Market Data

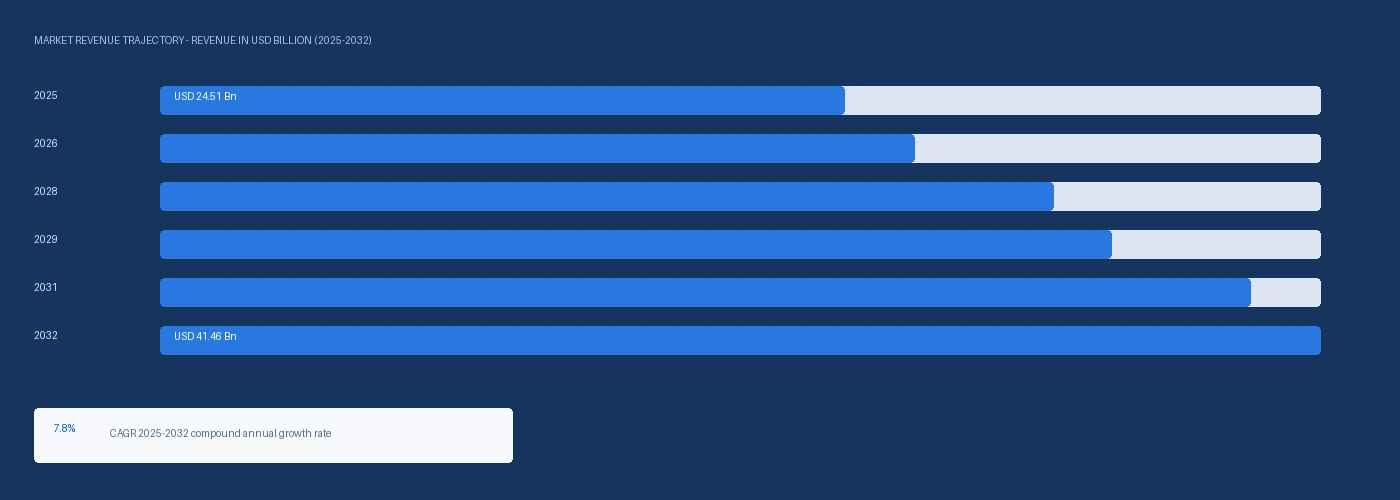

The global 1,4-butanediol, polytetramethylene ether glycol and spandex market size was USD 24.51 Billion in 2025 and is expected to register a revenue CAGR of 7.8% during the forecast period. Market revenue growth is supported by the completion of the 2022 to 2023 activewear and athleisure destocking cycle driving PTMEG and spandex offtake recovery, Chinese spandex nameplate capacity reaching approximately 1.2 million metric tonnes per year in 2025 per China Chemical Fibre Association data representing approximately 67% of global capacity, and rising PTMEG feedstock prices from the BDO supply allocation shift toward battery-grade NMP at integrated European producers. Huafon Group commissioned its latest integrated spandex and PTMEG capacity expansion at Chongqing in November 2024, adding 100,000 metric tonnes per year of spandex with corresponding PTMEG consumption, bringing total Huafon estimated capacity above 500,000 metric tonnes per year and reinforcing its position as the world's largest spandex producer. Dairen Chemical Corporation confirmed above-88% PTMEG utilisation at its Ta-lin, Taiwan facility in Q4 2024 and commissioned an additional 50,000 metric tonne per year PTMEG line in Q2 2024, with the line operating above 85% utilisation within six months on spandex market recovery demand from Taiwanese and South Korean fibre producers. Nike and Adidas both confirmed North American and European inventory normalisation in their Q4 2024 earnings, signalling that the destocking cycle had completed and that restocking demand was pulling spandex procurement above trough levels. BASF SE disclosed in its Q4 2025 earnings that NMP production expansion at Ludwigshafen was drawing additional BDO from internal Verbund supply that would otherwise have routed to THF and PTMEG production, the first explicit disclosure of a battery NMP versus PTMEG allocation trade-off at an integrated European BDO producer and a direct upstream tightening signal for European PTMEG buyers. For instance, in November 2024, Huafon Group, China, commissioned its latest integrated spandex and PTMEG capacity expansion at its Chongqing facility, adding 100,000 metric tonnes per year of spandex production capacity and corresponding PTMEG consumption, the largest single spandex capacity addition by any producer in 2024 and confirming Huafon as the reference price setter for standard spandex grades in Asian markets. These are some of the key factors driving revenue growth of the market.

