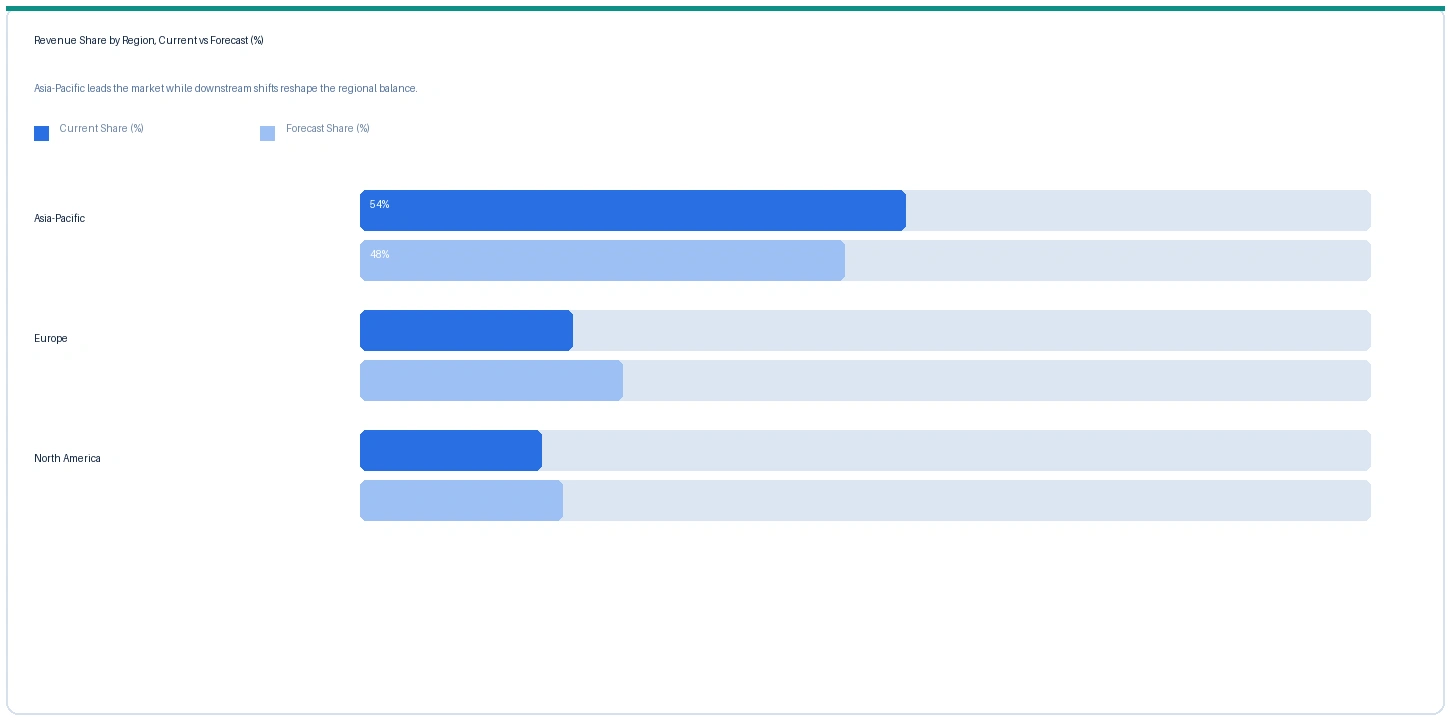

Asia-Pacific market accounted for largest revenue share over other regional markets in the global 1,4 butanediol market in 2025. Based on regional analysis, the 1,4 butanediol market in Asia-Pacific accounted for largest revenue share in 2025. China accounts for approximately 65% of global BDO nameplate capacity at approximately 3.2 million metric tonnes per year per CPCIF data, with Xinjiang Tianye at Shihezi, Inner Mongolia Pengyuan at Ordos, and Shandong Yuhuang among the largest single-site complexes. Chinese domestic BDO consumption of approximately 2.4 million metric tonnes per year is distributed across integrated PBT, PTMEG, GBL, THF, and NMP production at the same sites, with CATL and BYD as the dominant downstream NMP consumers generating above-1.4 million metric tonnes per year of NMP demand from CATL alone at reported 700 gigawatt-hour annual battery capacity. Japan and South Korea contribute an estimated 8% to 12% of global BDO production through Mitsubishi Chemical and Dairen Chemical Ta-lin facility operations.

The market in Europe is expected to register the second largest revenue share in the global 1,4 butanediol market. BASF SE at Ludwigshafen and Schwarzheide and INEOS at Gladbeck operate the primary European BDO production facilities, with Verbund integration at BASF providing a cost and logistics advantage for NMP, GBL, and PBT downstream derivative production from internal BDO feedstock. European BDO contract pricing was indicatively USD 1,680 per metric tonne in Q2 2026, a premium of approximately USD 340 per metric tonne above Asian spot, reflecting the combination of elevated maleic anhydride feedstock costs from the Strait of Hormuz disruption and the portfolio shift toward higher-margin derivatives that has reduced European BDO monomer spot market availability. Northvolt, ACC, and SVOLT Europe gigafactory NMP demand is expected to add approximately 80,000 to 120,000 metric tonnes per year of NMP consumption to European BDO derivative demand by 2028.