PTMEG 2000 molecular weight pricing in Asia-Pacific rose from USD 2,620 per metric tonne in Q2 2025 to USD 2,840 per metric tonne in Q2 2026, a 8.4% increase driven by Dairen Chemical above-88% utilisation, Huafon Chongqing expansion consuming an incremental 33,000 to 35,000 metric tonnes per year of PTMEG feedstock, and the BASF Ludwigshafen BDO allocation shift toward NMP tightening European PTMEG supply availability. Standard 20-denier spandex from Chinese producers was indicatively priced at USD 4,380 per metric tonne in Asia-Pacific in Q2 2026 against USD 4,110 per metric tonne in Q2 2025, a 6.6% increase driven by elevated PTMEG input costs partially passed through in contract pricing despite competitive pressure from Chinese overcapacity running at approximately 72% average utilisation per China Chemical Fibre Association 2024 data. Chinese spandex capacity of approximately 1.2 million metric tonnes per year against estimated domestic consumption of approximately 700,000 to 750,000 metric tonnes generates a structural export surplus directed at Southeast Asian, South Asian, and European markets at prices that have compressed margins for Hyosung TNC in South Korea and non-integrated producers unable to match the integrated PTMEG-spandex cost structure of Huafon, Yantai Tayho, and Zhejiang Huahai.

However, Chinese spandex nameplate capacity of approximately 1.2 million metric tonnes per year at approximately 72% average utilisation generates a structural export surplus that compresses standard grade spandex pricing for non-integrated producers globally, with Hyosung TNC disclosing margin compression in its standard spandex grades in its 2024 annual report despite geographic diversification across Vietnam, China, Turkey, and Brazil operations. PTMEG supply is simultaneously tightening relative to spandex capacity growth because PTMEG polymerisation capital requirements and technical barriers are higher than spandex spinning, meaning Chinese spandex capacity has grown faster than Chinese PTMEG supply can grow, and non-integrated Chinese spandex producers buying PTMEG externally face rising input costs in a market with compressed output pricing. These factors substantially limit BDO, PTMEG and spandex market growth over the forecast period.

Industry Trends & Market Dynamics

Drivers, Restraints and Market Dynamics

Global spandex demand returned to volume growth in 2024 following two years of supply chain destocking that had depressed PTMEG offtake independently of underlying consumer demand. Nike disclosed in its Q2 fiscal 2025 earnings that North American wholesale inventory had normalised to pre-destocking levels for the first time since Q3 2022, and Adidas confirmed in its Q4 2024 earnings that European retail sell-through had exceeded internal forecasts, both signals that restocking demand was pulling through spandex supply chains in 2025. Hyosung Corporation disclosed in its 2024 annual report that its Creora spandex brand had experienced above-plan volume recovery in H2 2024, particularly in European premium activewear and medical compression garment accounts. Medical textile applications consume spandex at concentrations of 15% to 30% by weight in compression garments, surgical hosiery, orthopaedic supports, and wound care dressings, with the European Compression Hosiery Association reporting approximately 6% expansion in European medical compression garment production in 2024 driven by ageing population demand independent of activewear market cycles. Medical-grade Invista LYCRA and Hyosung Creora commands a price premium of approximately 15% to 22% over standard activewear grades at USD 6,920 per metric tonne in European markets in Q2 2026. PTMEG-based polyurethane elastomers for automotive fuel hose, power transmission belts, mining screen panels, and hydraulic seals represent approximately 20% to 25% of global PTMEG consumption at 1000 to 2000 molecular weight grades, independent of spandex market cycles. BASF Elastollan and Covestro Desmopan are among the primary PTMEG-based thermoplastic polyurethane grades specified in automotive under-bonnet fluid handling and industrial applications, with OEM qualification requirements at Ford, GM, and BMW creating multi-year supply stability for PTMEG feedstock contracts backing these programmes. BDO Allocation Shift Toward NMP Creating PTMEG Supply Tightening BASF SE disclosed in its Q4 2025 earnings that NMP production expansion at Ludwigshafen was drawing additional BDO from internal Verbund supply that would otherwise have routed to THF and PTMEG production, the first explicit public disclosure of an allocation trade-off between battery NMP demand and PTMEG feedstock supply at an integrated European BDO producer. This allocation dynamic is structural rather than cyclical because battery gigafactory NMP demand from Northvolt, ACC, Panasonic Kansas, and CATL European plants is growing on a committed multi-decade manufacturing investment timeline, whereas PTMEG demand from spandex recovery is a cyclical rebound. Each tonne of BDO that BASF routes to NMP synthesis for battery customers is unavailable for THF and PTMEG production for European spandex and polyurethane elastomer customers. European PTMEG buyers sourcing from BASF Ludwigshafen are therefore facing a structural supply tightening that is driven by battery sector demand growth, not by PTMEG demand decline, and should be building this into medium-term supply planning.

Chinese spandex nameplate capacity exceeded 1.2 million metric tonnes per year in 2025 against estimated domestic consumption of approximately 700,000 to 750,000 metric tonnes per year per China Chemical Fibre Association data, generating a structural export surplus at approximately 72% average utilisation that has been directed at Southeast Asian, South Asian, and European markets at prices below the variable cost of production for non-integrated European and Korean spandex producers. Hyosung Corporation disclosed margin compression in standard spandex grades in its 2024 annual report despite geographic diversification across six production countries. The margin compression at spandex producers reduces their willingness to pay for PTMEG at current market pricing, creating a squeeze in the middle of the value chain between rising BDO-THF-PTMEG input costs and compressed spandex output pricing. Dairen Chemical Ta-lin operating above 88% PTMEG utilisation and the Huafon Chongqing expansion adding 33,000 to 35,000 metric tonnes per year of PTMEG demand simultaneously mean that PTMEG supply is tightening at the same time that integrated Chinese spandex producers are adding capacity, benefiting the integrated PTMEG-spandex producers and disadvantaging non-integrated spandex spinners who must absorb rising PTMEG costs in a compressed margin environment. The US-Iran conflict and Strait of Hormuz supply disruption confirmed by the IMF in March 2026 is adding maleic anhydride feedstock cost pressure at European Davy-process BDO producers of approximately USD 40 to USD 70 per metric tonne, elevating PTMEG production cost at European sites and widening the Europe-Asia PTMEG price differential from approximately USD 260 per metric tonne in Q2 2025 to approximately USD 400 per metric tonne in Q2 2026, creating additional competitive pressure for European-origin PTMEG in the global spandex feedstock market. These factors substantially limit BDO, PTMEG and spandex market growth over the forecast period.

Segmentation

| Segmentation Basis | Sub-segments | Leading Segment |

|---|---|---|

| Product | BDO, PTMEG, Spandex Fibre | BDO |

| Application | Spandex and Elastic Fibre, Polyurethane Elastomers, Coatings and Adhesives, THF Solvent, Engineering Plastics | Spandex and Elastic Fibre |

| End Use | Textiles and Apparel, Automotive, Footwear, Medical, Industrial | Textiles and Apparel |

| Region | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa | North America |

Spandex Fibre segment is expected to account for a significantly large revenue share in the global BDO, PTMEG and spandex market during the forecast period.