North America market is expected to register steady revenue growth in the global 1,4 butanediol market during the forecast period. The market in North America is anchored in BDO derivative consumption with Celanese at Bishop, Texas and BASF North America at Geismar, Louisiana as the primary US BDO producers. North American BDO demand is driven by PBT resin in automotive and electronics applications, pharmaceutical NMP and GBL solvent demand confirmed by American Chemistry Council at above-3% annual growth in 2024, and THF solvent consumption in pharmaceutical synthesis and polyurethane coating formulations. Inflation Reduction Act battery manufacturing tax credits supporting Panasonic Kansas, Toyota Battery Manufacturing North Carolina, and Stellantis-Samsung SDI Indiana will generate estimated 80,000 to 120,000 metric tonnes per year of additional NMP demand as those plants reach electrode coating production between 2026 and 2028.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| BDO Davy Process | Asia-Pacific | USD 1,340/MT | USD 1,200/MT | Rising | Chinese export ref |

| BDO Davy Process | Europe | USD 1,680/MT | USD 1,510/MT | Rising | BASF / INEOS ref |

| BDO Reppe Process | Europe | USD 1,820/MT | USD 1,650/MT | Rising | Legacy prod. premium |

| Bio-Based BDO | Europe | USD 2,140/MT | USD 1,980/MT | Rising | Novamont / Genomatica |

| BDO (industrial) | North America | USD 1,590/MT | USD 1,430/MT | Rising | Celanese / BASF NA |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and trade publication monitoring. BDO is traded under monthly and quarterly term contracts referenced against regional spot assessments. Prices vary by production route, purity grade, contract volume, and regional supply-demand balance.

Asian commodity BDO Davy process prices rose approximately 11.7% from USD 1,200 per metric tonne in Q2 2025 to USD 1,340 per metric tonne in Q2 2026, driven by NMP and PBT derivative demand pulling BDO production toward higher-margin internal derivative consumption at integrated Chinese complexes and reducing the volume available to external commodity buyers. European Davy process BDO prices rose approximately 11.3% from USD 1,510 per metric tonne in Q2 2025 to USD 1,680 per metric tonne in Q2 2026, reflecting the maleic anhydride feedstock cost increase of approximately USD 40 to USD 70 per metric tonne from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 and the tighter European BDO monomer balance from derivative portfolio shift. The Europe-Asia BDO price differential widened from approximately USD 310 per metric tonne in Q2 2025 to approximately USD 340 per metric tonne in Q2 2026, reflecting diverging feedstock cost trajectories. Bio-based BDO at USD 2,140 per metric tonne in Europe maintains a 27% premium above European Davy-process BDO, a premium that automotive OEMs with Scope 3 Category 1 commitments are absorbing to enable bio-attributed PBT component documentation.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the 1,4 butanediol market the Hormuz disruption operates through the maleic anhydride feedstock chain that underpins Davy-process BDO production in Europe. Saudi Arabia and UAE export maleic anhydride from benzene oxidation at GCC petrochemical complexes to European BDO producers including BASF and INEOS, and the Hormuz closure has partially disrupted these export flows, reducing European maleic anhydride availability and adding approximately USD 40 to USD 70 per metric tonne to European BDO production cost in Q2 2026. The Europe-Asia BDO price differential has widened from approximately USD 310 per metric tonne in Q2 2025 to approximately USD 340 per metric tonne in Q2 2026, partially reflecting this Hormuz-driven European feedstock cost elevation. Chinese BDO producers with captive domestic coal-based or natural gas-based maleic anhydride at Xinjiang Tianye and Inner Mongolia Pengyuan are partially insulated from the GCC maleic anhydride disruption, further entrenching their structural cost advantage over European non-integrated producers during the Hormuz closure period and accelerating European Reppe-to-Davy conversion evaluations at INEOS.

Company Insights

The two key dominant companies in the 1,4 butanediol market are BASF SE and Xinjiang Tianye Group, recognised for their positions as the largest integrated BDO producers in the Western and Asian markets respectively, their contrasting production route strategies defining the competitive dynamic between European Verbund-integrated Davy and Reppe production and Chinese captive-integrated large-scale Davy complexes, and their leadership in BDO derivative value chain capture.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 8.51 Billion |

| Market Size 2032 | USD 15.96 Billion |

| CAGR | 9.4% |

| Units | Revenue in USD Billion |

| Segments Covered | By Production Route, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Canada, Germany, UK, Italy, China, Japan, South Korea, Taiwan, India, Brazil, Saudi Arabia |

| Companies Profiled | BASF SE, Xinjiang Tianye, INEOS, Celanese, Dairen Chemical, Inner Mongolia Pengyuan, Shandong Yuhuang, Novamont, ISP, Mitsubishi Chemical, Ashland, Genomatica, Nan Ya Plastics |

| Key Data Sources | BASF SE and Lanxess investor presentations, IEA Global EV Outlook 2025, OICA vehicle production data, CPCIF Chinese BDO production statistics, American Chemistry Council, CATL annual report, Novamont innovation disclosures, 18 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 272 |

| Published | Q2 2026 |

| SKU | NXC-PC-004 |

Scope & Methodology

Primary Research

Secondary Research