This report evaluates product across BDO, PTMEG, Spandex Fibre for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates application across Spandex and Elastic Fibre, Polyurethane Elastomers, Coatings and Adhesives, THF Solvent, Engineering Plastics for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates end use across Textiles and Apparel, Automotive, Footwear, Medical, Industrial for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

This report evaluates region across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa for glycols & polyols, with segment-level positioning, share outlook, and downstream demand context imported directly from the research document.

Regional Insights

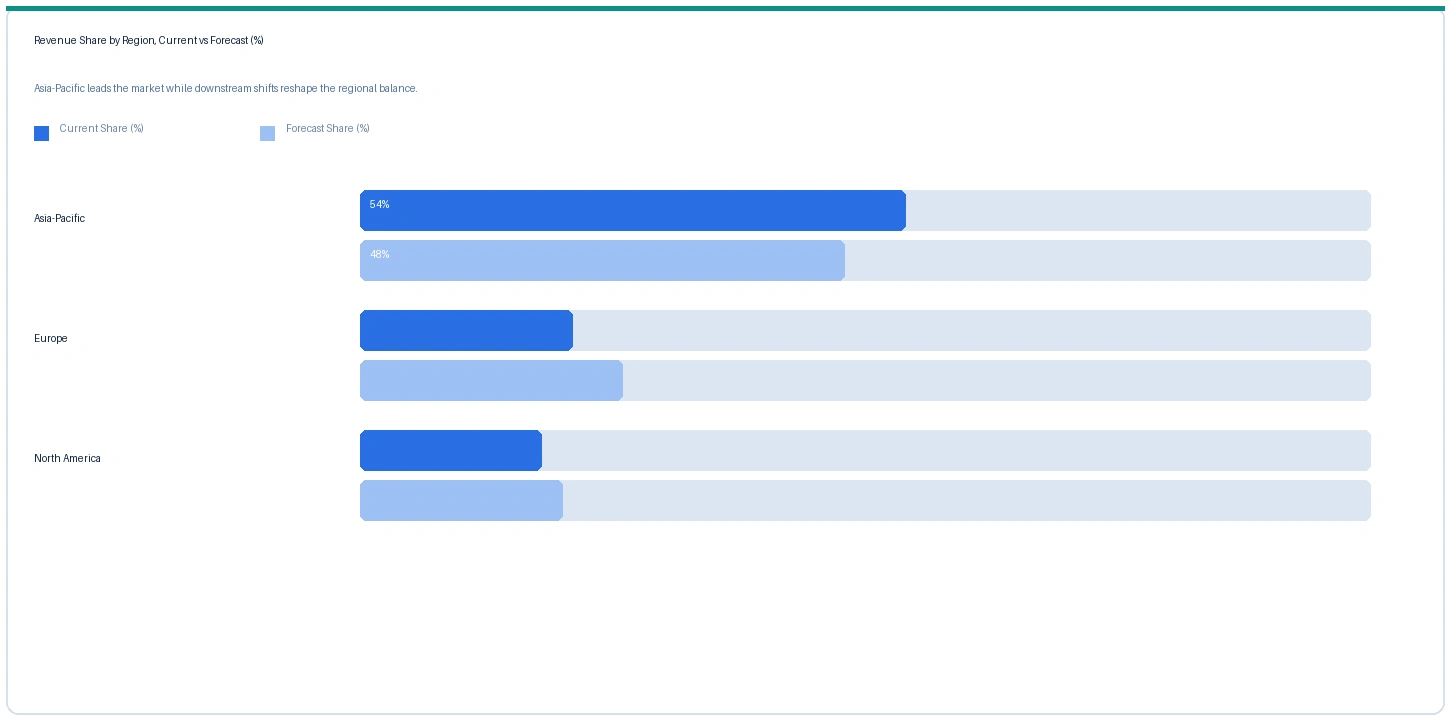

Asia-Pacific market accounted for largest revenue share over other regional markets in the global BDO, PTMEG and spandex market in 2025. Based on regional analysis, the BDO, PTMEG and spandex market in Asia-Pacific accounted for largest revenue share in 2025. China accounts for approximately 67% of global spandex nameplate capacity at approximately 1.2 million metric tonnes per year, with Huafon Group above 500,000 metric tonnes per year, Yantai Tayho, and Zhejiang Huahai among the largest integrated PTMEG-spandex producers sourcing BDO from domestic Chinese suppliers. The CPCIF reported combined Chinese BDO, PTMEG, and spandex production accounted for approximately 58% of global value chain output in 2024. Dairen Chemical at Ta-lin, Taiwan with estimated total PTMEG capacity of approximately 300,000 metric tonnes per year following the Q2 2024 expansion, and Nan Ya Plastics are the primary Taiwanese PTMEG producers supplying spandex producers in Taiwan, South Korea, and export markets.

Europe market accounted for second largest revenue share in the global BDO, PTMEG and spandex market in 2025. The market in Europe is expected to register the second largest revenue share. European demand is anchored in premium spandex applications including medical compression garments at European Compression Hosiery Association confirmed 6% 2024 production growth, premium activewear at USD 6,920 per metric tonne Invista LYCRA reference pricing, and technical textiles where Invista and Hyosung Creora hold specification-based pricing that insulates European spandex consuming markets from Chinese commodity grade pressure. BASF SE at Ludwigshafen and Dairen Chemical through European distribution supply PTMEG to European polyurethane elastomer manufacturers including BASF Elastollan and Covestro Desmopan programmes. The BASF Q4 2025 earnings disclosure that NMP expansion was drawing BDO from the internal PTMEG production chain is a direct supply tightening signal for European PTMEG buyers sourcing from Ludwigshafen.

North America market is expected to register steady revenue growth in the global BDO, PTMEG and spandex market during the forecast period. The market in North America is anchored by Invista supplying LYCRA from its integrated US production at Victoria, Texas and by Hyosung supplying Creora from its Vietnam and Brazil facilities to US apparel manufacturers. The US athletic footwear and apparel market, where Nike and Lululemon represent the primary premium spandex demand anchors, returned to restocking demand pull in 2025 following inventory normalisation confirmed in Q4 2024 earnings. American Chemistry Council data confirms the US as the second largest PTMEG-consuming market globally after China, with Invista Victoria PTMEG production supplemented by Dairen Chemical and BASF imports under term agreements.

Indicative Price Trends

Price Tracker

| Product / Grade | Region | Current | Previous | Direction | Note |

|---|---|---|---|---|---|

| BDO (Davy, Asian spot) | Asia-Pacific | USD 1,340/MT | USD 1,200/MT | Rising | THF / PTMEG feedstock |

| PTMEG 2000 MW | Asia-Pacific | USD 2,840/MT | USD 2,620/MT | Rising | Spandex grade |

| PTMEG 1000 MW | Europe | USD 3,240/MT | USD 2,840/MT | Rising | PU elastomer grade |

| Spandex 20D (standard) | Asia-Pacific | USD 4,380/MT | USD 4,110/MT | Rising | Chinese producer ref |

| Spandex 20D (premium) | Europe | USD 6,920/MT | USD 6,540/MT | Stable | Invista LYCRA ref |

The following indicative price data is compiled from Nexchem Intelligence primary contacts, producer commercial disclosures, and trade publication monitoring. BDO, PTMEG, and spandex are traded under monthly and quarterly term contracts. Prices vary by grade, molecular weight for PTMEG, denier and elasticity specification for spandex, and regional supply-demand balance.

PTMEG 2000 molecular weight in Asia-Pacific rose 8.4% from USD 2,620 per metric tonne in Q2 2025 to USD 2,840 per metric tonne in Q2 2026, driven by Dairen Chemical above-88% utilisation, Huafon Chongqing adding 33,000 to 35,000 metric tonnes per year of PTMEG demand, and BASF Ludwigshafen BDO allocation shift toward NMP tightening European supply. European PTMEG 1000 molecular weight for polyurethane elastomers rose 14.1% from USD 2,840 per metric tonne in Q2 2025 to USD 3,240 per metric tonne in Q2 2026, a steeper increase than Asian grades reflecting the combination of European BDO maleic anhydride feedstock cost elevation of approximately USD 40 to USD 70 per metric tonne from the Strait of Hormuz supply disruption confirmed by the IMF in March 2026 and the BDO allocation shift at BASF Ludwigshafen. Standard 20-denier spandex from Chinese producers rose 6.6% despite approximately 72% average Chinese capacity utilisation, confirming that PTMEG input cost increases are being partially passed through to spandex buyers even at current levels of overcapacity. Premium Invista LYCRA pricing is stable at USD 6,920 per metric tonne, reflecting the specification-based pricing structure that insulates premium medical and high-performance activewear grades from commodity spandex pricing dynamics.

Strategic Developments

Analyst Review

The IMF confirmed in March 2026 that the closure of the Strait of Hormuz had disrupted approximately 20% of global oil and seaborne LNG flows following escalation of the US-Iran conflict. For the BDO-PTMEG-spandex value chain the Hormuz disruption operates through maleic anhydride feedstock supply for Davy-process BDO producers in Europe, elevating European BDO production cost by approximately USD 40 to USD 70 per metric tonne and flowing through to PTMEG pricing in European markets. European PTMEG 1000 molecular weight rose 14.1% against Q2 2025 to USD 3,240 per metric tonne in Q2 2026, a larger increase than Asian PTMEG reflecting the combined effect of Hormuz maleic anhydride tightening and the BASF Ludwigshafen BDO allocation shift toward battery NMP. The Europe-Asia PTMEG 1000 molecular weight price differential has widened from approximately USD 260 per metric tonne in Q2 2025 to approximately USD 400 per metric tonne in Q2 2026. Freight cost elevation for PTMEG and spandex trade flows transiting Gulf of Oman and Suez Canal routes adds to delivered cost in Middle Eastern and South Asian markets, compressing the delivered cost advantage of Asian-origin product in GCC textile markets.

Company Insights

The two key dominant companies in the BDO, PTMEG and spandex market are Huafon Group and Invista, recognised for their vertically integrated positions from PTMEG production through spandex fibre manufacturing, their contrasting market positions as the scale-driven Chinese integrated leader and the brand-premium Western integrated leader, and their established supply relationships with global activewear, medical textile, and technical fibre brands.

Scope of Research

| Base Year | 2025 |

| Forecast Period | 2026 to 2032 |

| Market Size 2025 | USD 24.51 Billion |

| Market Size 2032 | USD 41.46 Billion |

| CAGR | 7.8% |

| Units | Revenue in USD Billion |

| Segments Covered | By Product, By Application, By End Use, By Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Countries Covered | US, Germany, Netherlands, Italy, France, China, Japan, South Korea, Taiwan, India, Brazil, Turkey |

| Companies Profiled | Huafon Group, Invista, Hyosung TNC, Toray Industries, Dairen Chemical, Yantai Tayho, Nan Ya Plastics, BASF SE, SK Chemicals, Asahi Kasei, Radici Group |

| Key Data Sources | China Chemical Fibre Association spandex capacity data, Invista and Hyosung annual reports, BASF SE Q4 2025 earnings disclosures, IEA battery NMP demand analysis, American Chemistry Council PTMEG data, European Compression Hosiery Association data, Nike and Adidas earnings inventory disclosures, 19 primary expert interviews |

| Format | PDF + Excel Data File |

| Customisation | Available -- [email protected] |

| Pages | 284 |

| Published | Q2 2026 |

| SKU | NXC-PC-005 |

Scope & Methodology

Primary Research

Secondary Research